|

市場調查報告書

商品編碼

2038314

公車市場機會、成長要素、產業趨勢分析及2026-2035年預測。Bus Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

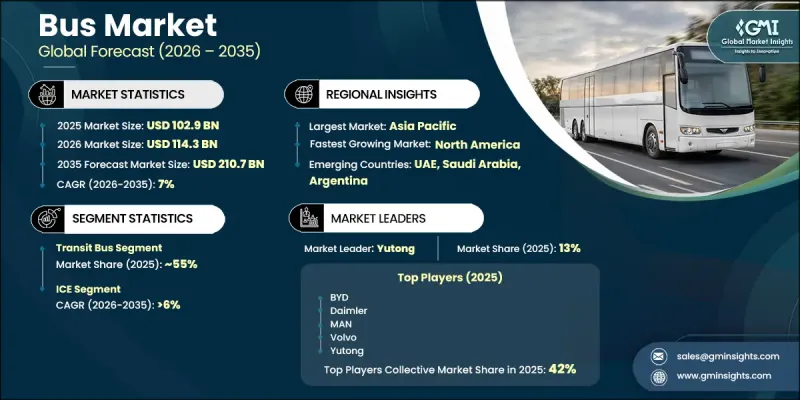

2025年全球巴士市場價值1,029億美元,預計到2035年將以7%的複合年成長率成長至2,107億美元。

不斷成長的城市人口和對公共交通基礎設施的持續投資塑造了這個市場。城市正優先考慮高容量的出行解決方案,以改善交通狀況並緩解堵塞,從而加速了整個交通網路對公車的需求。電氣化正成為核心趨勢,在政策支持和成本效益提升的推動下,純電動公車在許多地區迅速普及。車輛性能的提升,例如電池容量的增加和先進能源管理系統的應用,提高了營運可行性。同時,氫燃料公車等替代方案也開始應用於長途線路。電池成本的降低和政府的支持正在縮小傳統公車和零排放公車之間的成本差距,從而提高投資回報率(ROI)。開發中國家可負擔性的提高進一步促進了零排放公車的普及。總而言之,在技術進步、監管支援和對高效城市出行解決方案日益成長的需求的共同驅動下,市場正在不斷發展。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 1029億美元 |

| 預計金額 | 2107億美元 |

| 複合年成長率 | 7% |

電池驅動的電動公車在重點地區正迅速普及,預計到2030年,歐洲新售公車中近三分之二將是電動公車,而中國也正接近實現城市公車隊的全面電氣化。市場成長的驅動力來自人口稠密的大都會圈對頻繁、高效的公共運輸服務日益成長的需求。公共交通系統基礎設施的不斷完善持續推動著向清潔出行方式的轉型,加速了主要交通走廊柴油公車的淘汰。

電池技術的進步,包括容量超過700千瓦時的電池,以及用於能量最佳化的增強型軟體,正在提高車輛的效率和可靠性。氫燃料電池公車比純電動公車更柔軟性,並因其在長途線路上的應用而備受關注。國際能源機構的報告強調,電動車的材料成本正在下降,價格競爭力也在增強,尤其是新興市場。這些進步正在縮短零排放公車的投資回收期,尤其是在高利用率線路上,這得益於單車經濟效益的提高和持續的財政獎勵。

預計到2025年,公共汽車市場規模將達到576億美元,到2035年將達到1,286億美元。市場成長的驅動力在於對更高發車頻率服務的需求不斷成長,以及城市交通走廊的建設需要更大容量的車輛。公共運輸業者正在將零排放要求納入籌資策略,這加快了車輛的更新換代週期,並推動了對充電站等配套基礎設施的投資。

2025年,內燃機(ICE)公車市佔率為79%。預計2026年至2035年間,該細分市場將以6%的複合年成長率成長。雖然對內燃機公車的絕對需求依然強勁,但隨著零排放替代方案的發展,其整體市場佔有率正在逐漸下降。

預計到2025年,亞太地區巴士市場規模將達510億美元,2035年將擴大至993億美元。該地區正崛起為主要的成長中心,受益於強大的製造能力、中國的大規模普及以及印度和整個東南亞地區不斷成長的需求。

目錄

第1章:調查方法

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率分析

- 成本結構

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 大眾運輸車輛的電氣化

- 政府對公共交通基礎設施的投資

- 都市化進程和旅客出行需求的成長。

- 動力傳動系統技術進步

- 產業潛在風險與挑戰

- 電動和氫燃料電池公車的初始成本較高

- 充電和氫氣加註基礎設施的差距

- 供應鏈限制因素(電池和半導體)

- 對政府補貼的依賴程度

- 市場機遇

- 擴大電動公車採購計劃

- 氫燃料電池公車的引進

- 私家車營運商和出行服務的成長

- 智慧公車和連網公車

- 促進因素

- 成長潛力分析

- 監理情勢

- 北美洲

- 美國環保署(EPA)

- 美國國家公路交通安全管理局(NHTSA)

- 職業安全與健康管理局(OSHA)

- 美國運輸部(DOT)

- 加拿大車輛安全標準(CMVSS)

- 歐洲

- 歐盟通用安全法規

- 歐VI排放氣體標準

- 已完成車輛類型認證(WVTA)

- 符合CE標誌

- 行車記錄器及駕駛時間規定

- 亞太地區

- 中國強制產品認證(CCC)

- 印度第六階段排放氣體法規

- 中央機動車輛法規(CMVR)

- 日本道路運輸車輛法及安全標準

- 澳洲設計規則(ADR)

- 拉丁美洲

- 巴西國家交通委員會(CONTRAN)

- 巴西環境與可再生自然資源研究所 (IBAMA) 的排放法規

- 墨西哥商用車輛安全標準(NOM)

- 區域進口和型式認可要求

- 中東和非洲

- 海灣標準化組織(GSO)汽車法規

- 沙烏地阿拉伯標準、計量和品質組織(SASO)

- 南非國家法規服務局 (NRCS)

- 遵守《國家道路交通法》(NRTA)

- 北美洲

- 波特五力分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 價格分析(基於初步調查)

- 對過去價格趨勢的分析

- 按業務類型分類的定價策略(溢價/價值/成本加成)

- 貿易數據分析(基於付費研究)

- 進出口量及進口額趨勢

- 主要貿易走廊和關稅的影響

- 成本細分分析

- 專利分析(基於初步研究)

- 人工智慧和生成式人工智慧對市場的影響

- 利用人工智慧改造現有經營模式

- GenAI 各細分市場的應用案例與部署藍圖

- 風險、局限性和監管考量

- 生產能力和生產趨勢(基於初步調查)

- 按地區和主要生產商分類的設備產能

- 運轉率和擴張計劃

- 永續性和環境方面

- 永續計劃

- 減少廢棄物策略

- 生產中的能源效率

- 具有環保意識的舉措

- 關於碳足跡的考量

- 預測假設和情境分析(基於初步研究)

- 基本案例-驅動複合年成長率的關鍵宏觀經濟與產業變量

- 樂觀情境-宏觀經濟與產業的順風

- 悲觀情景-宏觀經濟放緩或產業逆風

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲(MEA)

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係和聯盟

- 新產品發布

- 業務拓展計劃及資金籌措

- 企業級分層基準測試

- 層級分類標準與選擇標準

- 按收入、地區和創新能力分類的層級定位矩陣。

第5章 市場估價與預測:依車輛類型分類,2022-2035年

- 公車線路

- 標準12公尺城市公車

- 鉸接式巴士

- 其他

- 長途汽車

- 城際定期巴士

- 豪華巴士和臥舖巴士

- 其他

- 校車

- A型

- B型

- C型

- D型

- 接駁巴士和機場巴士

- 其他

第6章 市場估算與預測:依座位容量分類,2022-2035年

- 不到40個座位

- 40~70

- 超過70個座位

第7章 市場估計與預測:依服務業分類,2022-2035年

- 城際

- 在城市裡

第8章 市場估算與預測:依促進因素分類,2022-2035年

- 內燃機(ICE)

- BEV

- FCEV

- PHEV

- HEV

第9章 市場估計與預測:依最終用途分類,2022-2035年

- 政府/公共交通

- 私人車隊營運商

- 企業和機構用車

- 旅遊和旅行社

- 教育機構

第10章 市場估價與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 東南亞

- ANZ

- 拉丁美洲

- 巴西

- 阿根廷

- 墨西哥

- 中東和非洲(MEA)

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

第11章:公司簡介

- 世界公司

- BYD

- Daimler

- Hyundai

- Iveco

- MAN

- Scania

- Volvo Buses

- Yutong

- 當地公司

- Blue Bird

- CAF

- Golden Dragon

- Higer

- IC Bus

- King Long

- Navistar

- Solaris

- VDL

- Zhongtong

- 新興企業

- Ashok Leyland

- Tata Motors

The Global Bus Market was valued at USD 102.9 billion in 2025 and is estimated to grow at a CAGR of 7% to reach USD 210.7 billion by 2035.

The market is shaped by expanding urban populations and sustained investment in public transportation infrastructure. Cities are prioritizing high-capacity mobility solutions to improve accessibility and reduce congestion, which is accelerating demand for buses across transit networks. Electrification is becoming a central theme, with battery-electric buses rapidly gaining traction in multiple regions, supported by policy mandates and cost efficiencies. Improvements in vehicle performance, including higher battery capacities and advanced energy management systems, are strengthening operational viability. At the same time, hydrogen-powered alternatives are emerging for longer routes. Declining battery costs and supportive government incentives are narrowing the cost gap between conventional and zero-emission buses, improving return on investment. Increasing affordability in developing economies is further boosting adoption. Overall, the market is evolving through a combination of technological progress, regulatory push, and rising demand for efficient urban mobility solutions.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $102.9 Billion |

| Forecast Value | $210.7 Billion |

| CAGR | 7% |

Battery-electric buses are expanding their footprint across key regions, with Europe expected to achieve nearly two-thirds of new bus sales from electric models by 2030, while China is approaching full electrification of new urban bus fleets. Market growth is driven by rising demand for frequent, efficient transit services in densely populated metropolitan areas. Infrastructure development in public transport systems continues to reinforce the shift toward cleaner mobility, thereby accelerating the replacement of diesel-powered buses in major transit corridors.

Advancements in battery technology, including capacities exceeding 700 kWh, along with enhanced software for energy optimization, are improving vehicle efficiency and reliability. Hydrogen-powered buses are gaining attention for long-distance operations, offering flexibility beyond the limitations of battery-electric buses. Reports from international energy authorities highlight declining material costs and increasing affordability of electric vehicles, particularly in emerging markets. These improvements are shortening payback periods for zero-emission buses, especially on high-utilization routes, driven by better unit economics and ongoing financial incentives.

The transit buses segment accounts for USD 57.6 billion in 2025 and is anticipated to reach USD 128.6 billion by 2035. Growth in this segment is supported by increasing demand for high-frequency services and upgrades to urban transit corridors that require higher-capacity vehicles. Public transit agencies are incorporating zero-emission requirements into procurement strategies, which is accelerating fleet replacement cycles and encouraging investment in supporting infrastructure such as charging depots.

The internal combustion engine buses segment held a 79% share in 2025. The segment is projected to grow at a CAGR of 6% between 2026 and 2035. Although demand for ICE buses remains strong in absolute terms, their overall market share is gradually declining as zero-emission alternatives gain momentum.

Asia Pacific Bus Market reached USD 51 billion in 2025 and is expected to rise to USD 99.3 billion by 2035. The region benefits from strong manufacturing capabilities, large-scale deployments in China, and increasing demand across India and Southeast Asia, positioning it as a key growth hub.

Key companies operating in the Global Bus Market include Blue Bird, BYD, CAF, Daimler, Golden Dragon, Hyundai, Iveco, MAN, Scania, Volvo, and Yutong. Companies in the bus market are strengthening their positions through a combination of product innovation, strategic partnerships, and geographic expansion. Manufacturers are investing heavily in electric and hydrogen-powered bus technologies to align with global emission regulations and evolving customer preferences. Collaboration with governments and transit agencies is enabling large-scale fleet deployments and infrastructure development. Firms are also focusing on enhancing battery performance, vehicle range, and energy efficiency to improve competitiveness. Expanding production capacity, particularly in high-growth regions such as the Asia Pacific, is another key strategy. Additionally, companies are leveraging digital solutions, including fleet management software and predictive maintenance systems, to deliver value-added services and improve operational efficiency for transit operators.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality Commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.2.1.1 Source consistency protocol

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research Trail & Confidence Scoring

- 1.3.1 Research Trail Components

- 1.3.2 Scoring Components

- 1.4 Data Collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.5.2 Sources, by region

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.7.1 Quantified market impact analysis

- 1.7.1.1 Mathematical impact of growth parameters on forecast

- 1.7.1 Quantified market impact analysis

- 1.8 Research transparency addendum

- 1.8.1 Source attribution framework

- 1.8.2 Quality assurance metrics

- 1.8.3 Our commitment to trust

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Vehicle

- 2.2.3 Seating Capacity

- 2.2.4 Service

- 2.2.5 Propulsion

- 2.2.6 End Use

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Electrification of public transport fleets

- 3.2.1.2 Government investments in mass transit infrastructure

- 3.2.1.3 Rising urbanization and passenger mobility demand

- 3.2.1.4 Technological advancements in powertrains

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High upfront cost of electric and hydrogen buses

- 3.2.2.2 Charging and hydrogen refueling infrastructure gaps

- 3.2.2.3 Supply chain constraints (batteries & semiconductors)

- 3.2.2.4 Dependence on government subsidies

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of electric bus procurement programs

- 3.2.3.2 Hydrogen fuel cell bus adoption

- 3.2.3.3 Growth of private fleet operators & mobility services

- 3.2.3.4 Smart and connected buses

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 Environmental Protection Agency (EPA)

- 3.4.1.2 National Highway Traffic Safety Administration (NHTSA)

- 3.4.1.3 Occupational Safety and Health Administration (OSHA)

- 3.4.1.4 U.S. Department of Transportation (DOT)

- 3.4.1.5 Canadian Motor Vehicle Safety Standards (CMVSS)

- 3.4.2 Europe

- 3.4.2.1 EU General Safety Regulation

- 3.4.2.2 Euro VI Emission Standards

- 3.4.2.3 Whole Vehicle Type Approval (WVTA)

- 3.4.2.4 CE Marking Compliance

- 3.4.2.5 Tachograph and Driver Hours Regulations

- 3.4.3 Asia Pacific

- 3.4.3.1 China Compulsory Certification (CCC)

- 3.4.3.2 Bharat Stage VI Emission Norms

- 3.4.3.3 Central Motor Vehicle Rules (CMVR)

- 3.4.3.4 Japanese Road Vehicle Act & Safety Standards

- 3.4.3.5 Australian Design Rules (ADR)

- 3.4.4 Latin America

- 3.4.4.1 Brazilian National Traffic Council (CONTRAN)

- 3.4.4.2 Brazilian Institute of Environment and Renewable Natural Resources (IBAMA) Emission Rules

- 3.4.4.3 Mexican NOM Commercial Vehicle Safety Standards

- 3.4.4.4 Regional Import & Homologation Requirements

- 3.4.5 Middle East & Africa

- 3.4.5.1 Gulf Standardization Organization (GSO) Vehicle Regulations

- 3.4.5.2 Saudi Standards, Metrology and Quality Organization (SASO)

- 3.4.5.3 South African National Regulator for Compulsory Specifications (NRCS)

- 3.4.5.4 National Road Traffic Act (NRTA) Compliance

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price analysis (Driven by Primary Research)

- 3.8.1 Historical Price Trend Analysis

- 3.8.2 Pricing Strategy by Player Type (Premium / Value / Cost-plus)

- 3.9 Trade data analysis (Driven by Paid Research)

- 3.9.1 Import/export volume & value trends

- 3.9.2 Key trade corridors & tariff impact

- 3.10 Cost breakdown analysis

- 3.11 Patent analysis (Driven by Primary Research)

- 3.12 Impact of AI & generative AI on the market

- 3.12.1 AI-driven disruption of existing business models

- 3.12.2 GenAI use cases & adoption roadmap by segment

- 3.12.3 Risks, limitations & regulatory considerations

- 3.13 Capacity & production landscape (Driven by Primary Research)

- 3.13.1 Installed capacity by region & key producer

- 3.13.2 Capacity utilization rates & expansion pipelines

- 3.14 Sustainability and environmental aspects

- 3.14.1 Sustainable practices

- 3.14.2 Waste reduction strategies

- 3.14.3 Energy efficiency in production

- 3.14.4 Eco-friendly Initiatives

- 3.14.5 Carbon footprint considerations

- 3.15 Forecast assumptions & scenario analysis (Driven by Primary Research)

- 3.15.1 Base Case - key macro & industry variables driving CAGR

- 3.15.2 Optimistic Scenarios - Favorable macro and industry tailwinds

- 3.15.3 Pessimistic Scenario - Macroeconomic slowdown or industry headwinds

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New Product Launches

- 4.5.4 Expansion Plans and funding

- 4.6 Company tier benchmarking

- 4.6.1 Tier classification criteria & qualifying thresholds

- 4.6.2 Tier positioning matrix by revenue, geography & innovation

Chapter 5 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Mn, Units)

- 5.1 Key trends

- 5.2 Transit buses

- 5.2.1 Standard 12 m city buses

- 5.2.2 Articulated buses

- 5.2.3 Others

- 5.3 Coach buses

- 5.3.1 Intercity scheduled coaches

- 5.3.2 Luxury and sleeper coaches

- 5.3.3 Others

- 5.4 School buses

- 5.4.1 Type A

- 5.4.2 Type B

- 5.4.3 Type C

- 5.4.4 Type D

- 5.5 Shuttle and airport buses

- 5.6 Others

Chapter 6 Market Estimates & Forecast, By Seating Capacity, 2022 - 2035 ($Mn, Units)

- 6.1 Key trends

- 6.2 Below 40

- 6.3 40-70

- 6.4 Above 70

Chapter 7 Market Estimates & Forecast, By Service, 2022 - 2035 ($Mn, Units)

- 7.1 Key trends

- 7.2 Intercity

- 7.3 Intracity

Chapter 8 Market Estimates & Forecast, By Propulsion, 2022 - 2035 ($Mn, Units)

- 8.1 Key trends

- 8.2 ICE

- 8.3 BEV

- 8.4 FCEV

- 8.5 PHEV

- 8.6 HEV

Chapter 9 Market Estimates & Forecast, By End Use, 2022 - 2035 ($Mn, Units)

- 9.1 Key trends

- 9.2 Government / Public transport authorities

- 9.3 Private fleet operators

- 9.4 Corporate / Institutional fleets

- 9.5 Tourism & travel operators

- 9.6 Educational institutions

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Southeast Asia

- 10.4.6 ANZ

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Argentina

- 10.5.3 Mexico

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 Saudi Arabia

- 10.6.3 South Africa

Chapter 11 Company Profiles

- 11.1 Global Players

- 11.1.1 BYD

- 11.1.2 Daimler

- 11.1.3 Hyundai

- 11.1.4 Iveco

- 11.1.5 MAN

- 11.1.6 Scania

- 11.1.7 Volvo Buses

- 11.1.8 Yutong

- 11.2 Regional Players

- 11.2.1 Blue Bird

- 11.2.2 CAF

- 11.2.3 Golden Dragon

- 11.2.4 Higer

- 11.2.5 IC Bus

- 11.2.6 King Long

- 11.2.7 Navistar

- 11.2.8 Solaris

- 11.2.9 VDL

- 11.2.10 Zhongtong

- 11.3 Emerging Players

- 11.3.1 Ashok Leyland

- 11.3.2 Tata Motors

2026年全球客車市場報告

2026年全球客車市場報告 全球臥舖巴士市場:市場規模、佔有率、趨勢和成長分析(2026-2034)

全球臥舖巴士市場:市場規模、佔有率、趨勢和成長分析(2026-2034) 無軌電車市場分析及至2035年的預測:類型、產品類型、技術、組件、應用、最終用戶、功能、安裝配置、運輸方式2026年全球巴士市場報告2026年全球長途客車市場報告

無軌電車市場分析及至2035年的預測:類型、產品類型、技術、組件、應用、最終用戶、功能、安裝配置、運輸方式2026年全球巴士市場報告2026年全球長途客車市場報告 豪華巴士市場規模、佔有率和成長分析:按燃料類型、巴士類型、應用和地區分類-2026-2033年產業預測

豪華巴士市場規模、佔有率和成長分析:按燃料類型、巴士類型、應用和地區分類-2026-2033年產業預測 臥舖巴士市場:市場機會、成長要素、產業趨勢分析及2026-2035年預測

臥舖巴士市場:市場機會、成長要素、產業趨勢分析及2026-2035年預測 歐洲巴士市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

歐洲巴士市場:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 全球鉸接式巴士市場

全球鉸接式巴士市場 城際電動巴士市場預測至2034年-全球動力系統、電池容量、巴士長度、座位數、續航里程、應用及區域分析

城際電動巴士市場預測至2034年-全球動力系統、電池容量、巴士長度、座位數、續航里程、應用及區域分析