|

市場調查報告書

商品編碼

2065785

背景調查:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)Background Screening - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

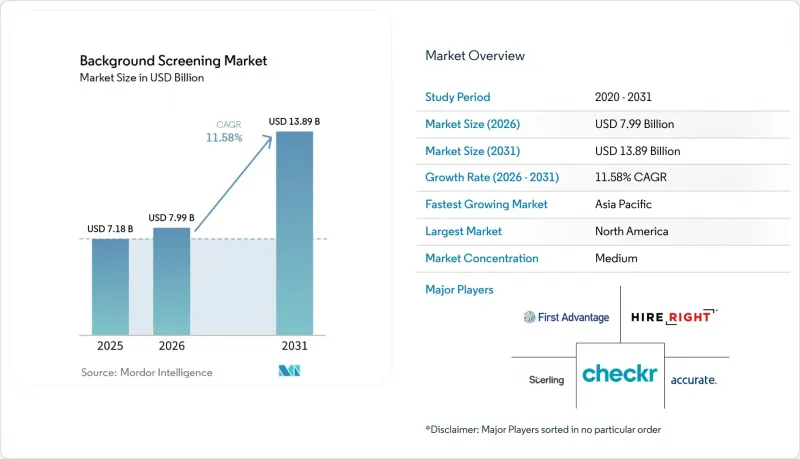

根據 Mordor Intelligence 預測,背景調查市場規模將從 2025 年的 71.8 億美元和 2026 年的 79.9 億美元成長到 2031 年的 138.9 億美元,2026 年至 2031 年的年複合成長率(CAGR)為 11.58%。

本報告按篩檢類型(僱用篩檢、犯罪背景調查等)、部署方式(雲端、本地部署)、產業(IT與電信、銀行、金融服務和保險等)、組織規模(大型企業、中小企業)和地區進行細分。市場預測以美元計價。

全球背景調查市場趨勢及洞察

零工經濟的發展正在推動北美地區篩檢的增加。

該零工平台整合了每月自動審核機制,涵蓋縣級犯罪記錄和性犯罪者登記信息,從而能夠對司機和送貨負責人進行即時風險評估。這項持續的審核流程增強了客戶對按需服務的信心,降低了法律責任風險,並且正在擴展到醫療保健人員配備領域——該領域需要對輪班工作的醫療保健專業人員進行持續的資格驗證。供應商利用與排班應用程式整合的API驅動工作流程,無需額外投入即可確保合規性。隨著零工經濟的日益普及,這一因素正在擴大背景調查的潛在市場,並加速與定期交易相關的平台的收入成長。

歐盟舉報人保護指令正在加快歐洲各地的犯罪記錄和信用調查。

2023/24 號指令強制要求企業保護舉報人,並鼓勵在財務、合規和審計職能部門進行更徹底的背景調查。同時實施的 GDPR 強制要求嚴格的同意管理,這推動了對歐洲託管的專業解決方案的需求,這些解決方案既能進行徹底調查,又能遵循數據最小化原則。金融服務機構主導將舉報人保護措施納入其現有的洗錢防制(AML) 框架,引領了這一趨勢。跨國公司隨後將這些高標準推廣至其全球子公司,使此因素的影響範圍擴展到歐洲以外。

拉丁美洲司法數據的碎片化導致處理時間和成本不斷增加。

在巴西法院,人工智慧正在試行用於清理積壓案件,但篩檢公司仍面臨許多挑戰,例如數位化程度不一、人工搜尋紀錄以及語言障礙,導致調查完成率僅50%至65%。相比之下,技術先進的地區完成率已達85%至90%。服務提供者需要雇用當地負責人、擴大服務範圍並提高預算費用,這給盈利帶來了壓力,並減緩了客戶的接受度。

細分市場分析

預計到2025年,就業核實將成為最大的收入來源,佔背景調查市場佔有率的62.18%。這主要得益於職業發展路徑日益靈活,需要對就業歷史進行嚴格的跨司法管轄區核實。同時,犯罪背景調查預計將以11.78%的複合年成長率成為成長最快的領域,反映出零工經濟、金融服務和醫療保健行業日益嚴格的安全要求。整合平台現在將教育背景、信用資訊和藥物檢測結果整合在一起,以降低客戶的使用門檻。人工智慧驅動的篩選引擎僅標示實質相關的違規行為,符合「清白紀錄」的法律合規要求。這些功能的結合正在擴大背景篩檢的潛在市場,並促進基於持續監控的經常性收入模式的形成。

區塊鏈檢驗學位證書的日益普及縮短了學歷認證所需的時間,使機構能夠專注於資料分析,從而評估學歷的相關性。在信用和財務審查方面,諸如公用事業收費繳費記錄等替代數據正被廣泛應用,提高了東協和中東及非洲地區銀行服務獲取管道有限的申請人的包容性。藥物和健康檢測正從一次性的入職前測試轉向與安全關鍵型工作安排相關的定期評估,進一步擴大了細分市場的背景調查規模。

至2025年,雲端技術將佔據背景調查市場71.05%的佔有率,並將在2031年之前保持11.95%的複合年成長率。基於SaaS的工作流程引擎支援與人力資源資訊系統(HRIS)、招募管理系統(ATS)和薪資核算平台的API連接,使分散的團隊能夠即時部署程式。可設定的合規性範本簡化了區域規則管理,這項功能深受尋求人才套利策略的跨國公司的青睞。

在國防、關鍵基礎設施和某些銀行業環境中,資料主權優先於速度,因此本地部署仍然十分普遍。然而,許多組織正在採用混合架構,將敏感資訊揭露表格保存在企業防火牆內,而標準檢驗則在經過認證的雲端節點上執行。這種柔軟性維持了背景篩檢市場在各種法規環境下的需求。

區域分析

預計到2025年,北美將佔全球收入的43.60%,這主要得益於《公平信用報告法案》(FCRA) 的要求、各州推行的「清白記錄法」以及醫療保健行業人才招聘的擴張。聯邦存款保險公司(FDIC)修訂的《銀行業公平招聘法案》(將於2024年10月生效)將進一步擴大對符合條件職位的強制性背景調查範圍。奧勒岡州、德克薩斯州和佛羅裡達州的州級隱私法規正在推動平台更新,將同意流程與候選人體驗相結合。大麻法律的差異迫使雇主在諮詢型篩檢機構的支持下實施更細緻的藥物檢測政策。

亞太地區以12.30%的複合年成長率領跑,主要得益於政府的數位化優先計畫以及東協內部勞動力的流動。新加坡強制性的COMPASS系統推動了基於技能的檢驗需求。印度的《數位個人資料保護法》引入了強制性跨境資料傳輸,而澳洲的《SOCI法案》則加強了對關鍵基礎設施營運供應商的審查。投資於國內數據節點和支援多種語言的演算法的供應商正在利用不斷成長的人才流動來提升其在該地區背景調查市場的佔有率。在歐洲,由於GDPR下獲取同意的複雜性,市場擴張速度較為緩慢,但包括金融服務在內的高價值產業正在推動對專家的需求。在中東,阿拉伯聯合大公國和沙烏地阿拉伯正在透過採用符合GDPR的資料保護框架並將其與積極的經濟多元化政策結合,增加對外籍人士的背景調查數量。在拉丁美洲,司法系統的碎片化阻礙了成長,但巴西和墨西哥的現代化努力正在為了解合規體系細微差別的區域專家創造局部商機。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 零工經濟的發展正在推動北美地區安全審查頻率的大幅提升。

- 歐盟舉報人保護指令正在加快歐洲各地的犯罪記錄和信用調查。

- 東協地區內部的跨境人才招聘正在推動多語言資格驗證的使用。

- 利用人工智慧進行持續監測,降低醫療保健提供者離職後的風險。

- 區塊鏈憑證錢包,可即時驗證學歷資格

- 強制性資料在地化正在推動對本地資料中心的投資。

- 市場限制因素

- 拉丁美洲司法數據的碎片化導致處理時間 (TAT) 和成本增加。

- GDPR下關於嚴格同意的規定限制了歐盟審查的徹底程度

- MEA申請人演算法姓名配對中出現誤報的風險

- 申請人實施詐欺的手段越來越複雜,傳統的技術已經不足以應付這些詐欺行為。

- 價值供應鏈分析

- 監管和技術展望

- 宏觀經濟影響評估

- 波特五力模型

第5章 市場規模與成長預測

- 按類型篩檢

- 僱用篩檢

- 犯罪紀錄調查

- 核實教育背景和資格

- 信用調查和財務調查

- 藥物和健康檢測

- 租戶和房產篩選

- 不同的發展

- 雲

- 現場

- 按行業

- IT/通訊

- BFSI

- 醫療保健和生命科學

- 政府/國防

- 教育

- 製造業和能源

- 零工平台和共享出行

- 按組織規模

- 大公司

- 中小企業

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 北歐國家(丹麥、瑞典、挪威、芬蘭)

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- ASEAN

- 澳洲

- 紐西蘭

- 其他亞太國家

- 中東和非洲

- 中東

- GCC

- 土耳其

- 以色列

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 埃及

- 其他非洲國家

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- HireRight Holdings Corp.

- First Advantage Corp.

- Sterling Check Corp.

- Checkr Inc.

- Accurate Background LLC

- InfoMart Inc.

- GoodHire(Inflection LLC)

- Orange Tree Employment Screening

- IntelliCorp Records Inc.

- Verity Screening Solutions

- CVCheck Ltd.

- Triton Canada Inc.

- SecUR Credentials Ltd.

- AuthBridge Research Services

- FactSuite

- SpringVerify

- Quinfy

- Idfy

- Verifacts Services

- Appexigo

- PeopleCheck Pty Ltd.

- Onfido Ltd.

- Certn Holdings Inc.

- HireRight MEA(formerly Powerchex)

第7章 市場機會與未來展望

According to Mordor Intelligence, the background screening market size is projected to expand from USD 7.18 billion in 2025 and USD 7.99 billion in 2026 to USD 13.89 billion by 2031, registering a CAGR of 11.58% between 2026 to 2031.

This report is Segmented by Screening Type (Employment Screening, Criminal Background Checks, and More), Deployment (Cloud, On-Premises), Industry Vertical (IT and Telecom, BFSI, and More), Organization Size (Large Enterprises, Small and Mid-Sized Enterprises), and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Background Screening Market Trends and Insights

Gig-economy growth boosting high-frequency re-screenings in North America

Gig platforms embed monthly automated checks that cover county criminal records and sex-offender registries, enabling real-time risk decisions for drivers and delivery personnel. Continuous protocols improve customer confidence for on-demand services, reduce liability exposure, and extend into healthcare staffing, where rotating clinicians require perpetual credential validation. Vendors leverage API-driven workflows that integrate with scheduling apps, ensuring compliance without added friction. As gig-work penetration rises, this driver elevates the addressable background screening market and accelerates platform revenue tied to recurring transactions

EU whistle-blower directive accelerating criminal and credit checks across Europe

The 2023/24 directive compels companies to protect whistle-blowers, prompting deeper vetting for finance, compliance, and audit roles. Parallel GDPR obligations demand strict consent controls, spurring demand for specialized European-hosted solutions that reconcile thorough checks with data minimization principles. Financial services institutions lead adoption as they overlay whistle-blower safeguards onto existing AML frameworks. Multinationals then export these elevated standards to global subsidiaries, amplifying the driver's influence beyond Europe.

Fragmented judiciary data in LATAM inflating TAT and cost

Brazil's courts trial AI for docket backlogs, yet screening firms still face inconsistent digitization, manual record retrieval, and language barriers that yield 50-65% completion rates versus 85-90% in developed regions. Providers must hire local agents, extend service-level agreements, and budget higher fees, suppressing profitability and slowing client adoption.

Other drivers and restraints analyzed in the detailed report include:

- ASEAN cross-border hiring fueling multilingual verifications

- Blockchain credential wallets enabling instant education verification

- Stringent GDPR consent rules limiting depth of EU checks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Employment verification generated the largest revenue, accounting for 62.18% of background screening market share in 2025. The driver stems from increasingly mobile career paths that necessitate rigorous, multi-jurisdiction employment history confirmation. Conversely, criminal background checks post the fastest 11.78% CAGR, reflecting heightened security mandates across gig-economy, financial services, and healthcare roles. Integrated platforms now bundle education, credit, and drug testing to lower client onboarding friction. AI-assisted adjudication engines flag only materially relevant offenses, aligning with "clean-slate" law compliance. The combined functionality enlarges the addressable background screening market and spurs recurrent revenue models anchored in continuous monitoring.

Emerging adoption of blockchain-verified diplomas compresses turnaround times for education checks, redirecting provider focus toward data analytics that interpret credential relevance. Credit and financial checks apply alternative data such as utility-payment histories, improving inclusion for under-banked applicants within ASEAN and MEA. Drug and health testing shifts from pre-hire snapshots to recurring assessments tied to safety-sensitive scheduling, further expanding the background screening market size at the segment level.

Cloud captured 71.05% of background screening market size in 2025 and retains top-line momentum with a 11.95% CAGR to 2031. SaaS-based workflow engines deliver API connectivity into HRIS, ATS, and payroll platforms, enabling same-day program rollouts for distributed teams. Configurable compliance templates simplify regional rule administration, a capability valued by multinationals pursuing talent arbitrage strategies.

On-premises installations persist in defense, critical infrastructure, and certain banking environments where data-sovereignty trumps speed. Even so, many organizations adopt hybrid architectures: sensitive disclosure forms reside behind corporate firewalls while standard verifications execute on accredited cloud nodes. This flexibility sustains overall background screening market demand across diverse regulatory settings.

Geography Analysis

North America generated 43.60% of 2025 revenue, anchored by FCRA obligations, state clean-slate laws, and healthcare staffing expansions. The FDIC's revised Fair Hiring in Banking Act (effective October 2024) further extends mandatory vetting for covered positions. State-level privacy statutes in Oregon, Texas, and Florida prompt platform updates that blend consent flows with candidate experience. Cannabis law divergence pushes employers toward nuanced drug-testing policies supported by consultative screening providers.

Asia Pacific records the highest 12.30% CAGR, fueled by digital-first governmental programs and intra-ASEAN labor mobility. Singapore's COMPASS mandates trigger skills-centric verifications; India's Digital Personal Data Protection Act introduces cross-border data-transfer obligations; and Australia's SOCI Act tightens vendor vetting for critical-infrastructure work. Providers that invest in in-country data nodes and language-aware algorithms capitalize on widening talent flows and grow their regional background screening market share. Europe exhibits moderate expansion constrained by GDPR consent complexity, though high-value industries-including financial services-drive specialist demand. In the Middle East, the UAE and Saudi Arabia embrace data-protection frameworks aligned with GDPR but combine them with aggressive economic diversification agendas, boosting screening volumes for expatriate roles. Latin America's fragmented judiciary landscape hampers growth; nevertheless, modernization initiatives in Brazil and Mexico create pockets of opportunity for regional specialists that grasp nuanced compliance regimes.

- HireRight Holdings Corp.

- First Advantage Corp.

- Sterling Check Corp.

- Checkr Inc.

- Accurate Background LLC

- InfoMart Inc.

- GoodHire (Inflection LLC)

- Orange Tree Employment Screening

- IntelliCorp Records Inc.

- Verity Screening Solutions

- CVCheck Ltd.

- Triton Canada Inc.

- SecUR Credentials Ltd.

- AuthBridge Research Services

- FactSuite

- SpringVerify

- Quinfy

- Idfy

- Verifacts Services

- Appexigo

- PeopleCheck Pty Ltd.

- Onfido Ltd.

- Certn Holdings Inc.

- HireRight MEA (formerly Powerchex)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Gig-economy growth boosting high-frequency re-screenings in North America

- 4.2.2 EU whistle-blower directive accelerating criminal and credit checks across Europe

- 4.2.3 ASEAN cross-border hiring fuelling multilingual verifications

- 4.2.4 AI-driven continuous monitoring reducing post-hire risk for healthcare providers

- 4.2.5 Blockchain credential wallets enabling instant education verification

- 4.2.6 Data-localization mandates spurring regional data-centre investments

- 4.3 Market Restraints

- 4.3.1 Fragmented judiciary data in LATAM inflating TAT and cost

- 4.3.2 Stringent GDPR consent rules limiting depth of EU checks

- 4.3.3 False positive risks in algorithmic name-match for MEA applicants

- 4.3.4 Rising applicant fraud sophistication outpacing legacy tech

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory and Technological Outlook

- 4.6 Macroeconomic Impact Assessment

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Screening Type

- 5.1.1 Employment Screening

- 5.1.2 Criminal Background Checks

- 5.1.3 Education and Credential Verification

- 5.1.4 Credit and Financial Checks

- 5.1.5 Drug and Health Testing

- 5.1.6 Tenant and Property Screening

- 5.2 By Deployment

- 5.2.1 Cloud

- 5.2.2 On-Premises

- 5.3 By Industry Vertical

- 5.3.1 IT and Telecom

- 5.3.2 BFSI

- 5.3.3 Healthcare and Life Sciences

- 5.3.4 Government and Defense

- 5.3.5 Education

- 5.3.6 Manufacturing and Energy

- 5.3.7 Gig-platforms and Shared Mobility

- 5.4 By Organization Size

- 5.4.1 Large Enterprises

- 5.4.2 Small and Mid-sized Enterprises (SMEs)

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Spain

- 5.5.3.5 Nordics (Denmark, Sweden, Norway, Finland)

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 ASEAN

- 5.5.4.6 Australia

- 5.5.4.7 New Zealand

- 5.5.4.8 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 GCC

- 5.5.5.1.2 Turkey

- 5.5.5.1.3 Israel

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Egypt

- 5.5.5.2.4 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 HireRight Holdings Corp.

- 6.4.2 First Advantage Corp.

- 6.4.3 Sterling Check Corp.

- 6.4.4 Checkr Inc.

- 6.4.5 Accurate Background LLC

- 6.4.6 InfoMart Inc.

- 6.4.7 GoodHire (Inflection LLC)

- 6.4.8 Orange Tree Employment Screening

- 6.4.9 IntelliCorp Records Inc.

- 6.4.10 Verity Screening Solutions

- 6.4.11 CVCheck Ltd.

- 6.4.12 Triton Canada Inc.

- 6.4.13 SecUR Credentials Ltd.

- 6.4.14 AuthBridge Research Services

- 6.4.15 FactSuite

- 6.4.16 SpringVerify

- 6.4.17 Quinfy

- 6.4.18 Idfy

- 6.4.19 Verifacts Services

- 6.4.20 Appexigo

- 6.4.21 PeopleCheck Pty Ltd.

- 6.4.22 Onfido Ltd.

- 6.4.23 Certn Holdings Inc.

- 6.4.24 HireRight MEA (formerly Powerchex)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

身分驗證軟體市場規模、佔有率和趨勢分析報告:按組件、部署模式、類型、企業規模、最終用途、地區和細分市場預測(2026-2033 年)

身分驗證軟體市場規模、佔有率和趨勢分析報告:按組件、部署模式、類型、企業規模、最終用途、地區和細分市場預測(2026-2033 年) 背景調查軟體:市佔率分析、產業趨勢與統計、成長預測(2026-2031)

背景調查軟體:市佔率分析、產業趨勢與統計、成長預測(2026-2031) 身分驗證解決方案市場預測—全球身分驗證類型、認證方法、階段、用例、最終用戶和地區分析—2034年

身分驗證解決方案市場預測—全球身分驗證類型、認證方法、階段、用例、最終用戶和地區分析—2034年 身分驗證市場:2026-2032年全球市場預測(按服務類型、驗證管道、資料類型、用例、產業、部署模式和組織規模分類)

身分驗證市場:2026-2032年全球市場預測(按服務類型、驗證管道、資料類型、用例、產業、部署模式和組織規模分類) 身分驗證市場規模、佔有率、趨勢和預測:按類型、組件、部署模式、組織規模、行業和地區分類,2026-2034 年

身分驗證市場規模、佔有率、趨勢和預測:按類型、組件、部署模式、組織規模、行業和地區分類,2026-2034 年 線上背景調查市場:按應用程式和地區分類身份驗證市場:按技術和地區分類通訊身分與認證服務:市場佔有率分析、產業趨勢與統計資料、成長預測(2026-2031 年)

線上背景調查市場:按應用程式和地區分類身份驗證市場:按技術和地區分類通訊身分與認證服務:市場佔有率分析、產業趨勢與統計資料、成長預測(2026-2031 年) 2026年全球創作者驗證平台市場報告2026年全球身分驗證軟體市場報告

2026年全球創作者驗證平台市場報告2026年全球身分驗證軟體市場報告