|

市場調查報告書

商品編碼

2044046

通訊身分與認證服務:市場佔有率分析、產業趨勢與統計資料、成長預測(2026-2031 年)Telecom Identity And Authentication Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

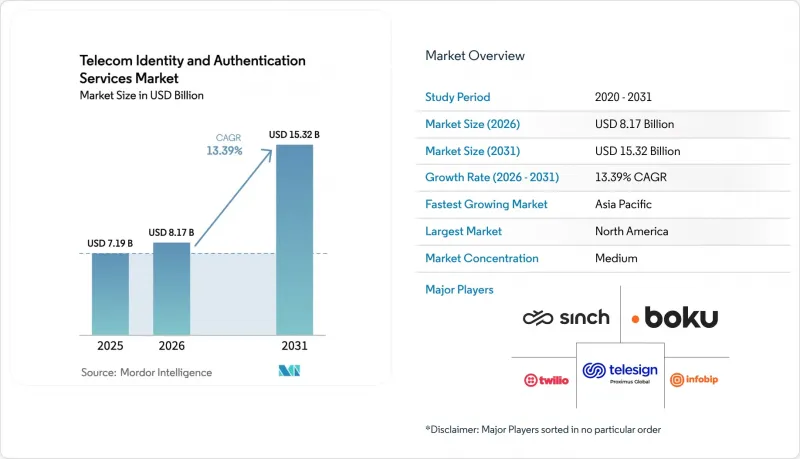

預計到 2025 年,通訊身分和認證服務市場規模將達到 71.9 億美元,到 2026 年將達到 81.7 億美元,到 2031 年將達到 153.2 億美元。

從2026年到2031年,市場預計將以13.39%的複合年成長率成長。對網路層級檢驗的強勁需求、SIM卡交換詐騙的激增以及行動通訊業者(MNO)面臨的獲利壓力,正在擴大那些將可程式設計電信憑證視為核心安全措施的企業的覆蓋範圍。儘管解決方案在2025年佔據了較大的收入佔有率,但託管服務正以更快的速度成長,因為銀行、零售商和金融科技公司更傾向於將監管合規性與即時詐欺偵測功能相結合的承包整合方案。由於支付高峰時段身份驗證工作負載激增,雲端採用佔據主導地位,並受益於彈性擴展。從地理上看,北美仍然是最大的收入來源,而亞太地區是成長最快的地區,這主要得益於政府主導的、利用通訊業者API的數位身分計畫。市場競爭強度適中。通訊聚合商(如 Twilio、Sinch 和 Infobip)與專業身分平台(如 Prove 和 Trulioo)展開競爭,而硬體安全廠商(如 Thales 和 IDEMIA)則利用其在安全元件方面的專業知識來部署嵌入式驗證解決方案。

全球通訊身分及認證服務市場趨勢及洞察

行動網路營運商數位身分API的擴展

行動網路營運商 (MNO) 正在將用戶資料轉化為可程式設計的身份識別原語。 GSMA 的 Mobile Connect 計畫在 2025 年底前在 31 個國家完成 47 次部署,透過單一合約為企業提供 SIM 卡交換檢查、裝置綁定和靜默檢驗等功能。沃達豐的 TrustHub 於 2025 年 2 月推出,提供 RESTful API,並承諾 99.99% 的運轉率,從而降低了需要滿足即時反詐騙措施的銀行的整合門檻。西班牙電信 (Telefónica) 於 2025 年 6 月將類似功能整合到 Azure Active Directory 中,顯示營運商身分驗證正逐漸成為雲端基礎架構的功能,而不再只是一項獨立的電信服務。競爭的焦點正從單純的連接性轉向延遲、詐欺訊號擴散和商業性透明度。預計在 2026 年至 2027 年間,更多歐洲和拉丁美洲的通訊業者將連接 API,進一步實現標準化,並擴大地理覆蓋範圍。

SIM卡交換和帳戶劫持詐騙呈現上升趨勢。

根據美國聯邦調查局 (FBI) 於 2026 年 3 月發布的《網路犯罪報告》,2025 年 SIM 卡交換事件增加了 48%,全球損失超過 27 億美元。攻擊者利用零售店的社交工程漏洞轉移號碼、攔截一次性驗證碼並繞過雙因素認證。為此,美國聯邦通訊委員會 (FCC) 於 2025 年 11 月頒布了一項規則,要求通訊業者在處理 SIM 卡變更之前應用多因素身份驗證。 2026 年 1 月,T-Mobile 推出了一項“帳戶盜用預防功能”,該功能會在 SIM 卡變更後自動禁用身份驗證 24 小時,以防止欺詐性使用。網路保險公司現在要求運營商級身份驗證作為承保的先決條件,這迫使各公司放棄易受攻擊的短信一次性驗證碼流程,轉而採用“靜默網路檢查”,以檢驗SIM 卡保留期限、設備指紋和最近的號碼可攜性歷史記錄。

關於集中式用戶資料儲存庫的隱私問題

2025年3月,歐洲資料保護委員會裁定,提供身分識別服務的通訊業者是完全的資料控制者,並對其施加了GDPR規定的義務,例如資料保護影響評估和72小時內通知資料外洩。歐洲電信網路營運商協會(ETNO)估計,合規負擔將使中小型業者的營運成本增加22%,有些業者甚至選擇不提供身分識別API。計劃者警告說,一次資料外洩可能導致數百萬用戶記錄遺失,從而可能被用於大規模監控和詐騙。因此,監管機構正在推動採用令牌化驗證方法,以在不持久保存個人識別碼的情況下證明SIM卡所有權。這種設計變更可能會減緩歐洲和美國一些對隱私高度敏感的州在2027年之前部署相關平台的速度。

細分市場分析

截至2025年,解決方案僅佔通訊業身分和認證服務市場收入的63.40%,但預計服務領域將以15.40%的複合年成長率成長,並在2031年超過解決方案。企業選擇託管認證是為了避免資本投資,透過數百家業通訊業者確保快速覆蓋全球,並將監管變更的管理外包出去。 Twilio在2025年以32億美元收購Segment,將客戶資料編配與基於號碼的認證相結合,展現了其專注於建立整合技術堆疊的決心,該技術堆疊能夠將行為洞察轉化為自適應認證挑戰。

在受嚴格監管、無法依賴多租戶雲端的產業中,解決方案仍然至關重要。遷移大型主機應用程式的銀行和受資料主權法規約束的醫院正在部署本地引擎,這些引擎可直接存取SS7標準和專用硬體安全模組。在這些領域,訂閱模式也越來越受歡迎。授權合約擴大包含持續的規則集更新和全天候欺詐檢測信息,模糊了永久許可軟體和託管服務之間的界限。因此,供應商正在完善混合模式,這些模式既能提供雲端分析功能,又能本地處理敏感數據,從而在不犧牲可擴展性的前提下保持合規性。

預計到 2025 年,雲端採用將佔通訊業身分和認證服務市場佔有率的 68.81%,到 2031 年將維持兩位數成長,複合年成長率 (CAGR) 為 15.11%。這主要歸因於即時支付對低延遲、彈性擴展和地理冗餘的需求日益成長。 Sinch 透過新增 18 個 AWS 區域擴展部署後,將其平均 API 回應時間從 340 毫秒縮短至 180 毫秒,從而顯著提升了結帳轉換率。

儘管本地部署的比例逐年下降,但在那些擁有監管跨境資料傳輸的國內法律的國家,本地部署仍然保持強勁勢頭。國防機構、關鍵基礎設施營運商以及德國和阿拉伯聯合大公國等市場的主權雲指令也支撐著部分需求。混合配置十分常見。企業透過在內部防火牆後運作決策引擎、呼叫雲端端點進行SIM卡交換檢查以及利用快取結果,在最大限度減少外部資料傳輸的同時,保持亞秒級的使用者體驗。

區域分析

到2025年,北美將佔通訊業身分識別和認證服務市場收入的36.22%。這主要得益於銀行業和醫療保健產業早期採用多因素認證(MFA)強制措施,以及載波聚合技術使得美國和加拿大境內的API呼叫速度達到亞秒。雖然5G的廣泛部署正在提升靜默認證的訊號質量,但網路保險的要求正迫使企業逐步淘汰傳統的簡訊驗證碼(SMS OTP)。

儘管歐洲的成長更為穩定,但卻受到嚴格的隱私法的限制。該地區受益於PSD2指令的協調統一,但各國的實施情況不盡相同,這增加了跨境電子商務的複雜性。例如,Orange和德國電信於2025年10月宣布成立的“歐洲認同平台”,旨在提供符合eIDAS 2.0要求的、與歐洲大陸錢包相容的服務,但其全面部署取決於成員國之間的協調程度。

亞太地區以16.72%的複合年成長率快速成長,主要驅動力來自印度對高價值UPI交易的SIM卡綁定要求,以及印尼在用戶註冊過程中引入通訊業者驗證的國家數位身分體系。中國OEM廠商在行動電話市場的主導地位正在加速eSIM的普及,迫使通訊業者重構其認證邏輯,轉向基於憑證的檢驗。同時,東南亞新興市場正快速擺脫紙本身分認證流程,直接利用營運商API為通訊業者經濟從業人員提供簡化的KYC註冊流程。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 擴展面向行動網路營運商 (MNO) 的數位身分 API

- SIM卡交換和帳戶劫持詐騙呈現上升趨勢。

- 穩健的客戶身份驗證的監管要求

- eSIM和物聯網設備認證的興起

- 通訊業者採用分散式識別碼框架

- 獲利壓力導致了「身分即服務 (IaaS)」服務的出現。

- 市場限制因素

- 關於集中式用戶資料儲存庫的隱私問題

- 行動虛擬網路營運商和中小企業的認知度較低

- 行動網路業者與身分聚合商之間複雜的收益分成模式

- 國際KYC標準碎片化

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素的影響

- 波特五力分析

- 新進入者的威脅

- 供應商的議價能力

- 買方的議價能力

- 替代品的威脅

- 產業間競爭

第5章 市場規模與成長預測

- 按組件

- 解決方案

- 服務

- 部署模式

- 現場

- 雲

- 按身份驗證類型

- 基於簡訊的一次性密碼

- 行動生物識別

- 多因素身份驗證令牌

- 數位身份驗證 API

- 最終用戶

- 行動網路營運商

- 虛擬行動服務業者

- OTT服務供應商

- 公司

- 按行業

- 金融服務

- 電子商務與零售

- 政府和公共部門

- 衛生保健

- 媒體與娛樂

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地區

- 歐洲

- 德國

- 英國

- 法國

- 俄羅斯

- 其他歐洲地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 亞太其他地區

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 其他非洲地區

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Boku Inc.

- Infobip DOO

- Telesign Corporation

- Sinch AB

- Twilio Inc.

- Mobileum Inc.

- Prove Identity Inc.

- Callsign Limited

- 1Kosmos Inc.

- Trulioo Information Services Inc.

- Authlete, Inc.

- Tru.ID Limited

- IDEMIA Group SAS

- Giesecke+Devrient GmbH

- Thales SA

- Amdocs Limited

- Tyntec GmbH

- Mitek Systems Inc.

- Aeris Communications Inc.

- Nexmo Inc.(Vonage)

第7章 市場機會與未來展望

The Telecom Identity and Authentication Services Market size is projected to be USD 7.19 billion in 2025, USD 8.17 billion in 2026, and reach USD 15.32 billion by 2031, growing at a CAGR of 13.39% from 2026 to 2031. Strong demand for network-level verification, escalating SIM-swap fraud, and monetization pressure on mobile network operators (MNOs) are expanding the addressable base of enterprises that now treat programmable telecom credentials as a core security control. Solutions captured a significant share of revenue in 2025, though managed services are scaling faster because banks, retailers, and fintechs prefer turnkey integrations that bundle regulatory compliance and real-time fraud intelligence. Cloud deployments dominate because authentication workloads spike during peak payment windows and benefit from elastic scaling. Geographically, North America remains the largest revenue contributor, while Asia-Pacific is the fastest-growing region, driven by government digital-identity schemes that use carrier APIs. Competitive intensity is moderate: messaging aggregators such as Twilio, Sinch, and Infobip compete with specialist identity platforms such as Prove and Trulioo, while hardware security vendors, including Thales and IDEMIA, leverage secure-element expertise to launch embedded authentication offerings.

Global Telecom Identity And Authentication Services Market Trends and Insights

Expansion of MNO Digital-Identity APIs

MNOs are transforming subscriber data into programmable identity primitives. GSMA's Mobile Connect reached 47 deployments across 31 countries by the end of 2025, giving enterprises a single contract for SIM-swap checks, device binding, and silent verification. Vodafone's TrustHub, launched in February 2025, exposes RESTful APIs with 99.99% uptime SLAs, lowering integration friction for banks that must satisfy real-time fraud controls. Telefonica integrated the same capabilities into Azure Active Directory in June 2025, signaling that carrier authentication is becoming a cloud infrastructure feature rather than a siloed telecom service. Competition now centers on latency, fraud-signal breadth, and commercial transparency rather than mere connectivity. Over 2026-2027, additional European and Latin-American operators will federate APIs, further standardizing implementation and expanding geographic coverage.

Surge in SIM-Swap and Account-Takeover Fraud

SIM-swap incidents grew 48% in 2025, generating global losses above USD 2.7 billion, according to the FBI Internet Crime Report issued in March 2026. Attackers exploit social-engineering gaps at retail outlets to port numbers and intercept one-time codes, bypassing two-factor authentication. The U.S. FCC responded in November 2025 with rules that force carriers to apply multi-factor verification before processing SIM changes. T-Mobile rolled out Account Takeover Protection in January 2026, automatically pausing authentication for 24 hours after a SIM change to deter fraud. Cyber-insurers now require carrier-grade verification as a prerequisite for coverage, pushing enterprises to retire vulnerable SMS OTP flows in favor of silent network checks that validate SIM tenure, device fingerprinting, and recent porting events.

Privacy Concerns Over Centralized Subscriber Data Repositories

The European Data Protection Board ruled in March 2025 that operators offering identity services are full data controllers, triggering GDPR duties such as data-protection impact assessments and breach notification within 72 hours. ETNO estimates that compliance overhead lifted operating costs by 22% for small carriers, discouraging some from launching identity APIs. Advocacy groups warn that a single breach could expose millions of subscriber records, enabling mass surveillance or fraud. Consequently, regulators push for tokenized confirmations that prove SIM possession without persisting personal identifiers, a design shift likely to slow platform rollouts in Europe and privacy-sensitive U.S. states through 2027.

Other drivers and restraints analyzed in the detailed report include:

- Regulatory Mandates for Strong Customer Authentication

- Rise of eSIM and IoT Device Authentication

- Complex Revenue-Sharing Models Between MNOs and Identity Aggregators

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solutions accounted for only 63.40% of the Telecom identity and authentication services market revenue in 2025, yet the services segment is forecast to grow at a 15.40% CAGR and surpass Solutions by 2031. Enterprises choose managed authentication to avoid capital expenditure, obtain instant geographic reach across hundreds of operators, and outsource regulatory change management. Twilio's USD 3.2 billion acquisition of Segment in 2025 bundled customer-data orchestration with number-based verification, illustrating the premium placed on integrated stacks that convert behavioral insights into adaptive authentication challenges.

Solutions remain essential for highly regulated verticals that cannot rely on multi-tenant clouds. Banks migrating mainframe applications or hospitals subject to data-sovereignty statutes deploy on-premises engines with direct SS7 access and dedicated hardware security modules. Even here, a subscription mindset is emerging: license agreements increasingly include continuous rule-set updates and 24/7 fraud-intelligence feeds, blurring the line between perpetual software and managed service. Consequently, vendors are refining hybrid models that deliver cloud analytics while processing sensitive payloads locally, preserving compliance without conceding scalability.

Cloud deployments commanded 68.81% of the Telecom identity and authentication services market share in 2025 and will sustain double-digit growth at a 15.11% CAGR by 2031, as latency, elastic scaling, and geographic redundancy are non-negotiable for real-time payments. Sinch trimmed the average API response time from 340 ms to 180 ms after expanding its footprint to 18 additional AWS regions, delivering a measurable uplift in checkout conversion rates.

On-premise adoption shrinks each year but resists extinction in countries where national rules restrict cross-border data transfers. Defense agencies, critical-infrastructure operators, and sovereign cloud mandates in markets such as Germany and the United Arab Emirates keep a rump demand alive. Hybrid postures are popular: enterprises run decision engines behind corporate firewalls yet call cloud endpoints for SIM-swap checks, leveraging cached results to minimize external data transfer while sustaining sub-second user experiences.

The Telecom Identity and Authentication Services Market Report is Segmented by Component (Solutions and Services), Deployment Mode (On-Premise and Cloud), Authentication Type (SMS-Based OTP, Mobile Biometrics, and More), End-User (Mobile Network Operators, and More), Industry Vertical (Financial Services, Ecommerce and Retail, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America contributed 36.22% of the Telecom identity and authentication services market revenue in 2025, anchored by early adoption of MFA mandates in banking and healthcare and supported by direct carrier aggregation that enables sub-second API calls across the United States and Canada. Widespread 5G rollout improves signal quality for silent verification, while cyber-insurance prerequisites compel enterprises to sunset legacy SMS OTP.

Europe's growth is steadier but shaped by stringent privacy laws. The region benefits from harmonized PSD2 directives, yet implementation varies by country, adding complexity for cross-border ecommerce. Joint ventures such as the Orange and Deutsche Telekom European Identity Platform, announced in October 2025, aim to deliver a continent-wide wallet-compatible service that meets eIDAS 2.0 requirements, but the full rollout depends on member-state alignment.

Asia-Pacific, expanding at 16.72% CAGR, is propelled by India's SIM binding requirement for high-value UPI transactions and Indonesia's national digital ID that embeds telecom checks at onboarding. Chinese OEM dominance in the handset market is accelerating eSIM adoption, compelling carriers to rewrite their authentication logic for certificate-based validation. Meanwhile, emerging markets in Southeast Asia leapfrog straight to carrier APIs for KYC-lite onboarding of gig-economy workers, bypassing paper ID processes.

List of Companies Covered in this Report:

- Boku Inc.

- Infobip D.O.O.

- Telesign Corporation

- Sinch AB

- Twilio Inc.

- Mobileum Inc.

- Prove Identity Inc.

- Callsign Limited

- 1Kosmos Inc.

- Trulioo Information Services Inc.

- Authlete, Inc.

- Tru.ID Limited

- IDEMIA Group S.A.S.

- Giesecke+Devrient GmbH

- Thales S.A.

- Amdocs Limited

- Tyntec GmbH

- Mitek Systems Inc.

- Aeris Communications Inc.

- Nexmo Inc. (Vonage)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expansion of Mobile Network Operator Digital Identity APIs

- 4.2.2 Surge in SIM Swap and Account Takeover Fraud

- 4.2.3 Regulatory Mandates for Strong Customer Authentication

- 4.2.4 Rise of eSIM and IoT Device Authentication

- 4.2.5 Telco Adoption of Decentralized Identifier Frameworks

- 4.2.6 Monetization Pressure Leading to Identity-As-A-Service Offerings

- 4.3 Market Restraints

- 4.3.1 Privacy Concerns Over Centralized Subscriber Data Repositories

- 4.3.2 Limited Awareness Among MVNOs and SMEs

- 4.3.3 Complex Revenue-Sharing Models Between MNOs and Identity Aggregators

- 4.3.4 Fragmented International KYC Standards

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Industry Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Solutions

- 5.1.2 Services

- 5.2 By Deployment Mode

- 5.2.1 On-Premise

- 5.2.2 Cloud

- 5.3 By Authentication Type

- 5.3.1 SMS-Based OTP

- 5.3.2 Mobile Biometrics

- 5.3.3 Multi-Factor Authentication Token

- 5.3.4 Digital Identity Verification API

- 5.4 By End-User

- 5.4.1 Mobile Network Operators

- 5.4.2 Mobile Virtual Network Operators

- 5.4.3 Over-The-Top Service Providers

- 5.4.4 Enterprises

- 5.5 By Industry Vertical

- 5.5.1 Financial Services

- 5.5.2 Ecommerce and Retail

- 5.5.3 Government and Public Sector

- 5.5.4 Healthcare

- 5.5.5 Media and Entertainment

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Russia

- 5.6.3.5 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 Saudi Arabia

- 5.6.5.1.2 United Arab Emirates

- 5.6.5.1.3 Rest of the Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Nigeria

- 5.6.5.2.3 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share For Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Boku Inc.

- 6.4.2 Infobip D.O.O.

- 6.4.3 Telesign Corporation

- 6.4.4 Sinch AB

- 6.4.5 Twilio Inc.

- 6.4.6 Mobileum Inc.

- 6.4.7 Prove Identity Inc.

- 6.4.8 Callsign Limited

- 6.4.9 1Kosmos Inc.

- 6.4.10 Trulioo Information Services Inc.

- 6.4.11 Authlete, Inc.

- 6.4.12 Tru.ID Limited

- 6.4.13 IDEMIA Group S.A.S.

- 6.4.14 Giesecke+Devrient GmbH

- 6.4.15 Thales S.A.

- 6.4.16 Amdocs Limited

- 6.4.17 Tyntec GmbH

- 6.4.18 Mitek Systems Inc.

- 6.4.19 Aeris Communications Inc.

- 6.4.20 Nexmo Inc. (Vonage)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

- 7.2 Analyst Recommendations and Suggestions

身分驗證軟體市場規模、佔有率和趨勢分析報告:按組件、部署模式、類型、企業規模、最終用途、地區和細分市場預測(2026-2033 年)

身分驗證軟體市場規模、佔有率和趨勢分析報告:按組件、部署模式、類型、企業規模、最終用途、地區和細分市場預測(2026-2033 年) 背景調查:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)背景調查軟體:市佔率分析、產業趨勢與統計、成長預測(2026-2031)

背景調查:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)背景調查軟體:市佔率分析、產業趨勢與統計、成長預測(2026-2031) 身分驗證解決方案市場預測—全球身分驗證類型、認證方法、階段、用例、最終用戶和地區分析—2034年

身分驗證解決方案市場預測—全球身分驗證類型、認證方法、階段、用例、最終用戶和地區分析—2034年 身分驗證市場:2026-2032年全球市場預測(按服務類型、驗證管道、資料類型、用例、產業、部署模式和組織規模分類)

身分驗證市場:2026-2032年全球市場預測(按服務類型、驗證管道、資料類型、用例、產業、部署模式和組織規模分類) 身分驗證市場規模、佔有率、趨勢和預測:按類型、組件、部署模式、組織規模、行業和地區分類,2026-2034 年

身分驗證市場規模、佔有率、趨勢和預測:按類型、組件、部署模式、組織規模、行業和地區分類,2026-2034 年 線上背景調查市場:按應用程式和地區分類身份驗證市場:按技術和地區分類

線上背景調查市場:按應用程式和地區分類身份驗證市場:按技術和地區分類 2026年全球創作者驗證平台市場報告2026年全球身分驗證軟體市場報告

2026年全球創作者驗證平台市場報告2026年全球身分驗證軟體市場報告