|

市場調查報告書

商品編碼

2066464

地熱能:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Geothermal Energy - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

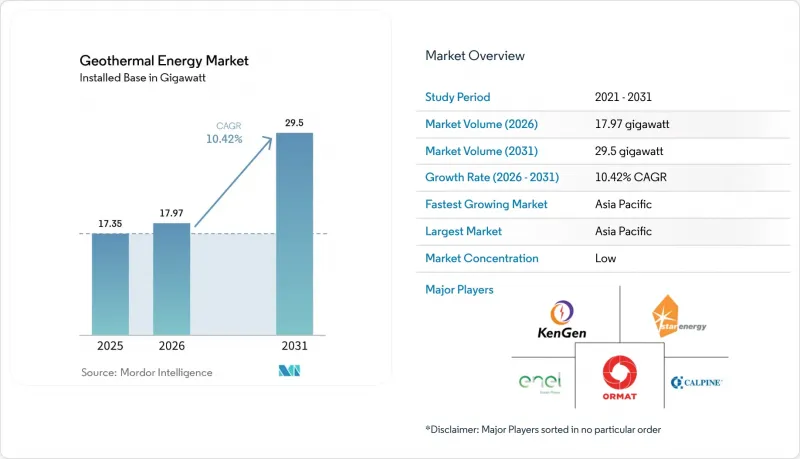

根據 Mordor Intelligence 預測,地熱能源市場(按裝置容量計算)預計將從 2025 年的 17.35 吉瓦和 2026 年的 17.97 吉瓦成長到 2031 年的 29.5 吉瓦,2026 年至 2031 年的年複合成長率(CAGR)。

本報告按電廠類型(乾蒸汽電廠、閃化蒸氣電廠、雙回圈電廠、聯合循環/混合電廠和增強型地熱系統)、應用(發電、區域供熱和製冷以及工業熱利用)和地區(北美、歐洲、亞太地區、南美以及中東和非洲)進行分類。

全球地熱能市場趨勢及洞察

政府獎勵基本負載可再生能源,並擴大上網電價補貼(FIT)制度。

上網電價補貼(FIT)和基於容量的支付機制正在重塑專案的經濟可行性,確保收入來源以抵消探勘風險。印尼將地熱上網電價提高至2025年每千瓦時1450印尼幣,這項12%的溢價加速了蘇門答臘島和蘇拉威西島的井場和現場作業。土耳其將上網電價補貼保障期限延長至2030年,促進了八座總裝置容量總合320兆瓦的新型雙回圈發電廠的建設。肯亞透過引進國家擔保鑽井保險,直接解決了私人資金籌措的最大障礙,該保險可賠償高達70%的井損失。歐盟將地熱發電的授權期限縮短至18個月以內,從而縮短了專案前置作業時間,提高了銀行貸款的接受度。在太陽能和風能發電上限已超過15%的市場中,這些舉措正在將投機性礦區轉變為可投資資產。

地源熱泵安裝擴建

地源熱泵的安裝正在形成一個獨立於發電的平行需求管道。在美國,一項30%的聯邦稅額扣抵預計將推動寒冷州的住宅熱泵系統安裝量在2025年前增加41%。在德國,隨著《建築節能法》逐步淘汰燃氣鍋爐,已發放了8.7萬張新的許可證。在瑞典,區域供熱廠大規模安裝地源熱泵已使營運成本維修了35%,並提高了季節性能係數。在日本,為了在2028年將建築物的石化燃料使用量減少20%,政府已累計180億日圓用於商業設施的維修。承包商認為該行業利潤豐厚且風險低,因為淺層鑽探避免了深層地質構造的不確定性。

初期鑽井風險高,且需要大量資金投入。

在未開發盆地,探勘井的成功率僅為55%至65%,一口乾井的成本可能高達800萬美元,這使得資金籌措變得困難。鑽井成本佔總資本投資的40%至50%,如果油井滲透率低,一口失敗的油井就可能導致一個20兆瓦的專案功虧一簣。在肯亞的梅嫩蓋油田,成功率僅38%,導致4,700萬美元的減損損失和18個月的工期延誤。在印尼的薩拉計畫中,意料之外的儲存分隔導致成本超支23%。雖然風險緩解基金可以部分彌補損失,但開發商仍面臨儲存性能的不確定性,因此將資金轉移到已有地下數據的維修工作。

細分市場分析

至2025年,閃蒸式蒸氣發電廠將佔總發電量的47.50%。這反映了其在印尼和菲律賓等高焓地熱區的長期成功經驗。該領域受益於成熟的供應鏈和成熟的儲存管理技術,將鑽井風險控制在較低水準。然而,隨著頁岩增產技術使得在以往獲利能力的乾熱岩層中形成儲存成為可能,預計到2031年,增強型地熱系統(EGS)的全球市場規模將以18.80%的複合年成長率成長。內華達州和猶他州的成功試點計畫表明,其成本基準約為每兆瓦420萬美元,與冷地熱田的雙循環地熱發電廠相當。雖然在「蓋瑟斯」等傳統地熱田仍採用乾蒸汽法,但隨著蒸氣地熱田的枯竭,其使用量正逐漸減少。雙回圈技術持續在歐洲低焓地熱市場得到應用,透過有機朗肯循環汽輪機減少85%的用水量,從而增強了全球地熱能源產業的實力。

增強型地熱系統(EGS)的發展動能正在改變供應鏈動態。擁有水平鑽井技術專長的服務公司紛紛湧入市場,加劇了套管、支撐劑和增產作業團隊的競爭。設備供應商則以模組化地上電站來應對,從而縮短建設週期。在高度偏遠的地區,採用聯合循環的混合系統正在興起,該系統將太陽能集熱器和地熱井置於同一地點,無需安裝新的渦輪機即可提高白天的發電量,並引領全球地熱能源市場向一體化可再生能源中心邁進。

區域分析

預計到2025年,亞太地區將佔全球地熱能源市場佔有率的44.27%,並在2031年之前以11.9%的複合年成長率成長。這主要得益於印尼計劃運作3.3吉瓦的新增發電裝置容量以及菲律賓簡化許可程序。 2025年,印尼國家石油公司(Pertamina Geothermal Energy)將在蘇門答臘島的三個油田新增總計165兆瓦的裝置容量,而星能公司(Star Energy)將在薩拉克油田完成110兆瓦的擴建項目,從而儲存的壽命延長18年。在日本,溫泉度假區附近的鑽探限制已解除,使得420平方公里的區域探勘。對此,三菱電力公司提案了在別府建設一座30兆瓦發電廠的計劃,預計將於2027年投入運作。中國持續致力於直接利用地下水供熱,目前華北平原淺層含水層提供的住宅供熱成本僅為燃煤鍋爐的三分之一。

在北美,隨著美國土地管理局於2025年發放47份總面積達7.8萬英畝的土地租賃契約,吸引了1.42億美元的額外競標,創下2008年以來的最高紀錄,北美地區出現了復甦的跡象。奧瑪特科技公司(Ormat Technologies)利用先前被認為獲利能力的度C155度流體雙回圈,將其蒸汽船綜合設施的裝置容量擴大了18兆瓦。加拿大設立了5,000萬加元的探勘基金,旨在維修枯竭的天然氣井。墨西哥聯邦電力委員會(CFE)目前擁有963兆瓦的裝置容量,但自2015年預算削減以來,新計畫寥寥無幾。

相較之下,歐洲、中東和非洲的發展趨勢則有所不同。土耳其將在2025年新增95兆瓦的雙回圈發電裝置容量,並享有10年電價保障,使其總裝置容量達到1.7吉瓦。冰島的裝置容量穩定在755兆瓦,其開發人員目前正在出口地熱電解制取的可再生氫氣。肯亞已在奧爾卡里亞五號水力發電廠建成兩台35兆瓦的機組,使其裝置容量提升至985兆瓦。此外,奧爾卡里亞一號水力發電廠計畫在2027年前新增140兆瓦的裝置容量。衣索比亞的圖爾莫耶水力發電廠計畫已獲得8億美元的資金籌措,目標是在2029年前建成520兆瓦的裝置容量。同時,由於安地斯山脈輸電成本高昂,智利目前唯一運作中的電廠是裝置容量為48兆瓦的塞羅帕維利翁水力發電廠。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 政府獎勵基本負載可再生能源,並擴大上網電價補貼(FIT)制度。

- 地源熱泵安裝擴建

- 全天候綠色電力對能源安全的需求日益成長。

- 將閒置油氣井改造為封閉回路型熱發電

- 新興的地熱能氫氣基地

- 市場限制因素

- 初期鑽井風險高,且需要大量資金投入。

- 來自太陽能和風能發電的成本競爭壓力

- 全球熟練地熱鑽井工人短缺

- 供應鏈分析

- 監理情勢

- 技術展望

- 現有及未來重大項目

- 投資與資金籌措分析

- 波特五力模型

第5章 市場規模與成長預測

- 按植物類型

- 乾蒸汽裝置

- 蒸氣裝置

- 雙回圈發電廠

- 聯合循環混合動力發電廠

- 增強型地熱系統(EGS)

- 透過使用

- 發電

- 區域供暖和製冷

- 工業製程熱

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 法國

- 英國

- 西班牙

- 北歐國家

- 土耳其

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 印尼

- 菲律賓

- 澳洲

- 其他亞太國家

- 南美洲

- 巴西

- 阿根廷

- 哥倫比亞

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 肯亞

- 奈及利亞

- 南非

- 其他中東和非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略性措施(併購、合資、資金籌措、購電協議)

- 市場佔有率分析(主要公司的市場排名和佔有率)

- 公司簡介

- Ormat Technologies Inc.

- Enel Green Power

- Calpine Corporation

- Toshiba Energy Systems & Solutions

- Mitsubishi Power Ltd.

- Fuji Electric Co. Ltd.

- Ansaldo Energia SpA

- Baker Hughes Company

- Turboden

- PT Pertamina Geothermal Energy

- Star Energy Geothermal

- KenGen(Kenya Electricity Generating Co.)

- ENGIE SA

- Aboitiz Power Corporation

- First Gen Corporation

- Sosian Energy Ltd.

- Tetra Tech Inc.

- Alterra Power Corp.

- Contact Energy

- Fervo Energy

第7章 市場機會與未來展望

According to Mordor Intelligence, the geothermal energy market size in terms of installed base is projected to expand from 17.35 gigawatt in 2025 and 17.97 gigawatt in 2026 to 29.5 gigawatt by 2031, registering a CAGR of 10.42% between 2026 to 2031.

This report is Segmented by Plant Type (Dry Steam Plants, Flash Steam Plants, Binary Cycle Plants, Combined Cycle/Hybrid Plants, and Enhanced Geothermal Systems), Application (Electricity Generation, District Heating and Cooling, and Industrial Process Heat), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa).

Global Geothermal Energy Market Trends and Insights

Rising Government Incentives & FiTs for Baseload Renewables

Feed-in tariffs and capacity payments are reshaping project economics by locking in revenue streams that neutralize exploration risk. Indonesia lifted its geothermal tariff to IDR 1,450 per kWh in 2025, a 12% premium that accelerated well-field work in Sumatra and Sulawesi. Turkey extended its tariff guarantee to 2030, triggering eight new binary-cycle plants totaling 320 MW. Kenya introduced sovereign drilling insurance that now covers up to 70% of well losses, directly addressing the single largest barrier to private finance. The European Union shortened geothermal permitting to below 18 months, improving project lead times and bankability. These moves convert speculative acreage into investable assets in markets where solar and wind curtailment already exceeds 15%.

Growing Deployment of Geothermal Heat Pumps

Ground-source heat-pump installations are creating a parallel demand channel that is independent of electricity generation. A 30% U.S. federal tax credit drove a 41% year-on-year jump in residential systems during 2025 in cold-climate states. Germany issued 87,000 new permits as gas boilers are phased out under the Building Energy Act. Sweden retrofitted district-heating plants with large-scale pumps that cut operating costs by 35% and improved seasonal performance ratios. Japan earmarked JPY 18 billion in subsidies for commercial retrofits, pursuing a 20% fossil-fuel reduction in buildings by 2028. Contractors see this segment as high margin and low risk because shallow drilling avoids deep subsurface uncertainty.

High Upfront Drilling Risk & Capex

Exploration wells succeed only 55%-65% of the time in frontier basins, with dry-hole costs up to USD 8 million, making financing difficult. Drilling consumes 40%-50% of total capex, and one failed well can sink a 20 MW project if permeability is poor. Kenya's Menengai field saw only a 38% success rate, causing USD 47 million in write-offs and 18-month delays. Indonesia's Sarulla project ended 23% over budget due to unexpected reservoir compartmentalization. Risk-mitigation funds cover part of the loss, but developers remain exposed to reservoir performance uncertainty, steering capital toward retrofits with known subsurface data.

Other drivers and restraints analyzed in the detailed report include:

- Heightened Energy-Security Needs for 24/7 Green Power

- Repurposing Idle Oil & Gas Wells for Closed-Loop Geothermal

- Cost-Competitive Pressure from Solar & Wind

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Flash-steam plants represented 47.50% of capacity in 2025, reflecting their long track record in high-enthalpy zones across Indonesia and the Philippines. The segment benefits from established supply chains and proven reservoir management practices, keeping drilling risk moderate. However, the global geothermal energy market size for Enhanced Geothermal Systems is projected to expand at an 18.80% CAGR to 2031 as shale-style stimulation creates reservoirs in previously uneconomic hot-dry-rock formations. Pilot successes in Nevada and Utah validated cost benchmarks near USD 4.2 million per MW, on par with binary plants in lower-temperature fields. Dry-steam configurations persist at legacy sites like The Geysers but face a gradual decline as vapor-dominated fields deplete. Binary-cycle technology continues to serve low-enthalpy markets in Europe, where organic Rankine turbines cut water use by 85%, strengthening the global geothermal energy industry mix.

EGS momentum is altering supply-chain dynamics. Service companies with horizontal-drilling expertise are entering the market, increasing competition for casing, proppant, and stimulation crews. Equipment vendors respond with modular surface plants that shorten construction timelines. Combined-cycle hybrids that co-locate solar collectors with geothermal wells are emerging in regions with strong isolation, adding daytime output without new turbines and nudging the global geothermal energy market toward integrated renewable hubs.

Geography Analysis

Asia-Pacific held a 44.27% global geothermal energy market share in 2025 and is projected to grow at an 11.9% CAGR through 2031, supported by Indonesia's plan to commission 3.3 GW of new capacity and the Philippines' streamlined permitting framework. Indonesia's Pertamina Geothermal Energy added 165 MW across three Sumatra fields in 2025, and Star Energy completed a 110 MW expansion at Salak to prolong reservoir life by 18 years. Japan removed drilling limits near onsen resorts, opening 420 km2 for exploration and prompting Mitsubishi Power to propose a 30 MW plant in Beppu slated for 2027. China continues to focus on direct-use heating; shallow aquifers in the North China Plain now supply residential heat at one-third the cost of coal boilers.

North America is experiencing a resurgence as the U.S. Bureau of Land Management issued 47 leases covering 78 000 acres in 2025, attracting USD 142 million in bonus bids, the highest since 2008. Ormat Technologies expanded the Steamboat complex by 18 MW using binary cycles that tap 155 °C fluids formerly deemed sub-economic. Canada's CAD 50 million exploration fund targets retrofits in depleted gas wells, while Mexico's Comision Federal de Electricidad maintains 963 MW but lacks fresh projects after 2015 budget cuts.

Europe, the Middle East, and Africa reveal contrasting trajectories. Turkey reached 1.7 GW after adding 95 MW of binary-cycle capacity in 2025 under a 10-year tariff guarantee. Iceland's installed base is steady at 755 MW, with developers now exporting renewable hydrogen from geothermal electrolysis. Kenya lifted its capacity to 985 MW after completing two 35 MW units at Olkaria V, and a further 140 MW is planned at Olkaria I by 2027. Ethiopia's Tulu Moye project secured a USD 800 million package to target 520 MW by 2029, while Chile's only operating plant remains Cerro Pabellon at 48 MW amid high Andean transmission costs.

- Ormat Technologies Inc.

- Enel Green Power

- Calpine Corporation

- Toshiba Energy Systems & Solutions

- Mitsubishi Power Ltd.

- Fuji Electric Co. Ltd.

- Ansaldo Energia SpA

- Baker Hughes Company

- Turboden

- PT Pertamina Geothermal Energy

- Star Energy Geothermal

- KenGen (Kenya Electricity Generating Co.)

- ENGIE SA

- Aboitiz Power Corporation

- First Gen Corporation

- Sosian Energy Ltd.

- Tetra Tech Inc.

- Alterra Power Corp.

- Contact Energy

- Fervo Energy

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising government incentives & FiTs for baseload renewables

- 4.2.2 Growing deployment of geothermal heat pumps

- 4.2.3 Heightened energy-security needs for 24/7 green power

- 4.2.4 Repurposing idle oil & gas wells for closed-loop geothermal

- 4.2.5 Emerging geothermal-to-hydrogen production hubs

- 4.3 Market Restraints

- 4.3.1 High upfront drilling risk & capex

- 4.3.2 Cost-competitive pressure from solar & wind

- 4.3.3 Global shortage of specialised geothermal drill crews

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Existing and Key Upcoming Projects

- 4.8 Investment & Financing Analysis

- 4.9 Porter's Five Forces

- 4.9.1 Bargaining Power of Suppliers

- 4.9.2 Bargaining Power of Consumers

- 4.9.3 Threat of New Entrants

- 4.9.4 Threat of Substitute Products & Services

- 4.9.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Plant Type

- 5.1.1 Dry Steam Plants

- 5.1.2 Flash Steam Plants

- 5.1.3 Binary Cycle Plants

- 5.1.4 Combined Cycle/Hybrid Plants

- 5.1.5 Enhanced Geothermal Systems (EGS)

- 5.2 By Application

- 5.2.1 Electricity Generation

- 5.2.2 District Heating and Cooling

- 5.2.3 Industrial Process Heat

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 France

- 5.3.2.3 United Kingdom

- 5.3.2.4 Spain

- 5.3.2.5 NORDIC Countries

- 5.3.2.6 Turkey

- 5.3.2.7 Russia

- 5.3.2.8 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 Indonesia

- 5.3.3.6 Philippines

- 5.3.3.7 Australia

- 5.3.3.8 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 Kenya

- 5.3.5.4 Nigeria

- 5.3.5.5 South Africa

- 5.3.5.6 Rest of Middle East and Africa

- 5.3.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, JVs, Funding, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Products & Services, Recent Developments)

- 6.4.1 Ormat Technologies Inc.

- 6.4.2 Enel Green Power

- 6.4.3 Calpine Corporation

- 6.4.4 Toshiba Energy Systems & Solutions

- 6.4.5 Mitsubishi Power Ltd.

- 6.4.6 Fuji Electric Co. Ltd.

- 6.4.7 Ansaldo Energia SpA

- 6.4.8 Baker Hughes Company

- 6.4.9 Turboden

- 6.4.10 PT Pertamina Geothermal Energy

- 6.4.11 Star Energy Geothermal

- 6.4.12 KenGen (Kenya Electricity Generating Co.)

- 6.4.13 ENGIE SA

- 6.4.14 Aboitiz Power Corporation

- 6.4.15 First Gen Corporation

- 6.4.16 Sosian Energy Ltd.

- 6.4.17 Tetra Tech Inc.

- 6.4.18 Alterra Power Corp.

- 6.4.19 Contact Energy

- 6.4.20 Fervo Energy

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

2034 年超高溫岩石地熱市場預測:按資源類型、發電能力、技術、應用、最終用戶和地區進行全球分析。深層地熱能市場預測至2034年:按資源類型、發電容量、技術、最終用戶和地區分類的全球分析

2034 年超高溫岩石地熱市場預測:按資源類型、發電能力、技術、應用、最終用戶和地區進行全球分析。深層地熱能市場預測至2034年:按資源類型、發電容量、技術、最終用戶和地區分類的全球分析 地熱能市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、應用、地區和競爭格局分類,2021-2031年地熱能源系統市場預測至2034年—按類型、資源類型、組件、技術、應用、最終用戶和地區分類的全球分析

地熱能市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、應用、地區和競爭格局分類,2021-2031年地熱能源系統市場預測至2034年—按類型、資源類型、組件、技術、應用、最終用戶和地區分類的全球分析 地熱能市場:依技術、組件、應用和最終用途分類-2026-2032年全球市場預測

地熱能市場:依技術、組件、應用和最終用途分類-2026-2032年全球市場預測 地熱能源市場機會、成長要素、產業趨勢分析及2026-2035年預測。

地熱能源市場機會、成長要素、產業趨勢分析及2026-2035年預測。 全球地熱能源市場規模、佔有率、趨勢和成長分析報告:2026-2034年

全球地熱能源市場規模、佔有率、趨勢和成長分析報告:2026-2034年 2026年全球地熱能源市場報告

2026年全球地熱能源市場報告 地熱能市場規模、佔有率和成長分析(按類型、模式、深度、溫度、功率、應用、最終用途和地區分類)-2026-2033年產業預測地熱能市場預測至2032年:按電站類型、組件、技術、應用、最終用戶和地區分類的全球分析

地熱能市場規模、佔有率和成長分析(按類型、模式、深度、溫度、功率、應用、最終用途和地區分類)-2026-2033年產業預測地熱能市場預測至2032年:按電站類型、組件、技術、應用、最終用戶和地區分類的全球分析