|

市場調查報告書

商品編碼

2066382

口腔護理產品:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Oral Care Products - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

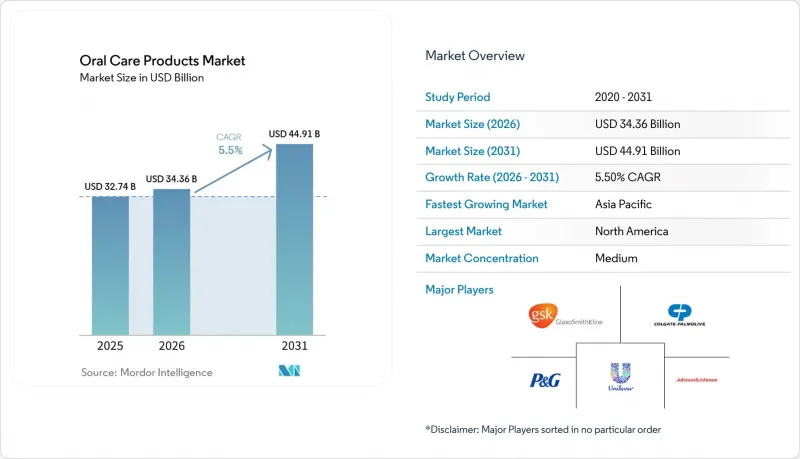

根據 Mordor Intelligence 預測,口腔護理產品市場規模將從 2025 年的 327.4 億美元和 2026 年的 343.6 億美元成長到 2031 年的 449.1 億美元,2026 年至 2031 年的年複合成長率(CAGR)為 5.5%。

本報告按產品類型(例如牙膏)、分銷管道(例如大賣場、超級市場)、最終用戶(例如0-12歲兒童)和地區(北美、歐洲、亞太、中東和非洲、南美)進行細分。市場預測以美元計價。

全球口腔護理產品市場趨勢與洞察

全球齲齒和牙周疾病的盛行率正在上升。

根據世界衛生組織(WHO)的數據,全球有35億人患有口腔疾病,顯示人們對具有臨床療效的日常口腔護理產品有著強勁的需求。 [1] 製造商正在增加活性成分的含量,並將美白和修復琺瑯質的功效結合起來,例如高露潔棕欖公司於2024年推出的Elixir牙膏。由於口腔護理是必需品,即使在景氣衰退時期,該品類的銷售也不會跌至谷底,已開發國家和開發中國家的口腔護理市場都持續成長。

電子商務和D2C(直接面對消費者)分銷的快速擴張。

由於訂閱模式和社群媒體帶來的產品發現,預計到2025年,北美和歐洲的電商市場滲透率將超過品類總銷售額的25%,而中國的天貓和京東等電商平台的這一比例將超過30%。隨著數位原生品牌擺脫商店庫存的限制並維持更高的利潤率,傳統企業被迫推出自己的D2C(直接面對消費者)入口網站和數據驅動的補貨方案。

監管機構對口服製劑中氟化物和二氧化鈦的審查

歐洲食品安全局 (EFSA) 認定二氧化鈦不安全,導致各成員國紛紛更改配方並停產美白牙膏。 [2] 在北美,圍繞氟化物的類似爭論使情況變得複雜,迫使品牌同時提供不含氟和含氟產品,導致 SKU 增加和庫存成本上升。

細分市場分析

漱口水和漱喉液預計將以6.24%的複合年成長率推動銷售成長,這主要得益於不含酒精和添加益生菌的產品,這些產品有助於平衡口腔微生物群。牙膏在2025年將佔銷售額的34.83%,這主要歸功於美白和舒緩敏感等子系列產品,但其市場佔有率正逐漸向功能性漱口水和智慧牙刷轉移。根據目前的成長趨勢,預計到2031年,漱口水口腔護理產品市場規模將超過110億美元。

智慧電動牙刷憑藉著人工智慧指導和遊戲化應用程式,定位高階市場;而牙間刷和牙線則因牙醫主導的宣傳活動而需求激增。高露潔棕欖公司計劃於2024年推出益生菌漱口水,聯合利華公司則推出了酵素活性美白牙膏,這些都反映了口腔護理產品持續創新的趨勢。整體而言,口腔護理產品市場仍呈現兩極化的格局,一邊是銷量高的牙膏,另一邊是利潤豐厚的配件產品類型。

區域分析

預計亞太地區將主導市場,到2025年將佔全球銷售額的32.40%,並有望以6.89%的複合年成長率成長,這主要得益於政府主導的宣傳活動和行動商務的快速發展加速了產品的普及。印度的學校氟化物漱口水計畫和中國的直播購物模式,都促進了市場滲透率的提高以及消費者向高級產品的更換。在日本,人口老化推動了對敏感牙齒和假牙護理產品的需求;而在印尼和越南,電動牙刷的普及率正呈現兩位數的成長。

在北美和歐洲,預計市場將保持溫和成長,這主要得益於優質化和以價值為導向的保險方案。隨著美國保險公司補貼智慧牙刷,以及德國將高氟牙膏納入保險範圍,消費者需求正轉向以科學為基礎的產品。為符合二氧化鈦法規而快速調整產品配方,正在影響歐洲口腔護理產品的市場佔有率,而這種快速適應能力對規模較大、較成熟的公司更有利。

在中東和非洲,清真認證和無酒精漱口水的消費量正在加速成長。同時,在南美洲,儘管經濟波動,巴西和阿根廷的牙膏銷售量依然強勁。在聖保羅和杜拜等都市區,美白產品和智慧設備領域的商機更為集中,這印證了高階細分市場的地域覆蓋範圍之廣。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 全球齲齒和牙周疾病的盛行率正在上升。

- 電子商務和直接面對消費者的銷售模式迅速擴張。

- 新興市場可支配所得成長和都市化加快

- 將口腔微生物益生菌納入日常口腔衛生習慣

- 在基於價值的醫療保健合約中,支付方對預防口腔健康的獎勵

- 企業健康計劃,為智慧口腔清潔用品設備提供補貼

- 市場限制因素

- 監管機構對口服製劑中氟化物和二氧化鈦的審查

- 山梨糖醇、二氧化矽和包裝塑膠等原料價格波動。

- 供應鏈排放目標旨在限制在美白噴霧中使用氣霧劑推進劑。

- 關於分析智慧牙刷使用情況的資料隱私問題。

- 供應鏈分析

- 監理展望

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 依產品類型

- 牙膏

- 貼上

- 凝膠

- 粉末

- 磨料

- 牙刷及相關產品

- 手動的

- 電動(振動式、聲波式、超音波式)

- 電池式牙刷

- 替換牙刷頭

- 漱口水/漱喉液

- 非藥物漱口水

- 含藥漱口水

- 牙科配件/附件

- 牙線

- 緩解口臭的產品

- 用於牙齒美容的美白產品

- 牙科水刀

- 牙科產品

- 定影劑

- 其他義齒相關產品

- 假牙清潔液

- 牙膏

- 透過分銷管道

- 大賣場和超級市場

- 藥局/藥局

- 線上零售

- 最終用戶

- 兒童(0-12歲)

- 13-17歲的青少年

- 成年人(18-59歲)

- 老年人(60歲以上)

- 地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲

- 其他亞太國家

- 中東和非洲

- GCC

- 南非

- 其他中東和非洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 市佔率分析

- 公司簡介

- Church & Dwight Co. Inc.

- Colgate-Palmolive Company

- Dabur India Ltd.

- Dentsply Sirona Inc.

- Dr. Fresh LLC

- GC International AG

- GSK plc

- Henkel AG & Co. KGaA

- Himalaya Wellness Company

- Institut Straumann AG

- Kenvue

- Koninklijke Philips NV

- Lion Corporation

- Panasonic Holdings Corp.

- Procter & Gamble

- Solventum

- Sunstar Suisse SA

- Unilever

- Water Pik, Inc.

- Young Innovations, Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the oral care products market size is projected to expand from USD 32.74 billion in 2025 and USD 34.36 billion in 2026 to USD 44.91 billion by 2031, registering a CAGR of 5.5% between 2026 to 2031.

This report is Segmented by Product Type (Toothpastes, and More), Distribution Channel (Hypermarkets & Supermarkets, and More), End-User (Children (0-12 Yrs) and More), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). Market Forecasts are Provided in Terms of Value (USD).

Global Oral Care Products Market Trends and Insights

Escalating Global Prevalence of Dental Caries and Periodontal Diseases

World Health Organization data indicate that 3.5 billion people live with oral diseases, underscoring the steady demand for daily-use solutions that promise clinical-grade results[1]. Manufacturers are increasing active-ingredient loads and combining whitening with enamel repair, as seen in Colgate-Palmolive's 2024 Elixir toothpaste. The non-discretionary nature of oral care buffers category volumes during economic downturns and sustains growth in both mature and developing countries.

Rapid Expansion of E-Commerce and Direct-to-Consumer Distribution

Subscription models and social media discovery drove e-commerce penetration above 25% of total category sales in North America and Europe in 2025, while China's Tmall and JD.com surpassed 30%. Digital-native brands bypass shelf constraints and maintain healthier margins, prompting incumbents to launch their own proprietary direct-to-consumer (D2C) portals and data-driven replenishment programs.

Regulatory Scrutiny of Fluoride and Titanium Dioxide in Oral Formulations

The European Food Safety Authority ruled titanium dioxide unsafe, triggering reformulation or withdrawal of whitening pastes across member states[2]. Parallel debates over fluoride in North America add complexity, compelling brands to supply both fluoride-free and fluoride-rich options, which raises SKU counts and inventory costs.

Other drivers and restraints analyzed in the detailed report include:

- Rising Disposable Incomes and Urbanization in Emerging Markets

- Integration of Oral Microbiome Probiotics into Daily Hygiene Regimens

- Volatility in Raw-Material Prices for Sorbitol, Silica, and Packaging Plastics

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Mouthwashes and rinses are projected to lead value expansion, climbing at 6.24% CAGR on the back of alcohol-free and probiotic formulas that rebalance the oral microbiome. Toothpaste still generated 34.83% of 2025 revenue, thanks to whitening and sensitivity-relief sublines; however, the share is gradually shifting to functional rinses and smart brushes. The oral care products market size for mouthwashes is expected to exceed USD 11 billion by 2031, based on current growth trajectories.

Smart electric toothbrushes, boosted by AI guidance and app gamification, command premium price points, while interdental brushes and floss benefit from dentist-driven awareness. Colgate-Palmolive's launch of a probiotic mouthwash in 2024 and Unilever's enzyme-activated whitening paste illustrate sustained innovation. Overall, the oral care products market continues to bifurcate between high-volume toothpaste and higher-margin adjunct categories.

Geography Analysis

The Asia-Pacific region dominated with 32.40% revenue in 2025 and is forecasted to grow at a 6.89% CAGR as government campaigns and mobile-commerce growth accelerate uptake. India's school-based fluoride-rinse programs and China's live-stream shopping contribute to both wider penetration and premium trading-up. Japan's aging demographic drives demand for sensitive and denture-care products, while Indonesia and Vietnam experience double-digit growth in electric toothbrush adoption.

North America and Europe are expected to maintain modest growth, buoyed by premiumization and value-based insurance schemes. U.S. carriers subsidize smart brushes, and Germany reimburses high-fluoride pastes, channeling demand into evidence-backed products. The swift reformulation of products influences the oral care products market share in Europe to comply with titanium-dioxide restrictions, a capability that favors scaled incumbents.

The Middle East and Africa are registering an accelerating consumption of halal-certified and alcohol-free rinses. At the same time, South America balances economic volatility with steady toothpaste volumes in Brazil and Argentina. Urban centers such as Sao Paulo and Dubai present concentrated opportunities for whitening and smart devices, confirming the geographic spread of premium niches.

- Church & Dwight

- Colgate-Palmolive Company

- Dabur India Ltd.

- Dentsply Sirona

- Dr. Fresh

- GC International AG

- GlaxoSmithKline

- Henkel

- Himalaya

- Straumann Group

- Kenvue

- Koninklijke Philips

- Lion

- Panasonic Holdings Corp.

- Procter & Gamble

- Solventum

- Sunstar Suisse

- Unilever

- Water Pik

- Young Innovations, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope Of The Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Escalating Global Prevalence of Dental Caries and Periodontal Diseases

- 4.2.2 Rapid Expansion of E-Commerce and Direct-to-Consumer Distribution

- 4.2.3 Rising Disposable Incomes and Urbanization in Emerging Markets

- 4.2.4 Integration of Oral Microbiome Probiotics into Daily Hygiene Regimens

- 4.2.5 Payor Incentivization of Preventive Oral Health Within Value-Based Care Contracts

- 4.2.6 Corporate Wellness Programs Subsidizing Smart Oral Devices

- 4.3 Market Restraints

- 4.3.1 Regulatory Scrutiny of Fluoride and Titanium Dioxide in Oral Formulations

- 4.3.2 Volatility in Raw Material Prices for Sorbitol, Silica, and Packaging Plastics

- 4.3.3 Supply-Chain Emissions Targets Limiting Aerosol Propellant Use in Whitening Sprays

- 4.3.4 Data Privacy Concerns Around Connected Toothbrush Usage Analytics

- 4.4 Supply Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 Toothpaste

- 5.1.1.1 Pastes

- 5.1.1.2 Gels

- 5.1.1.3 Powders

- 5.1.1.4 Polishes

- 5.1.2 Toothbrushes & Accessories

- 5.1.2.1 Manual

- 5.1.2.2 Power (Oscillating, Sonic, Ultrasonic)

- 5.1.2.3 Battery-Powered Toothbrushes

- 5.1.2.4 Replacement Toothbrush Heads

- 5.1.3 Mouthwashes / Rinses

- 5.1.3.1 Non-Medicated Mouthwashes

- 5.1.3.2 Medicated Mouthwashes

- 5.1.4 Dental Accessories / Ancillaries

- 5.1.4.1 Dental Flosses

- 5.1.4.2 Breath Fresheners

- 5.1.4.3 Cosmetic Dental Whitening Products

- 5.1.4.4 Dental Water Jets

- 5.1.5 Dental Products

- 5.1.5.1 Fixatives

- 5.1.5.2 Other Denture Products

- 5.1.6 Dental Prosthesis Cleaning Solutions

- 5.1.1 Toothpaste

- 5.2 By Distribution Channel

- 5.2.1 Hypermarkets & Supermarkets

- 5.2.2 Pharmacies & Drug Stores

- 5.2.3 Online Retail

- 5.3 By End-User

- 5.3.1 Children (0-12 Yrs)

- 5.3.2 Adolescents (13-17 Yrs)

- 5.3.3 Adults (18-59 Yrs)

- 5.3.4 Geriatric (60+ Yrs)

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 South Korea

- 5.4.3.5 Australia

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East And Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (Includes Global-Level Overview, Market-Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products & Services, Recent Developments)

- 6.3.1 Church & Dwight Co. Inc.

- 6.3.2 Colgate-Palmolive Company

- 6.3.3 Dabur India Ltd.

- 6.3.4 Dentsply Sirona Inc.

- 6.3.5 Dr. Fresh LLC

- 6.3.6 GC International AG

- 6.3.7 GSK plc

- 6.3.8 Henkel AG & Co. KGaA

- 6.3.9 Himalaya Wellness Company

- 6.3.10 Institut Straumann AG

- 6.3.11 Kenvue

- 6.3.12 Koninklijke Philips N.V.

- 6.3.13 Lion Corporation

- 6.3.14 Panasonic Holdings Corp.

- 6.3.15 Procter & Gamble

- 6.3.16 Solventum

- 6.3.17 Sunstar Suisse S.A.

- 6.3.18 Unilever

- 6.3.19 Water Pik, Inc.

- 6.3.20 Young Innovations, Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment

牙刷消毒器市場-2026-2032年全球市場預測

牙刷消毒器市場-2026-2032年全球市場預測 全球口腔護理產品市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球口腔護理產品市場規模、佔有率、趨勢和成長分析報告(2026-2034年) LED口腔護理套裝市場分析及預測(至2035年):類型、產品類型、技術、組件、應用、最終用戶、功能、安裝方式、模式

LED口腔護理套裝市場分析及預測(至2035年):類型、產品類型、技術、組件、應用、最終用戶、功能、安裝方式、模式 口腔護理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)歐洲口腔護理:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)

口腔護理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)歐洲口腔護理:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031) 微生物組驅動的口腔護理市場預測至2034年:按產品類型、微生物菌株類型、配方技術、應用、分銷管道、最終用戶和地區分類的全球分析

微生物組驅動的口腔護理市場預測至2034年:按產品類型、微生物菌株類型、配方技術、應用、分銷管道、最終用戶和地區分類的全球分析 口腔耗材市場規模、佔有率和成長分析:按產品、材料、最終用戶和地區分類-2026-2033年產業預測

口腔耗材市場規模、佔有率和成長分析:按產品、材料、最終用戶和地區分類-2026-2033年產業預測 口腔護理市場報告:趨勢、預測和競爭分析(至2035年)功能性口腔護理市場預測至2034年—全球產品類型、成分類型、功能、劑型、應用、分銷管道、最終用戶和地區分析牙科清潔設備市場:產品類型、電源、應用、分銷管道、最終用途—2026-2032年全球市場預測

口腔護理市場報告:趨勢、預測和競爭分析(至2035年)功能性口腔護理市場預測至2034年—全球產品類型、成分類型、功能、劑型、應用、分銷管道、最終用戶和地區分析牙科清潔設備市場:產品類型、電源、應用、分銷管道、最終用途—2026-2032年全球市場預測