|

市場調查報告書

商品編碼

1982350

地熱能源市場機會、成長要素、產業趨勢分析及2026-2035年預測。Geothermal Energy Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

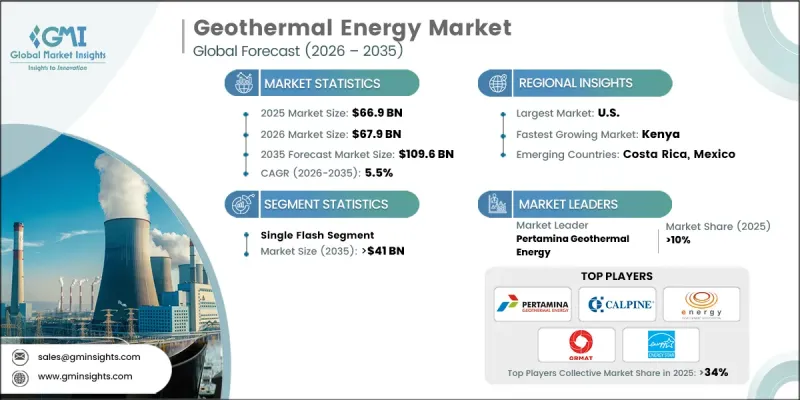

預計到 2025 年,全球地熱能源市場價值將達到 669 億美元,並將以 5.5% 的複合年成長率成長,到 2035 年達到 1,096 億美元。

該市場受清潔農業電力採購義務的驅動,這些義務旨在保障電網可靠性並優先發展高運轉率地熱資源。較低的計劃成本、透過學習效應實現的績效提升以及電力公司監管支持的採購,為長期回報提供了保障,並增強了投資的合法性。企業正擴大利用底部循環汽電共生技術最佳化現有棕地,以重複利用現有油井和蒸氣田,並快速擴大發電能力。對能源安全的擔憂和優惠融資政策促成了世界首批地熱發電廠在小規模島嶼地區的建設。市場成長依然緩慢且集中,現有設施的擴建是主要趨勢。政策制定者正將地熱定位為可靠的能源,以補充可變可再生能源,而先進的地熱技術正從研發階段邁向現場示範階段,從而擴大了可應用的地質類型和計劃。實施挑戰和併網限制正在影響採購趨勢,分階段部署是首選方案。亞洲各國政府主導的措施正在擴大可用資金籌措管道,加劇計劃開發權的競爭,而對現有發電廠進行改造和提高產量,比新建待開發區發電廠能更快地在短期內增加發電量。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 669億美元 |

| 預測金額 | 1096億美元 |

| 複合年成長率 | 5.5% |

預計2025年,單閃蒸地熱發電市場佔有率將達35.9%,2035年將達410億美元。單閃蒸系統將高壓地熱水轉化為蒸氣驅動汽輪機,剩餘流體則重新註入儲存。其成熟的技術、簡單的操作以及在高溫地熱田中的高效性使其成為全球領先的地熱解決方案。

預計2025年,美國地熱能源市場規模將達155億美元。這一成長反映了對可再生能源投資的增加、對低排放電力需求的成長以及政府為促進清潔能源發展而採取的獎勵。聯邦政府對公共土地的許可和計劃核准正在加速地熱開發,這降低了不確定性並開闢了新的資源區域。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 監理情勢

- 影響產業的因素

- 促進因素

- 產業潛在風險與挑戰

- 成長潛力分析

- 波特的分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- PESTEL 分析

- 價格趨勢分析,2022-2035年

- 新機會與趨勢

- 投資分析及未來展望

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃及資金籌措

- 競爭性標竿分析

- 創新與永續性現狀

第5章 市場規模及預測:依技術分類,2022-2035年

- 二進位

- 單次閃光

- 雙閃光

- 三重閃光

- 乾燥

- 反壓

第6章 市場規模與預測:依國家分類,2022-2035年

- 美國

- 墨西哥

- 土耳其

- 冰島

- 義大利

- 德國

- 中國

- 菲律賓

- 印尼

- 紐西蘭

- 日本

- 肯亞

- 衣索比亞

- 哥斯大黎加

- 薩爾瓦多

- 尼加拉瓜

- 瓜地馬拉

- 世界其他地區

第7章:公司簡介

- Ansaldo Energia

- Calpine

- Contact Energy

- Energy Development Corporation

- Enel Green Power

- Enertime

- Exergy International

- First Gen

- Fuji Electric

- GE Vernova

- Halliburton

- KenGen

- Mitsubishi Heavy Industries

- Ormat Technologies

- Pertamina Geothermal Energy

- Reykjavik Geothermal

- SLB

- Star Energy

- Toshiba

- Turboden

The Global Geothermal Energy Market was valued at USD 66.9 billion in 2025 and is estimated to grow 5.5% to reach USD 109.6 billion by 2035.

The market is propelled by clean-firm procurement mandates that support grid reliability, rewarding high-capacity-factor geothermal resources. Falling project costs, improved performance through learning effects, and regulatory-backed utility procurement are strengthening the investment case by providing long-term revenue certainty. Companies are increasingly optimizing brownfield sites using bottoming-cycle cogeneration, leveraging existing wells and steamfields to add capacity quickly. Energy security concerns and concessional financing are enabling first-of-a-kind geothermal plants in small island systems. Market growth remains gradual and concentrated, with incremental additions dominating. Policymakers are positioning geothermal as a reliable complement to variable renewables, while advanced geothermal technologies are moving from R&D to field demonstrations, expanding viable geologies and project types. Execution challenges and interconnection constraints are shaping procurement, favoring phased deployment. Government-led initiatives in Asia are expanding bankable pipelines and intensifying competition for project development rights, while repowering and uprating existing plants provide near-term output gains faster than new greenfield development.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $66.9 Billion |

| Forecast Value | $109.6 Billion |

| CAGR | 5.5% |

The single-flash geothermal segment accounted for 35.9% share in 2025 and is projected to reach USD 41 billion by 2035. Single-flash systems convert high-pressure geothermal water into steam to drive turbines, reinjecting remaining fluid into reservoirs. Their proven technology, operational simplicity, and efficiency in high-temperature hydrothermal fields make them the dominant geothermal solution globally.

U.S. Geothermal Energy Market reached USD 15.5 billion in 2025. This growth reflects rising investments in renewable energy, demand for low-emission electricity, and government incentives promoting clean power. Federal permitting and project approvals on public lands have accelerated geothermal development by reducing uncertainties and unlocking new resource areas.

Key players in the Global Geothermal Energy Market include Ansaldo Energia, Energy Development Corporation, Enel Green Power, Contact Energy, Ormat Technologies, Pertamina Geothermal Energy, GE Vernova, Halliburton, Mitsubishi Heavy Industries, Star Energy, Reykjavik Geothermal, Fuji Electric, SLB, Exergy International, Calpine, Enertime, Toshiba, Turboden, and KenGen. Companies in the Geothermal Energy Market are focusing on strategic initiatives to strengthen their position. They are investing in technology upgrades, including advanced drilling, resource characterization, and high-efficiency turbines, to improve plant output and operational reliability. Many are entering joint ventures and partnerships to share project risks, expand geographic reach, and accelerate development pipelines. Firms are also leveraging government incentives, concessional financing, and carbon credit programs to lower CAPEX barriers and improve ROI. Additionally, players are repowering and uprating existing plants to boost output cost-effectively while expanding service offerings to include engineering, procurement, and operations management for integrated solutions.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Market estimates & forecast parameters

- 1.3 Forecast

- 1.3.1 Key trends for market estimates

- 1.3.2 Quantified market impact analysis

- 1.3.2.1 Mathematical impact of growth parameters on forecast

- 1.3.3 Scenario analysis framework

- 1.4 Primary research and validation

- 1.4.1 Some of the primary sources (but not limited to)

- 1.5 Data mining sources

- 1.5.1 Paid Sources

- 1.5.2 Sources, by region

- 1.6 Research trail & scoring components

- 1.6.1 Research trail components

- 1.6.2 Scoring components

- 1.7 Research transparency addendum

- 1.7.1 Source attribution framework

- 1.7.2 Quality assurance metrics

- 1.7.3 Our commitment to trust

- 1.8 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022 - 2035

- 2.1.1 Business trends

- 2.1.2 Technology trends

- 2.1.3 Country trends

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

- 3.6.1 Political factors

- 3.6.2 Economic factors

- 3.6.3 Social factors

- 3.6.4 Technological factors

- 3.6.5 Legal factors

- 3.6.6 Environmental factors

- 3.7 Price trend analysis, 2022-2035

- 3.8 Emerging opportunities & trends

- 3.9 Investment analysis & future prospects

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis, 2025

- 4.3 Key developments

- 4.3.1 Mergers & acquisitions

- 4.3.2 Partnerships & collaborations

- 4.3.3 New product launches

- 4.3.4 Expansion plans and funding

- 4.4 Competitive benchmarking

- 4.5 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Technology, 2022 - 2035 (USD Million & MW)

- 5.1 Key trends

- 5.2 Binary

- 5.3 Single flash

- 5.4 Double flash

- 5.5 Triple flash

- 5.6 Dry

- 5.7 Back pressure

Chapter 6 Market Size and Forecast, By Country, 2022 - 2035 (USD Million & MW)

- 6.1 Key trends

- 6.2 U.S.

- 6.3 Mexico

- 6.4 Turkey

- 6.5 Iceland

- 6.6 Italy

- 6.7 Germany

- 6.8 China

- 6.9 Philippines

- 6.10 Indonesia

- 6.11 New Zealand

- 6.12 Japan

- 6.13 Kenya

- 6.14 Ethiopia

- 6.15 Costa Rica

- 6.16 El Salvador

- 6.17 Nicaragua

- 6.18 Guatemala

- 6.19 Rest of World

Chapter 7 Company Profiles

- 7.1 Ansaldo Energia

- 7.2 Calpine

- 7.3 Contact Energy

- 7.4 Energy Development Corporation

- 7.5 Enel Green Power

- 7.6 Enertime

- 7.7 Exergy International

- 7.8 First Gen

- 7.9 Fuji Electric

- 7.10 GE Vernova

- 7.11 Halliburton

- 7.12 KenGen

- 7.13 Mitsubishi Heavy Industries

- 7.14 Ormat Technologies

- 7.15 Pertamina Geothermal Energy

- 7.16 Reykjavik Geothermal

- 7.17 SLB

- 7.18 Star Energy

- 7.19 Toshiba

- 7.20 Turboden

2034 年超高溫岩石地熱市場預測:按資源類型、發電能力、技術、應用、最終用戶和地區進行全球分析。深層地熱能市場預測至2034年:按資源類型、發電容量、技術、最終用戶和地區分類的全球分析

2034 年超高溫岩石地熱市場預測:按資源類型、發電能力、技術、應用、最終用戶和地區進行全球分析。深層地熱能市場預測至2034年:按資源類型、發電容量、技術、最終用戶和地區分類的全球分析 地熱能市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、應用、地區和競爭格局分類,2021-2031年

地熱能市場-全球產業規模、佔有率、趨勢、機會、預測:按類型、應用、地區和競爭格局分類,2021-2031年 地熱能:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)地熱能源系統市場預測至2034年—按類型、資源類型、組件、技術、應用、最終用戶和地區分類的全球分析

地熱能:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)地熱能源系統市場預測至2034年—按類型、資源類型、組件、技術、應用、最終用戶和地區分類的全球分析 地熱能市場:依技術、組件、應用和最終用途分類-2026-2032年全球市場預測

地熱能市場:依技術、組件、應用和最終用途分類-2026-2032年全球市場預測 全球地熱能源市場規模、佔有率、趨勢和成長分析報告:2026-2034年

全球地熱能源市場規模、佔有率、趨勢和成長分析報告:2026-2034年 2026年全球地熱能源市場報告

2026年全球地熱能源市場報告 地熱能市場規模、佔有率和成長分析(按類型、模式、深度、溫度、功率、應用、最終用途和地區分類)-2026-2033年產業預測地熱能市場預測至2032年:按電站類型、組件、技術、應用、最終用戶和地區分類的全球分析

地熱能市場規模、佔有率和成長分析(按類型、模式、深度、溫度、功率、應用、最終用途和地區分類)-2026-2033年產業預測地熱能市場預測至2032年:按電站類型、組件、技術、應用、最終用戶和地區分類的全球分析