|

市場調查報告書

商品編碼

2066504

歐洲口腔護理:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)Europe Oral Care - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

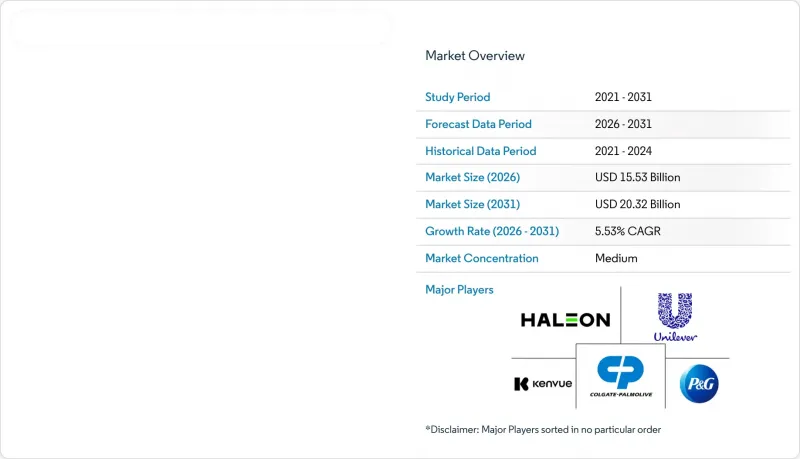

根據 Mordor Intelligence 估計,2026 年歐洲口腔護理市場價值為 155.3 億美元,預計在預測期(2026-2031 年)內將以 5.53% 的複合年成長率成長,到 2031 年達到 203.2 億美元。

本報告按產品類型(牙膏、漱口水/漱喉劑等)、類別(天然/有機、傳統/合成)、最終用戶(兒童、成人)、分銷管道(超級市場/大賣場、藥局/藥房等)和地區(德國、英國、義大利、西班牙等)進行細分。市場預測以美元計價。

歐洲口腔護理市場趨勢與洞察

消費者對天然有機牙膏的需求日益成長

不含合成界面活性劑、人工甜味劑和微塑膠的「潔淨標示」配方正在改變歐洲零售連鎖店的籌資策略。傳統的十二烷基硫酸鈉正被椰子油衍生的界面活性劑所取代,而根據歐盟法規2022/63,二氧化鈦雖然被允許用於食品,但在口腔護理產品中正被自願逐步淘汰。 2024年,Humble公司擴大了竹製牙刷和天然成分牙膏片產品線,在家庭福和樂購等大型超市佔據了原本屬於跨國品牌的貨架空間。同樣在2024年,Denttabs公司推出了含氟牙膏片,回應了長期以來人們對牙膏片形式會影響防齲效果的批評。該產品還符合ISO 11609磨損性標準,表明其已準備好獲得臨床批准。這種轉變並非僅僅由消費者需求所驅動。醫院和療養院的採購負責人正在將永續性標準納入競標規範,並優先考慮已獲得「從搖籃到搖籃」或「歐盟生態標籤」等認證的供應商,這些認證可證明包裝可生物分解且活性成分來源符合道德規範。

消費者對口腔衛生的關注度日益提高

歐洲消費者越來越重視口腔衛生,這推動了口腔護理市場的成長。他們認知到良好的口腔健康直接影響心血管健康、糖尿病管理和呼吸系統健康。這種認知使口腔護理從簡單的日常習慣轉變為重要的健康實踐。老年人更容易出現牙齒問題,因此他們會積極尋找先進的口腔護理產品,並養成良好的口腔衛生習慣。根據經合組織的數據,65歲及以上人口的比例預計將從2023年的21%增加到2050年的30%。人口老化正在積極影響口腔護理市場,他們需要特定的產品。他們需要一些專門的產品,例如用於緩解口乾的牙膏、用於預防牙周疾病的漱口水以及假牙護理產品。這種針對口腔衛生產品的定向需求促使企業開發新的解決方案,並推動了專業口腔護理市場的擴張。

傳統刷牙法的傳播

許多歐洲消費者仍然堅持傳統的口腔清潔用品方法,這阻礙了該地區先進口腔清潔用品的發展。成本考量、對新產品認知度低以及口腔健康教育資源有限,導致許多人繼續使用手動牙刷和普通牙膏。這種趨勢在老年人和農村居民中尤其明顯。許多消費者將口腔清潔用品僅僅視為例行公事,認為每天用手動工具刷牙兩次就足夠了,即使牙醫推薦了最新的替代方案。在中歐和東歐的低收入地區,電動牙刷、牙間清潔工具和治療產品的普及率極低。這種低普及率直接影響了創新口腔衛生產品的銷售。

細分市場分析

到2025年,牙膏將佔據46.38%的市場佔有率,這反映出其作為氟化物主要輸送方式和日常斑塊控制手段的穩固地位。同時,漱口水和漱喉劑的年複合成長率將達到5.97%,到2031年將維持此成長速度,成為所有產品類型中最快的。這種加速成長歸功於無酒精、保護口腔微生物群配方產品的商業化,以應對消費者和臨床醫生日益成長的對抗生素抗藥性和口腔微生物群紊亂的擔憂。 2024年,Haleon推出了Parodontax Active Gum Health漱口水,該產品採用氟化錫和氯化十六烷基吡啶配製而成,旨在解決牙齦出血問題。該配方已獲得德國法定醫療保險的報銷核准,可用於治療牙周炎患者。牙刷(包括手動和電動牙刷)的成長速度較慢,但智慧功能使其價格較高,目前仍僅限於富裕的都市區。其他產品類型,如牙間刷、舌苔清潔器和牙線,雖然只佔很小的市場佔有率,但由於牙醫會將其用於術後護理和正畸維護,因此它們有助於整體銷售量的成長。

漱口水市場的成長趨勢正因與遠端醫療工作流程的協同作用而進一步加速。新冠疫情期間的遠距醫療催生了在線上處方箋治療性漱口水處方的做法,隨著醫療系統減少面對面就診的負擔,這種做法仍在繼續。牙膏領域的創新正轉向給藥方式、微膠囊化美白劑和酵素增強型生物膜破壞技術,這些技術能夠提供兩分鐘刷牙以外的效果。然而,監管方面的延誤正在減緩商業化進程,因為歐盟化妝品法規要求製造商通過多年的臨床試驗來證明新活性成分的安全性和有效性。牙刷市場正日益兩極化:一方面是面向公共採購的超低價手動牙刷,另一方面是可與智慧型手機應用程式連接的高科技電動牙刷,而中等價位的手動牙刷則面臨利潤率壓力。這種細分市場的轉變凸顯了一個更廣泛的趨勢:能夠提供可衡量的健康益處並與數位健康生態系統相連接的產品正在經歷顯著成長,而缺乏差異化的通用產品則面臨著來自自有品牌的價格競爭壓力。

L29:到2025年,傳統和合成產品將佔據89.47%的市場。這主要得益於其成本效益、已確立的臨床證據以及與大規模生產基礎設施的兼容性。然而,在監管利好和採購標準變化的推動下,天然和有機替代品預計將以6.35%的複合年成長率快速成長,直至2031年。歐盟禁止在食品中使用二氧化鈦(如2022/63號法規所規定)產生了連鎖反應,迫使口腔護理品牌自願更改其配方,儘管該成分在化妝品領域的使用仍然合法。為此,聯合利華於2024年推出了“Zendium Complete Protection”,該產品不含合成色素和防腐劑,並採用模擬唾液抗菌特性的天然酶(Glucosidase、葡萄糖氧化酵素、乳過氧化物酶)。

L30:歐洲藥品管理局已批准多種天然活性成分用於治療性口腔護理產品,從而推動了含有檢驗具有健康功效的天然成分產品的開發。世界衛生組織2024年發布的《環境健康決定因素報告》強調,應減少個人保健產品(包括口腔護理產品)中的化學物質暴露,並為天然替代品提供政策支援。根據英國土壤協會統計,2023年英國有機健康和美容產品(包括口腔護理產品)的銷售量有所成長。在科學證據和監管合規的推動下,消費者對天然和有機口腔護理產品的需求正在成長。消費者優先考慮兼具有效性、安全性和環境永續性的口腔護理產品。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 消費者對天然有機牙膏的需求日益成長

- 消費者對口腔衛生的關注度日益提高

- 將智慧科技融入電動牙刷

- 政府在口腔衛生方面採取的積極措施

- 人口老化和牙科保健需求

- 可支配收入和醫療保健成本增加

- 市場限制因素

- 傳統刷牙方法的普及

- 仿冒品會影響品牌聲譽。

- 原物料價格波動

- 監理合規要求

- 消費者需求分析

- 監理展望

- 波特五力模型

第5章 市場規模與成長預測

- 產品類型

- 牙膏

- 漱口水/漱喉液

- 牙刷

- 其他產品類型

- 類別

- 天然/有機

- 常規/合成

- 最終用戶

- 孩子們

- 成人

- 分銷管道

- 超級市場和大賣場

- 藥局/藥房

- 網路商店

- 其他分銷管道

- 地區

- 德國

- 英國

- 義大利

- 法國

- 西班牙

- 荷蘭

- 波蘭

- 比利時

- 瑞典

- 其他歐洲國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Colgate-Palmolive Company

- Procter & Gamble Co.

- Unilever PLC

- Haleon PLC

- Kenvue, Inc.

- Koninklijke Philips NV(Philips Oral Healthcare)

- Sunstar Suisse SA

- Church & Dwight Co., Inc.

- Henkel AG & Co. KGaA

- Pierre Fabre SA

- Hawley & Hazel(BVI)Co., Ltd.

- Denttabs GmbH

- The Humble Co.

- Curaden AG

- TePe Munhygienprodukter AB

- Jordan AS(Orkla)

- GC Corporation(Europe)

- Venture Life Group

- Polished London

- Ludovico Martelli SpA

第7章 市場機會與未來展望

According to Mordor Intelligence, the europe oral care market size is estimated at USD 15.53 billion in 2026, and is expected to reach USD 20.32 billion by 2031, at a CAGR of 5.53% during the forecast period (2026-2031).

This report is Segmented by Product Type (Toothpaste, Mouthwash/Rinses, and More), Category (Natural/Organic, and Conventional/Synthetic), End-User (Kids/Children, and Adult), Distribution Channel (Supermarkets/Hypermarket, Drug Stores/Pharmacies, and More), and Geography (Germany, United Kingdom, Italy, Spain, and More). The Market Forecasts are Provided in Terms of Value (USD).

Europe Oral Care Market Trends and Insights

Rising Demand for Natural and Organic Toothpaste

Clean-label formulations free from synthetic surfactants, artificial sweeteners, and microplastics are reshaping procurement strategies across European retail chains. Conventional sodium lauryl sulfate is yielding to coconut-derived surfactants, while titanium dioxide, banned in food applications under EU Regulation 2022/63, faces voluntary phase-outs in oral care despite remaining legally permissible. The Humble Co. expanded its bamboo toothbrush and natural toothpaste tablet range in 2024, securing listings in Carrefour and Tesco that previously reserved shelf space for multinational brands. Denttabs introduced fluoride-infused toothpaste tablets in 2024, addressing a long-standing criticism that tablet formats compromised caries prevention, and the product achieved ISO 11609 compliance for abrasivity, signaling readiness for clinical endorsement. This shift is not purely consumer-driven; procurement officers at hospital trusts and care homes are embedding sustainability criteria into tender specifications, favoring suppliers with Cradle to Cradle or EU Ecolabel certifications that verify biodegradable packaging and ethically sourced actives.

Increase Consumer Focus on Oral Hygiene

European consumers are actively prioritizing oral hygiene, which drives growth in the oral care market. They recognize that good oral health directly affects cardiovascular health, diabetes management, and respiratory well-being. This understanding has transformed oral care from a simple daily routine into a crucial health practice. Older adults, who experience more dental problems, actively seek advanced oral care products and follow thorough hygiene routines. According to the OECD, the population aged 65 and older will grow from 21% in 2023 to 30% by 2050 . This aging population actively shapes the oral care market by demanding specific products. They need specialized items like dry mouth toothpaste, anti-gum disease mouthwashes, and denture care solutions. Their requirements for targeted oral health products drive companies to develop new solutions and expand the specialized oral care market.

Prevalence of Traditional Way of Tooth Cleaning

European consumers largely stick to traditional oral care methods, which restricts the growth of advanced oral care products in the region. Many people continue to use manual toothbrushes and basic toothpaste due to cost concerns, lack of awareness about newer products, and limited access to dental education. This behavior is especially common among the elderly and rural populations. Most consumers treat oral care as a simple daily task and believe brushing twice a day with manual tools meets their needs, even when dentists recommend modern alternatives. Lower-income regions in Central and Eastern Europe show minimal adoption of electric toothbrushes, interdental cleaning tools, and therapeutic products. This low adoption directly impacts sales of innovative oral hygiene products.

Other drivers and restraints analyzed in the detailed report include:

- Integration of Smart Technologies in Electric Toothbrush

- Favorable Government Initiatives on Oral Hygiene

- Counterfeit Products Affecting Brand Reputation

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Toothpaste held a 46.38% share in 2025, reflecting its entrenched position as the primary vehicle for fluoride delivery and daily plaque control, yet mouthwash and rinses are expanding at a 5.97% CAGR through 2031, the fastest pace among product categories. This acceleration stems from the commercialization of alcohol-free, microbiome-preserving formulations that address growing consumer and clinical concerns about antimicrobial resistance and oral dysbiosis. Haleon introduced Parodontax Active Gum Health mouthwash in 2024, incorporating stannous fluoride and cetylpyridinium chloride to target bleeding gums, a formulation that secured reimbursement approval under Germany's statutory health insurance for patients with diagnosed periodontitis. Toothbrushes, encompassing both manual and electric variants, are growing at a moderate pace as smart features command premium pricing but remain confined to affluent urban segments. Other product types, interdental brushes, tongue scrapers, and dental floss, serve niche roles yet collectively contribute incremental volume as dentists prescribe them for post-surgical care and orthodontic maintenance.

Mouthwash's trajectory is further amplified by its compatibility with telemedicine workflows; remote consultations during the COVID-19 pandemic normalized virtual prescriptions for therapeutic rinses, a practice that persists as health systems seek to reduce in-person visit loads. Toothpaste innovation is shifting toward delivery mechanisms, microencapsulated whitening agents, and enzyme-enhanced biofilm disruption that extend efficacy beyond the 2-minute brushing window, yet regulatory inertia slows commercialization as the EU Cosmetics Regulation requires manufacturers to demonstrate safety and efficacy for novel actives through multi-year clinical trials. Toothbrushes are bifurcating into ultra-low-cost manual variants for public procurement and high-tech electric models that integrate with smartphone apps, leaving mid-priced manual brushes in a margin squeeze. The segment's evolution underscores a broader pattern: products that enable measurable health outcomes and align with digital health ecosystems are capturing disproportionate growth, while undifferentiated commodity offerings face pricing pressure from private-label competition.

L29: Conventional and synthetic products commanded an 89.47% share in 2025, sustained by their cost efficiency, established clinical evidence, and compatibility with mass-production infrastructure, yet natural and organic alternatives are accelerating at a 6.35% CAGR through 2031, driven by regulatory tailwinds and shifting procurement criteria. The EU's ban on titanium dioxide in food applications, codified in Regulation 2022/63, created a halo effect that pressured oral care brands to voluntarily reformulate despite the ingredient's continued legality in cosmetics, with Unilever's Zendium Complete Protection, launched in 2024, eliminating synthetic colorants and preservatives in favor of natural enzymes (amyloglucosidase, glucose oxidase, and lactoperoxidase) that mimic saliva's antimicrobial properties.

L30: The European Medicines Agency has approved multiple naturally derived active ingredients for therapeutic oral care products, enabling natural formulations with validated health claims. The WHO's 2024 report on environmental determinants of health emphasizes reducing chemical exposure through personal care products, including oral care, and providing policy support for natural alternatives. The sales value of organic health and beauty products, including oral care, in the United Kingdom increased in 2023, according to the Soil Association . The demand for natural and organic oral care products has grown, driven by scientific research validation and regulatory compliance. Consumers are prioritizing oral care products that combine effectiveness with safety and environmental sustainability.

List of Companies Covered in this Report:

- Colgate-Palmolive Company

- Procter & Gamble Co.

- Unilever PLC

- Haleon PLC

- Kenvue, Inc.

- Koninklijke Philips N.V. (Philips Oral Healthcare)

- Sunstar Suisse S.A.

- Church & Dwight Co., Inc.

- Henkel AG & Co. KGaA

- Pierre Fabre S.A.

- Hawley & Hazel (BVI) Co., Ltd.

- Denttabs GmbH

- The Humble Co.

- Curaden AG

- TePe Munhygienprodukter AB

- Jordan AS (Orkla)

- GC Corporation (Europe)

- Venture Life Group

- Polished London

- Ludovico Martelli SpA

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising demand for natural and organic toothpaste

- 4.2.2 Increase consumer focus on oral hygiene

- 4.2.3 Integration of smart technologies in electric toothbrush

- 4.2.4 Favorable government initiatives on oral-hygiene

- 4.2.5 Aging population and dental health needs

- 4.2.6 Rising disposable income and healthcare spending

- 4.3 Market Restraints

- 4.3.1 Prevalence of traditional way of tooth cleaning

- 4.3.2 Counterfeit products affecting brand reputation

- 4.3.3 Raw material price fluctuations

- 4.3.4 Regulatory compliance requirements

- 4.4 Consumer Demand Analysis

- 4.5 Regulatory Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 Product Type

- 5.1.1 Toothpaste

- 5.1.2 Mouthwash/Rinses

- 5.1.3 Toothbrush

- 5.1.4 Other Product Types

- 5.2 Category

- 5.2.1 Natural/Organic

- 5.2.2 Conventional/Synthetic

- 5.3 End-User

- 5.3.1 Kids/Children

- 5.3.2 Adult

- 5.4 Distribution Channel

- 5.4.1 Supermarkets/Hypermarkets

- 5.4.2 Drug Stores/Pharmacies

- 5.4.3 Online Stores

- 5.4.4 Other Distribution Channels

- 5.5 Geography

- 5.5.1 Germany

- 5.5.2 United Kingdom

- 5.5.3 Italy

- 5.5.4 France

- 5.5.5 Spain

- 5.5.6 Netherlands

- 5.5.7 Poland

- 5.5.8 Belgium

- 5.5.9 Sweden

- 5.5.10 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Colgate-Palmolive Company

- 6.4.2 Procter & Gamble Co.

- 6.4.3 Unilever PLC

- 6.4.4 Haleon PLC

- 6.4.5 Kenvue, Inc.

- 6.4.6 Koninklijke Philips N.V. (Philips Oral Healthcare)

- 6.4.7 Sunstar Suisse S.A.

- 6.4.8 Church & Dwight Co., Inc.

- 6.4.9 Henkel AG & Co. KGaA

- 6.4.10 Pierre Fabre S.A.

- 6.4.11 Hawley & Hazel (BVI) Co., Ltd.

- 6.4.12 Denttabs GmbH

- 6.4.13 The Humble Co.

- 6.4.14 Curaden AG

- 6.4.15 TePe Munhygienprodukter AB

- 6.4.16 Jordan AS (Orkla)

- 6.4.17 GC Corporation (Europe)

- 6.4.18 Venture Life Group

- 6.4.19 Polished London

- 6.4.20 Ludovico Martelli SpA

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

牙刷消毒器市場-2026-2032年全球市場預測

牙刷消毒器市場-2026-2032年全球市場預測 全球口腔護理產品市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球口腔護理產品市場規模、佔有率、趨勢和成長分析報告(2026-2034年) LED口腔護理套裝市場分析及預測(至2035年):類型、產品類型、技術、組件、應用、最終用戶、功能、安裝方式、模式

LED口腔護理套裝市場分析及預測(至2035年):類型、產品類型、技術、組件、應用、最終用戶、功能、安裝方式、模式 口腔護理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)口腔護理產品:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

口腔護理:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)口腔護理產品:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 微生物組驅動的口腔護理市場預測至2034年:按產品類型、微生物菌株類型、配方技術、應用、分銷管道、最終用戶和地區分類的全球分析

微生物組驅動的口腔護理市場預測至2034年:按產品類型、微生物菌株類型、配方技術、應用、分銷管道、最終用戶和地區分類的全球分析 口腔耗材市場規模、佔有率和成長分析:按產品、材料、最終用戶和地區分類-2026-2033年產業預測

口腔耗材市場規模、佔有率和成長分析:按產品、材料、最終用戶和地區分類-2026-2033年產業預測 口腔護理市場報告:趨勢、預測和競爭分析(至2035年)功能性口腔護理市場預測至2034年—全球產品類型、成分類型、功能、劑型、應用、分銷管道、最終用戶和地區分析牙科清潔設備市場:產品類型、電源、應用、分銷管道、最終用途—2026-2032年全球市場預測

口腔護理市場報告:趨勢、預測和競爭分析(至2035年)功能性口腔護理市場預測至2034年—全球產品類型、成分類型、功能、劑型、應用、分銷管道、最終用戶和地區分析牙科清潔設備市場:產品類型、電源、應用、分銷管道、最終用途—2026-2032年全球市場預測