|

市場調查報告書

商品編碼

2066441

印尼黏合劑和密封劑市場:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)Indonesia Adhesives And Sealants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

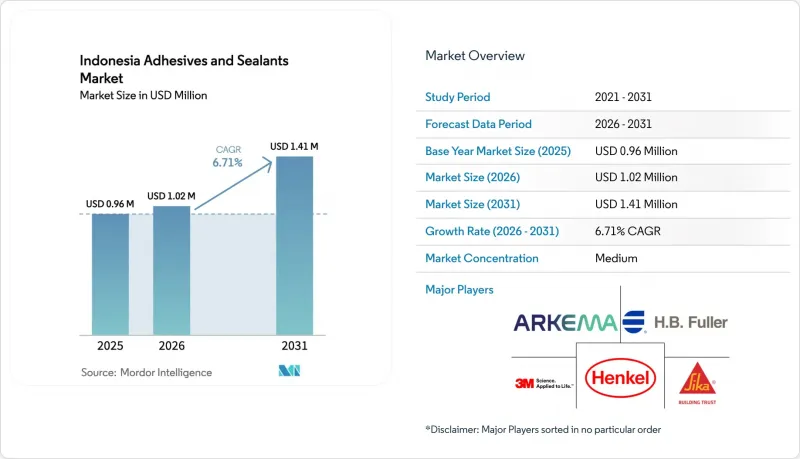

根據 Mordor Intelligence 預測,印尼黏合劑和密封劑市場規模預計將在 2025 年達到 96 萬美元,2026 年達到 102 萬美元,到 2031 年達到 141 萬美元,2026 年至 2031 年的複合年成長率為 6.71%。

本報告按樹脂類型(丙烯酸樹脂、氰基丙烯酸酯樹脂、環氧樹脂、聚氨酯樹脂、矽酮樹脂等)、黏合劑技術(熱熔膠、反應型黏合劑、溶劑型黏合劑、紫外光固化黏合劑等)、密封劑類型(聚氨酯密封劑、環氧樹脂密封劑等)以及用戶產業細分(航太、航太汽車、建築等)進行細分。市場預測以美元計價。

印尼黏合劑和密封劑市場趨勢及洞察

印尼快速消費品(FMCG)軟包裝產業強勁成長。

預計軟包裝產量將從2019年的1,413億件增加至2024年的1,592億件。此外,品牌所有者對循環經濟的承諾要求複合膠和壓敏黏著劑供應商確保產品符合食品接觸要求、可回收且具有更高的耐熱性。跨國公司正透過針對自動化紙箱成型生產線最佳化的快速固化熱熔膠來應對這些挑戰,而小型加工商則難以在不斷變化的歐盟和東協法規下獲得配方認證。因此,產量激增加劇了技術差距,市場需求正集中於那些擁有區域試點實驗室、食品接觸測試和數位化追溯平台的供應商。

正在進行的大型基礎設施項目正在加速對建築黏合劑的需求。

2023年政府批准的基礎設施項目總額達250億瑞士法郎(約合272.4億美元),2024年總建設預算達2500億瑞士法郎(約合2726.9億美元),這些因素持續推動著瓷磚黏合劑、水泥漿和結構性黏著劑的需求成長,其成長速度甚至超過了GDP增速。根據ISO 13007修訂的SNI性能標準正在影響公共競標,導致市場需求轉向符合ISO標準的品牌,這些品牌能夠保證產品在潮濕的沿海地區和地震多發地區具有長期耐久性。因此,大型橋樑、新機場和高層住宅大樓的建設正在推動砂漿、密封劑和混凝土修補化學品的長期需求。

進口石化原料價格波動

由於印尼進口約42%的聚乙烯和57%的聚丙烯,用於黏合劑的EVA、VAE和SB乳膠的價格會隨著石腦油價格和外匯波動。擁有自有樹脂工廠的跨國公司透過簽訂多年期非需求組合來規避風險,但小規模的調配商依賴現貨運輸,導致成本波動更大。計畫中的國內裂解裝置擴建工程或許能從2027年起緩解供不應求,但短期風險敞口仍是營運資金的阻礙因素。

細分市場分析

預計到2025年,丙烯酸類產品將佔據印尼黏合劑和密封劑市場29.00%的佔有率。由於運動鞋出口商對更高耐熱性和剝離強度的需求不斷成長,聚氨酯產品市場預計將以7.02%的複合年成長率成長。對棕櫚油衍生多元醇和木質素基非異氰酸酯製造方法的研究表明,其剪切強度可達26.2 MPa,這支持了未來向更安全、更可再生原料的轉變。

在印尼的黏合劑和密封劑市場,丙烯酸乳液的收入仍主要來自膠帶、標籤和低成本木工黏合劑,但歐盟不斷提高的VOC排放上限迫使加工商轉向水性聚氨酯產品。環氧樹脂、氰基丙烯酸酯和酚醛樹脂在電子、MRO(維護、維修和營運)以及膠合板領域佔據著一定的市場佔有率。性能和價格的多樣性使得跨國公司能夠按化學類型細分產品系列組合,而本地生產商則專注於資本密集度較低的丙烯酸和動物基黏合劑產品線。

預計到2025年,水性產品將佔據38.4%的市場佔有率,成為家具、鞋類和印刷品行業的主要層壓工藝。聚氨酯-丙烯酸酯混合分散體可提高初始強度並縮短壓制時間。在印尼黏合劑和密封劑市場,反應型熱熔膠技術的市場佔有率預計在預測期(2026-2031年)內將以6.97%的複合年成長率成長。這主要是由於瓦楞紙板製造商對無需烘箱即可獲得即時初始黏合強度和高最終黏合強度的產品需求不斷成長,以滿足電子商務的需求。

雖然溶劑型產品線對於需要最高剝離強度的特殊鞋類仍然至關重要,但紫外線固化和厭氧系統正在電子產品和維修等細分市場中找到應用。供應商目前正在運作兩條試點生產線——一條是用於培訓中爪哇中小企業用戶的水性產品線,另一條是為雅加達物流中心提供的濕氣固化熱熔膠產品線——在買家簽訂合約之前,透過生產線速度來證明其經濟可行性。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 印尼快速消費品軟包裝產業強勁成長

- 正在進行的大型基礎設施項目正在加速對建築黏合劑的需求。

- 擴大國內鞋類製造業規模,面向出口市場

- 熱熔技術在電子商務物流包裝生產線中的快速普及。

- 為了遵守對歐盟的出口限制,當地湧現許多家具中小企業,它們正在轉型使用水性塗料系統。

- 市場限制因素

- 進口石化原料價格波動

- 印尼幣持續貶值,原料成本不斷上漲。

- 島際物流的碎片化推高了配送成本。

- 價值鏈分析

- 監理情勢

- 波特五力模型

第5章 市場規模與成長預測

- 依樹脂類型

- 丙烯酸纖維

- 氰基丙烯酸酯

- 環氧樹脂

- 聚氨酯

- 矽酮

- VAE/EVA

- 其他樹脂

- 黏合劑技術

- 熱熔膠

- 反應型

- 溶劑型

- 紫外線固化型

- 水溶液

- 樹脂專用密封劑

- 聚氨酯

- 環氧樹脂

- 丙烯酸纖維

- 矽酮

- 其他樹脂

- 按最終用戶行業分類

- 航太

- 車

- 建築/施工

- 鞋類和皮革

- 衛生保健

- 包裝

- 電子設備/家用電器

- 木工和細木工

- 其他終端用戶產業

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率和排名分析

- 公司簡介

- 3M

- Alteco Chemical Pte Ltd.

- Arkema

- Avery Dennison Corporation.

- BASF

- Dextone Indonesia

- Dow

- HB Fuller Company

- Henkel AG & Co. KGaA

- Hexcel Corporation

- Hilti Indonesia

- Huntsman International LLC

- Jowat SE

- MAPEI SpA

- PT. Pamolite Adhesive Industry

- Pidilite Industries Ltd.

- Sika AG

- Soudal

第7章 市場機會與未來展望

According to Mordor Intelligence, the indonesia adhesives and Sealants Market size is projected to be USD 0.96 million in 2025, USD 1.02 million in 2026, and reach USD 1.41 million by 2031, growing at a CAGR of 6.71% from 2026 to 2031.

This report is Segmented by Adhesives by Resin (Acrylic, Cyanoacrylate, Epoxy, Polyurethane, Silicone, and More), Adhesives by Technology (Hot Melt, Reactive, Solvent-Borne, UV Cured, and More), Sealants by Resin (Polyurethane, Epoxy, and More), and End-User Industry (Aerospace, Automotive, Building and Construction, and More). The Market Forecasts are Provided in Terms of Value (USD).

Indonesia Adhesives And Sealants Market Trends and Insights

Robust Growth in Indonesia's FMCG Flexible-Packaging Sector

Flexible packaging output rose to 159.2 billion units in 2024, up from 141.3 billion in 2019, and brand-owner circularity pledges compel laminating and pressure-sensitive adhesive suppliers to guarantee food contact, recycling compatibility, and higher heat-resistance thresholds. Multinationals respond with rapid-cure hot melts optimized for automated case-forming lines, while smaller converters struggle to certify formulations under evolving EU and ASEAN regulations. The volume surge is therefore widening the technology gap and consolidating demand around suppliers that run regional pilot labs, food-contact testing, and digital traceability platforms.

Ongoing Mega-Infrastructure Projects Accelerating Construction Adhesives Demand

Government infrastructure approvals totaling CHF 25 billion (USD 27.84 billion) in 2023 and an overall construction wallet valued at CHF 240 billion (USD 272.69 billion) in 2024 continue to drive tile-adhesive, grout, and structural bonding demand at above-GDP rates. Revised SNI performance norms aligned with ISO 13007 now influence public tenders, shifting volume toward ISO-compliant brands that can guarantee long-term durability in humid coastal and seismic zones. Mega-bridges, new airports, and high-rise residential towers thus anchor a long-tail pull for mortar, sealant, and concrete-repair chemistries.

Volatility in Imported Petrochemical Feedstock Prices

Indonesia imports about 42% of polyethylene and 57% of polypropylene, so adhesive grade EVA, VAE, and SB latex prices move with naphtha and exchange fluctuations. Multinationals with captive resin plants hedge risk through multiyear offtake contracts, while small batch blenders rely on spot cargoes, amplifying cost swings. Upcoming domestic cracker expansions may ease shortages after 2027, but near-term exposure remains a working-capital constraint.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Domestic Footwear Manufacturing for Export Markets

- Rapid Adoption of Hot-Melt Technologies in E-Commerce Logistics Packaging Lines

- Fragmented Inter-Island Logistics Inflating Distribution Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Acrylic maintained a 29.00% share in 2025 of the Indonesia Adhesives and Sealants market. The market size for polyurethane products is projected to expand at a 7.02% CAGR as athletic-shoe exporters specify higher heat resistance and peel strength. Research on palm-oil-derived polyols and lignin-based non-isocyanate routes demonstrated 26.2 MPa shear strength, validating a future shift toward safer, renewable feedstocks.

Indonesia Adhesives and Sealants market gains from acrylic emulsions remain anchored in tapes, labels, and low-cost woodworking glues, but escalating EU VOC ceilings push converters toward water-borne PU grades. Epoxies, cyanoacrylates, and phenol-formaldehyde occupy niche positions in electronics, MRO, and plywood. The widening performance-price spectrum allows multinationals to segment portfolios across chemistry families, while local formulators focus on acrylic or animal-glue lines that require lower capital intensity.

Water-borne products held 38.4% share in 2025 and dominate furniture, footwear, and graphic-arts lamination lines. Hybrid polyurethane-acrylic dispersions improve early green strength, reducing press time. Indonesia Adhesives and Sealants market share for reactive hot-melt technology is set to climb at a CAGR of 6.97% during the forecast period (2026-2031) because e-commerce carton makers value instant green strength and high final bond without ovens.

Solvent-borne lines remain essential for specialty footwear requiring the highest peel, while UV-curable and anaerobic systems serve electronics and maintenance niches. Suppliers now run dual pilot lines, water-borne for training SME users in Central Java and moisture-cure hot melts for Jakarta logistics hubs, to demonstrate line-speed economics before buyers commit.

List of Companies Covered in this Report:

- 3M

- Alteco Chemical Pte Ltd.

- Arkema

- Avery Dennison Corporation.

- BASF

- Dextone Indonesia

- Dow

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Hexcel Corporation

- Hilti Indonesia

- Huntsman International LLC

- Jowat SE

- MAPEI S.p.A.

- PT. Pamolite Adhesive Industry

- Pidilite Industries Ltd.

- Sika AG

- Soudal

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Robust growth in Indonesia's FMCG flexible-packaging sector

- 4.2.2 Ongoing mega-infrastructure projects accelerating construction adhesives demand

- 4.2.3 Expansion of domestic footwear manufacturing for export markets

- 4.2.4 Rapid adoption of hot-melt technologies in e-commerce logistics packaging lines

- 4.2.5 Emergence of local furniture SMEs upgrading to water-based systems for EU export compliance

- 4.3 Market Restraints

- 4.3.1 Volatility in imported petro-chemical feedstock prices

- 4.3.2 Persistent rupiah depreciation inflating raw-material costs

- 4.3.3 Fragmented inter-island logistics inflating distribution costs

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Forces

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 Adhesives by Resin

- 5.1.1 Acrylic

- 5.1.2 Cyanoacrylate

- 5.1.3 Epoxy

- 5.1.4 Polyurethane

- 5.1.5 Silicone

- 5.1.6 VAE / EVA

- 5.1.7 Other Resins

- 5.2 Adhesives by Technology

- 5.2.1 Hot Melt

- 5.2.2 Reactive

- 5.2.3 Solvent-borne

- 5.2.4 UV Cured

- 5.2.5 Water-borne

- 5.3 Sealants by Resin

- 5.3.1 Polyurethane

- 5.3.2 Epoxy

- 5.3.3 Acrylic

- 5.3.4 Silicone

- 5.3.5 Other Resins

- 5.4 By End-user Industry

- 5.4.1 Aerospace

- 5.4.2 Automotive

- 5.4.3 Building and Construction

- 5.4.4 Footwear and Leather

- 5.4.5 Healthcare

- 5.4.6 Packaging

- 5.4.7 Electronics and Appliances

- 5.4.8 Woodworking and Joinery

- 5.4.9 Other End-user Industries

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 3M

- 6.4.2 Alteco Chemical Pte Ltd.

- 6.4.3 Arkema

- 6.4.4 Avery Dennison Corporation.

- 6.4.5 BASF

- 6.4.6 Dextone Indonesia

- 6.4.7 Dow

- 6.4.8 H.B. Fuller Company

- 6.4.9 Henkel AG & Co. KGaA

- 6.4.10 Hexcel Corporation

- 6.4.11 Hilti Indonesia

- 6.4.12 Huntsman International LLC

- 6.4.13 Jowat SE

- 6.4.14 MAPEI S.p.A.

- 6.4.15 PT. Pamolite Adhesive Industry

- 6.4.16 Pidilite Industries Ltd.

- 6.4.17 Sika AG

- 6.4.18 Soudal

7 Market Opportunities and Future Outlook

- 7.1 Innovation in bio-based, palm-oil-derivative adhesives

- 7.2 White-space and Unmet-need Assessment

建築圍護結構黏合劑和密封劑市場-2026-2032年全球市場預測防水黏合劑和密封劑市場:2026-2032年全球市場預測(依產品類型、技術、形態、固化機制、基材、最終用途、應用和分銷通路分類)黏合劑和密封劑市場:2026-2032年全球市場預測(按產品類型、技術、形態、最終用途產業、應用和分銷管道分類)彈性黏合劑和密封劑市場:按樹脂類型、包裝類型、技術、形式、終端用戶產業和分銷管道分類-全球預測,2026-2032年

建築圍護結構黏合劑和密封劑市場-2026-2032年全球市場預測防水黏合劑和密封劑市場:2026-2032年全球市場預測(依產品類型、技術、形態、固化機制、基材、最終用途、應用和分銷通路分類)黏合劑和密封劑市場:2026-2032年全球市場預測(按產品類型、技術、形態、最終用途產業、應用和分銷管道分類)彈性黏合劑和密封劑市場:按樹脂類型、包裝類型、技術、形式、終端用戶產業和分銷管道分類-全球預測,2026-2032年 混合型黏合劑和密封劑:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)

混合型黏合劑和密封劑:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年) 雙層玻璃黏合劑和密封劑市場報告:按樹脂類型、最終用戶和地區分類(2026-2034 年)

雙層玻璃黏合劑和密封劑市場報告:按樹脂類型、最終用戶和地區分類(2026-2034 年) 全球黏合劑和密封劑市場,2026-2030年混合型黏合劑和密封劑市場報告:按樹脂類型、終端用途產業和地區分類(2026-2034 年)黏合劑和密封劑市場報告:黏合劑類型、密封劑類型、技術、應用和地區分類(2026-2034 年)

全球黏合劑和密封劑市場,2026-2030年混合型黏合劑和密封劑市場報告:按樹脂類型、終端用途產業和地區分類(2026-2034 年)黏合劑和密封劑市場報告:黏合劑類型、密封劑類型、技術、應用和地區分類(2026-2034 年) 黏合劑和密封劑市場:黏合劑技術、黏合劑產品、黏合劑應用、密封劑產品、密封劑應用和地區分類。

黏合劑和密封劑市場:黏合劑技術、黏合劑產品、黏合劑應用、密封劑產品、密封劑應用和地區分類。