|

市場調查報告書

商品編碼

2071399

農業機械市場機會、成長促進因素、產業趨勢分析及2026-2035年預測。Agriculture Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

全球農業機械市場預計到 2025 年將達到 1,236 億美元,年複合成長率為 5.9%,到 2035 年將達到 2,012 億美元。

隨著全球糧食需求持續成長,農業生產力面臨越來越大的壓力,農業機械市場正經歷穩定成長。人口成長和農產品需求的增加促使農民投資於能夠提高作業效率和最大化產量的現代化機械。隨著農業生產者尋求在有限的耕地上最佳化生產,同時應對節約勞動力的挑戰,機械化農業的重要性日益凸顯。精密農業技術的引入透過實現更精準的田間管理和資源利用,進一步推動了農業機械產業的變革。技術進步催生了配備智慧系統的先進農業機械,這些機械能夠改善監測、耕作和收穫作業。自動化、定位技術和數位化農業工具的整合,使生產者能夠在提高生產力的同時降低操作複雜性。此外,對永續農業實踐的日益重視,推動了對環保農業機械的需求,這些機械有助於減少排放、提高資源利用效率和改善土壤管理。這些因素,加上持續的創新和不斷發展的農業實踐,將繼續增強農業機械市場的長期前景。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 起始金額 | 1236億美元 |

| 預測金額 | 2012億美元 |

| 複合年成長率 | 5.9% |

預計到2025年,農業曳引機市場規模將達515億美元。精密農業技術的日益普及推動了對先進播種和施肥設備的需求成長,這些設備能夠最佳化種子投放和養分施用。農民們正不斷投資於旨在提高生產力、最大化作物產量和高效利用資源的專用機械。對提高農業產量和提升農業效率的持續需求預計將繼續推動該領域的需求成長。

預計到2025年,手動農機具市佔率將達到49%。手動農機具在農業生產中仍發揮著至關重要的作用,尤其是在農業規模相對較小、先進技術普及程度有限的地區。成本效益高、操作簡便、功能實用等優勢持續支撐著市場對手動農機具的需求。同時,自動化投資的不斷成長也為先進農業機械創造了巨大的發展機會。然而,部分農業活動仍依賴傳統的手動工具和設備。

預計到2025年,美國農業機械市場將佔據全球80%的佔有率,市場規模將達到274億美元。全國的市場成長主要得益於持續的技術進步、機械化以及精密農業技術的普及。大型農場主持續增加對先進農業機械的投資,以提高生產力、營運效率並簡化農業流程。預計在整個預測期內,對現代化、資源最佳化和高產農業技術的重視將持續支撐美國對農業機械的需求。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章 行業洞察

- 產業生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 供應鏈分析

- 主要投入材料

- 區域製造地與採購模式

- 供應鏈脆弱性與風險緩解

- 影響產業的因素

- 成長促進因素

- 產業潛在風險與挑戰

- 機會

- 成長潛力分析

- 價格趨勢

- 對過去價格趨勢的分析

- 定價策略:按業務類型分類

- 監理框架

- 世界排放氣體與安全標準(EPA Tier 4、歐盟 Stage V、中國 Stage III/IV)

- 北美監理框架

- 歐洲法規結構(歐盟綠色交易,「從農場到餐桌」政策的影響)

- 亞太地區:中國和印度的法規結構和資助項目

- 貿易政策、關稅和進出口法規

- 波特五力分析

- PESTLE分析

- 貿易數據分析

- 進出口量及進口額趨勢

- 主要貿易路線及關稅的影響

- 人工智慧和生成式人工智慧對市場的影響

- 人工智慧正在改變傳統的經營模式。

- 按客戶群分類的生成式人工智慧用例和部署藍圖

- 風險、限制和監管考量

- 未來市場趨勢

- 技術與創新展望

- 最新科技趨勢

- 新興技術

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係和聯盟

- 新產品發布

- 業務拓展計劃

第5章 市場估算與預測:依機械類型分類,2022-2035年

- 農用曳引機

- 小型園圃曳引機

- 小型曳引機

- 多用途曳引機

- 行式曳引機

- 果園和葡萄園用曳引機

- 高功率四驅曳引機

- 其他(卡車式/履帶式曳引機等)

- 收割機械

- 聯合收割機

- 飼料收割機

- 脫粒機

- 收割機

- 犁地和農用機械

- 犁

- 光環

- 耕耘機和分蘗機

- 播種和施肥機械

- 播種機

- 播種機

- 撒佈器

- 噴霧機

- 乾草收割機

- 打包機

- 修剪和護理

- 耙草機和耙子

- 其他(灌溉機械、收穫後後處理設備等)

第6章 市場估計與預測:依產量分類,2022-2035年

- 小於30馬力

- 31~100 HP

- 101~200 HP

- 超過200馬力

第7章 市場估計與預測:依技術分類,2022-2035年

- 手動的

- 半自動

- 全自動

第8章 市場估計與預測:依應用領域分類,2022-2035年

- 一排作品

- 水果和蔬菜

- 葡萄園和果園

- 家畜

- 林業

第9章 市場估價與預測:依通路分類,2022-2035年

- 直銷

- 間接銷售

第10章 市場估價與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 荷蘭

- 亞太地區

- 中國

- 日本

- 印度

- 澳洲

- 韓國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- UAE

第11章:公司簡介

- 全球主要公司

- AGCO

- CLAAS

- CNH Industrial

- John Deere

- Kubota

- Mahindra & Mahindra

- Yanmar Holdings

- 當地公司

- Escorts Kubota

- International Tractors

- Lovol

- Stara

- TAFE

- YTO Group

- Zoomlion Heavy Industry

- 新興企業和專業公司

- Carbon Robotics

- Energreen

- Lindsay

- Naio Technologies

- Oxbo

- Topcon Agriculture

- XAG

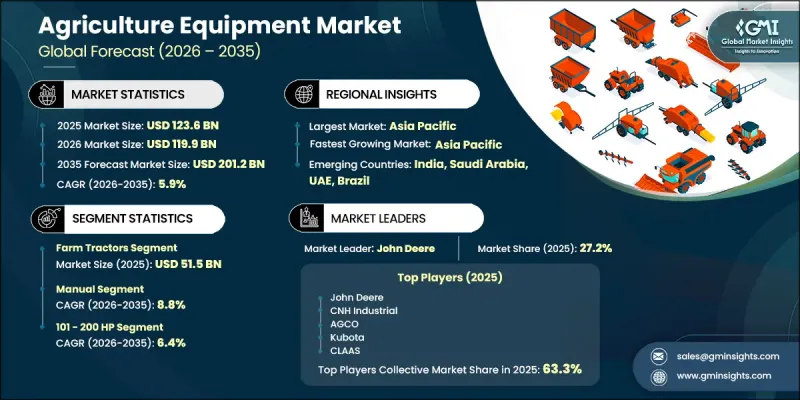

The Global Agriculture Equipment Market was valued at USD 123.6 billion in 2025 and is estimated to grow at a CAGR of 5.9% to reach USD 201.2 billion by 2035.

The agriculture equipment market is witnessing steady expansion as rising food requirements continue to place greater pressure on agricultural productivity worldwide. Growing population levels and increasing demand for agricultural output are encouraging farmers to invest in modern machinery capable of improving operational efficiency and maximizing crop yields. Mechanized farming has become increasingly important as agricultural producers seek to optimize production on limited arable land while addressing labor availability challenges. The adoption of precision agriculture technologies is further transforming the industry by enabling more accurate field management and resource utilization. Technological developments have introduced advanced equipment equipped with intelligent systems that improve monitoring, cultivation, and harvesting activities. The integration of automation, positioning technologies, and digital farming tools is helping producers enhance productivity while reducing operational complexity. In addition, the growing emphasis on sustainable farming practices is supporting demand for environmentally responsible machinery that contributes to lower emissions, improved resource efficiency, and better soil management. These factors, combined with ongoing innovation and evolving agricultural practices, continue to strengthen the long-term outlook for the agriculture equipment market.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $123.6 Billion |

| Forecast Value | $201.2 Billion |

| CAGR | 5.9% |

The farm tractors segment generated USD 51.5 billion in 2025. Rising awareness regarding precision farming techniques is increasing demand for advanced planting and fertilization equipment capable of optimizing seed placement and nutrient application. Farmers are increasingly investing in specialized machinery designed to improve productivity, maximize crop performance, and support efficient resource utilization. The growing need for higher agricultural output and improved farming efficiency is expected to continue driving demand across this segment.

The manual equipment segment accounted for 49% share in 2025. Manual equipment continues to play a vital role in agricultural operations, particularly in regions where farming activities remain smaller in scale and access to advanced technologies is limited. Cost-effectiveness, ease of operation, and practical functionality continue to support demand for manual equipment. At the same time, increasing investments in automation are creating significant growth opportunities for advanced agricultural machinery, although certain farming activities still rely on conventional manual tools and equipment.

United States Agriculture Equipment Market held an 80% share and generated USD 27.4 billion in 2025. Market growth across the country is being supported by ongoing technological advancements, increased mechanization, and the wider adoption of precision farming practices. Large-scale agricultural operations continue to invest heavily in advanced machinery to improve productivity, enhance operational efficiency, and streamline farming processes. Strong emphasis on modernization, resource optimization, and high-yield farming techniques is expected to sustain equipment demand across the country throughout the forecast period.

Key participants operating in the global agriculture equipment market include John Deere, Mahindra & Mahindra, Kubota, CNH Industrial, CLAAS, AGCO, Yanmar Holdings, Zoomlion Heavy Industry, Escorts Kubota, TAFE, YTO Group, International Tractors, Lovol, Stara, Lindsay, Topcon Agriculture, Carbon Robotics, Naio Technologies, Energreen, Oxbo, and XAG. Companies operating in the agriculture equipment market are focusing on product innovation, automation, and precision farming technologies to strengthen their competitive position and expand market presence. Manufacturers are investing heavily in research and development to introduce intelligent machinery equipped with advanced monitoring, automation, and connectivity features. Strategic partnerships with technology providers are helping companies enhance digital farming capabilities and deliver integrated solutions to agricultural producers. Market participants are also expanding manufacturing facilities and distribution networks to improve product accessibility across key agricultural regions. In addition, businesses are emphasizing sustainability by developing equipment that improves fuel efficiency, reduces emissions, and supports environmentally responsible farming practices.

Table of Contents

Chapter 1 Methodology and scope

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.1.1 Sources, by region

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation for any one approach

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Machinery

- 2.2.3 Power

- 2.2.4 Technology

- 2.2.5 Application

- 2.2.6 Distribution channel

Chapter 3 Industry insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Supply chain analysis

- 3.2.1 Key input materials

- 3.2.2 Manufacturing hubs & sourcing patterns by region

- 3.2.3 Supply chain vulnerabilities & risk mitigation

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.3.3 Opportunities

- 3.4 Growth potential analysis

- 3.5 Price trends

- 3.5.1 Historical price trend analysis

- 3.5.2 Pricing strategy by player type

- 3.6 Regulatory framework

- 3.6.1 Global Emissions & Safety Standards (EPA Tier 4, EU Stage V, China Stage III/IV)

- 3.6.2 North America Regulatory Framework

- 3.6.3 Europe Regulatory Framework (EU Green Deal, Farm to Fork Impact)

- 3.6.4 Asia Pacific: China & India Regulatory Framework & Subsidy Programs

- 3.6.5 Trade Policy, Tariffs & Import/Export Regulations

- 3.7 Porter's five forces analysis

- 3.8 PESTEL analysis

- 3.9 Trade data analysis (based on paid database) (HS Code: 8432)

- 3.9.1 Import/export volume & value trends

- 3.9.2 Key trade corridors & tariff impact

- 3.10 Impact of AI & generative AI on the market

- 3.10.1 AI-driven disruption of traditional business models

- 3.10.2 GenAI use cases & adoption roadmap by customer segment

- 3.10.3 Risks, limitations & regulatory considerations

- 3.11 Future market trends

- 3.12 Technology and innovation landscape

- 3.12.1 Current technological trends

- 3.12.2 Emerging technologies

Chapter 4 Competitive landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 MEA

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Machinery, 2022 - 2035 ($Billion, Thousand Units)

- 5.1 Key trends

- 5.2 Farm tractors

- 5.2.1 Sub-compact & garden tractors

- 5.2.2 Compact tractors

- 5.2.3 Utility tractors

- 5.2.4 Row crop tractors

- 5.2.5 Orchard & vineyard tractors

- 5.2.6 High-power & 4WD tractors

- 5.2.7 Others (track / crawler tractors etc.)

- 5.3 Harvesting machinery

- 5.3.1 Combine harvester

- 5.3.2 Forage harvester

- 5.3.3 Thresher

- 5.3.4 Reaper

- 5.4 Plowing and cultivation machinery

- 5.4.1 Ploughs

- 5.4.2 Harrows

- 5.4.3 Cultivators & tillers

- 5.5 Planting and fertilizing machinery

- 5.5.1 Seed drills

- 5.5.2 Planters

- 5.5.3 Spreaders

- 5.5.4 Sprayers

- 5.6 Haying machinery

- 5.6.1 Balers

- 5.6.2 Mower-conditioner

- 5.6.3 Tedders & rakes

- 5.7 Others (irrigation machinery, post-harvest equipment etc.)

Chapter 6 Market Estimates & Forecast, By Power, 2022 - 2035 ($Billion, Thousand Units)

- 6.1 Key trends

- 6.2 < 30 HP

- 6.3 31 - 100 HP

- 6.4 101 - 200 HP

- 6.5 > 200 HP

Chapter 7 Market Estimates & Forecast, By Technology, 2022 - 2035 ($Billion, Thousand Units)

- 7.1 Key trends

- 7.2 Manual

- 7.3 Semi-automated

- 7.4 Fully automated

Chapter 8 Market Estimates & Forecast, By Application, 2022 - 2035 ($Billion, Thousand Units)

- 8.1 Key trends

- 8.2 Row crops

- 8.3 Fruit & vegetables

- 8.4 Vineyards & orchards

- 8.5 Livestock farming

- 8.6 Forestry

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035 ($Billion, Thousand Units)

- 9.1 Key trends

- 9.2 Direct sales

- 9.3 Indirect sales

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Billion, Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Key Players

- 11.1.1 AGCO

- 11.1.2 CLAAS

- 11.1.3 CNH Industrial

- 11.1.4 John Deere

- 11.1.5 Kubota

- 11.1.6 Mahindra & Mahindra

- 11.1.7 Yanmar Holdings

- 11.2 Regional Players

- 11.2.1 Escorts Kubota

- 11.2.2 International Tractors

- 11.2.3 Lovol

- 11.2.4 Stara

- 11.2.5 TAFE

- 11.2.6 YTO Group

- 11.2.7 Zoomlion Heavy Industry

- 11.3 Emerging/Niche Specialists

- 11.3.1 Carbon Robotics

- 11.3.2 Energreen

- 11.3.3 Lindsay

- 11.3.4 Naio Technologies

- 11.3.5 Oxbo

- 11.3.6 Topcon Agriculture

- 11.3.7 XAG

全球農業機械市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球農業機械市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 農業機械設備市場:2026-2032年全球市場預測(按類型、功率輸出、引擎類型、變速箱類型、自動化程度、移動性、所有權類型、應用、最終用戶和銷售管道)

農業機械設備市場:2026-2032年全球市場預測(按類型、功率輸出、引擎類型、變速箱類型、自動化程度、移動性、所有權類型、應用、最終用戶和銷售管道) 農業切碎機市場-全球產業規模、佔有率、趨勢、機會和預測:按產品類型、自動化等級、商業模式、地區和競爭格局分類,2021-2031年

農業切碎機市場-全球產業規模、佔有率、趨勢、機會和預測:按產品類型、自動化等級、商業模式、地區和競爭格局分類,2021-2031年 2026年全球農業加長型堆高機市場報告

2026年全球農業加長型堆高機市場報告 農業及農業機械市場規模、佔有率及成長分析:依設備類型、產量、自動化程度、應用、驅動系統、最終用戶、銷售管道及地區分類-2026-2033年產業預測

農業及農業機械市場規模、佔有率及成長分析:依設備類型、產量、自動化程度、應用、驅動系統、最終用戶、銷售管道及地區分類-2026-2033年產業預測 農業機械:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

農業機械:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 2034年農業打包機市場預測-全球產品、動力來源、配置、技術、應用、最終用戶和區域分析2034年農產品出口品質監測市場預測-按組件、參數、產品/服務類型、最終用戶和地區分類的全球分析英國農業機械:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)

2034年農業打包機市場預測-全球產品、動力來源、配置、技術、應用、最終用戶和區域分析2034年農產品出口品質監測市場預測-按組件、參數、產品/服務類型、最終用戶和地區分類的全球分析英國農業機械:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年) 農業機械市場規模、佔有率和成長分析:按機器類型、自動化程度、動力來源、所有權類型、應用、最終用途和地區分類-2026-2033年產業預測

農業機械市場規模、佔有率和成長分析:按機器類型、自動化程度、動力來源、所有權類型、應用、最終用途和地區分類-2026-2033年產業預測