|

市場調查報告書

商品編碼

2066505

口腔護理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Oral Care - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

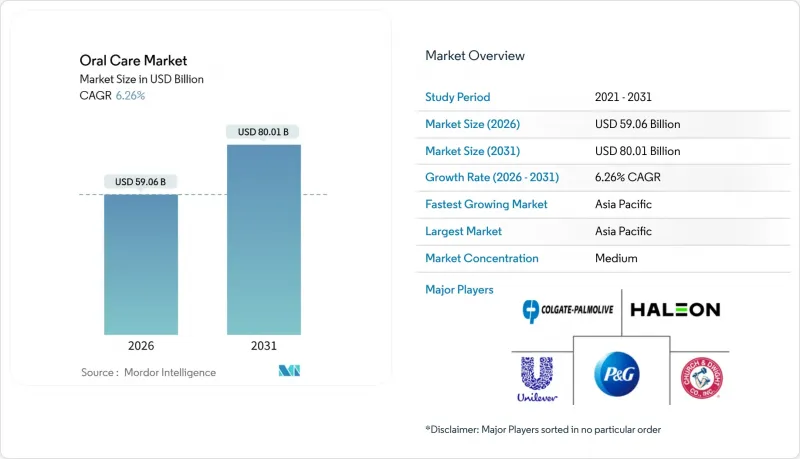

根據 Mordor Intelligence 預測,口腔護理市場規模預計將在 2026 年達到 590.6 億美元,到 2031 年達到 800.1 億美元,年複合成長率為 6.26%。

本報告按產品類型(牙膏、漱口水/漱喉劑等)、成分(傳統成分和天然/有機成分)、最終用戶(兒童和成人)、配銷通路(超級市場/大賣場、藥店/藥房等)以及地區(北美、歐洲、亞太、南美、中東和非洲)進行細分。市場預測以美元計價。

全球口腔護理市場趨勢與洞察

人們的健康和衛生意識日益增強。

人們對健康和衛生意識的提高是全球口腔護理市場發展的關鍵驅動力。這是因為消費者越來越將口腔健康視為整體健康的重要組成部分。隨著人們對口腔衛生不良與心血管疾病、糖尿病和感染疾病等全身性疾病之間聯繫的認知不斷加深,口腔護理正從單純的基本衛生習慣轉變為預防保健的重點。牙科協會、公共衛生組織和口腔護理行業的各個品牌都在進行宣傳活動,強調定期刷牙、使用牙線以及使用漱口水等輔助產品的重要性。因此,口腔護理產品的使用頻率和普及率都在不斷提高。消費者現在更注重預防,而不是在牙齒問題出現後才進行治療,這導致對齲齒、牙周病、斑塊控制、牙齒敏感和口臭等功能性和治療性口腔護理解決方案的需求不斷成長。口腔護理市場日益成長的這種意識正在推動人們採用多步驟的口腔護理程序,並鼓勵人們嘗試根據自身健康偏好量身定做的先進、專業和天然配方。

口腔疾病負擔加重

口腔疾病盛行率的上升是全球口腔護理市場的重要驅動力。這是因為牙科疾病的頻繁發生已使口腔衛生從「可有可無的習慣」轉變為「醫療必需品」。齲齒、牙周病和牙齦積液在兒童和成人中的普遍流行,推動了對預防性和治療性口腔護理產品的需求,例如防齲牙膏、藥用漱口水和牙齦護理產品。在口腔清潔用品市場,未治療的口腔疾病帶來的臨床和經濟影響促使各國政府、醫療保健機構和消費者將早期療育和日常口腔衛生放在首位。例如,衛生署的一份報告指出,沙烏地阿拉伯2025年的齲齒盛行率將非常高,6歲兒童的盛行率將達到96%,12歲兒童的盛行率將達到93.7%,這清楚地顯示了公共衛生挑戰的嚴峻程度。此外,牙科治療費用約佔醫療保健總費用的5%,凸顯了可預防的口腔疾病帶來的巨大經濟負擔。口腔清潔用品市場的這些統計數據凸顯了預防性口腔清潔用品習慣的重要性,以及人們越來越依賴日常產品作為臨床治療的經濟有效的替代方案。

產品安全問題與召回

產品安全問題和召回事件是全球口腔護理市場的主要限制因素,它們會削弱消費者信任,損害品牌聲譽,並延緩新配方和新技術的推出。由於口腔護理產品每日使用,並直接接觸敏感的口腔組織,因此消費者和監管機構都要求產品具有高度安全性。例如,電動牙刷的副作用、污染、過度磨損或電池相關問題等設備故障報告,都可能導致產品召回、負面媒體報告以及監管機構更嚴格的審查。這些安全問題也將延緩產品上市,因為口腔護理公司將面臨更嚴格的測試流程、配方修改要求以及更長的核准程序。此外,召回和安全問題也會為公司帶來經濟損失、法律責任和長期聲譽損害。在一個信任和專家建議至關重要的市場中,回想事件可能會促使消費者重新選擇熟悉的傳統產品,最終限制該品類的成長和創新潛力。

細分市場分析

預計到2025年,牙膏將佔據口腔護理市場49.76%的主導地位,持續推動全球口腔護理市場的發展,在日常口腔衛生中發揮著至關重要的作用,並受到各個年齡層的廣泛認可。牙膏被公認為最不可或缺的口腔護理產品,是人們經常購買和重複購買的商品,已成為日常生活中不可或缺的一部分。牙膏在口腔清潔用品市場的主導地位,得益於配方不斷創新,以滿足各種口腔健康需求,包括預防蛀牙、護理牙齦、緩解牙齒敏感、美白牙齒、修復琺瑯質和預防口臭。這些進步使品牌能夠同時滿足預防、治療和美容方面的需求。此外,牙醫的大力支持和公共衛生指南建議每天刷牙兩次,進一步鞏固了刷牙習慣作為口腔清潔用品基礎的地位。

預計到2031年,漱口水和漱喉劑將以6.76%的複合年成長率成長,成為全球口腔護理市場成長最快的產品類型之一。其日益普及源於人們認知到,漱口水和漱喉劑是全面口腔衛生習慣中不可或缺的補充。消費者越來越意識到,僅靠刷牙不足以解決口臭、牙菌斑堆積、牙齦炎以及難以清潔部位的細菌控制等問題。這種意識的增強正在加速漱口水作為日常預防措施的使用。此外,牙醫的建議和治療後口腔清潔用品指南也促進了含藥漱口水和治療性漱口水的使用,使其應用範圍從改善口臭擴展到臨床和預防用途。

預計到2025年,傳統配方將佔據全球口腔清潔用品口腔清潔用品力。它們基於氟化物和抗菌劑等經過科學驗證的成分,能夠有效解決常見的口腔健康問題,例如預防齲齒、控制斑塊和維護牙齦健康。因此,它們深受消費者和牙科專業人士的青睞。此外,消費者對這些產品的熟悉度和信任度也降低了其普及門檻,確保了它們在口腔清潔用品流程中持續佔據重要地位,即使高級產品和特色產品在市場上逐漸興起。

預計到2031年,有機產品將以7.12%的複合年成長率成長,隨著消費者偏好轉向「潔淨標示」、成分透明和整體健康理念,有機產品正推動全球口腔護理市場穩步成長。這一成長的促進因素是人們日益關注長期接觸合成化學物質,促使消費者選擇植物來源、草本和天然替代品,這些替代品被認為更溫和、更適合日常使用。有機口腔護理產品深受注重健康的消費者、家長和敏感肌膚人群的青睞,因為它們避免使用刺激性添加劑,並專注於源自植物萃取物、精油和礦物質的活性成分。此外,口腔護理與健康和預防醫學趨勢之間的廣泛聯繫也促進了這一細分市場的發展,因為口腔衛生日益被認為是整體健康不可或缺的一部分。

區域分析

亞太地區預計將成為成長最快的區域市場,到2025年將佔據全球口腔護理市場規模的29.91%,並在2031年之前保持強勁成長,年複合成長率(CAGR)將達到7.83%。這一成長主要得益於口腔衛生意識的提高、預防保健措施的改進以及都市區和半都市區現代口腔衛生習慣的養成。龐大的人口基數、對日常口腔清潔用品習慣的日益重視以及有組織的零售和電子商務平台的擴張等因素,正在加速產品滲透。中國和印度等國家在這一成長中發揮著核心作用,這得益於政府主導的口腔健康舉措、學校口腔衛生項目以及人們對功能性產品(例如抗敏牙膏、牙齦護理產品和草藥產品)日益成長的接受度。該地區對傳統和天然口腔清潔用品產品的接受度,進一步鞏固了其作為長期成長驅動力的地位。

北美和歐洲的口腔清潔用品市場仍然成熟,在口腔衛生意識高、牙醫影響力強以及預防性牙科護理實踐完善的推動下,市場保持穩定成長。這些地區的成長主要由產品創新、優質化以及對專業口腔清潔用品解決方案(例如美白、琺瑯質修復、牙齦保護和無酒精或治療性漱口水)的需求所驅動。這些市場的消費者表現出較高的品牌忠誠度,同時也樂於接受先進的配方、智慧口腔護理設備和有機產品。儘管市場整體已趨於成熟,但監管政策的明確性、牙科保健服務的廣泛覆蓋以及強大的零售和線上分銷網路,進一步促進了市場的穩定擴張。

南美洲、中東和非洲的口腔護理市場仍相對欠缺發展。價格敏感、專業牙科服務取得管道有限,以及牙膏棒、草本粉末和家庭療法等傳統口腔衛生習慣的盛行,都阻礙了市場成長。在這些地區的許多地方,口腔清潔用品仍然被視為基本的衛生習慣,而非預防性醫療保健的重點,這限制了專業和高級產品的普及。此外,人們對現代口腔清潔用品益處的認知不足以及零售基礎設施的不完善,進一步減緩了市場成長。然而,隨著教育水平的逐步提高、都市化的推進以及公共衛生意識的增強,這些地區有望創造長期成長機會,並成為新的成長前沿。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 人們的健康和衛生意識增強

- 口腔疾病負擔加重

- 產品配方與技術創新

- 人口老化及老年人口腔清潔用品需求

- 轉向天然、草本和環保產品。

- 積極主動的行銷和品牌建設

- 市場限制因素

- 產品安全問題與召回

- 傳統刷牙方法的普及

- 監理和合規挑戰

- 在服務不易取得的地區,人們的意識較低。

- 消費行為分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 依產品類型

- 牙膏

- 漱口水/漱喉液

- 牙刷

- 其他產品類型

- 按成分

- 傳統的

- 天然/有機

- 最終用戶

- 兒童/孩子

- 成人

- 透過分銷管道

- 超級市場和大賣場

- 藥局/藥房

- 線上零售商店

- 其他分銷管道

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 其他北美國家

- 歐洲

- 德國

- 英國

- 義大利

- 法國

- 西班牙

- 荷蘭

- 波蘭

- 比利時

- 瑞典

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 印尼

- 韓國

- 泰國

- 新加坡

- 其他亞太國家

- 南美洲

- 巴西

- 阿根廷

- 哥倫比亞

- 智利

- 秘魯

- 其他南美國家

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 奈及利亞

- 埃及

- 摩洛哥

- 土耳其

- 其他中東和非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- Market Positioning Analysis

- 公司簡介

- Colgate-Palmolive Company

- The Procter & Gamble Company

- Unilever PLC

- Haleon plc

- Church & Dwight Co., Inc.

- Kenvue Inc.

- Henkel AG & Co. KGaA

- LG Household & Health Care Ltd.

- Lion Corporation

- Sunstar Suisse SA

- Koninklijke Philips NV

- Panasonic Corporation

- Water Pik, Inc.

- Dabur India Ltd.

- Himalaya Global Holdings Ltd

- Patanjali Ayurved Limited

- Perrigo Company plc

- Dr. Fresh LLC

- The Humble Co.

- Marico Limited

第7章 市場機會與未來展望

According to Mordor Intelligence, the oral care market, valued at USD 59.06 billion in 2026 and projected to reach USD 80.01 billion by 2031, is expected to grow at a CAGR of 6.26%.

This report is Segmented by Product Type (Toothpaste, Mouthwash/Rinses, and More), Ingredient (Conventional and Natural/Organic), End User (Kids/Children and Adult), Distribution Channel (Supermarkets/Hypermarkets, Drug Stores/Pharmacies, and More), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Oral Care Market Trends and Insights

Growing health and hygiene awareness

Increasing awareness of health and hygiene is a significant factor driving the global oral care market, as consumers increasingly view oral health as a critical aspect of overall well-being. The growing understanding of the connection between poor oral hygiene and systemic conditions, such as cardiovascular disease, diabetes, and infections, has shifted oral care from a basic hygiene practice to a preventive healthcare priority. Educational initiatives in the oral care industry by dental associations, public health organizations, and brands have emphasized the importance of regular brushing, flossing, and the use of complementary products like mouthwashes. This has resulted in higher usage frequency and greater adoption of oral care products. Consumers are now more focused on preventing dental problems rather than addressing them after they occur, fueling demand for functional and therapeutic oral care solutions targeting cavities, gum disease, plaque control, sensitivity, and bad breath. This increased awareness in the oral care market is also driving the adoption of multi-step oral care routines and encouraging experimentation with advanced, specialized, and natural formulations that align with individual health preferences.

Rising burden of oral diseases

The rising prevalence of oral diseases is a significant driver for the global oral care market, as the persistent occurrence of dental conditions has shifted oral hygiene from a discretionary practice to a healthcare necessity. The widespread incidence of tooth decay, cavities, gum disease, and periodontal disorders among both children and adults is fueling demand for preventive and therapeutic oral care products, such as anti-cavity toothpaste, medicated mouthwashes, and gum-care solutions. The clinical and financial implications of untreated oral diseases in the oral care market are encouraging governments, healthcare providers, and consumers to prioritize early intervention and daily oral hygiene. For example, according to the Ministry of Health, in 2025, the prevalence of tooth decay in Saudi Arabia was notably high, affecting 96% of children aged 6 years and 93.7% of children aged 12 years, illustrating the scale of the public health challenge . Furthermore, dental treatments account for approximately 5% of total health spending, highlighting the economic burden of preventable oral conditions. These statistics in the oral care market emphasize the importance of preventive oral care routines and the growing reliance on daily-use products as a cost-effective alternative to clinical treatments.

Product safety concerns and recalls

Product safety concerns and recalls pose a significant restraint on the global oral care market by undermining consumer trust, damaging brand credibility, and slowing the adoption of new formulations and technologies. Oral care products are used daily and come into direct contact with sensitive oral tissues, leading to high safety expectations from both consumers and regulatory authorities. Reports of adverse reactions, contamination, excessive abrasiveness, or malfunctioning devices, such as battery-related issues in electric toothbrushes, can prompt recalls, negative media coverage, and increased regulatory scrutiny. These safety concerns can also delay product launches as companies in the oral care market face stricter testing protocols, reformulation requirements, and extended approval timelines. Additionally, recalls and safety issues can result in financial losses, legal liabilities, and long-term reputational damage for companies. In markets where trust and professional endorsements are crucial, recalls may drive consumers back to familiar or traditional products, thereby limiting category growth and innovation potential.

Other drivers and restraints analyzed in the detailed report include:

- Innovations in product formulations and technology

- Aging population and geriatric oral needs

- Prevalence of traditional way of tooth cleaning

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Toothpaste, which held a dominant 49.76% of the oral care market share in 2025, remains a key driver of the global oral care market due to its essential role in daily oral hygiene and its universal appeal across all age groups. Recognized as the most indispensable oral care product, toothpaste is a high-frequency, repeat-purchase item integrated into daily routines. Its dominance in the oral care market is further bolstered by ongoing innovations in formulations that address diverse oral health needs, including cavity protection, gum care, sensitivity relief, whitening, enamel repair, and fresh breath. These advancements enable brands to meet preventive, therapeutic, and cosmetic demands simultaneously. Additionally, strong endorsements from dentists and public health recommendations emphasizing twice-daily brushing with toothpaste reinforce its habitual use as a cornerstone of oral care practices.

Mouthwash and rinses, anticipated to grow at a CAGR of 6.76% through 2031, are emerging as one of the fastest-growing product categories in the global oral care market. Their increasing adoption is driven by their positioning as a complementary yet essential component of comprehensive oral hygiene routines. Consumers are becoming more aware that brushing alone is insufficient to address issues such as bad breath, plaque buildup, gum inflammation, and bacterial control in hard-to-reach areas. This awareness is accelerating the use of mouthwashes as a daily preventive solution. Furthermore, dentist recommendations and post-procedure oral care guidance are promoting the use of medicated and therapeutic mouth rinses, expanding their application beyond cosmetic breath freshening to include clinical and preventive purposes.

Conventional formulations, which held a dominant 91.38% of the global oral care market share in 2025, are driving the global oral care market due to their established clinical credibility, functional reliability, and widespread use in daily oral hygiene practices. These formulations are based on scientifically validated ingredients, including fluoride and antibacterial agents, which effectively address common oral health concerns such as cavity prevention, plaque control, and gum health. This makes them the preferred choice for both consumers and dental professionals. Additionally, consumer familiarity and trust in these products minimize adoption barriers, ensuring their continued prominence in oral care routines, even as premium and niche alternatives gain market traction.

Organic variants, expected to grow at a CAGR of 7.12% through 2031, are contributing to incremental growth in the global oral care market as consumer preferences shift toward cleaner labels, ingredient transparency, and holistic wellness. This growth is driven by increasing concerns over long-term exposure to synthetic chemicals, prompting consumers to opt for plant-based, herbal, and naturally derived alternatives perceived as gentler and safer for daily use. Organic oral care products appeal strongly to health-conscious consumers, parents, and individuals with sensitivities, as they focus on botanical extracts, essential oils, and mineral-based actives while avoiding harsh additives. The segment is also benefiting from the broader alignment of oral care with wellness and preventive health trends, where oral hygiene is increasingly viewed as an integral part of overall health.

Geography Analysis

The Asia-Pacific region accounted for a significant 29.91% of the global oral care market value in 2025 and is projected to grow at a robust CAGR of 7.83% through 2031, making it the fastest-growing regional market. This growth is driven by increasing oral health awareness, improved preventive care practices, and the adoption of modern oral hygiene routines across urban and semi-urban populations. Factors such as large population bases, a growing emphasis on daily oral care habits, and the expansion of organized retail and e-commerce platforms are accelerating product penetration. Countries like China and India are central to this growth, supported by government-led oral health initiatives, school-based hygiene programs, and the rising acceptance of functional products, including sensitivity, gum care, and herbal formulations. The region's receptiveness in the oral care market to both conventional and natural oral care solutions further solidifies its role as a long-term growth driver.

North America and Europe remain mature regions in the oral care market with steady growth, supported by high oral hygiene awareness, strong dentist influence, and well-established preventive dental care practices. Growth in these regions is primarily driven by product innovation, premiumization, and demand for specialized oral care solutions such as whitening, enamel repair, gum protection, and alcohol-free or therapeutic mouthwashes. Consumers in these markets exhibit high brand loyalty while also showing a willingness to adopt advanced formulations, smart oral care devices, and organic variants. Regulatory clarity, widespread access to dental care services, and robust retail and online distribution networks further contribute to stable market expansion despite the overall maturity of these markets.

South America and the Middle East and Africa remain relatively under-penetrated regions in the oral care market, with growth hindered by price sensitivity, limited access to professional dental care, and the continued prevalence of traditional tooth-cleaning practices such as chewing sticks, herbal powders, or home remedies. In many areas within these regions, oral care is still perceived as a basic hygiene activity rather than a preventive health priority, limiting the adoption of specialized or premium products. Additionally, low awareness of the benefits of modern oral care and uneven retail infrastructure further slow market growth. However, gradual improvements in education, urbanization, and public health outreach are expected to create long-term opportunities, positioning these regions as emerging growth frontiers.

- Colgate-Palmolive Company

- The Procter & Gamble Company

- Unilever PLC

- Haleon plc

- Church & Dwight Co., Inc.

- Kenvue Inc.

- Henkel AG & Co. KGaA

- LG Household & Health Care Ltd.

- Lion Corporation

- Sunstar Suisse SA

- Koninklijke Philips N.V.

- Panasonic Corporation

- Water Pik, Inc.

- Dabur India Ltd.

- Himalaya Global Holdings Ltd

- Patanjali Ayurved Limited

- Perrigo Company plc

- Dr. Fresh LLC

- The Humble Co.

- Marico Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing health and hygiene awareness

- 4.2.2 Rising burden of oral diseases

- 4.2.3 Innovations in product formulations and technology

- 4.2.4 Aging population and geriatric oral needs

- 4.2.5 Shift toward natural, herbal and eco-friendly products

- 4.2.6 Aggressive marketing and brand building

- 4.3 Market Restraints

- 4.3.1 Product safety concerns and recalls

- 4.3.2 Prevalence of traditional way of tooth cleaning

- 4.3.3 Regulatory and compliance challenges

- 4.3.4 Limited awareness in underserved regions

- 4.4 Consumer Behaviour Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Toothpaste

- 5.1.2 Mouthwash/Rinses

- 5.1.3 Toothbrush

- 5.1.4 Other Product Types

- 5.2 By Ingredient

- 5.2.1 Conventional

- 5.2.2 Natural/Organic

- 5.3 By End User

- 5.3.1 Kids/Children

- 5.3.2 Adult

- 5.4 By Distribution Channel

- 5.4.1 Supermarkets/Hypermarkets

- 5.4.2 Drug Stores/Pharmacies

- 5.4.3 Online Retail Stores

- 5.4.4 Others Distribution Channel

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.1.4 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 Italy

- 5.5.2.4 France

- 5.5.2.5 Spain

- 5.5.2.6 Netherlands

- 5.5.2.7 Poland

- 5.5.2.8 Belgium

- 5.5.2.9 Sweden

- 5.5.2.10 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 Australia

- 5.5.3.5 Indonesia

- 5.5.3.6 South Korea

- 5.5.3.7 Thailand

- 5.5.3.8 Singapore

- 5.5.3.9 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Colombia

- 5.5.4.4 Chile

- 5.5.4.5 Peru

- 5.5.4.6 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 South Africa

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 United Arab Emirates

- 5.5.5.4 Nigeria

- 5.5.5.5 Egypt

- 5.5.5.6 Morocco

- 5.5.5.7 Turkey

- 5.5.5.8 Rest of Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Positioning Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Colgate-Palmolive Company

- 6.4.2 The Procter & Gamble Company

- 6.4.3 Unilever PLC

- 6.4.4 Haleon plc

- 6.4.5 Church & Dwight Co., Inc.

- 6.4.6 Kenvue Inc.

- 6.4.7 Henkel AG & Co. KGaA

- 6.4.8 LG Household & Health Care Ltd.

- 6.4.9 Lion Corporation

- 6.4.10 Sunstar Suisse SA

- 6.4.11 Koninklijke Philips N.V.

- 6.4.12 Panasonic Corporation

- 6.4.13 Water Pik, Inc.

- 6.4.14 Dabur India Ltd.

- 6.4.15 Himalaya Global Holdings Ltd

- 6.4.16 Patanjali Ayurved Limited

- 6.4.17 Perrigo Company plc

- 6.4.18 Dr. Fresh LLC

- 6.4.19 The Humble Co.

- 6.4.20 Marico Limited

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

牙刷消毒器市場-2026-2032年全球市場預測

牙刷消毒器市場-2026-2032年全球市場預測 全球口腔護理產品市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球口腔護理產品市場規模、佔有率、趨勢和成長分析報告(2026-2034年) LED口腔護理套裝市場分析及預測(至2035年):類型、產品類型、技術、組件、應用、最終用戶、功能、安裝方式、模式

LED口腔護理套裝市場分析及預測(至2035年):類型、產品類型、技術、組件、應用、最終用戶、功能、安裝方式、模式 歐洲口腔護理:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)口腔護理產品:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

歐洲口腔護理:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)口腔護理產品:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 微生物組驅動的口腔護理市場預測至2034年:按產品類型、微生物菌株類型、配方技術、應用、分銷管道、最終用戶和地區分類的全球分析

微生物組驅動的口腔護理市場預測至2034年:按產品類型、微生物菌株類型、配方技術、應用、分銷管道、最終用戶和地區分類的全球分析 口腔耗材市場規模、佔有率和成長分析:按產品、材料、最終用戶和地區分類-2026-2033年產業預測

口腔耗材市場規模、佔有率和成長分析:按產品、材料、最終用戶和地區分類-2026-2033年產業預測 口腔護理市場報告:趨勢、預測和競爭分析(至2035年)功能性口腔護理市場預測至2034年—全球產品類型、成分類型、功能、劑型、應用、分銷管道、最終用戶和地區分析牙科清潔設備市場:產品類型、電源、應用、分銷管道、最終用途—2026-2032年全球市場預測

口腔護理市場報告:趨勢、預測和競爭分析(至2035年)功能性口腔護理市場預測至2034年—全球產品類型、成分類型、功能、劑型、應用、分銷管道、最終用戶和地區分析牙科清潔設備市場:產品類型、電源、應用、分銷管道、最終用途—2026-2032年全球市場預測