|

市場調查報告書

商品編碼

2062263

背景調查軟體:市佔率分析、產業趨勢與統計、成長預測(2026-2031)Background Check Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

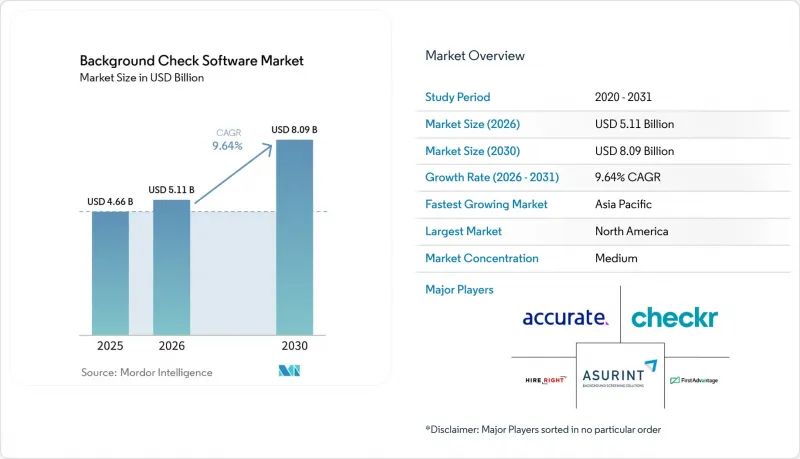

根據 Mordor Intelligence 預測,背景調查軟體市場規模將從 2025 年的 46.6 億美元成長到 2026 年的 51.1 億美元,然後在 2031 年達到 80.9 億美元,2026 年至 2031 年的複合年成長率為 9.64%。

本報告按組件(軟體和服務)、研究類型(例如,入職前篩檢)、部署模式(雲端和本地部署)、組織規模(大型企業和中小企業)、最終用戶行業(例如,IT和電信、銀行、金融服務和保險、醫療保健和生命科學、教育)以及地區進行細分。市場預測以價值(美元)表示。

全球背景調查軟體市場趨勢及洞察

零工經濟的興起和對遠距工作需求的不斷成長。

隨著《公平信用報告法案》(FCRA) 的實施,美國平台雇主預計到 2025 年將處理超過 6,800 萬份篩檢,比兩年前增加 34%。整合式 API 讓篩檢引擎和入職入口網站協同工作,讓電力用戶將招募時間從大約兩週縮短到不到 48 小時。最新產品內建的多司法管轄區合規邏輯可自動執行當地的「禁止詢問犯罪記錄」和隱私法規,從而減輕人手不足的人力資源團隊的工作量。採用率最高的是那些在多個州僱用遠距員工的 SaaS(軟體即服務)新創公司。這些趨勢正在擴大背景調查軟體市場,吸引不同的勞動力群體,並隨著承包商在不同專案間的流動,增加重新審查的頻率。

加強監管要求(FCRA、GDPR)

2025年,美國聯邦貿易委員會(FTC)針對《公平信用報告法》(FCRA)違規行為發布了23項和解令,是前兩年的兩倍,平均和解金額接近500萬美元。在歐洲, 《一般資料保護規則》(GDPR)第22條規定,自動化決策必須經過人工審核,要求供應商增加解釋機制。這會使處理時間增加一個工作日,但可以降低錯誤率。英國資訊專員於2025年1月發布的指南規定,處理大多數犯罪記錄資訊必須獲得候選人的明確同意。合規相關支出佔中型供應商收入的8%至11%,但對於財務實力雄厚的供應商而言,由於其龐大的基本客群,審計成本可以分攤,從而實現規模經濟。這些壓力可能會繼續推動以法律模板、審計追蹤和特定司法管轄區工作流程為標準功能的平台的普及。

嚴格的資料隱私法限制資料共用

印度的《數位個人資料保護法》禁止在未經同意和監管部門批准的情況下跨境傳輸犯罪記錄數據,迫使跨國供應商建立區域資料中心或與當地機構合作。中國的《個人資料保護法》要求候選人選擇退出自動分析,實際上禁止了不透明的人工智慧評分模型。巴西和韓國的類似框架可能導致每次違規處以相當於年收入2%至5,000萬美元的罰款。這些分散的管理體制導致資料流碎片化,增加了工程成本,限制了許多全球客戶所期望的通用API,從而減緩了背景調查軟體市場可實現的成長速度。

細分市場分析

預計到2031年,服務業將以10.40%的複合年成長率成長,到2025年將縮小與軟體業65.15%(以收入計)的差距。企業買家依賴託管服務來應對不利行動通知、跨國隱私法規以及季度犯罪記錄審查。結合自然語言處理演算法和分析師檢驗的混合軟體包模糊了「數據」和「人工」之間的界限,同時也推高了平均售價。然而,在零工經濟平台上,高吞吐量API仍佔據軟體產業的主導地位,因為在這些平台上,決策必須在一分鐘內做出。擴展服務選項為提升銷售開闢了途徑,擴大了背景調查軟體市場,同時為供應商帶來了持續的訂閱收入。從獲利角度來看,由於可以根據季節性波動靈活調整分析師能力,服務業的利潤率可能低於純軟體業務,但隨著服務範圍的擴大,毛利將會提高。

持續的自動化並不意味著人工干預的終結。複雜的糾紛、國際調查和專業資格檢驗仍然需要人工調查,這鞏固了服務系統的基礎。能夠協調案件經理之間機器學習和任務分配的供應商,正在以最短的處理時間樹立行業標竿。正如即時監控正在將曾經的招募前成本中心轉變為貫穿整個職業生涯的合規環節一樣,這種協調能力也正在成為品牌差異化的關鍵因素。

到2025年,招募和入職前服務包將佔銷售額的36.45%,但成長最快的領域是全球觀察名單和負面媒體掃描,預計其複合年成長率將達到12.25%,這主要得益於洗錢防制(AML)法規的更新。金融機構現在要求對所有承包商進行即時制裁核查,從而推動了對政治影響力人物(PEP)數據每日更新的需求。同時,由於美國已有11個州限制或禁止使用信用報告,信用報告市場正在萎縮。

儘管對犯罪背景調查的需求仍然旺盛,但一個主要障礙是,如果縣法院不提供電子記錄,處理時間可能長達一週。生物識別和其他身份驗證流程如今至關重要。對於學歷和執照證明,區塊鏈專案正在被應用,發證機構將防篡改的資格資訊記錄在分散式帳本上,從而將驗證時間從幾天縮短到幾分鐘。這些綜效促使預算重新分配到持續更新的內容上,背景調查軟體市場也正向訂閱式經營模式轉型。

區域分析

預計到2025年,北美將佔背景調查軟體市場收入的41.50%,這主要得益於2024年至2025年間與《公平信用報告法》(FCRA)相關的訴訟和解金額總合12億美元。供應商正在投資建造爭議解決平台和消費者通知流程,以降低集體訴訟的風險。加拿大提案的C-27法案將強制要求進行演算法影響評估,並加強模型權重和訓練資料的透明度。墨西哥2025年的外包改革將對大部分合約工進行重新分類,擴大篩檢,並推動交易量達到兩位數成長。美國聯邦貿易委員會(FTC)即將訂定的商業監管規則可能會限制第三方資料仲介的資料供應,從而對嚴重依賴外部資料來源的平台構成壓力。

亞太地區是成長最快的地區,預計到2031年將以12.85%的複合年成長率成長。印度的《數位個人資料保護法》強制要求跨境資料傳輸必須獲得明確同意,這鼓勵了主要供應商建立國內資料中心。中國的《個人資料保護法》強制要求以可解釋的人工智慧取代不透明的評分系統,這不僅促使程式碼重構,也為注重透明度的優質服務開闢了市場。在日本,2024年對《個人資料保護法》的修訂創建了一個充分性決定清單,簡化了來自美國和歐洲的資料流,加速了跨國公司的部署。印尼和越南的行動優先趨勢強勁,由於寬頻連接的桌上型電腦在都市區仍然很少見,因此他們依賴自拍和近距離場通訊(NFC)技術來獲取身分識別資訊。

歐洲的情況介於兩者之間,GDPR第22條的嚴格規定增加了人工審核的負擔,導致處理時間延長,但準確性有所提高。英國脫歐後,可能偏離GDPR的部分同意機制,從而可能形成雙重框架。在德國,覆蓋超過20%員工的專案需要獲得工人代表委員會的批准,這構成了實施的結構性障礙。同時,在中東和非洲,與國家數位身分系統相關的早期實施正在推進,例如阿拉伯聯合大公國的身份系統改革,可以將身分驗證時間縮短至幾分鐘。儘管南非的《資料保護法》意味著非洲大陸的法律法規尚未統一,但跨國公司正在將本地政策提升至全球標準,並為在非洲的擴張奠定基礎。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 零工經濟的興起和對遠距工作需求的不斷成長。

- 加強監管要求(FCRA、GDPR)

- 網路安全問題正在推動身份驗證技術的整合。

- 人力資源科技的整合正在推動嵌入式篩檢API的發展。

- 利用人工智慧技術篩檢負面媒體可以縮短處理時間。

- 基於區塊鏈的憑證錢包正變得越來越受歡迎。

- 市場限制因素

- 嚴格的資料隱私法限制資料共用

- 新興市場中小企業面臨的高解決方案成本

- 人工智慧演算法偏見引發的訴訟風險

- 全球犯罪記錄資料庫分散

- 產業價值/價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 按組件

- 軟體

- 服務

- 檢查類型

- 入職前篩檢

- 犯罪紀錄調查

- 身份驗證和社會安全號碼 (SSN) 驗證

- 信用和財務歷史

- 核實教育背景和資格

- 全球觀察名單與負面媒體報道

- 其他類型的檢查

- 不同的發展

- 雲

- 現場

- 按組織規模

- 大公司

- 中小企業

- 按最終用途行業分類

- IT/通訊

- BFSI

- 醫療保健和生命科學

- 政府/公共部門

- 製造業

- 零售與電子商務

- 教育

- 其他終端用戶產業

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲

- 其他亞太國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他中東國家

- 非洲

- 南非

- 埃及

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Sterling Infosystems, Inc.

- HireRight Holdings Corporation

- First Advantage Corporation

- Checkr, Inc.

- Accurate Background, LLC

- IntelliCorp Records, Inc.

- Inflection Risk Solutions, LLC

- Orange Tree Employment Screening, LLC

- Asurint, LLC

- Information Mart, Inc.

- Verified Credentials, Inc.

- Employment Screening Resources LLC

- Onfido Limited

- Certn Inc.

- PeopleCheck Pty Ltd

- Triton Canada Inc.

- Pinkerton Consulting and Investigations, Inc.

- SpringRole Technologies Pvt. Ltd.

- Choice Screening, Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the background check software market size is expected to grow from USD 4.66 billion in 2025 to USD 5.11 billion in 2026 and is forecast to reach USD 8.09 billion by 2031 at 9.64% CAGR over 2026-2031.

This report is Segmented by Component (Software, and Services), Check Type (Employment/Pre-Hire Screening, and More), Deployment (Cloud, and On-Premise), Organization Size (Large Enterprises, and Small and Medium Enterprises), End-Use Industry (IT and Telecommunication, BFSI, Healthcare and Life-Sciences, Education, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Background Check Software Market Trends and Insights

Rising Gig-Economy and Remote Hiring Demand

Platform employers processed more than 68 million screens in the United States during 2025, up 34% from two years earlier, after FCRA obligations were extended to ride-hailing and delivery contractors. Integrated APIs now connect screening engines to onboarding portals so power-users can cut time-to-hire from roughly two weeks to fewer than 48 hours. Multijurisdictional compliance logic embedded in modern products automatically applies local ban-the-box and privacy rules, easing the operational burden on lean human-resources teams. Adoption is spreading fastest among software-as-a-service start-ups that hire fully remote staff across several states. These trends enlarge the background check software market by pulling in non-traditional worker categories and by raising the frequency of rescreens as contractors flow in and out of projects.

Increasing Regulatory Mandates (FCRA, GDPR)

The U.S. Federal Trade Commission issued 23 consent decrees for FCRA non-compliance during 2025, doubling the prior biennium and raising average settlement values to nearly USD 5 million.In Europe, Article 22 of the General Data Protection Regulation compels human review of automated decisions, compelling vendors to insert explainability layers that add one business day but reduce error rates. The U.K. Information Commissioner's January 2025 guidance now requires explicit candidate consent for most criminal-records processing. Compliance outlays have reached 8-11% of mid-tier vendor revenue yet simultaneously create scale advantages for well-funded providers able to spread audit costs across large client bases. These pressures are likely to keep raising adoption of platforms that package legal templates, audit trails, and jurisdiction-aware workflows out of the box.

Stringent Data-Privacy Laws Limiting Data Sharing

India's Digital Personal Data Protection Act bars cross-border transfer of criminal-record data without consent and regulator sign-off, forcing multinational vendors to add regional data centers and local partnerships. China's Personal Information Protection Law demands candidate opt-outs for automated profiling, effectively banning opaque AI scoring models. Similar frameworks in Brazil and South Korea threaten fines ranging from 2% of annual revenue to USD 50 million per infraction. These decentralized regimes fragment data-flows, inflate engineering overhead, and restrict the universal API vision many global clients expect, thereby slowing the attainable growth rate of the background check software market.

Other drivers and restraints analyzed in the detailed report include:

- Cyber-Security Worries Driving ID Verification Tie-Ins

- HR-Tech Consolidation Pushing Embedded Screening APIs

- High Solution Cost for SMEs in Emerging Markets

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Services are poised for a 10.40% CAGR through 2031, closing the gap with software's 65.15% revenue base in 2025. Enterprise buyers lean on managed offerings when navigating adverse-action notices, multi-country privacy rules, and quarterly criminal rescreens. Hybrid bundles that combine natural-language-processing algorithms with analyst validations blur the old boundary between bits and bodies, but they also lift average selling prices. Among gig-economy platforms that require sub-one-minute decisions, however, high-throughput APIs maintain a software lead. The widening menu supports upsell paths that enlarge the background check software market while giving vendors recurring subscription visibility. In monetization terms, enhanced services lift gross profit even as margins stay below pure software because analyst capacity can be flexed to meet seasonality.

Ongoing automation does not spell the end of human intervention. Complex disputes, international checks, and professional-license verifications still require manual research, which entrenches the services line. Vendors that orchestrate task routing between machine learning and case managers achieve the shortest turnaround benchmarks. Such orchestration is emerging as a brand differentiator just as real-time monitoring converts what once was a pre-hire cost center into a career-long compliance layer.

Employment and pre-hire packages held 36.45% revenue share in 2025, but the fastest lane is global watch-list and adverse-media scans projected at a 12.25% CAGR thanks to updated anti-money laundering (AML) rules. Financial institutions now require real-time sanction vetting for every contractor, magnifying demand for daily refreshes of politically exposed persons (PEP) data. At the same time, credit reports face a shrinking niche after 11 U.S. states limited or banned their use.

Criminal-history searches remain large but are hampered when county courts lack digital record feeds, so turnaround can stretch to one week. Identity-verification layers such as biometric liveness checks are now table stakes. Education and license attestations are benefiting from blockchain projects where issuers place tamper-proof credentials on distributed ledgers, cutting verification cycles from days to minutes. The cumulative effect reallocates budget toward content that updates continuously, nudging the background check software market toward subscription economics.

Geography Analysis

North America contributed 41.50% of background check software market revenue in 2025, supported by FCRA litigation settlements that totaled USD 1.2 billion in 2024-2025. Vendors invest in dispute-resolution portals and consumer notice workflows to reduce class-action exposure. Canada's proposed Bill C-27 would mandate algorithmic-impact assessments, forcing transparency into model weights and training data. Mexico's 2025 outsourcing reform reclassified large segments of contract labor, swelling the screening universe and driving double-digit transaction growth. Looking forward, a forthcoming U.S. Federal Trade Commission commercial-surveillance rule could curtail third-party data-broker feeds, pressuring platforms that rely heavily on external data sources.

Asia-Pacific is the highest-velocity region, forecast to expand at a 12.85% CAGR through 2031. India's Digital Personal Data Protection Act obliges explicit consent for cross-border data transfers and pushed leading vendors to erect in-country data centers. China's Personal Information Protection Law forces the replacement of opaque scoring with explainable AI, compelling code refactoring but also opening a premium tier for transparency. Japan's 2024 amendment to its Act on the Protection of Personal Information created an adequacy list that simplifies data flows from the United States and Europe, accelerating multinational rollouts. Indonesia and Vietnam, deeply mobile-first, rely on selfie and near-field-communication ID capture because broadband desktops remain rare outside urban cores.

Europe occupies a middle position where strict GDPR Article 22 clauses enlarge human-review overhead, lengthening turnaround yet increasing accuracy. The United Kingdom may diverge from some GDPR consent mechanics post-Brexit, creating dual frameworks. Germany's works-council approval requirement for programs covering beyond 20% of staff represents a structural adoption barrier. Meanwhile, the Middle East and Africa witness early adoption tied to national digital-identity systems such as the Emirates ID revamp, which can slash verification times to minutes. South Africa's Protection of Personal Information Act still leaves the continent fragmented, but multinationals upgrade policies there to global standards, setting a beachhead for wider African expansion.

- Sterling Infosystems, Inc.

- HireRight Holdings Corporation

- First Advantage Corporation

- Checkr, Inc.

- Accurate Background, LLC

- IntelliCorp Records, Inc.

- Inflection Risk Solutions, LLC

- Orange Tree Employment Screening, LLC

- Asurint, LLC

- Information Mart, Inc.

- Verified Credentials, Inc.

- Employment Screening Resources LLC

- Onfido Limited

- Certn Inc.

- PeopleCheck Pty Ltd

- Triton Canada Inc.

- Pinkerton Consulting and Investigations, Inc.

- SpringRole Technologies Pvt. Ltd.

- Choice Screening, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Gig-Economy and Remote Hiring Demand

- 4.2.2 Increasing Regulatory Mandates (FCRA, GDPR)

- 4.2.3 Cyber-Security Worries Driving ID Verification Tie-Ins

- 4.2.4 HR-Tech Consolidation Pushing Embedded Screening APIs

- 4.2.5 AI-Powered Adverse-Media Scans Cut Turnaround Time

- 4.2.6 Blockchain-Based Credential Wallets Gain Traction

- 4.3 Market Restraints

- 4.3.1 Stringent Data-Privacy Laws Limiting Data Sharing

- 4.3.2 High Solution Cost for SMEs in Emerging Markets

- 4.3.3 Litigation Risk from Biased AI Algorithms

- 4.3.4 Fragmented Global Criminal-Record Databases

- 4.4 Industry Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Check Type

- 5.2.1 Employment / Pre-Hire Screening

- 5.2.2 Criminal History Check

- 5.2.3 Identity and SSN Verification

- 5.2.4 Credit and Financial History

- 5.2.5 Education and License Verification

- 5.2.6 Global Watch-List and Adverse-Media Scan

- 5.2.7 Other Check Types

- 5.3 By Deployment

- 5.3.1 Cloud

- 5.3.2 On-Premise

- 5.4 By Organization Size

- 5.4.1 Large Enterprises

- 5.4.2 Small and Medium Enterprises (SMEs)

- 5.5 By End-Use Industry

- 5.5.1 IT and Telecommunication

- 5.5.2 BFSI

- 5.5.3 Healthcare and Life-Sciences

- 5.5.4 Government and Public Sector

- 5.5.5 Manufacturing

- 5.5.6 Retail and E-Commerce

- 5.5.7 Education

- 5.5.8 Other End-Use Industries

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 South Korea

- 5.6.3.5 Australia

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Argentina

- 5.6.4.3 Rest of South America

- 5.6.5 Middle East

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Egypt

- 5.6.6.3 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Sterling Infosystems, Inc.

- 6.4.2 HireRight Holdings Corporation

- 6.4.3 First Advantage Corporation

- 6.4.4 Checkr, Inc.

- 6.4.5 Accurate Background, LLC

- 6.4.6 IntelliCorp Records, Inc.

- 6.4.7 Inflection Risk Solutions, LLC

- 6.4.8 Orange Tree Employment Screening, LLC

- 6.4.9 Asurint, LLC

- 6.4.10 Information Mart, Inc.

- 6.4.11 Verified Credentials, Inc.

- 6.4.12 Employment Screening Resources LLC

- 6.4.13 Onfido Limited

- 6.4.14 Certn Inc.

- 6.4.15 PeopleCheck Pty Ltd

- 6.4.16 Triton Canada Inc.

- 6.4.17 Pinkerton Consulting and Investigations, Inc.

- 6.4.18 SpringRole Technologies Pvt. Ltd.

- 6.4.19 Choice Screening, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

身分驗證軟體市場規模、佔有率和趨勢分析報告:按組件、部署模式、類型、企業規模、最終用途、地區和細分市場預測(2026-2033 年)

身分驗證軟體市場規模、佔有率和趨勢分析報告:按組件、部署模式、類型、企業規模、最終用途、地區和細分市場預測(2026-2033 年) 背景調查:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)

背景調查:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年) 身分驗證解決方案市場預測—全球身分驗證類型、認證方法、階段、用例、最終用戶和地區分析—2034年

身分驗證解決方案市場預測—全球身分驗證類型、認證方法、階段、用例、最終用戶和地區分析—2034年 身分驗證市場:2026-2032年全球市場預測(按服務類型、驗證管道、資料類型、用例、產業、部署模式和組織規模分類)

身分驗證市場:2026-2032年全球市場預測(按服務類型、驗證管道、資料類型、用例、產業、部署模式和組織規模分類) 身分驗證市場規模、佔有率、趨勢和預測:按類型、組件、部署模式、組織規模、行業和地區分類,2026-2034 年

身分驗證市場規模、佔有率、趨勢和預測:按類型、組件、部署模式、組織規模、行業和地區分類,2026-2034 年 線上背景調查市場:按應用程式和地區分類身份驗證市場:按技術和地區分類通訊身分與認證服務:市場佔有率分析、產業趨勢與統計資料、成長預測(2026-2031 年)

線上背景調查市場:按應用程式和地區分類身份驗證市場:按技術和地區分類通訊身分與認證服務:市場佔有率分析、產業趨勢與統計資料、成長預測(2026-2031 年) 2026年全球創作者驗證平台市場報告2026年全球身分驗證軟體市場報告

2026年全球創作者驗證平台市場報告2026年全球身分驗證軟體市場報告