|

市場調查報告書

商品編碼

2066435

歐洲環氧樹脂:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Europe Epoxy Resins - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

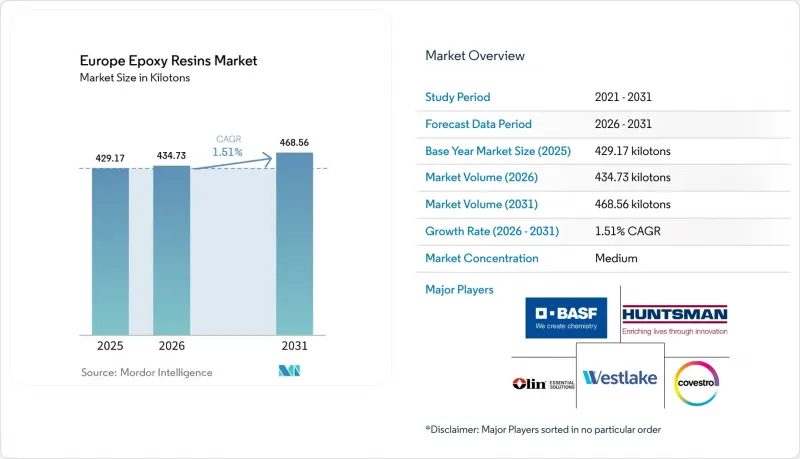

據 Mordor Intelligence 稱,歐洲環氧樹脂市場預計將從 2025 年的 429.17 千噸成長到 2026 年的 434.73 千噸,到 2031 年達到 468.56 千噸,2026 年至 2031 年的複合年成長率為 1.51%。

本報告按原料(DGBEA、DGBEF、酚醛樹脂、脂肪族樹脂、縮水甘油胺及其他原料)、應用領域(油漆和塗料、黏合劑和密封劑、複合材料、電氣和電子設備、風力發電機等)以及地區(德國、英國、法國、義大利、西班牙、俄羅斯、北歐國家及其他歐洲國家)進行細分。市場預測以噸為單位。

歐洲環氧樹脂市場的趨勢與洞察

風力渦輪機葉片需求激增

歐洲的目標是到2030年達到510吉瓦的風電裝置容量,但國際能源總署(IEA)預測,歐洲的總裝置容量僅為370吉瓦,這將造成28%的缺口,並延長工程建設前置作業時間。每台兆瓦級風力發電機組的葉片生產需要消耗高達10噸環氧樹脂,這推動了丹麥、西班牙和義大利的樹脂消耗,維斯塔斯和西門子歌美颯在這些國家運作葉片工廠。 2024年,維斯塔斯累計5.31億歐元用於綠色研發,其中2050萬歐元分配給了CETEC,這是一個由奧林和斯特納回收公司組成的聯合體,旨在展示到2026年達到使用壽命終點的葉片的化學回收利用技術。如果成功,這將創建一個循環原料庫,從而緩解對原生樹脂的需求壓力。北海離岸風力發電的擴張持續推動對依賴環氧樹脂化學的海洋塗料和海底水泥漿應用的需求。

推廣汽車用輕量複合材料

空中巴士公司計劃在2024年將A350的月產量提高到10架,該機型52%的結構將採用環氧樹脂基複合材料。為此,海克塞爾公司在法國和奧地利新建了預浸料生產線,使其2024年第四季的銷售額成長了12.5%。在汽車領域,電池組的加入使電動車的重量增加了400-500公斤,促使汽車製造商從鋼材轉向碳纖維環氧樹脂車身面板,後者可減輕高達50%的重量。里卡多預測,到2030年,複合材料在歐洲輕型汽車的應用將會增加,東麗和西恩科等公司正在擴大其碳纖維產能以滿足市場需求。

對雙酚A和環氧氯丙烷的法規進行審查

2024/3190號規則將自2025年起禁止在食品接觸材料中使用雙酚A,僅大型儲存槽和聚碸膜等極少數情況例外。同時,CLP規則的修訂在常用促進劑上增加了「致癌性1B」和「皮膚致敏物1A」的標籤,使中型製造商的合規成本增加高達12%。此外,新的標籤檢視要求客戶對產品進行重新認證,延長了配方變更的前置作業時間。根據理事會第2024/745號規則實施的製裁進一步限制了與某些俄羅斯公司的資料共用,使特殊等級產品的聯合研發更加複雜。

細分市場分析

預計到2025年,DGBEA將維持在歐洲環氧樹脂市場36.05%的佔有率,並持續以6.05%的複合年成長率成長至2031年。然而,其對雙酚A的高度依賴使混配商面臨監管風險,促使市場轉向雙酚F和酚醛樹脂等替代品。酚醛樹脂的交聯密度比DGBEA高30-40%,玻璃化轉變溫度超過150 度C,因此一旦英特爾馬德堡工廠和台積電德累斯頓工廠於2027年運作,它們將成為半導體封裝的關鍵材料。因此,預計歐洲環氧樹脂市場中酚醛樹脂的市場規模成長速度將超過基準。玻璃化轉變溫度超過200 度C的縮水甘油胺樹脂仍是航太預浸料的標竿材料,符合空中巴士A350的運作要求。同時,環脂族和脂肪族塗料可解決裝飾塗料和LED封裝中的紫外線穩定性問題。 REACH法規的申報費用和資料共用義務正在推動行業重組,而垂直整合的大型企業由於能夠將合規成本分攤到更廣泛的生產環節,因此保持了其優勢。

此外,複合材料生產商也正在檢驗以甘油為原料的生物基環氧氯丙烷。雖然商業性供應有限,但若能成功擴大生產規模,則可望減少氯的使用量並改善碳足跡。正在進行的試驗表明,其在地板材料和電子封裝材料方面的性能與生物基環氧氯丙烷相當,但要實現成本上的可比性,則需要在亞洲擴大產能或在歐洲建造專用工廠。同時,大多數生產商正透過將生物基組分與傳統原料混合來平衡機械性能和價格,從而規避風險。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 風力渦輪機葉片需求激增

- 促進輕質複合材料在汽車領域的廣泛應用

- 電子電氣設備製造業的擴張

- 建築防護塗料市場的復甦

- 歐盟「翻新浪潮」計畫為地板材料提供補貼

- 市場限制因素

- 對雙酚A和環氧氯丙烷的監管

- 與原油價格相關的原物料價格波動

- 生物基樹脂替代帶來的威脅

- 價值鏈分析

- 波特五力模型

第5章 市場規模與成長預測

- 按成分

- DGBEA(雙酚A和ECH)

- DGBEF(雙酚F和ECH)

- 酚醛樹脂(甲醛和苯酚)

- 脂肪族(脂肪醇)

- 縮水甘油胺(芳香胺和ECH)

- 其他原料

- 透過使用

- 油漆和塗料

- 黏合劑和密封劑

- 複合材料

- 電氣和電子設備

- 風力發電機

- 其他用途

- 按地區

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐國家

- 其他歐洲國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率和排名分析

- 公司簡介

- 3M

- Aditya Birla Chemicals

- Arkema

- BASF

- Bitrez Ltd

- Covestro AG

- DIC Corporation

- DuPont

- Huntsman International LLC

- Leuna-Harze GmbH

- Olin Corporation

- POLYNT-REICHHOLD GROUP

- Sika AG

- Sir Industriale

- Solvay

- Spolchemie

- Westlake Corporation

第7章 市場機會與未來展望

According to Mordor Intelligence, the europe epoxy resins market size is expected to increase from 429.17 kilotons in 2025 to 434.73 kilotons in 2026 and reach 468.56 kilotons by 2031, growing at a CAGR of 1.51% over 2026-2031.

This report is Segmented by Raw Material (DGBEA, DGBEF, Novolac, Aliphatic, Glycidylamine, and Other Raw Materials), Application (Paints and Coatings, Adhesives and Sealants, Composites, Electrical and Electronics, Wind Turbines, and More), and Geography (Germany, United Kingdom, France, Italy, Spain, Russia, Nordic Countries, and Rest of Europe). The Market Forecasts are Provided in Terms of Volume (Tons).

Europe Epoxy Resins Market Trends and Insights

Surge in Wind-Energy Blade Demand

Europe aims to achieve 510 GW of installed wind capacity by 2030; however, the International Energy Agency forecasts the continent will reach only 370 GW, resulting in a 28% gap that is lengthening project lead times. Blade production consumes up to 10 tons of epoxy per multi-MW unit, driving resin consumption across Denmark, Spain, and Italy, where Vestas and Siemens Gamesa run blade plants. Vestas earmarked EUR 531 million for green R&D in 2024, with EUR 20.5 million allocated to CETEC, a consortium comprising Olin and Stena Recycling, which aims to demonstrate the chemical recycling of end-of-life blades by 2026. Success would create a circular feedstock pool and alleviate pressures on virgin resin demand. Offshore wind growth in the North Sea continues to drive demand for marine coatings and subsea grout applications, which also rely on epoxy chemistry.

Lightweight Automotive Composites Push

Airbus increased A350 output to 10 aircraft per month in 2024, and the model uses epoxy-matrix composites for 52% of its structure. Hexcel responded with new prepreg lines in France and Austria, supporting a 12.5% sales rise in Q4 2024. On the road, battery packs add 400-500 kg to electric vehicles, prompting OEMs to switch from steel to carbon-fiber epoxy body panels, which reduce mass by up to 50%. Ricardo projects rising composite content in European light vehicles through 2030, while Toray and Syensqo have expanded carbon-fiber capacity to meet demand.

BPA and ECH Regulatory Scrutiny

Regulation 2024/3190 bans bisphenol A in food-contact materials from 2025, leaving only narrow derogations for large storage tanks and polysulfone membranes. Parallel CLP amendments add Carcinogen 1B and Skin Sensitizer 1A tags to popular accelerators, raising compliance costs by up to 12% for mid-tier producers. The new labels also extend reformulation lead times as products pass customer requalification. Sanctions under Council Regulation 2024/745 further restrict data sharing with certain Russian entities, complicating joint research and development on specialty grades.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Electronics and Electricals Manufacturing

- Rebound in Protective Construction Coatings

- Crude-Linked Raw-Material Price Volatility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

DGBEA retained 36.05% of Europe epoxy resin market share in 2025 and is trending at a 6.05% CAGR to 2031, yet its reliance on bisphenol A exposes formulators to regulatory risk that is triggering a pivot toward bisphenol-F and novolac alternatives. Novolac resins deliver crosslink densities 30-40% above DGBEA, raising glass-transition temperatures beyond 150°C and making them indispensable for semiconductor encapsulation once Intel's Magdeburg and TSMC's Dresden lines commence operation in 2027. Europe epoxy resin market size for novolac grades is therefore set to expand more quickly than the baseline. Glycidylamine systems remain the benchmark for aerospace prepregs due to their glass-transition temperatures above 200°C, which meet Airbus A350 service requirements. Meanwhile, cycloaliphatic and aliphatic grades address ultraviolet stability in decorative finishes and LED encapsulation. REACH fees and data-sharing obligations have encouraged consolidation, giving vertically integrated majors an edge as they can amortize compliance costs across broader volumes.

Formulators are also validating bio-based epichlorohydrin from glycerol. While commercial supply is limited, a successful scale-up would reduce chlorine use and improve carbon footprints. Ongoing trials suggest performance parity in flooring and electrical potting, but cost parity requires larger Asian capacities or European on-purpose plants. Until then, most producers hedge by blending bio-content with conventional feedstocks to balance mechanical performance and pricing.

List of Companies Covered in this Report:

- 3M

- Aditya Birla Chemicals

- Arkema

- BASF

- Bitrez Ltd

- Covestro AG

- DIC Corporation

- DuPont

- Huntsman International LLC

- Leuna-Harze GmbH

- Olin Corporation

- POLYNT-REICHHOLD GROUP

- Sika AG

- Sir Industriale

- Solvay

- Spolchemie

- Westlake Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in wind-energy blade demand

- 4.2.2 Lightweight automotive composites push

- 4.2.3 Expansion of Electronics and Electricals manufacturing

- 4.2.4 Rebound in protective construction coatings

- 4.2.5 EU "Renovation Wave" subsidies for epoxy floors

- 4.3 Market Restraints

- 4.3.1 BPA and ECH regulatory scrutiny

- 4.3.2 Crude-linked raw-material price volatility

- 4.3.3 Bio-based resin substitution threat

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size & Growth Forecasts (Volume)

- 5.1 By Raw Material

- 5.1.1 DGBEA (Bisphenol A and ECH)

- 5.1.2 DGBEF (Bisphenol F and ECH)

- 5.1.3 Novolac (Formaldehyde and Phenols)

- 5.1.4 Aliphatic (Aliphatic Alcohols)

- 5.1.5 Glycidylamine (Aromatic Amines and ECH)

- 5.1.6 Other Raw Materials

- 5.2 By Application

- 5.2.1 Paints and Coatings

- 5.2.2 Adhesives and Sealants

- 5.2.3 Composites

- 5.2.4 Electrical and Electronics

- 5.2.5 Wind Turbines

- 5.2.6 Other Applications

- 5.3 By Geography

- 5.3.1 Germany

- 5.3.2 United Kingdom

- 5.3.3 France

- 5.3.4 Italy

- 5.3.5 Spain

- 5.3.6 Russia

- 5.3.7 NORDIC Countries

- 5.3.8 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 3M

- 6.4.2 Aditya Birla Chemicals

- 6.4.3 Arkema

- 6.4.4 BASF

- 6.4.5 Bitrez Ltd

- 6.4.6 Covestro AG

- 6.4.7 DIC Corporation

- 6.4.8 DuPont

- 6.4.9 Huntsman International LLC

- 6.4.10 Leuna-Harze GmbH

- 6.4.11 Olin Corporation

- 6.4.12 POLYNT-REICHHOLD GROUP

- 6.4.13 Sika AG

- 6.4.14 Sir Industriale

- 6.4.15 Solvay

- 6.4.16 Spolchemie

- 6.4.17 Westlake Corporation

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

風力渦輪機葉片樹脂市場預測至2034年-按樹脂類型、應用、最終用戶和地區分類的全球分析

風力渦輪機葉片樹脂市場預測至2034年-按樹脂類型、應用、最終用戶和地區分類的全球分析 水性環氧樹脂市場:依應用、產品類型、分子量、最終用途產業和地區分類。

水性環氧樹脂市場:依應用、產品類型、分子量、最終用途產業和地區分類。 環氧樹脂市場:2026-2032年全球市場預測(依樹脂類型、形態、應用、終端用戶產業及通路分類)

環氧樹脂市場:2026-2032年全球市場預測(依樹脂類型、形態、應用、終端用戶產業及通路分類) 柔軟性環氧樹脂:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

柔軟性環氧樹脂:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 環氧樹脂市場:市場規模、佔有率、成長率、全球產業分析、按類型、應用和地區分類的分析以及未來預測(2026-2034 年)

環氧樹脂市場:市場規模、佔有率、成長率、全球產業分析、按類型、應用和地區分類的分析以及未來預測(2026-2034 年) 生物可再生環氧樹脂市場分析及預測(至2035年):類型、產品、應用、技術、材料類型、最終用戶、形態、製程、功能、安裝類型2026-2034年雙酚A氫全球市場規模、佔有率、趨勢和成長分析報告全球生物基環氧樹脂市場規模、佔有率、趨勢和成長分析報告(2026-2034)

生物可再生環氧樹脂市場分析及預測(至2035年):類型、產品、應用、技術、材料類型、最終用戶、形態、製程、功能、安裝類型2026-2034年雙酚A氫全球市場規模、佔有率、趨勢和成長分析報告全球生物基環氧樹脂市場規模、佔有率、趨勢和成長分析報告(2026-2034) 2026年全球環氧樹脂市場報告2026年全球高純度環氧樹脂市場報告

2026年全球環氧樹脂市場報告2026年全球高純度環氧樹脂市場報告