|

市場調查報告書

商品編碼

2066407

農業機械:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Agricultural Machinery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

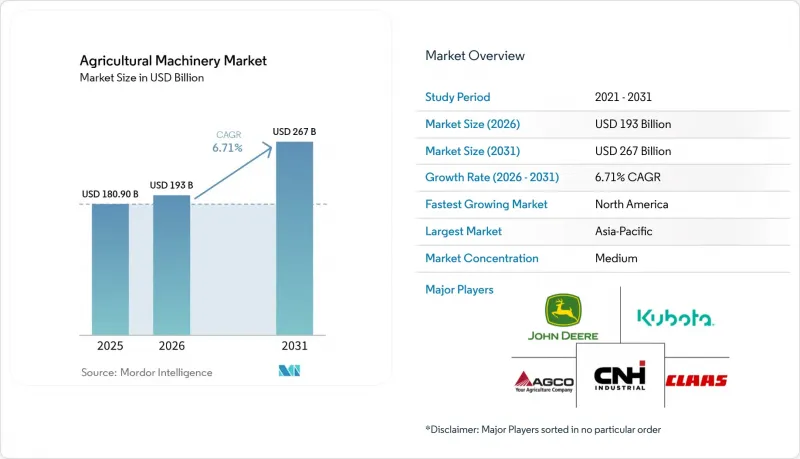

根據 Mordor Intelligence 預測,農業機械市場規模將從 2025 年的 1,809 億美元成長到 2026 年的 1,930 億美元,到 2031 年將達到 2,670 億美元,2026 年至 2031 年的複合年成長率為 6.71%。

本報告按類型(曳引機、土壤耕作機械、播種機械及其他)、自動化程度(手動、全自動、半自動)和地區(北美、歐洲、亞太、南美、中東和非洲)進行細分。市場預測以美元計價。

全球農業機械市場趨勢及洞察

農業勞動力短缺和工資上漲

目前,農業機械市場正受到農業勞動市場緊張的影響。根據美國農場局聯合會統計,2024財政年度約發放了384,900份H-2A臨時農場工人簽證。儘管如此,許多季節性工作仍面臨勞動力短缺的問題。這影響了農業機械市場的購買決策,生產者越來越傾向於權衡人事費用與機械設備的成本和營運穩定性。儘管整體農業機械需求依然疲軟,但能夠緩解收割、播種和噴灑等作業尖峰時段勞動力需求的設備正日益受到歡迎。

精密農業與遠端資訊處理的融合

農業機械市場正日益朝著中高階機型標配遠端資訊處理和數位化農業工具的方向發展。 2025年2月,迪爾公司推出了「精準基礎套件」(Precision Essentials),其中包括StarFire 7500接收器、G5顯示器和JDLink數據機。該套件能夠更有效率地升級新舊機器。此舉對農業機械市場意義重大,因為改造升級方案不僅能延長現有機器的使用壽命,還能引進諸如導航操作、互聯互通和現場資料處理等新功能。因此,市場競爭格局正從單純的硬體競爭演變為由硬體、軟體和服務組成的一體化生態系統。

高昂的初始成本和資金籌措的壓力

農業機械市場面臨許多挑戰,例如新設備高成本以及大規模採購的財務負擔。大馬力曳引機和聯合收割機的這個問題尤其突出,由於融資緊張和借貸成本上升,農民們正在推遲更換週期。 AGCO公司報告稱,其2025年的淨銷售額將為101億美元,比2024年下降13.5%。根據美國農業機械製造商協會(AEM)發布的2026年報告,與2025年3月相比,美國農業曳引機的銷量將下降9.1%,聯合收割機的銷量將下降25.3%。這主要是由於農場管理水平下降和融資壓力增大所致。農業機械需求的強勁復甦需要經銷商庫存的正常化和信貸環境的改善。

細分市場分析

預計到2025年,曳引機將在農業機械市場佔據35.9%的市場佔有率,繼續保持其銷售量最大的產品類別地位。這一主導地位反映了曳引機在大多數農業系統中作為犁地、播種、運輸、作物管理以及各種附件的主要動力來源的作用。然而,曳引機市場內部的需求存在差異。小型曳引機在園藝和特種作物應用領域表現出色,而100馬力及以上的曳引機對於北美和歐洲的大規模行栽作物種植仍然至關重要。此外,自動駕駛和特種作物精準噴灑技術的進步也推動了人們對專為果園和葡萄園設計的曳引機的興趣日益濃厚。

在農業機械市場中,收割機械細分市場預計將在2026年至2031年間以6.0%的複合年成長率成長,成為成長最快的細分市場。這一成長主要得益於自動化設定、作物感測、割台控制和穀物品管等技術的日益普及,這些技術提高了有限收割季節的田間作業效率。此外,市場也不斷拓展,不再局限於傳統的聯合收割機和脫粒機,飼料收割機在酪農養殖和畜牧業中日益受到關注,而特種作物收割機也正從試點計畫走向全面商業化。其他主要類別,例如土壤準備和耕作機械、播種機械以及噴灑和作物保護機械,也持續受益於保護性耕作、精準噴灑和投入品管理等方面的技術進步。

區域分析

到2025年,亞太地區將佔全球農業機械市場佔有率的36.8%,成為最大的區域市場。推動亞太市場成長的主要動力來自中國農業機械現代化建設以及印度對曳引機的巨大需求。中國正著力發展智慧農業機械、自動駕駛輔助系統和新能源設備,農業無人機的應用已相當廣泛。在印度,活躍的農業活動和持續的機械化需求也推動了市場需求。例如,馬恆達公司(Mahindra & Mahindra)報告稱,其2026年4月的曳引機銷量將達到46,404台,比上年同期成長20%。同時,日本和澳洲的農業機械市場更為成熟,技術主導發展更為顯著,而東南亞市場則正透過小規模農戶的機械化計畫不斷擴張。

預計北美地區將以7.2%的複合年成長率(CAGR)實現最高成長率,2026年至2031年將成為農業機械市場成長最快的地區。目前,該市場正處於經濟週期的低谷,過去十年購置車輛的更換需求預計將推動經濟復甦的後半程。南美洲仍然是農業機械市場潛力巨大的地區。在巴西和阿根廷,大規模的農作物生產支撐著市場,但信貸環境的收緊正在減緩短期採購。

歐洲憑藉其強大的製造業基礎、高度的機械化水平以及對精密農業技術的持續投資,仍然是農業機械的重要市場。該地區的需求受多種因素影響,例如設備更新周期、資金籌措條件以及旨在提高農場效率的永續性發展農業政策。在中東,灌溉擴建計畫和環境控制農業正在推動對專用機械和水資源管理設備的需求。非洲的機械化仍處於起步階段,但在一些發展中農業經濟體政府主導的農業現代化計畫和糧食安全措施的支持下,長期機械需求正在逐步成長。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 農業勞動力短缺和工資上漲

- 精密農業與遠端資訊處理的融合

- 機械化補貼和貸款支持

- 農場整合和提高單位面積產量的壓力

- 拓展客製化租賃和「設備即服務 (EaaS)」業務

- 為再生農業和低排放設備資金籌措

- 市場限制因素

- 高昂的初始成本和資金籌措的壓力

- 農業結構分散,利潤分配不均

- 自主現場作業監理方面的不確定性

- 資料所有權、維修權限和互通性。

- 監理情勢

- 技術展望

- 波特五力模型

第5章 市場規模與成長預測

- 按類型

- 聯結機

- 按馬力

- 小於40馬力

- 40 HP~99 HP

- 100馬力或以上

- 曳引機類型

- 小型多用途曳引機

- 通用曳引機

- 行式曳引機

- 果園和葡萄園用曳引機

- 按馬力

- 土壤準備和農業機械

- 犁

- 光環

- 耕耘機和分蘗機

- 種植/播種機械

- 播種機

- 播種機

- 撒佈器

- 種植機

- 收割機械

- 聯合收割機和脫粒機

- 飼料收割機

- 專用農作物收割機

- 噴灑和作物保護機械

- 自走式噴霧機

- 拖曳式和懸掛式噴霧器

- 飛機和無人機噴灑系統

- 乾草和飼料機械

- 割草和修剪

- 打包機

- 耙子和耙子

- 灌溉機械

- 噴水灌溉

- 滴灌

- 機械樞軸系統

- 聯結機

- 按自動化級別

- 手動的

- 半自動

- 自動的

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 其他北美國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 法國

- 英國

- 義大利

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 其他亞太國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Deere & Company

- CNH Industrial NV

- AGCO Corporation

- Kubota Corporation

- Mahindra & Mahindra Limited

- CLAAS KGaA mbH

- SDF SpA

- Yanmar Holdings Co., Ltd.

- Iseki & Co., Ltd.

- Argo Tractors SpA

- Bucher Industries AG

- Valmont Industries, Inc.

- Lindsay Corporation

- Tractors and Farm Equipment Limited

- Maschio Gaspardo SpA

第7章 市場機會與未來展望

According to Mordor Intelligence, the agricultural machinery market size is projected to grow from USD 180.9 billion in 2025 to USD 193.0 billion in 2026 and USD 267.0 billion by 2031, registering a CAGR of 6.71% during 2026-2031.

This report is Segmented by Type (Tractors, Soil Preparation and Cultivation Machinery, Planting and Seeding Machinery, and Other Types), by Automation Level (Manual, Automatic, and Semi-Automatic), and by Geography (North America, Europe, Asia-Pacific, South America, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Agricultural Machinery Market Trends and Insights

Farm Labor Scarcity and Wage Inflation

The agricultural machinery market is currently influenced by tighter farm labor conditions. According to America Farm Bureau Federation, nearly 384,900 H-2A temporary agricultural worker visas were issued in fiscal year 2024 . Despite this, labor shortages persist in many seasonal operations. This has impacted purchasing decisions within the agricultural machinery market, as growers increasingly compare labor costs with the expenses and operational stability associated with machine ownership. Equipment that reduces peak labor demand in activities such as harvesting, transplanting, and spraying is gaining popularity, even as overall demand for machinery remains subdued.

Precision Agriculture and Telematics Integration

The agricultural machinery market is increasingly transitioning to a stage where telematics and digital agronomy tools are becoming standard features on mid-range and premium equipment. In February 2025, Deere & Company launched its Precision Essentials package, which includes a StarFire 7500 receiver, G5 display, and JDLink modem. This package enables both newer and older machines to be upgraded more efficiently. This development is significant for the agricultural machinery market, as retrofit options allow farmers to extend the lifespan of existing equipment while adopting features such as guided operations, connectivity, and field data functionalities. Consequently, market competition is evolving from a focus solely on hardware to integrated ecosystems comprising hardware, software, and services.

High Upfront Cost and Financing Pressure

The agricultural machinery market faces challenges due to the high cost of new equipment and the financial strain associated with large purchases. This issue is particularly pronounced in high-horsepower tractors and combines, where farmers are postponing replacement cycles due to constrained cash flow and increased borrowing costs. AGCO Corporation reported net sales of USD 10.1 billion in 2025, a 13.5% decrease compared to 2024 . According to the Association of Equipment Manufacturers (AEM) 2026 report, the sales of agricultural tractors in the United States were down 9.1%, and combine sales dropped 25.3% compared to March 2025, driven by weaker farm economics and financial pressures. Dealer inventory normalization and improved credit conditions are critical for a stronger recovery in equipment demand.

Other drivers and restraints analyzed in the detailed report include:

- Subsidies and Mechanization Credit Support

- Farm Consolidation and Output-Per-Acre Pressure

- Fragmented Farm Structures and Uneven Payback

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Tractors led the agricultural machinery market with 35.9% of the market share in 2025, keeping them the largest type category by value. This dominance reflects their role as the primary power source for field preparation, planting, haulage, crop care, and various attachments across most farming systems. However, demand within the tractor category varies. Compact models are performing well in horticulture and specialty applications, while machines with 100 horsepower and above remain essential for large row-crop operations in North America and Europe. Additionally, there is growing interest in purpose-built orchard and vineyard tractors, driven by advancements in autonomy and precision spraying for specialty crops.

The harvesting machinery segment of the agricultural machinery market is projected to grow at a CAGR of 6.0% from 2026 to 2031, making it the fastest-growing segment. This growth is attributed to increased adoption of automated settings, crop sensing, header control, and grain-quality management technologies, which enhance field efficiency during limited harvest periods. The market is also expanding beyond traditional combines and threshers, with forage harvesters gaining traction in dairy and livestock systems and specialty crop harvesters transitioning from pilot use to broader commercialization. Other key categories, such as soil preparation and cultivation machinery, planting and seeding machinery, and spraying and crop protection machinery, continue to benefit from advancements in conservation tillage, precision application, and improved input control.

Geography Analysis

Asia-Pacific accounted for the largest 36.8% of the agricultural machinery market size in 2025, which made it the largest regional market. The market in this region is driven by China's fleet modernization initiatives and India's significant tractor demand by volume. China is focusing on intelligent machinery, autonomous driving support systems, and new-energy equipment, with agricultural drone usage already operating at a substantial scale. In India, demand is bolstered by robust farm activity and ongoing mechanization needs. For instance, Mahindra and Mahindra Limited reported tractor sales of 46,404 units in April 2026, reflecting a 20% year-on-year increase. Meanwhile, the agricultural machinery markets in Japan and Australia are more mature and technology-driven, whereas Southeast Asian markets are expanding through smallholder mechanization programs.

North America is projected to grow at the fastest 7.2% CAGR from 2026 to 2031, which makes it the fastest-growing geography in the agricultural machinery market. Although the market is currently experiencing a cyclical trough, replacement demand from fleets purchased in the last decade is projected to drive a later-cycle recovery. South America remains a high-potential region for the agricultural machinery market. Brazil and Argentina are supported by large-scale crop production, although tighter credit conditions have slowed near-term purchases.

Europe continues to be a significant agricultural machinery market due to its robust manufacturing base, high levels of mechanization, and ongoing investments in precision farming technologies. Demand in the region is shaped by factors such as replacement cycles, financing conditions, and agricultural policies focused on sustainability, which promote efficiency improvements on farms. In the Middle East, irrigation expansion projects and controlled-environment agriculture are driving demand for specialized machinery and water-management equipment. Africa, while at an earlier stage of mechanization, is witnessing gradual growth in long-term machinery demand, supported by government-led agricultural modernization programs and food security initiatives in several developing farming economies.

- Deere & Company

- CNH Industrial N.V.

- AGCO Corporation

- Kubota Corporation

- Mahindra & Mahindra Limited

- CLAAS KGaA mbH

- SDF S.p.A.

- Yanmar Holdings Co., Ltd.

- Iseki & Co., Ltd.

- Argo Tractors S.p.A.

- Bucher Industries AG

- Valmont Industries, Inc.

- Lindsay Corporation

- Tractors and Farm Equipment Limited

- Maschio Gaspardo S.p.A.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Farm labor scarcity and wage inflation

- 4.2.2 Precision agriculture and telematics integration

- 4.2.3 Subsidies and mechanization credit support

- 4.2.4 Farm consolidation and output-per-acre pressure

- 4.2.5 Custom hiring and equipment-as-a-service expansion

- 4.2.6 Regenerative and low-emission equipment funding

- 4.3 Market Restraints

- 4.3.1 High upfront cost and financing pressure

- 4.3.2 Fragmented farm structures and uneven payback

- 4.3.3 Autonomous field-operation regulatory uncertainty

- 4.3.4 Data ownership, repair access, and interoperability frictions

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Tractors

- 5.1.1.1 By Horsepower

- 5.1.1.1.1 Less than 40 HP

- 5.1.1.1.2 40 HP to 99 HP

- 5.1.1.1.3 100 HP and Above

- 5.1.1.2 By Tractor Type

- 5.1.1.2.1 Compact Utility Tractors

- 5.1.1.2.2 Utility Tractors

- 5.1.1.2.3 Row Crop Tractors

- 5.1.1.2.4 Orchard and Vineyard Tractors

- 5.1.1.1 By Horsepower

- 5.1.2 Soil Preparation and Cultivation Machinery

- 5.1.2.1 Plows

- 5.1.2.2 Harrows

- 5.1.2.3 Cultivators and Tillers

- 5.1.3 Planting and Seeding Machinery

- 5.1.3.1 Seed Drills

- 5.1.3.2 Planters

- 5.1.3.3 Broadcast Spreaders

- 5.1.3.4 Transplanters

- 5.1.4 Harvesting Machinery

- 5.1.4.1 Combine Harvesters and Threshers

- 5.1.4.2 Forage Harvesters

- 5.1.4.3 Specialty Crop Harvesters

- 5.1.5 Spraying and Crop Protection Machinery

- 5.1.5.1 Self-Propelled Sprayers

- 5.1.5.2 Trailed and Mounted Sprayers

- 5.1.5.3 Aerial and Drone-Enabled Spraying Systems

- 5.1.6 Hay and Forage Machinery

- 5.1.6.1 Mower-Conditioners

- 5.1.6.2 Balers

- 5.1.6.3 Rakes and Tedders

- 5.1.7 Irrigation Machinery

- 5.1.7.1 Sprinkler Irrigation

- 5.1.7.2 Drip Irrigation

- 5.1.7.3 Mechanized Pivot Systems

- 5.1.1 Tractors

- 5.2 By Automation Level

- 5.2.1 Manual

- 5.2.2 Semi-Automatic

- 5.2.3 Automatic

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.1.4 Rest of North America

- 5.3.2 South America

- 5.3.2.1 Brazil

- 5.3.2.2 Argentina

- 5.3.2.3 Rest of South America

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 France

- 5.3.3.3 United Kingdom

- 5.3.3.4 Italy

- 5.3.3.5 Russia

- 5.3.3.6 Rest of Europe

- 5.3.4 Asia-Pacific

- 5.3.4.1 China

- 5.3.4.2 India

- 5.3.4.3 Japan

- 5.3.4.4 Australia

- 5.3.4.5 Rest of Asia-Pacific

- 5.3.5 Middle East

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 Turkey

- 5.3.5.4 Rest of Middle East

- 5.3.6 Africa

- 5.3.6.1 South Africa

- 5.3.6.2 Nigeria

- 5.3.6.3 Rest of Africa

- 5.3.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Deere & Company

- 6.4.2 CNH Industrial N.V.

- 6.4.3 AGCO Corporation

- 6.4.4 Kubota Corporation

- 6.4.5 Mahindra & Mahindra Limited

- 6.4.6 CLAAS KGaA mbH

- 6.4.7 SDF S.p.A.

- 6.4.8 Yanmar Holdings Co., Ltd.

- 6.4.9 Iseki & Co., Ltd.

- 6.4.10 Argo Tractors S.p.A.

- 6.4.11 Bucher Industries AG

- 6.4.12 Valmont Industries, Inc.

- 6.4.13 Lindsay Corporation

- 6.4.14 Tractors and Farm Equipment Limited

- 6.4.15 Maschio Gaspardo S.p.A.

7 Market Opportunities and Future Outlook

全球農業機械市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球農業機械市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 農業機械設備市場:2026-2032年全球市場預測(按類型、功率輸出、引擎類型、變速箱類型、自動化程度、移動性、所有權類型、應用、最終用戶和銷售管道)

農業機械設備市場:2026-2032年全球市場預測(按類型、功率輸出、引擎類型、變速箱類型、自動化程度、移動性、所有權類型、應用、最終用戶和銷售管道) 農業機械市場機會、成長促進因素、產業趨勢分析及2026-2035年預測。

農業機械市場機會、成長促進因素、產業趨勢分析及2026-2035年預測。 農業切碎機市場-全球產業規模、佔有率、趨勢、機會和預測:按產品類型、自動化等級、商業模式、地區和競爭格局分類,2021-2031年

農業切碎機市場-全球產業規模、佔有率、趨勢、機會和預測:按產品類型、自動化等級、商業模式、地區和競爭格局分類,2021-2031年 2026年全球農業加長型堆高機市場報告

2026年全球農業加長型堆高機市場報告 農業及農業機械市場規模、佔有率及成長分析:依設備類型、產量、自動化程度、應用、驅動系統、最終用戶、銷售管道及地區分類-2026-2033年產業預測

農業及農業機械市場規模、佔有率及成長分析:依設備類型、產量、自動化程度、應用、驅動系統、最終用戶、銷售管道及地區分類-2026-2033年產業預測 2034年農業打包機市場預測-全球產品、動力來源、配置、技術、應用、最終用戶和區域分析2034年農產品出口品質監測市場預測-按組件、參數、產品/服務類型、最終用戶和地區分類的全球分析

2034年農業打包機市場預測-全球產品、動力來源、配置、技術、應用、最終用戶和區域分析2034年農產品出口品質監測市場預測-按組件、參數、產品/服務類型、最終用戶和地區分類的全球分析 英國農業機械:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)

英國農業機械:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年) 農業機械市場規模、佔有率和成長分析:按機器類型、自動化程度、動力來源、所有權類型、應用、最終用途和地區分類-2026-2033年產業預測

農業機械市場規模、佔有率和成長分析:按機器類型、自動化程度、動力來源、所有權類型、應用、最終用途和地區分類-2026-2033年產業預測