|

市場調查報告書

商品編碼

2061596

混合型黏合劑和密封劑:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)Hybrid Adhesives And Sealants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

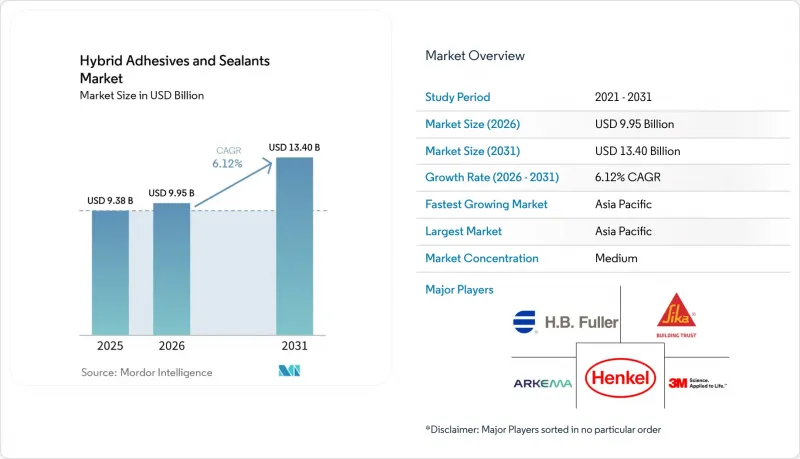

根據 Mordor Intelligence 預測,混合黏合劑和密封劑市場將從 2025 年的 93.8 億美元成長到 2026 年的 99.5 億美元,到 2031 年達到 134 億美元。

預計從 2026 年到 2031 年,其複合年成長率將達到 6.12%。

本報告按樹脂類型(MS聚合物混合、環氧聚氨酯樹脂、環氧氰基丙烯酸酯樹脂及其他樹脂)、終端用戶產業(建築、運輸、電子及其他終端用戶產業)和地區(亞太地區、北美地區、歐洲地區、南美地區以及中東和非洲地區)進行細分。市場規模和預測均以美元計價。

全球混合型黏合劑和密封劑市場趨勢及洞察

汽車和建築業需求激增

目前電動車電池組採用單體電池結構,需要一種能夠散熱、承受高達150 度C溫度波動且可依指示剝離以便回收的黏合劑。杜邦公司的Betaforce彈性結構系列黏合劑無需表面預處理即可黏合鋁塑複合軟包電池,使每個模組的組裝週期縮短15-20分鐘。類似的趨勢也出現在亞洲的高層建築項目中,快速固化的MS聚合物混合使得幕牆安裝和防水工作可以在同一天完成,從而降低了起重機租賃和人事費用。北美住宅建築商傾向於使用雙組分聚氨酯系統來黏合預製板。消除鋼龍骨造成的熱橋效應可以提高牆體的U值,使工程符合綠建築認證要求。 HB Fuller於2024年收購了HS Butyl,在其產品線中增加了防水膠帶,使歐洲各地幕牆安裝人員的生產效率提高了一倍。隨著電氣化和模組化建築的融合,採購團隊越來越傾向於根據總擁有成本 (TCO) 而不是初始材料價格來評估黏合劑的價值。

加強全球揮發性有機化合物和異氰酸酯法規

歐盟REACH法規附件十七的修訂要求所有處理二異氰酸酯含量超過0.1%材料的工人必須完成認證培訓,加工商也被迫過渡到使用不含異氰酸酯的MS聚合物或環氧丙烯酸酯混合材料。同時,歐盟包裝和包裝廢棄物法規將從2026年8月起將總氟含量限制在50 ppm以內,這要求配方必須進行調整,以去除那些會阻礙回收的含氟脫模劑。與歐洲的做法類似,加州「更安全消費品計畫」已將幾種二異氰酸酯列為優先化學品。 3M公司透過在2025年底前逐步淘汰所有PFAS生產來規避責任,雖然每年損失8.9億美元的黏合劑銷售額,但該公司於2025年9月推出了一種風險較低的丙烯酸替代品——Scotch-Weld DP8507NS。能夠證明其混合產品不含VOC和異氰酸酯的供應商,無需進行工廠通風升級或對員工進行大規模再培訓,即可獲得相關規範認證。

原料和矽烷價格波動

瓦克公司宣布,由於鉑催化劑成本翻番,將於2026年2月將其矽酮產品價格上調至多25%。預計這將使黏合劑的毛利率下降至多400個基點。由於中國太陽能發電熱潮吸收了新增的電子級矽烷產能,加上美國高達245%的關稅限制了進口,矽烷現貨價格一直居高不下。黏合劑生產商面臨兩種選擇:要麼自行承擔價格上漲,要麼將成本轉嫁給消費者,從而冒著失去市場佔有率的風險。黏合劑整合是緩解此問題的途徑之一。西卡公司已在德克薩斯州投資9,000萬美元興建了一家屋頂板材廠,以確保原料的穩定供應,並擴大了其在蘇州的聚氨酯生產技術。然而,鉑金和特種矽烷價格波動的不確定性可能會在市場穩定、產能增加之前,抑制短期盈利。

細分市場分析

預計到2025年,MS聚合物混合將佔據混合型黏合劑和密封劑市場56.87%的佔有率,並在2031年之前以7.30%的複合年成長率成長。該細分市場的快速成長反映了其監管優勢,因為濕固化矽烷骨架不會釋放揮發性有機化合物(VOC)或異氰酸酯。漢高公司於2025年12月發布的樂泰MS 9650,目標市場是汽車顯示器黏合,並符合REACH法規附件XVII的要求。環氧-聚氨酯互穿網路在風力發電機和航太結構中仍佔有一席之地,其具有自修復和抗疲勞性能,但價格高出15-25%。環氧-氰基丙烯酸酯混合物滿足了醫療和電子產業對固化時間60秒或更短的細分市場需求。 HB Fuller於2024年收購了Medifil和GEM,擴大了其外科業務,並新增了傷口縫合黏合劑。

2026年至2031年間,隨著複合材料生產商縮小搭接剪切強度方面的歷史差距,並在室溫固化測試中達到2 MPa以上的強度,預計銷售量將轉向MS聚合物。環氧樹脂混合材料在超高模量和極端耐熱性超出監管限制的領域仍保持其獨特的市場地位。由於應用特定性能要求的限制,熱熔混合材料和環氧-聚硫化物船用密封劑的應用範圍則更為有限。

區域分析

預計到2025年,亞太地區將佔混合型黏合劑和密封劑市場收入的45.44%,並在預測期(2026-2031年)內以8.41%的複合年成長率成長。瓦克在張家港的投資使該地區的矽酮產能提高了約20個百分點,使當地原始設備製造商(OEM)能夠更快地獲得用於建築密封劑和電動汽車溫度控管的高純度流體。印度1200億美元的基礎設施項目和印尼1500億美元的預算撥款正在推動預製橋面板、地鐵系統和玻璃幕牆領域對黏合劑需求的成長。日本和韓國在筑波和鎮川的增產進一步鞏固了它們在亞洲功能性矽酮市場的主導地位。

在北美和歐洲,預計成長將達到中等個位數,這主要得益於嚴格的排放法規推動了不含異氰酸酯的混合產品的需求。歐盟的包裝和包裝廢棄物法規迫使加工商重新設計多層複合材料,並考慮其可回收性,推動了對水性膠帶和無溶劑複合膠黏合劑的需求。漢高在2026年的一系列收購,特別是對Stahl集團和ATP Adhesive Systems的收購,將帶來12億歐元的銷售額,並加強其服務於這兩個地區的水性技術平台。同時,3M在全面停止使用PFAS後,正在圍繞更安全的壓克力產品重組其產品組合。

中東和非洲地區正受益於沙烏地阿拉伯的「2030願景」。該願景的目標是到2030年實現特種化學品產能670萬噸,年銷售額達935億沙烏地里亞爾,預計到2035年,西卡將在該地區的混合型黏合劑和密封劑市場佔據約22%的佔有率。西卡在摩洛哥、坦尚尼亞和南非的工廠正積極籌備可再生能源、水處理和交通走廊等基礎建設投資項目。受外匯波動的影響,南美洲仍是成長最慢的地區,但西卡和富樂集團在巴西和阿根廷的產能擴張可望推動該地區實現週期性復甦。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場促進因素

- 汽車和建築需求激增

- 加強全球揮發性有機化合物和異氰酸酯法規

- 過渡到多功能黏合劑(機械緊固件的替代品)

- 亞太地區的基礎建設熱潮

- 模組化和預製建築的普及

- 市場限制因素

- 原料和矽烷價格波動

- 與通用密封劑相比,單價較高

- 特種矽烷生產能力瓶頸

- 價值鏈分析

- 波特五力模型

第5章 市場規模與成長預測

- 依樹脂類型

- MS聚合物混合

- 環氧聚氨酯

- 環氧氰基丙烯酸酯

- 其他樹脂(環氧樹脂、聚硫化物等)

- 按最終用戶行業分類

- 建築/施工

- 運輸

- 電子設備

- 其他終端用戶產業

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 其他亞太國家

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 義大利

- 法國

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲國家

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率和排名分析

- 公司簡介

- 3M

- American Sealants Inc.

- Arkema

- Dymax Corporation

- Forgeway

- HB Fuller Company

- Henkel AG & Co. KGaA

- Jowat SE

- Hermann Otto GmbH

- Hodgson Sealants

- Kisling AG

- MAPEI SpA

- Master Bond Inc.

- Sika AG

- Permabond LLC

- TREMCO ILLBRUCK

- Wacker Chemie AG

- Merz+benteli AG

- McCoy Soudal

第7章 市場機會與未來展望

According to Mordor Intelligence, the hybrid adhesives and Sealants Market size is expected to increase from USD 9.38 billion in 2025 to USD 9.95 billion in 2026 and reach USD 13.40 billion by 2031, growing at a CAGR of 6.12% over 2026-2031.

This report is Segmented by Resin Type (MS Polymer Hybrid, Epoxy-Polyurethane, Epoxy-Cyanoacrylate, and Other Resins), by End-User Industry (Building and Construction, Transportation, Electronics, and Other End-User Industries), and by Geography (Asia-Pacific, North America, Europe, South America, and the Middle East and Africa). The Market Sizes and Forecasts are Provided in Terms of Value (USD).

Global Hybrid Adhesives And Sealants Market Trends and Insights

Rapid Automotive and Construction Demand

Electric-vehicle battery packs now incorporate cell-to-pack architectures that require adhesives to dissipate heat, tolerate 150°C excursions, and debond on command for recycling. DuPont's Betaforce elastic structural series bonds aluminum-laminated pouch cells without surface pretreatment, trimming 15-20 minutes from each module assembly cycle. Parallel momentum is visible in high-rise Asian projects where rapid-cure MS polymer hybrids let facades be hung and waterproofed on the same day, cutting crane rental and labor expense. North American residential builders favor prefabricated panels held together with two-component polyurethane systems; eliminating steel-stud thermal bridges improves wall U-values and qualifies projects for green-building credits. H.B. Fuller's 2024 purchase of HS Butyl added waterproofing tapes that double the throughput of curtain-wall installers across Europe. As electrification and modular construction converge, procurement teams increasingly evaluate adhesives on total cost of ownership rather than upfront material price.

Stricter Global VOC and Isocyanate Regulations

The European Union's REACH Annex XVII amendment obliges any worker handling more than 0.1% diisocyanate content to complete certified training, pushing converters toward isocyanate-free MS polymer and epoxy-acrylic hybrids. Concurrently, the EU Packaging and Packaging Waste Regulation caps total fluorine at 50 ppm from August 2026, compelling reformulation away from fluorinated release agents that hinder recyclability. California's Safer Consumer Products program flags several diisocyanates as priority chemicals, echoing European pressure. 3M pre-empted liability by exiting all PFAS production by end-2025, sacrificing USD 890 million in annual adhesive revenue but launching a low-hazard acrylic replacement, Scotch-Weld DP8507NS, in September 2025. Suppliers able to certify VOC-free, isocyanate-free hybrids win specifications without forcing plant ventilation upgrades or extensive worker retraining.

Raw-Material and Silane Price Volatility

Wacker announced up to 25% price hikes on silicone goods in February 2026 after platinum catalyst costs doubled, pressuring adhesive gross margins by as much as 400 basis points. Spot silane prices stayed elevated when China's photovoltaic boom absorbed new electronic-grade capacity and US tariffs of up to 245% restricted imports. Adhesive formulators must either swallow the increases or risk share loss by passing them through. Vertical integration is one mitigation path: Sika invested USD 90 million in a roofing-membrane plant in Texas and expanded polyurethane technologies in Suzhou to secure feedstock flows. Nonetheless, unpredictability in platinum and specialty silanes will restrain short-run profitability until additional capacity stabilizes the market.

Other drivers and restraints analyzed in the detailed report include:

- Shift Toward Multifunctional Bonding

- APAC Infrastructure Boom

- Higher Unit Cost Versus Commodity Sealants

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

MS polymer hybrids captured 56.87% of the Hybrid Adhesives and Sealants market share in 2025 and are set to grow at 7.30% CAGR to 2031. The segment's leap reflects regulatory favor, because moisture-cure silyl backbones release no VOCs or isocyanates. Henkel's Loctite MS 9650, unveiled in December 2025, targets in-car display bonding and sidesteps REACH Annex XVII training mandates. Epoxy-polyurethane interpenetrating networks retain a foothold in wind-turbine and aerospace structures, trading 15-25% higher prices for self-healing and fatigue resistance. Epoxy-cyanoacrylate blends fill medical and electronics niches demanding less than or equal to 60-second fixture speeds; H.B. Fuller's 2024 purchase of Medifill and GEM added wound-closure adhesives that expand its surgical franchise.

Across 2026-2031, volume tilts toward MS polymers as formulators close the historic gap in lap-shear strength, now surpassing 2 MPa in ambient-cure tests. Epoxy-based hybrids keep a specialized territory where ultra-high modulus or extreme heat resistance outweigh regulatory constraints. Hot-melt hybrids and epoxy-polysulfide marine sealants serve even narrower roles, constrained by application-specific performance envelopes.

Geography Analysis

Asia-Pacific retained 45.44% of the Hybrid Adhesives and Sealants market revenue in 2025 and is projected to expand at an 8.41% CAGR during the forecast period (2026-2031). Wacker's Zhangjiagang investment boosted regional silicone capacity by roughly 20 percentage points, giving local OEMs faster access to high-purity fluids for construction sealants and EV thermal management. India's USD 120 billion infrastructure pipeline and Indonesia's USD 150 billion allocation funnel adhesive demand into precast bridge decks, metro systems, and glass facades. Japanese and South Korean expansions in Tsukuba and Jincheon further tighten Asia's grip on functional silicones.

North America and Europe exhibit mid-single-digit growth, buoyed by strict emissions caps that favor isocyanate-free hybrids. The EU Packaging and Packaging Waste Regulation forces converters to redesign multilayer laminates for recyclability, boosting demand for water-based tapes and solvent-free laminating adhesives. Henkel's 2026 acquisition spree, Stahl Group, and ATP Adhesive Systems, added EUR 1.2 billion in revenue and deepened water-based technology platforms serving both regions. Meanwhile, 3M's complete PFAS exit repositions its portfolio around safer acrylics.

The Middle East and Africa benefit from Saudi Arabia's Vision 2030, which earmarks 6.7 million tons of specialty-chemical capacity and SAR 93.5 billion annual revenue by 2030, raising the region's share of Hybrid adhesives and sealants market to an estimated 22% by 2035. Sika's Moroccan, Tanzanian, and South African plants prepare for infrastructure spending in renewable energy, water treatment, and transit corridors. South America remains the slowest-growing territory, restrained by currency swings, yet capacity builds in Brazil and Argentina by Sika and H.B. Fuller position the region for cyclical rebounds.

- 3M

- American Sealants Inc.

- Arkema

- Dymax Corporation

- Forgeway

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Jowat SE

- Hermann Otto GmbH

- Hodgson Sealants

- Kisling AG

- MAPEI SpA

- Master Bond Inc.

- Sika AG

- Permabond LLC

- TREMCO ILLBRUCK

- Wacker Chemie AG

- Merz+benteli AG

- McCoy Soudal

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Drivers

- 4.1.1 Rapid automotive and construction demand

- 4.1.2 Stricter global VOC and isocyanate regulations

- 4.1.3 Shift toward multifunctional bonding (mechanical fastener replacement)

- 4.1.4 APAC infrastructure boom

- 4.1.5 Modular and prefabricated building uptake

- 4.2 Market Restraints

- 4.2.1 Raw-material and silane price volatility

- 4.2.2 Higher unit cost vs. commodity sealants

- 4.2.3 Bottlenecks in specialty silane capacity

- 4.3 Value Chain Analysis

- 4.4 Porter's Five Forces

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitutes

- 4.4.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Resin Type

- 5.1.1 MS Polymer Hybrid

- 5.1.2 Epoxy-Polyurethane

- 5.1.3 Epoxy-Cyanoacrylate

- 5.1.4 Other Resins (Epoxy - Polysulfide, and more)

- 5.2 By End-user Industry

- 5.2.1 Building and Construction

- 5.2.2 Transportation

- 5.2.3 Electronics

- 5.2.4 Other End-user Industries

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 3M

- 6.4.2 American Sealants Inc.

- 6.4.3 Arkema

- 6.4.4 Dymax Corporation

- 6.4.5 Forgeway

- 6.4.6 H.B. Fuller Company

- 6.4.7 Henkel AG & Co. KGaA

- 6.4.8 Jowat SE

- 6.4.9 Hermann Otto GmbH

- 6.4.10 Hodgson Sealants

- 6.4.11 Kisling AG

- 6.4.12 MAPEI SpA

- 6.4.13 Master Bond Inc.

- 6.4.14 Sika AG

- 6.4.15 Permabond LLC

- 6.4.16 TREMCO ILLBRUCK

- 6.4.17 Wacker Chemie AG

- 6.4.18 Merz+benteli AG

- 6.4.19 McCoy Soudal

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

建築圍護結構黏合劑和密封劑市場-2026-2032年全球市場預測防水黏合劑和密封劑市場:2026-2032年全球市場預測(依產品類型、技術、形態、固化機制、基材、最終用途、應用和分銷通路分類)黏合劑和密封劑市場:2026-2032年全球市場預測(按產品類型、技術、形態、最終用途產業、應用和分銷管道分類)彈性黏合劑和密封劑市場:按樹脂類型、包裝類型、技術、形式、終端用戶產業和分銷管道分類-全球預測,2026-2032年

建築圍護結構黏合劑和密封劑市場-2026-2032年全球市場預測防水黏合劑和密封劑市場:2026-2032年全球市場預測(依產品類型、技術、形態、固化機制、基材、最終用途、應用和分銷通路分類)黏合劑和密封劑市場:2026-2032年全球市場預測(按產品類型、技術、形態、最終用途產業、應用和分銷管道分類)彈性黏合劑和密封劑市場:按樹脂類型、包裝類型、技術、形式、終端用戶產業和分銷管道分類-全球預測,2026-2032年 雙層玻璃黏合劑和密封劑市場報告:按樹脂類型、最終用戶和地區分類(2026-2034 年)

雙層玻璃黏合劑和密封劑市場報告:按樹脂類型、最終用戶和地區分類(2026-2034 年) 印尼黏合劑和密封劑市場:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)

印尼黏合劑和密封劑市場:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年) 全球黏合劑和密封劑市場,2026-2030年混合型黏合劑和密封劑市場報告:按樹脂類型、終端用途產業和地區分類(2026-2034 年)黏合劑和密封劑市場報告:黏合劑類型、密封劑類型、技術、應用和地區分類(2026-2034 年)

全球黏合劑和密封劑市場,2026-2030年混合型黏合劑和密封劑市場報告:按樹脂類型、終端用途產業和地區分類(2026-2034 年)黏合劑和密封劑市場報告:黏合劑類型、密封劑類型、技術、應用和地區分類(2026-2034 年) 黏合劑和密封劑市場:黏合劑技術、黏合劑產品、黏合劑應用、密封劑產品、密封劑應用和地區分類。

黏合劑和密封劑市場:黏合劑技術、黏合劑產品、黏合劑應用、密封劑產品、密封劑應用和地區分類。