|

市場調查報告書

商品編碼

2065590

整合通訊(UC)硬體:市場佔有率分析、產業趨勢和統計數據以及成長預測(2026-2031 年)Unified Communications (UC) Hardware - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

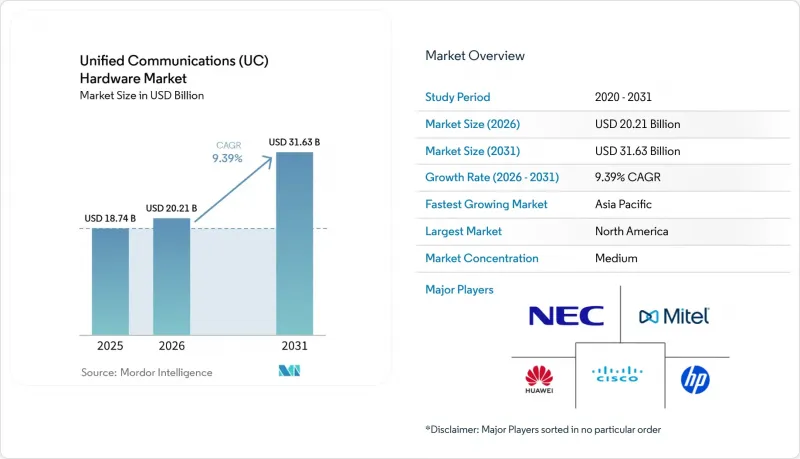

據 Mordor Intelligence 稱,2025 年整合通訊(UC) 硬體市場價值為 187.4 億美元,預計到 2031 年將達到 316.3 億美元,而 2026 年為 202.1 億美元,預測期(2026-2031 年)的複合年成長率為 9.39%。

本報告按硬體類型(IP電話硬體、視訊會議系統等)、銷售模式(離線、線上)、終端用戶產業(IT和電信、銀行、金融服務和保險、醫療保健和生命科學等)、組織規模(大型企業、中小企業)和地區進行細分。市場預測以價值(美元)表示。

全球整合通訊(UC) 硬體市場趨勢與洞察

混合工作環境的廣泛採用

隨著混合辦公模式的永久普及,企業被迫以企業認證的終端設備取代臨時使用的個人設備,這些終端設備提供集中式管理和安全保障。 Gartner 指出,設備品質不佳導致約三分之二的員工在使用數位化設備時遇到困難,設備更新周期縮短至三到四年。思科等廠商正透過提供內建人工智慧運算功能的協作白板來解決這個問題,這些白板無需外部周邊設備,並簡化了遠端配置。按角色和會議室類型對設備組合進行標準化,可以降低支援成本並改善使用者體驗。因此,高效能統一通訊硬體被視為人才保留和營運韌性的關鍵策略要素。

公司範圍內的視訊協作需求激增

視訊應用正從負責人辦公室擴展到個人辦公桌和小型會議空間,這推動了對支援模組化升級的可擴展系統的需求。 Jabra 的「2026 PanaCast Room Kits」提供 1、3 和 5 個攝影機配置,使 IT 團隊能夠根據實際情況進行投資,同時確保未來的擴充性。 Logitech 的「Rally AI Camera Pro」以 2,999 美元的價格引入了雙鏡頭智慧技術,彌補了大型空間中的可視盲區。整合日程安排面板可以有效利用昂貴的會議空間,減少“幽靈會議”,並最佳化空間利用。

傳統統一通訊終端的平均售價正在下降。

像億聯這樣的亞洲廠商現在提供的微軟Teams認證桌上型電話,價格比西方老牌廠商低40%之多,這給通用硬體的利潤率帶來了壓力。這種商品化趨勢使得買家可以從多個供應商購買終端設備,迫使傳統供應商要麼捆綁增值軟體,要麼專注於具有增強型人工智慧功能的高階產品。廠商們正在透過訂閱服務來應對這項挑戰,例如Jabra Engage AI Complete,它將語音分析和轉錄功能整合到按用戶付費的套餐中,從而產生持續收入以彌補硬體利潤率的下降。

細分市場分析

IP電話硬體仍然是收入最高的細分市場,預計到2025年將佔據整合通訊(UC)硬體市場32.25%的佔有率,但隨著語音功能整合到更廣泛的協作套件中,其成長速度正在放緩。視訊會議系統則呈現最快的成長速度,從2026年到2031年,其複合年成長率將達到11.24%。隨著企業尋求為混合團隊提供全面的會議體驗,這些系統將繼續成為新功能研發的重點。

邊緣人工智慧晶片技術的進步使攝影機無需依賴雲端運算即可實現即時說話者追蹤和語音轉文字功能,從而降低延遲並滿足隱私要求。將相機、麥克風、揚聲器和轉碼器整合到單一裝置中的協作條形模組降低了安裝複雜性,並已成為快速部署方案中的首選外形規格。擁有完善的軟體藍圖和經認證的跨平台相容性的供應商持續超越僅提供硬體的競爭對手。

2025年,線下銷售模式仍將主導銷售管道,佔總收入的68.27%。這主要是由於大型企業和關鍵任務環境對複雜的會議室整合和現場支援的需求。然而,線上通路正迅速從小眾選擇轉變為主流購買途徑,年複合成長率達12.08%。這種成長在USB耳機和個人網路攝影機等標準化即插即用產品中尤其明顯,這些產品的部署複雜性極低。

為了掌握這項轉變帶來的機遇,製造商正加大對直接面對消費者的電子商務平台和雲端市場的投資,使客戶能夠快速且有效率地配置和購買認證套裝。中小企業尤其青睞這些平台,因為它們定價透明,採購流程精簡。同時,思科不斷演進的策略夥伴等措施也反映了整個產業的轉型趨勢:隨著交易型銷售日益向數位化通路轉移,傳統經銷商正在重新定位,以提供更高附加價值的服務。

區域分析

北美地區在強勁的企業更新換代週期和美國聯邦通訊委員會(FCC)的「全IP現代化計畫」的推動下,預計到2025年將佔據34.82%的市場佔有率。美國企業繼續優先考慮符合嚴格安全準則的人工智慧設備,而在加拿大,公共部門的強勁需求與企業支出相輔相成。墨西哥則受益於美墨加協定(USMCA)的獎勵,該協定旨在促進跨境供應鏈的整合和組裝業務的近岸外包。

亞太地區預計將成為所有地區中成長最快的地區,2026年至2031年的複合年成長率將達到11.92%。中國政府主導的人工智慧推廣和城市層面強制推行的智慧辦公,正使華為和中興等國內大型企業受益匪淺。隨著政府主導的數位化計畫將光纖網路擴展到市政廳和學校,印度的二線城市正成為新的焦點。日本和韓國正在利用成熟的5G網路部署以行動為中心的協作解決方案,而澳洲則依靠環境適應性強、支援衛星通訊的設備來支撐其分佈在廣闊地區的分散式礦業和能源設施。

歐洲的市場前景獨具特色,主要得益於英國計劃於2027年1月逐步淘汰公共交換電話網路(PSTN)。隨著企業更換依賴銅線的設備,採購需求將出現分階段激增。德國和法國在規模上緊隨其後,但嚴格的《一般資料保護規則》(GDPR)要求正促使需求轉向混合或本地部署架構。南美洲的成長主要集中在巴西和阿根廷,兩國不斷完善的寬頻基礎設施使中小企業能夠直接遷移到雲端原生統一通訊(UC)。在中東,沙烏地阿拉伯的國家人工智慧計畫和世博會推動了基礎設施升級,帶來了不定期但盈利的競標。而非洲市場仍處於起步階段,主要集中在南非、奈及利亞和肯亞。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 混合工作環境的廣泛採用

- 公司範圍內的視訊協作需求激增

- 從公共交換電話網路 (PSTN) 遷移到基於 IP 的電話系統

- 透過設備整合提高成本效益

- 新興市場中硬體最佳化型UCaaS閘道器的興起

- 人工智慧音訊周邊設備的整合正在逐步推進。

- 市場限制因素

- 傳統統一通訊終端的平均售價正在下降。

- 關於SIP和VoIP閘道器的安全性問題

- 網路應用專用積體電路(ASIC)的供應鏈仍不足。

- 限制耳機中使用一次性塑膠的環境法規

- 產業價值/價值鏈分析

- 宏觀經濟因素對市場的影響

- 監理情勢

- 技術展望

- 產業吸引力—五力分析

- 新進入者的威脅

- 供應商的議價能力

- 買方的議價能力

- 替代品的威脅

- 競爭公司之間的競爭

第5章 市場規模與成長預測

- 依硬體類型

- IP電話硬體

- 視訊會議系統

- UC閘道器和基礎設施硬體

- 耳機和音訊設備

- 合作酒吧/房間套件

- 其他硬體類型

- 按分佈模型

- 離線

- 線上

- 按最終用戶行業分類

- 資訊科技/通訊

- BFSI

- 醫療保健和生命科學

- 零售和消費品

- 教育

- 政府/公共部門

- 製造業

- 媒體與娛樂

- 其他工業部門

- 按組織規模

- 大公司

- 小型企業

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 其他亞太國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 肯亞

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Cisco Systems, Inc.

- Avaya LLC

- HP Inc.

- Mitel Networks Corporation

- NEC Corporation

- Unify Software and Solutions GmbH and Co. KG

- 8x8, Inc.

- Alcatel-Lucent Enterprise International

- Huawei Technologies Co., Ltd.

- ZTE Corporation

- Grandstream Networks, Inc.

- Yealink Network Technology Co., Ltd.

- Ribbon Communications Inc.

- Sangoma Technologies Corporation

- AudioCodes Ltd.

- GN Audio A/S(Jabra)

- Logitech International SA

- Crestron Electronics, Inc.

- Lifesize Communications, Inc.

- ClearOne, Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the unified communications (UC) hardware market size was valued at USD 18.74 billion in 2025 and estimated to grow from USD 20.21 billion in 2026 to reach USD 31.63 billion by 2031, at a CAGR of 9.39% during the forecast period (2026-2031).

This report is Segmented by Hardware Type (IP Telephony Hardware, Video Conferencing Systems, and More), Distribution Model (Offline, and Online), End-User Industry (IT and Telecommunication, BFSI, Healthcare and Life Sciences, and More), Organization Size (Large Enterprises, and Small and Medium-Sized Enterprises), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Unified Communications (UC) Hardware Market Trends and Insights

Increasing Adoption of Hybrid Work Environments

Permanent hybrid schedules are compelling organizations to replace ad-hoc consumer devices with enterprise-certified endpoints that can be centrally managed and secured. Gartner has noted that poor device quality contributes to digital friction for roughly two-thirds of employees, prompting refresh cycles to shrink to three-to-four years. Vendors such as Cisco have responded with collaboration boards that embed AI compute, eliminating the need for external peripherals and simplifying remote provisioning. Standardizing device portfolios by role and room type reduces support costs and improves the user experience, positioning high-performance UC hardware as a strategic enabler of talent retention and operational resilience.

Surge in Enterprise-Wide Video Collaboration Demand

Video usage has expanded from executive suites to every desk and huddle room, driving demand for scalable systems that support modular upgrades. Jabra's 2026 PanaCast Room Kits, offered in one-, three-, and five-camera variants, allow IT teams to right-size investments while preserving future expansion paths. Logitech's Rally AI Camera Pro introduces dual-camera intelligence at the USD 2,999 price point, addressing visibility gaps in large spaces. Integration of scheduling panels ensures that expensive meeting spaces are utilized efficiently, reducing "ghost meetings" and optimizing real estate.

Declining Average Selling Prices of Legacy UC Endpoints

Asian vendors such as Yealink now offer Microsoft Teams-certified desk phones at prices up to 40% below Western incumbents, eroding margins on commodity hardware. The commoditization trend enables buyers to source endpoints from multiple suppliers, forcing legacy providers to bundle value-added software or shift focus to premium AI-enhanced categories. Vendors have responded with subscription offerings like Jabra Engage AI Complete, which fuses tone analytics and transcription into a per-user fee, creating recurring revenue to offset lower hardware margins.

Other drivers and restraints analyzed in the detailed report include:

- Migration from PSTN to IP-Based Telephony Systems

- Cost Efficiencies Achieved Through Equipment Consolidation

- Security Concerns Around SIP and VoIP Gateways

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

IP telephony hardware still generated the highest category revenue, holding a 32.25% Unified Communications Hardware market share in 2025, yet its growth rate is moderating as voice becomes an embedded feature within broader collaboration suites. Video conferencing systems recorded the fastest growth, advancing at an 11.24% CAGR between 2026 and 2031. They remain the focal point of new feature investment as enterprises seek inclusive meeting experiences across hybrid teams.

Advances in edge-AI silicon now allow cameras to perform real-time speaker tracking and language transcription without relying on cloud compute, reducing latency and meeting privacy mandates. Collaboration bars that integrate a camera, microphone, speaker, and codec into a single device lower installation complexity and have become a preferred form factor for rapid rollout programs. Vendors with strong software roadmaps and certified cross-platform compatibility continue to displace pure-play hardware competitors.

Offline distribution model continued to dominate the distribution landscape in 2025, accounting for 68.27% of total revenue, largely due to the need for complex room integrations and on-site support in large enterprises and mission-critical environments. Despite this, online channels are rapidly transitioning from a niche option to a mainstream purchasing route, growing at a CAGR of 12.08%. Their adoption is particularly strong for standardized, plug-and-play products such as USB headsets and personal webcams, where deployment complexity is minimal.

To capitalize on this shift, manufacturers are expanding investments in direct e-commerce platforms and cloud-based marketplaces that allow customers to configure and purchase certified bundles quickly and efficiently. Small and medium-sized enterprises (SMEs) are particularly inclined toward these platforms due to transparent pricing and streamlined procurement processes. At the same time, initiatives like Cisco's evolving partner strategy reflect a broader industry transition, where traditional resellers are being repositioned toward higher-value services as transactional sales increasingly migrate to digital channels.

Geography Analysis

North America captured 34.82% revenue share in 2025, buoyed by robust enterprise refresh cycles and the FCC's all-IP modernization agenda. United States enterprises continue to prioritize AI-infused devices that meet stringent security guidelines, while Canada's strong public-sector demand complements corporate spending. Mexico benefits from cross-border supply-chain integration and USMCA incentives that encourage nearshoring of assembly operations.

Asia-Pacific is projected to record the fastest regional growth at an 11.92% CAGR between 2026-2031. China's sovereign AI push and city-level smart-office mandates favor domestic champions such as Huawei and ZTE. India's tier-2 cities are emerging hotspots as government-led digitization programs extend fiber connectivity to municipal buildings and schools. Japan and South Korea leverage mature 5G networks to roll out mobile-centric collaboration solutions, while Australia relies on ruggedized, satellite-ready gear to support mining and energy installations spread across vast distances.

Europe's outlook is uniquely shaped by the United Kingdom's January 2027 PSTN switch-off, which is generating staggered procurement spikes as enterprises replace copper-dependent devices. Germany and France are next in scale, although strict GDPR requirements tilt demand toward hybrid or on-premises architectures. South American growth is clustered in Brazil and Argentina, where improved broadband is allowing SMEs to leapfrog directly to cloud-native UC. In the Middle East, Saudi Arabia's national AI plan and Expo-driven infrastructure upgrades create lumpy but lucrative tenders, while Africa remains an early-stage opportunity concentrated in South Africa, Nigeria, and Kenya.

- Cisco Systems, Inc.

- Avaya LLC

- HP Inc.

- Mitel Networks Corporation

- NEC Corporation

- Unify Software and Solutions GmbH and Co. KG

- 8x8, Inc.

- Alcatel-Lucent Enterprise International

- Huawei Technologies Co., Ltd.

- ZTE Corporation

- Grandstream Networks, Inc.

- Yealink Network Technology Co., Ltd.

- Ribbon Communications Inc.

- Sangoma Technologies Corporation

- AudioCodes Ltd.

- GN Audio A/S (Jabra)

- Logitech International S.A.

- Crestron Electronics, Inc.

- Lifesize Communications, Inc.

- ClearOne, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Adoption of Hybrid Work Environments

- 4.2.2 Surge in Enterprise-Wide Video Collaboration Demand

- 4.2.3 Migration From PSTN to IP-Based Telephony Systems

- 4.2.4 Cost Efficiencies Achieved Through Equipment Consolidation

- 4.2.5 Rise of Hardware-Optimised UCaaS Gateways in Emerging Markets

- 4.2.6 Growing Integration of AI-Enabled Audio Peripherals

- 4.3 Market Restraints

- 4.3.1 Declining Average Selling Prices of Legacy UC Endpoints

- 4.3.2 Security Concerns Around SIP and VoIP Gateways

- 4.3.3 Persistent Supply-Chain Chips Shortage in Networking ASICs

- 4.3.4 Environmental Regulations Limiting Single-Use Plastics in Headsets

- 4.4 Industry Value / Supply-Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Industry Attractiveness - Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Hardware Type

- 5.1.1 IP Telephony Hardware

- 5.1.2 Video Conferencing Systems

- 5.1.3 UC Gateways and Infrastructure Hardware

- 5.1.4 Headsets and Audio Devices

- 5.1.5 Collaboration Bars/Room Kits

- 5.1.6 Other Hardware Types

- 5.2 By Distribution Model

- 5.2.1 Offline

- 5.2.2 Online

- 5.3 By End-user Industry

- 5.3.1 IT and Telecommunication

- 5.3.2 BFSI

- 5.3.3 Healthcare and Lifesciences

- 5.3.4 Retail and Consumer Goods

- 5.3.5 Education

- 5.3.6 Government and Public Sector

- 5.3.7 Manufacturing

- 5.3.8 Media and Entertainment

- 5.3.9 Other Industry Verticals

- 5.4 By Organization Size

- 5.4.1 Large Enterprises

- 5.4.2 Small and Medium-Sized Enterprises

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Kenya

- 5.5.6.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Cisco Systems, Inc.

- 6.4.2 Avaya LLC

- 6.4.3 HP Inc.

- 6.4.4 Mitel Networks Corporation

- 6.4.5 NEC Corporation

- 6.4.6 Unify Software and Solutions GmbH and Co. KG

- 6.4.7 8x8, Inc.

- 6.4.8 Alcatel-Lucent Enterprise International

- 6.4.9 Huawei Technologies Co., Ltd.

- 6.4.10 ZTE Corporation

- 6.4.11 Grandstream Networks, Inc.

- 6.4.12 Yealink Network Technology Co., Ltd.

- 6.4.13 Ribbon Communications Inc.

- 6.4.14 Sangoma Technologies Corporation

- 6.4.15 AudioCodes Ltd.

- 6.4.16 GN Audio A/S (Jabra)

- 6.4.17 Logitech International S.A.

- 6.4.18 Crestron Electronics, Inc.

- 6.4.19 Lifesize Communications, Inc.

- 6.4.20 ClearOne, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

整合通訊市場:按組件、解決方案、部署類型、組織規模、應用和最終用戶產業分類-2026-2032年全球市場預測

整合通訊市場:按組件、解決方案、部署類型、組織規模、應用和最終用戶產業分類-2026-2032年全球市場預測 工業製造領域工人技術:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)

工業製造領域工人技術:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031) 整合通訊市場機會、成長要素、產業趨勢分析及2026-2035年預測

整合通訊市場機會、成長要素、產業趨勢分析及2026-2035年預測 整合通訊市場-全球產業規模、佔有率、趨勢、機會、預測:按產品、解決方案、組織規模、應用、地區和競爭對手分類,2021-2031年醫療產業的整合通訊即服務:市場佔有率分析、產業趨勢和統計數據以及成長預測(2026-2031 年)

整合通訊市場-全球產業規模、佔有率、趨勢、機會、預測:按產品、解決方案、組織規模、應用、地區和競爭對手分類,2021-2031年醫療產業的整合通訊即服務:市場佔有率分析、產業趨勢和統計數據以及成長預測(2026-2031 年) 整合通訊(UC) 和商務耳機市場預測至 2034 年—按產品類型、類別、價格、分銷管道、應用、最終用戶和地區分類的全球分析

整合通訊(UC) 和商務耳機市場預測至 2034 年—按產品類型、類別、價格、分銷管道、應用、最終用戶和地區分類的全球分析 整合通訊即服務 (UCaaS) 市場報告:按解決方案類型、組織規模、部署類型、產業和地區分類 (2026–2034)

整合通訊即服務 (UCaaS) 市場報告:按解決方案類型、組織規模、部署類型、產業和地區分類 (2026–2034) 2026年全球通訊與協作市場報告整合通訊和商務耳機市場規模:按產品、類型、價格、分銷管道、應用、最終用途和地區分類(2026-2034 年)整合通訊市場報告:按組件、產品、組織規模、最終用戶和地區分類(2026-2034 年)

2026年全球通訊與協作市場報告整合通訊和商務耳機市場規模:按產品、類型、價格、分銷管道、應用、最終用途和地區分類(2026-2034 年)整合通訊市場報告:按組件、產品、組織規模、最終用戶和地區分類(2026-2034 年)