|

市場調查報告書

商品編碼

2043868

柔軟性環氧樹脂:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Flexible Epoxy Resin - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

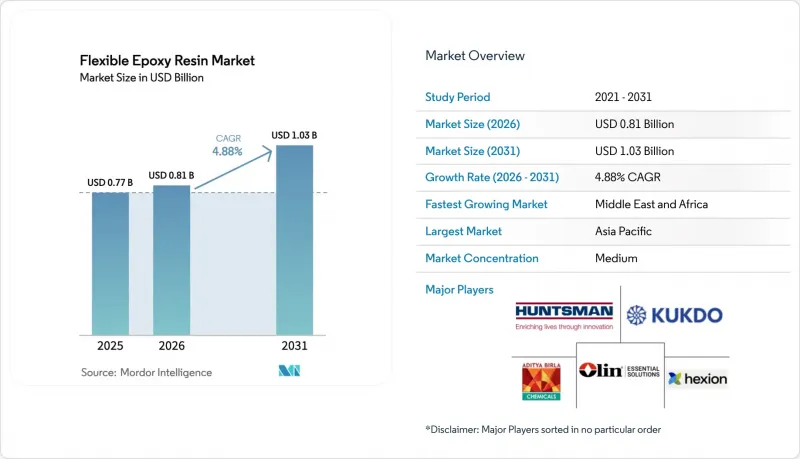

預計柔軟性環氧樹脂市場將從 2025 年的 7.7 億美元和 2026 年的 8.1 億美元成長到 2031 年的 10.3 億美元,2026 年至 2031 年的年複合成長率(CAGR)為 4.88%。

該產業曾一度以通用建築黏合劑為主導,如今正將重心轉向高附加價值應用領域。這些應用包括電動車的電力電子裝置、風力發電機葉片維修以及用於穿戴式裝置的軟性印刷電路板。橡膠改質黏合劑在結構複合材料領域仍佔據主導地位,但胺甲酸乙酯改質化學品的使用量正在顯著成長,尤其是在電子封裝應用領域。亞太地區憑藉其蓬勃發展的電子和建築業,已成為主要的需求中心。然而,中東和非洲地區的成長速度最快,這主要得益於沙烏地阿拉伯雄心勃勃的基礎設施發展計畫和開創性的NEOM計畫。儘管如此,由於環氧氯丙烷價格波動以及雙酚A縮水甘油醚監管力度加大,該產業的盈利面臨挑戰。在這種不斷變化的環境中,垂直整合型企業和生物基創新企業憑藉其在原料供應和合規性挑戰方面的專業知識,佔據了有利地位。

全球柔軟性環氧樹脂市場趨勢及洞察

建築和基礎設施支出激增

亞太、中東和北美地區的基礎設施預算正推動對軟性環氧樹脂黏合劑和塗料的穩定需求。 2024年,中國為鐵路和地鐵擴建計畫撥出了大量預算,凸顯了對吸振環氧樹脂接頭的需求。同時,印度的國家基礎設施計畫重點關注公路和城市交通,預計2025年將投入大量資金。這項措施刺激了對鋼筋防腐蝕環氧樹脂塗料的需求,尤其是在沿海高架公路。過去五年,美國在橋樑維修投入巨資,並傾向於使用裂縫灌漿環氧樹脂,這種材料可將橋樑封閉時間縮短一半。沙烏地阿拉伯的「2030願景」發展計畫(由NEOM主導)強調了低VOC柔軟性環氧樹脂塗料的重要性,以確保其在沙漠酷熱環境下的耐久性。然而,儘管這些項目推動了強勁的需求,但必須認知到,資金籌措延遲和外匯波動可能會使黏合劑的採購週期延長至多一年。

家用電子電器和電動汽車電力電子產品的電氣化

目前,所有電池式電動車(BEV)都配備了數千個積層陶瓷電容,這些電容器受益於軟性環氧樹脂端子。這一數量遠超傳統電池式電動車型。這些端子確保焊點在-40°C至+150°C的溫度範圍內保持耐久性。近年來,全球純電動車產量大幅成長,預計這一趨勢也將持續。因此,灌封和封裝的使用量也隨之增加。在家用電子電器領域,胺甲酸乙酯改質環氧樹脂的應用正在折疊式智慧型手機和健康監測穿戴裝置中不斷擴展。這些特殊環氧樹脂以其高延伸率而聞名,旨在通過嚴格的彎曲測試。一個值得關注的產業趨勢是,日本和韓國企業正在大力投資先進封裝技術,目標是在2020年代末完成相關研發。這些尖端封裝的關鍵組件是低模量環氧樹脂底部填充材料。預計電子產業的這些趨勢將推動該細分市場在 2026 年至 2031 年的預測期內實現 6.31% 的複合年成長率。

環氧氯丙烷和雙酚A原料價格的波動

近年來,隨著中國生產商大幅擴大產能,環氧氯丙烷和雙酚A的現貨價格出現顯著波動。這兩種化學品在生產成本中佔很大比例。因此,受年度合約約束的歐美配方生產商一直飽受價格不穩定的困擾。丙烯原料價格的飆升導致歐洲環氧氯丙烷價格暴漲,毛利率大幅下降。如果中小型加工商無法調整黏合劑供應合約的價格,且缺乏避險策略或後向整合,則可能面臨季度虧損的風險。

細分市場分析

2025年,採用雙相結構的橡膠改質環氧樹脂銷售量佔比達41.38%,展現出更優異的斷裂韌性。這項改進在風力渦輪機葉片和工業黏合劑等應用領域至關重要。預計在2026年至2031年的預測期內,橡膠改質柔軟性環氧樹脂市場將與整體市場複合年成長率保持一致,主要受建築和複合材料行業需求的驅動。胺甲酸乙酯改質化學品預計將以6.24%的複合年成長率(2026-2031年)成長,這主要得益於其在電子封裝領域的應用。在電子封裝領域,高延伸率和低於冰點的玻璃化轉變溫度等特性對於保護焊點至關重要。受此趨勢影響,2024年推出的產品彈性模量顯著降低,凸顯了材料性能向低應力下晶片附件的轉變趨勢。同時,儘管市佔率較小,但二聚酸基產品主要集中在專業船舶塗料領域,強調防水性和生物含量。

市場區隔基於成本績效的微妙平衡。結構性黏著劑使用者往往更傾向於橡膠改質產品。而晶片製造商則深知現場故障可能帶來的保固責任,即使聚氨酯價格更高,他們也會選擇胺甲酸乙酯。柔軟性環氧樹脂市場的主要參與者巧妙地應對了這種情況,在汽車電子領域推廣胺甲酸乙酯應用的同時,也保持了橡膠基產品在建築領域的市場佔有率。腰果衍生的二聚體酸樹脂已在離岸風力發電的基礎結構中佔據了一席之地。然而,由於碳定價政策推動了早期材料替代,預計這一細分市場的成長速度將會放緩,從而刺激需求成長。

區域分析

2025年,亞太地區佔了47.36%的銷售佔有率,佔據主導地位,但此後成長放緩。成長放緩歸因於中國建築週期降溫以及電子產品生產的成熟。 KUKDO和南亞等國內企業以低於競爭對手的到岸成本向印刷基板組裝商供貨,鞏固了該地區的市場主導地位。然而,由於季風影響和資金籌措挑戰,印度的基礎設施項目時常停滯,這抑制了短期前景。同時,日本和韓國對半導體產業的投資推動了樹脂的年度需求,抵消了智慧型手機組裝的停滯。東南亞國協正在取得進展,但物流和政策不匹配正在減緩產能擴張的速度。

北美將在2025年成為主要消費地區,預計在2026年至2031年的預測期內將保持穩定成長。聯邦政府的橋樑維護計畫正擴大採用環氧樹脂進行裂縫灌漿,這可以顯著減少停工時間。奧林公司正策略性地擴大國內環氧氯丙烷的生產,旨在降低對中國進口的依賴。 2025年,隨著電池式電動車產量的成長,對封裝的需求也隨之增加。雖然與更成熟的建築業相比,這一需求仍然小規模,但加拿大鐵路電氣化和墨西哥近岸電子產品生產線等措施正在創造巨大的成長機會。

歐洲預計在2025年將佔相當大的銷售佔有率,但同時也面臨能源成本飆升和REACH法規嚴格合規等挑戰。然而,歐洲在永續化學技術方面處於主導。歐洲正在推廣可回收的風力渦輪機葉片,並透過碳邊境調節機制為生物基複合材料提供獎勵。從2025年起,德國和英國將強制使用可回收的複合材料,並正在加速推廣Swancoal公司的「EzCiclo」技術。同時,法國和義大利正在優先考慮使用低VOC(揮發性有機化合物)內牆塗料進行鐵路維修。俄羅斯的相關活動仍然較為低迷,但德國和英國在這些趨勢中處於領先地位。

中東和非洲地區正經歷最快成長,預計在2026年至2031年的預測期內,年複合成長率將達到5.94%。柔軟性環氧樹脂正被應用於沙烏地阿美公司的賈夫拉輸油管和NEOM高層建築。在南非,無煤焦油塗料正被用於沿海鐵路的維修項目,但由於資金限制,採購工作有所延誤。南美洲正處於穩定成長的軌道上,這主要得益於巴西的地鐵計畫和阿根廷的頁岩氣開發。然而,由於關稅波動和外匯波動等挑戰,原料成本正在上漲。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 建築和基礎設施支出激增

- 家用電子電器和電動汽車電力電子產品的電氣化

- 風力渦輪機葉片生產和維修的快速擴張

- 對耐腐蝕工業塗料的需求日益成長

- 在穿戴式裝置和物聯網裝置的軟性PCB中採用柔軟性環氧樹脂。

- 市場限制因素

- 環氧氯丙烷和雙A原料的價格波動

- 職業毒性和 REACH/EPA 合規成本

- 對整個環氧樹脂價值鏈中的範圍 3排放進行審查

- 價值鏈分析

- 波特五力模型

- 供應商的議價能力

- 消費者議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭程度

第5章 市場規模與成長預測

- 按類型

- 改質胺甲酸乙酯

- 橡膠改性

- 齊默酸變性

- 透過使用

- 電氣和電子

- 黏合劑

- 複合材料

- 油漆和塗料

- 其他

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 東南亞國協

- 亞太其他地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 義大利

- 法國

- 俄羅斯

- 其他歐洲地區

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率(%)/排名分析

- 公司簡介

- Aditya Birla Chemicals

- BASF SE

- Cardolite Corporation

- Conren Limited

- DIC Corporation

- Dow

- EPOXONIC

- Henkel AG & Co. KGaA

- Hexion

- Huntsman Corporation

- INTERTRONICS

- KUKDO Chemical(Kunshan)Co., Ltd.

- LymTal International, Inc.

- Mereco Technologies

- Nan Ya Plastic Corporation

- Olin Corporation

- Sicomin Epoxy Systems

- Solvay

第7章 市場機會與未來展望

The Flexible Epoxy Resin Market size is projected to expand from USD 0.77 billion in 2025 and USD 0.81 billion in 2026 to USD 1.03 billion by 2031, registering a CAGR of 4.88% between 2026 to 2031.

Once centered on commodity construction adhesives, the industry is now pivoting towards high-value applications. These encompass electric-vehicle power electronics, wind-turbine blade repairs, and flexible printed circuits designed for wearables. While rubber-modified grades continue to dominate structural composites, there is a marked rise in the use of urethane-modified chemistries, particularly for electronics encapsulation. The Asia-Pacific region, strengthened by its vibrant electronics and construction sectors, stands as the primary demand hub. Yet, the Middle-East and Africa are experiencing the swiftest growth, spurred by Saudi Arabia's ambitious infrastructure initiatives and the groundbreaking NEOM project. Despite this growth, industry profitability is challenged by the volatile pricing of epichlorohydrin and intensified regulatory scrutiny on bisphenol-A diglycidyl ether. In this evolving landscape, vertically integrated firms and bio-based innovators find themselves at an advantage, adeptly securing feedstock and navigating compliance hurdles.

Global Flexible Epoxy Resin Market Trends and Insights

Surging Construction and Infrastructure Spending

Infrastructure budgets across Asia-Pacific, the Middle-East, and North America are driving a steady demand for flexible epoxy adhesives and coatings. In 2024, China made a significant budget allocation for rail lines and metro extensions, highlighting the need for vibration-damping epoxy joints. Concurrently, India's National Infrastructure Pipeline set its sights on roads and urban transit, with substantial funding slated for 2025. This initiative spurred demand for anti-corrosion epoxy coatings, particularly for rebar in coastal flyovers. Over the past five years, the United States has channeled significant investments into bridge rehabilitation, favoring crack-injection epoxies that halve closure times. Saudi Arabia's Vision 2030 development project, with NEOM at its forefront, underscored the importance of low-VOC flexible epoxy coatings, ensuring durability against the desert's harsh heat. Yet, despite the robust demand driven by these projects, it is essential to recognize that financing delays and currency fluctuations could extend adhesive procurement timelines by up to a year.

Electrification of Consumer Electronics and Electric-Vehicle Power Electronics

Thousands of multilayer ceramic capacitors in every battery electric vehicle (BEV) now benefit from flexible epoxy terminations. This number notably surpasses that found in traditional combustion engine models. These terminations ensure solder-joint durability across a temperature range of -40 to +150 degrees Celsius. The global production of battery electric vehicles has increased significantly in recent years, with forecasts indicating this trend will continue. As a result, there has been a corresponding rise in the use of potting and encapsulants. In consumer electronics, foldable phones and health wearables are increasingly utilizing urethane-modified epoxies. These specialized epoxies, known for their high elongation, are designed to pass rigorous bend tests. In a noteworthy industry development, firms from Japan and South Korea are channeling substantial investments into advanced packaging, targeting completion by the end of the decade. A pivotal component for these cutting-edge packages is the low-modulus epoxy underfills. These trends in electronics are driving the segment's projected 6.31% CAGR during the forecast period of 2026-2031.

Volatile Prices of Epichlorohydrin and Bis-A Raw Materials

In recent years, Chinese producers expanded their capacity significantly, leading to notable fluctuations in spot prices for epichlorohydrin and bisphenol-A. These two chemicals constitute a major portion of production costs. As a result, Western formulators, tied to annual contracts, grappled with pricing instability. A spike in propylene feedstocks drove European epichlorohydrin prices up sharply, reducing gross margins. Smaller converters, lacking hedging strategies or backward integration, faced the risk of quarterly losses if they could not adjust prices in their adhesive supply agreements.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Expansion of Wind-Energy Blade Production and Repair

- Rising Demand for Corrosion-Resistant Industrial Coatings

- Occupational Toxicity and REACH/EPA Compliance Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, rubber-modified grades, leveraging two-phase morphologies, accounted for 41.38% of the revenue, enhancing fracture toughness. This enhancement proved vital for applications in wind blades and industrial adhesives. The market for rubber-modified flexible epoxy resins is projected to grow in tandem with the overall CAGR during the forecast period of 2026-2031, driven by demand from the construction and composite sectors. Urethane-modified chemistries are expected to expand at a 6.24% CAGR (2026-2031), fueled by their role in electronics encapsulation. Here, attributes such as high elongation and a glass-transition temperature below freezing are essential for safeguarding solder joints. Echoing this trend, a 2024 product launch marked a notable reduction in modulus, highlighting a pivot toward materials adept for lower-stress die attachment. On a different note, dimer-acid products, with a small share, focus on specialized marine coatings, emphasizing hydrophobicity and bio-content.

The market's segmentation thrives on a nuanced interplay of cost-performance dynamics. Structural adhesive users lean toward rubber-modified grades. Conversely, chipmakers opt for urethane at a premium, acutely aware of potential warranty liabilities from field failures. Dominant players in the flexible epoxy resin market skillfully navigate this terrain, championing urethane applications in automotive electronics while preserving rubber shares for the construction sector. Cashew-based dimer-acid resins have carved out a space in offshore wind foundations. However, this niche anticipates sluggish growth, eyeing a possible uplift from hastened material substitutions spurred by carbon pricing.

The Flexible Epoxy Resin Market Report is Segmented by Type (Urethane Modified, Rubber Modified, and Dimer Acid Modified), Application (Electrical and Electronics, Adhesives, Composites, Paints and Coatings, and Others), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

In 2025, the Asia-Pacific region held a commanding 47.36% share of the revenue, but growth has since moderated. This slowdown is attributed to a cooling construction cycle in China and a maturing electronics output. Domestic players, such as KUKDO and Nan Ya, are supplying printed-circuit assemblers at landed costs lower than those of their competitors, which strengthens the region's dominance. However, India's infrastructure projects have occasionally stalled due to monsoon impacts and financing challenges, tempering short-term expectations. Meanwhile, investments in semiconductors from Japan and South Korea are driving annual resin demand, counterbalancing a plateau in smartphone assembly. The ASEAN nations are progressing, but inconsistencies in logistics and policy are slowing their capacity expansions.

North America, a significant consumer in 2025, is projected to experience steady growth during the forecast period of 2026-2031. Federal bridge programs are increasingly favoring crack-injection epoxies, which notably minimize downtime. Olin's strategic domestic expansion of epichlorohydrin aims to reduce reliance on Chinese imports. In 2025, as battery electric vehicle production increased, so did the demand for encapsulants. While this demand remains modest compared to the more established construction sector, initiatives such as Canada's rail electrification and Mexico's nearshored electronics lines are providing notable growth opportunities.

Europe, while accounting for a significant share of 2025 sales, has faced challenges such as high energy costs and stringent REACH filings. However, the continent is leading sustainable chemistry initiatives. Europe is advocating for recyclable wind blades and incentivizing bio-based formulations through the Carbon Border Adjustment Mechanism. Starting in 2025, both Germany and the United Kingdom have mandated recyclable composites, accelerating the adoption of Swancor's EzCiclo. Meanwhile, France and Italy are prioritizing rail upgrades with low-VOC interior coatings. While Russia's activity remains subdued, Germany and the United Kingdom are at the forefront of these developments.

The Middle-East and Africa are experiencing the fastest growth, boasting a 5.94% CAGR during the forecast period of 2026-2031. Projects such as Saudi Aramco's Jafurah pipeline and the NEOM smart city are opting for flexible epoxies, highlighting their resistance to thermal shock and sand abrasion. GCC desalination plants and the facades of Dubai's high-rises are utilizing water-borne epoxies, which are recognized for their energy-efficient curing. In South Africa, coastal rail rehabilitation is employing coal-tar-free coatings but is facing procurement delays due to fiscal constraints. South America, driven by metro projects in Brazil and shale developments in Argentina, is on a steady growth path. However, challenges such as tariff fluctuations and currency swings are increasing feedstock costs.

- Aditya Birla Chemicals

- BASF SE

- Cardolite Corporation

- Conren Limited

- DIC Corporation

- Dow

- EPOXONIC

- Henkel AG & Co. KGaA

- Hexion

- Huntsman Corporation

- INTERTRONICS

- KUKDO Chemical (Kunshan) Co., Ltd.

- LymTal International, Inc.

- Mereco Technologies

- Nan Ya Plastic Corporation

- Olin Corporation

- Sicomin Epoxy Systems

- Solvay

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging construction and infrastructure spending

- 4.2.2 Electrification of consumer electronics and Electric Vehicle power-electronics

- 4.2.3 Rapid expansion of wind-energy blade production and repair

- 4.2.4 Rising demand for corrosion-resistant industrial coatings

- 4.2.5 Adoption of flexible epoxies in wearable and IoT flexible PCBs

- 4.3 Market Restraints

- 4.3.1 Volatile prices of epichlorohydrin and bis-A raw materials

- 4.3.2 Occupational toxicity and REACH/EPA compliance costs

- 4.3.3 Scope-3 emissions scrutiny across epoxy value chains

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Consumers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Urethane Modified

- 5.1.2 Rubber Modified

- 5.1.3 Dimer Acid Modified

- 5.2 By Application

- 5.2.1 Electrical and Electronics

- 5.2.2 Adhesives

- 5.2.3 Composites

- 5.2.4 Paints and Coatings

- 5.2.5 Others

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN Countries

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Russia

- 5.3.3.6 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 Aditya Birla Chemicals

- 6.4.2 BASF SE

- 6.4.3 Cardolite Corporation

- 6.4.4 Conren Limited

- 6.4.5 DIC Corporation

- 6.4.6 Dow

- 6.4.7 EPOXONIC

- 6.4.8 Henkel AG & Co. KGaA

- 6.4.9 Hexion

- 6.4.10 Huntsman Corporation

- 6.4.11 INTERTRONICS

- 6.4.12 KUKDO Chemical (Kunshan) Co., Ltd.

- 6.4.13 LymTal International, Inc.

- 6.4.14 Mereco Technologies

- 6.4.15 Nan Ya Plastic Corporation

- 6.4.16 Olin Corporation

- 6.4.17 Sicomin Epoxy Systems

- 6.4.18 Solvay

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

風力渦輪機葉片樹脂市場預測至2034年-按樹脂類型、應用、最終用戶和地區分類的全球分析

風力渦輪機葉片樹脂市場預測至2034年-按樹脂類型、應用、最終用戶和地區分類的全球分析 環氧樹脂市場:2026-2032年全球市場預測(依樹脂類型、形態、應用、終端用戶產業及通路分類)

環氧樹脂市場:2026-2032年全球市場預測(依樹脂類型、形態、應用、終端用戶產業及通路分類) 環氧樹脂市場:市場規模、佔有率、成長率、全球產業分析、按類型、應用和地區分類的分析以及未來預測(2026-2034 年)

環氧樹脂市場:市場規模、佔有率、成長率、全球產業分析、按類型、應用和地區分類的分析以及未來預測(2026-2034 年) 生物可再生環氧樹脂市場分析及預測(至2035年):類型、產品、應用、技術、材料類型、最終用戶、形態、製程、功能、安裝類型2026-2034年雙酚A氫全球市場規模、佔有率、趨勢和成長分析報告全球生物基環氧樹脂市場規模、佔有率、趨勢和成長分析報告(2026-2034)

生物可再生環氧樹脂市場分析及預測(至2035年):類型、產品、應用、技術、材料類型、最終用戶、形態、製程、功能、安裝類型2026-2034年雙酚A氫全球市場規模、佔有率、趨勢和成長分析報告全球生物基環氧樹脂市場規模、佔有率、趨勢和成長分析報告(2026-2034) 2026年全球環氧樹脂市場報告2026年全球高純度環氧樹脂市場報告2026年生物基環氧樹脂全球市場報告

2026年全球環氧樹脂市場報告2026年全球高純度環氧樹脂市場報告2026年生物基環氧樹脂全球市場報告 環氧樹脂市場規模、佔有率和趨勢分析報告:按應用、地區和細分市場預測(2026-2033 年)

環氧樹脂市場規模、佔有率和趨勢分析報告:按應用、地區和細分市場預測(2026-2033 年)