|

市場調查報告書

商品編碼

2065746

歐洲巴士市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Europe Bus - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

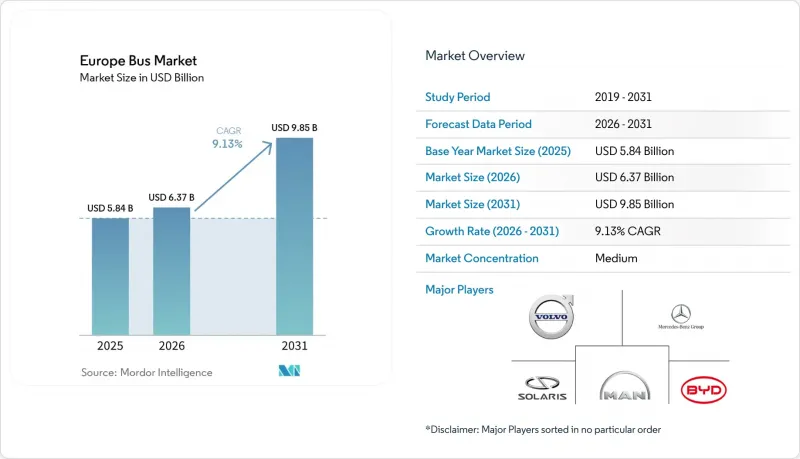

根據 Mordor Intelligence 預測,歐洲巴士市場規模將從 2025 年的 58.4 億美元成長到 2026 年的 63.7 億美元,然後在 2031 年達到 98.5 億美元,2026 年至 2031 年的複合年成長率為 9.13%。

本報告按車身類型(單層和雙層)、用途(例如,線路公車)、燃料類型(例如,柴油、純電動)、座位數(例如,30座或以下)、車身長度(9米以下、9-12米、12米以上)和地區進行細分。市場預測以貨幣價值(美元)和銷售(輛)兩種形式呈現。

歐洲巴士市場的趨勢和洞察

歐盟清潔浴室法規(2025 年和 2030 年目標)

根據《清潔車輛指令》,成員國必須確保到2025年其採購的公車中有相當一部分是清潔能源車輛,這一要求到2030年將進一步加強。具體而言,這些公車中必須有一半配備零排放驅動系統。營運商正在加緊努力以滿足這項要求。例如,DB Regio已下達了大規模訂單,訂購數千輛公車。此舉不僅避免了潛在的處罰,也鞏固了對純電動公車平台的需求。顯然,實際進展遠遠超出了法規要求。到2024年,歐盟交付的新城市公車中將近一半是零排放車輛,比前一年顯著成長,這清楚地表明了車輛規劃的轉變。擁有可適應各成員國法規的模組化平台的原始設備製造商(OEM)將獲得最大的收益,並有望快速擴張。

都市區低排放區和零排放區的擴大

歐洲已有35個城市設立或宣佈設立零排放區,實際上禁止柴油公車在特定區域運作。此舉加速了內燃機(ICE)車輛的提前退役。倫敦目前營運超過1800輛電動公車,從2025年起,所有新投入營運的雙層公車都必須是零排放車輛。同樣,巴黎也在推進其RATP車隊到2025年全面電氣化的計劃,這將需要4700輛電動公車以及相應的充電基礎設施。零排放區的設立正造成市場兩極化。都市區營運商正努力應對嚴格的合規期限,而郊區營運商仍然可以柔軟性使用柴油車輛,同時,市場對長度小於9公尺、能夠靈活穿梭於城市歷史街區的高性能公車的需求也在不斷成長。

逐步減少政府對購買電動巴士的補貼

在德國,KsNI補貼已大幅削減至遠低於標價的水平。同時,英國的ZEBRA計畫已於2024年3月結束,目前尚無明顯的替代方案。為了應對資金籌措挑戰,營運商正與戴姆勒和沃爾沃等原始設備製造商簽訂電池租賃和殘值協議。鑑於財政限制,地方公車業者可能會推遲電動化進程,訂單數量也可能暫時減少,直到新的財政措施訂定。

細分市場分析

預計到2031年,雙層巴士市場將以9.15%的複合年成長率成長。因此,儘管單層巴士在2025年佔據了81.31%的市場佔有率,但預計歐洲雙層巴士市場的成長速度將超過單層巴士。近期的一些合約案例包括:向Go-Ahead Oxford交付104輛Wrightbus StreetDeck Electroliner雙層巴士,以及愛爾蘭國家交通管理局授予的800輛雙層巴士框架契約,這些都表明英國和愛爾蘭對雙層巴士的需求強勁。中國汽車製造商也嘗試進入這一領域,宇通的U11DD測試車配備了662千瓦時的電池容量,專為長途城際線路設計。這種成長與在路肩空間有限的情況下對大容量車輛的需求密切相關,尤其是在倫敦、都柏林和貝爾法斯特等城市。

由於初始投資成本低、高度限制寬鬆且服務網路成熟,單層巴士很可能仍將主導日常城市營運。然而,其成長速度放緩表明,未來的擴張將是漸進式的,而非爆發性的。汽車製造商之間的差異化將取決於其提供模組化佈局的能力,即使歐洲大陸各地的車門位置和內裝規格有所不同,這些模組化佈局也能實現快速的車型認證。

儘管2025年普通客車交付比仍高達67.37%,但預計到2031年,長途城際線路和旅遊巴士的複合年成長率將達到9.21%,成為成長最快的領域,這將徹底改變歐洲客車市場格局。沃爾沃的「8900 Electric」已獲得瑞典Svealandstrafiken公司的60輛訂單,而DB Regio則為區域路線引進了200輛比亞迪電動旅遊巴士。營運商認為,500-700公里的續航里程是其在柏林-漢堡和馬德里-瓦倫西亞等主要線路上取代柴油車輛的關鍵因素。

儘管校車和包車市場規模仍然較小,但為了符合歐盟無障礙法規,低地板無階梯巴士的普及度正在逐步提振市場需求。在城市和城際線路中共用動力系統和電子設備的原始設備製造商(OEM)正享受著規模經濟效益,提高利潤率,並簡化營運商的零件庫存管理。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 歐盟清潔浴室法規(2025 年和 2030 年目標)

- 都市區低排放區和零排放區的擴大

- 歐盟復甦與韌性基金的資本支出

- 新冠疫情後公共交通客流量的恢復

- OEM「電池即服務」和殘值保證

- 城際低地板電動巴士的競標數量增加

- 市場限制因素

- 各國逐步減少購買電動公車的補貼

- 火車車庫電網連接和電力容量出現延誤。

- 專業駕駛人短缺

- 氫燃料電池公車的初始成本很高。

- 價值供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

第5章 市場規模與成長預測

- 按甲板類型

- 單身的

- 雙倍的

- 透過使用

- 公車線路

- 城際巴士/長途巴士

- 校車

- 其他

- 按燃料類型

- 柴油引擎

- 電池式電動車

- 插電式混合動力

- 燃料電池電動車

- 其他

- 按座位數

- 30個座位或更少

- 31-50個座位

- 超過50個座位

- 按巴士長度

- 9米或以下

- 9~12 m

- 超過12米

- 國家

- 德國

- 法國

- 英國

- 義大利

- 西班牙

- 其他歐洲國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- BYD Company Ltd

- Daimler Buses(Mercedes-Benz Group AG)

- MAN Truck & Bus SE

- Volvo Group

- Solaris Bus & Coach

- Traton Group(Scania, Volkswagen CVI)

- IVECO Group(Heuliez Bus)

- VDL Bus & Coach

- Alexander Dennis Ltd

- Wrightbus

- Ebusco Holding NV

- Yutong Europe

- Irizar e-Mobility

- Van Hool

- Otokar Otomotiv

- Rampini Carbri

- Karsan

- Unvibus

- Hyzon Motors

第7章 市場機會與未來展望

According to Mordor Intelligence, the europe bus market size is expected to grow from USD 5.84 billion in 2025 to USD 6.37 billion in 2026 and is forecast to reach USD 9.85 billion by 2031 at a 9.13% CAGR over 2026-2031.

This report is Segmented by Deck Type (Single and Double), Application (Transit Bus and More), Fuel Type (Diesel, Battery Electric, and More), Seating Capacity (Up To 30 Seats and More), Bus Length (Up To 9 M, 9-12 M, and More Than 12 M), and Geography. Market Forecasts are Provided in Value (USD) and Volume (Units).

Europe Bus Market Trends and Insights

EU Clean-Bus Mandate (2025/30 Targets)

Under the Clean Vehicle Directive, member states must ensure that by 2025, a significant percentage of procured buses are clean, with this requirement increasing further by 2030 . Notably, half of these buses must feature zero-emission drivetrains. In response, operators are securing their positions: DB Regio, for instance, has placed a substantial multi-year order for thousands of units. This move not only sidesteps potential penalties but also solidifies demand for battery-electric platforms. Evidence of over-compliance is apparent: in 2024, nearly half of new city buses delivered in the EU were zero-emission, a notable increase from the previous year, showcasing a shift in fleet planning . OEMs boasting modular platforms adaptable to various member-state regulations stand to gain the most, positioning themselves for rapid scaling.

Expansion of Urban Low-/Zero-Emission Zones

Thirty-five cities across Europe have either implemented or announced zero-emission zones, effectively banning diesel buses in specific areas. This move is hastening the early retirement of internal combustion engine (ICE) assets. London currently boasts over 1,800 electric buses and has mandated that all new double-decker buses must be zero-emission starting in 2025 . Similarly, Paris is on track to fully electrify its RATP fleet by 2025, necessitating 4,700 electric buses and corresponding charging infrastructure upgrades. These zero-emission zones have led to a divided market: urban operators grapple with strict compliance deadlines, while their suburban counterparts still have the flexibility to use diesel, driving up the demand for nimble sub-9-meter buses adept at navigating the city's historic districts.

Phase-Down of National E-Bus Purchase Subsidies

Germany has reduced its KsNI subsidy to a significantly lower portion of the list price. Meanwhile, the UK's ZEBRA program lapsed in March 2024, and there's no immediate replacement in sight. To navigate financing challenges, operators are turning to battery-leasing and residual-value agreements with OEMs like Daimler and Volvo. Given their capital constraints, regional fleets might postpone electrification, leading to a temporary dip in orders until fresh fiscal solutions are introduced.

Other drivers and restraints analyzed in the detailed report include:

- Post-COVID Public-Transport Ridership Rebound

- EU Recovery and Resilience Facility Capital Spending

- Depot Grid-Connection and Power-Capacity Delays

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Double-deckers are advancing at a 9.15% CAGR through 2031. The Europe bus market size for this deck type will therefore widen faster than that of single-decks, even though single-decks commanded 81.31% share in 2025. Recent contracts include 104 Wrightbus StreetDeck Electroliners delivered to Go-Ahead Oxford and an 800-unit framework awarded by Ireland's National Transport Authority, signaling strong replacement demand in the UK and Ireland. Chinese OEMs are also testing the segment: Yutong's U11DD trial offers 662 kWh of battery capacity aimed at long-range intercity work. Growth is tied to the need for high-capacity vehicles on constrained curb space, especially in London, Dublin, and Belfast.

Single-deckers will keep dominating everyday urban operations because of lower acquisition cost, broader height clearance, and mature service networks. However, their slower growth rate suggests incremental rather than breakout volume. OEM differentiation will hinge on offering modular layouts that can be homologated quickly for varying door positions and interior specifications across continental Europe.

Transit buses drove 67.37% of 2025 deliveries but intercity and motorcoach applications will post the quickest 9.21% CAGR to 2031, transforming the Europe bus market. Volvo's 8900 Electric secured 60-unit orders from Sweden's Svealandstrafiken, while DB Regio added 200 BYD electric coaches to serve regional corridors. Operators cite 500-700 km certified range as the tipping point for diesel replacement on popular lines such as Berlin-Hamburg and Madrid-Valencia.

Although school and charter niches remain small, the shift toward step-free, low-entry coach designs to comply with EU accessibility mandates adds incremental demand. OEMs with platforms that share drivetrains and electronics across transit and intercity variants capture scale efficiencies, boosting margins while simplifying parts inventory for operators.

List of Companies Covered in this Report:

- BYD Company Ltd

- Daimler Buses (Mercedes-Benz Group AG)

- MAN Truck & Bus SE

- Volvo Group

- Solaris Bus & Coach

- Traton Group (Scania, Volkswagen CVI)

- IVECO Group (Heuliez Bus)

- VDL Bus & Coach

- Alexander Dennis Ltd

- Wrightbus

- Ebusco Holding NV

- Yutong Europe

- Irizar e-Mobility

- Van Hool

- Otokar Otomotiv

- Rampini Carbri

- Karsan

- Unvibus

- Hyzon Motors

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 EU Clean-Bus Mandate (2025/30 Targets)

- 4.2.2 Expansion of Urban Low-/Zero-Emission Zones

- 4.2.3 EU Recovery and Resilience Facility Capital Spending

- 4.2.4 Post-COVID Public-Transport Ridership Rebound

- 4.2.5 OEM "Battery-As-A-Service" and Residual-Value Guarantees

- 4.2.6 Growth of Intercity Low-Entry E-Bus Tenders

- 4.3 Market Restraints

- 4.3.1 Phase-Down of National E-Bus Purchase Subsidies

- 4.3.2 Depot Grid-Connection and Power-Capacity Delays

- 4.3.3 Professional-Driver Shortages

- 4.3.4 High Upfront Cost of Hydrogen Fuel-Cell Buses

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD) and Volume (Units))

- 5.1 By Deck Type

- 5.1.1 Single

- 5.1.2 Double

- 5.2 By Application

- 5.2.1 Transit Bus

- 5.2.2 Intercity Bus / Motorcoach

- 5.2.3 School Bus

- 5.2.4 Others

- 5.3 By Fuel Type

- 5.3.1 Diesel

- 5.3.2 Battery Electric

- 5.3.3 Plug-in Hybrid

- 5.3.4 Fuel Cell Electric

- 5.3.5 Others

- 5.4 By Seating Capacity

- 5.4.1 Up to 30 seats

- 5.4.2 31 - 50 seats

- 5.4.3 More than 50 seats

- 5.5 By Bus Length

- 5.5.1 Up to 9 m

- 5.5.2 9 - 12 m

- 5.5.3 More than 12 m

- 5.6 By Country

- 5.6.1 Germany

- 5.6.2 France

- 5.6.3 United Kingdom

- 5.6.4 Italy

- 5.6.5 Spain

- 5.6.6 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 BYD Company Ltd

- 6.4.2 Daimler Buses (Mercedes-Benz Group AG)

- 6.4.3 MAN Truck & Bus SE

- 6.4.4 Volvo Group

- 6.4.5 Solaris Bus & Coach

- 6.4.6 Traton Group (Scania, Volkswagen CVI)

- 6.4.7 IVECO Group (Heuliez Bus)

- 6.4.8 VDL Bus & Coach

- 6.4.9 Alexander Dennis Ltd

- 6.4.10 Wrightbus

- 6.4.11 Ebusco Holding NV

- 6.4.12 Yutong Europe

- 6.4.13 Irizar e-Mobility

- 6.4.14 Van Hool

- 6.4.15 Otokar Otomotiv

- 6.4.16 Rampini Carbri

- 6.4.17 Karsan

- 6.4.18 Unvibus

- 6.4.19 Hyzon Motors

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment

2026年全球客車市場報告

2026年全球客車市場報告 全球臥舖巴士市場:市場規模、佔有率、趨勢和成長分析(2026-2034)

全球臥舖巴士市場:市場規模、佔有率、趨勢和成長分析(2026-2034) 無軌電車市場分析及至2035年的預測:類型、產品類型、技術、組件、應用、最終用戶、功能、安裝配置、運輸方式2026年全球巴士市場報告2026年全球長途客車市場報告

無軌電車市場分析及至2035年的預測:類型、產品類型、技術、組件、應用、最終用戶、功能、安裝配置、運輸方式2026年全球巴士市場報告2026年全球長途客車市場報告 豪華巴士市場規模、佔有率和成長分析:按燃料類型、巴士類型、應用和地區分類-2026-2033年產業預測

豪華巴士市場規模、佔有率和成長分析:按燃料類型、巴士類型、應用和地區分類-2026-2033年產業預測 臥舖巴士市場:市場機會、成長要素、產業趨勢分析及2026-2035年預測

臥舖巴士市場:市場機會、成長要素、產業趨勢分析及2026-2035年預測 全球鉸接式巴士市場公車市場機會、成長要素、產業趨勢分析及2026-2035年預測。

全球鉸接式巴士市場公車市場機會、成長要素、產業趨勢分析及2026-2035年預測。 城際電動巴士市場預測至2034年-全球動力系統、電池容量、巴士長度、座位數、續航里程、應用及區域分析

城際電動巴士市場預測至2034年-全球動力系統、電池容量、巴士長度、座位數、續航里程、應用及區域分析