|

市場調查報告書

商品編碼

2061527

醫療產業的整合通訊即服務:市場佔有率分析、產業趨勢和統計數據以及成長預測(2026-2031 年)Unified Communications-as-a-Service In Healthcare - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

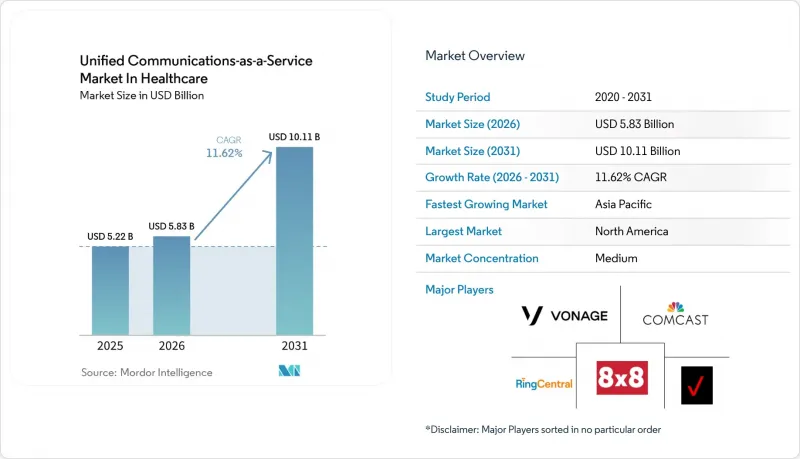

預計到 2026 年,醫療產業整合通訊即服務 (UCaaS) 的市場規模將達到 58.3 億美元。

這比 2025 年的 52.2 億美元有所成長,預計到 2031 年將達到 101.1 億美元,2026 年至 2031 年的複合年成長率為 11.62%。

本報告按部署模式(公共雲端、私有雲端、混合雲端)、組件(電話/語音、統一通訊等)、應用(臨床通訊與協作等)、組織規模(大型企業等)、最終用戶(醫院等)和地區進行細分。市場預測以價值(美元)表示。

醫療產業整合通訊即服務 (UCaaS) 市場的趨勢與發展。

新冠疫情後遠端醫療的擴展

遠端保健的使用量持續成長,迫使醫療服務提供者將語音、視訊和遠端監控流量整合到一個統一的平台上。虛擬醫療的平均單次診療成本已下降高達 17%,據報道,由於工作流程集中在一個安全可靠的環境中,醫療專業人員的工作滿意度也更高。醫療服務提供者現在正與僅在線進行諮詢的「虛擬醫生」簽訂契約,這要求他們能夠保持符合 HIPAA 標準的持續連接,以便進行交接和升級。隨著預測分析和人工智慧驅動的分流技術的整合,遠距醫療正從一次性服務發展成為長期照護模式。同時,電子健康記錄 (EHR) 中對上下文通訊的需求日益成長,這為能夠保證互通性的統一通訊即服務 (UCaaS) 供應商創造了新的商機。

UCaaS 成本降低營運支出模型

從資本密集型PBX硬體遷移到基於訂閱的統一通訊即服務(UCaaS)可以釋放資金,用於以患者為中心的投資。一個擁有40個站點的區域醫療保健網路透過將2000名員工遷移到RingCentral,每年節省了35萬美元的成本。這反映了多站點系統普遍存在的趨勢,即降低支援相關費用。這種營運支出(OPEX)模式無需大規模續訂,並允許成本根據患者數量的波動進行調整。在基於價值的薪酬體系的壓力下,財務長往往更傾向於可預測的月度費用,而不是不規則的資本支出。規模小規模的醫療保健機構受益最大,因為雲端提供者負責維護、安全修補程式和災害復原,從而降低了部署企業級通訊系統的人力資源門檻。

資料安全和 HIPAA 合規問題是推廣應用的障礙。

對靜態資料和傳輸中資料進行加密、實施細粒度存取控制以及簽訂業務夥伴協議都會產生成本和延誤。小規模診所報告稱,由於安全團隊檢驗雲端架構並繪製資料流程圖,專案延誤時間長達 6 至 12 個月。資料外洩的罰款可能超過每次 150 萬美元,這導致風險意識增強,並促使人們更傾向於選擇擁有長期合規記錄的成熟供應商。在多租戶雲端環境中,人們對病患記錄共存問題的擔憂日益加劇,儘管成本更高,但對混合雲和專用實例的興趣仍在成長。

細分市場分析

公共雲端滿足了對按需擴展和自動化軟體更新的需求,佔據市場主導地位,預計到2025年,其在醫療保健行業的整合通訊即服務 (UCaaS) 市場佔有率將達到45.10% 。大規模綜合醫療保健網路利用全球資料中心為地理位置分散的醫療團隊提供支持,而新創公司則採用付費使用制以避免前期投資。由於隱私和資料主權法律要求醫療服務提供者將臨床資料庫保存在本地儲存庫中,混合雲端預計將成為所有部署類型中成長最快的,複合年成長率 (CAGR) 將達到16.70%。預計到2031年,醫療產業整合通訊即服務 (UCaaS) 的混合雲端市場規模將達到66.2億美元。醫療服務提供者通常在本地託管通話詳細記錄和音訊數據,同時將即時工作負載卸載到雲端。這種配置可以減少現場產生緊急代碼時的延遲,並實現與醫院防火牆內的電梯、警報系統和醫療設備閘道的整合。

對私有雲端的需求仍然是一個小眾市場,主要集中在進行高風險臨床試驗或受國家安全約束的機構,例如大學醫院。由於需要專用硬體和營運商網路,這些部署成本高昂。然而,捆綁安全設備和全天候監控的託管服務正在降低准入門檻。一些服務提供者正在採取分階段的方法,首先將人力資源和計費等非臨床部門遷移到公共雲端,然後在管治模式成熟後再遷移面向患者的工作負載。

預計到2025年,語音通訊/語音領域將維持26.60%的市場佔有率,凸顯了語音在緊急呼叫、諮詢和總機操作中的關鍵作用。然而,協作工具才是成長的主要驅動力,其複合年成長率將達到17.90%。在多學科團隊會議中,臨床醫生現在更傾向於使用始終線上聊天室、文件共用空間以及整合到電子病歷(EHR)駕駛座中的視訊會議入口網站。在醫療產業的整合通訊即服務(UCaaS)市場中,預計到2031年,協作工具的市場佔有率將超過31.80%。供應商正透過整合人工智慧驅動的筆記功能、自動語言翻譯以及直接連結到患者記錄的虛擬白板等功能來脫穎而出。

統一通訊將語音郵件、電子郵件和簡訊整合到一個統一的佇列中,消除了訊息碎片化。會議解決方案整合了高清攝影機推車和聽診器周邊設備,實現了虛擬查房。客服中心整合對於全通路病人參與仍然至關重要,它透過統一的隊列路由檢測結果、預約提醒和藥房諮詢。隨著醫療服務提供者在基於價值的補償模式下優先考慮提升消費者體驗以留住患者,這一領域正蓬勃發展。

區域分析

在既定的 HIPAA 法規、廣泛的電子病歷 (EHR) 應用以及積極的 AI先導計畫的推動下,北美預計將在 2025 年佔據 35.90% 的收入佔有率。微軟的 DAX Copilot運作,產生了 950 萬份病患記錄,並展示了大規模臨床級語音辨識。醫療機構正在利用成熟的寬頻和 5G 網路實現病房間的遠距醫療和機構間資源共用。聯邦政府靈活的遠距遠端醫療報銷政策已延長至 2026 年,這進一步鞏固了對雲端運算的依賴。

亞太地區以13.40%的複合年成長率引領成長動能。泰國、韓國和中國的公共部門智慧醫院試點計畫是5G賦能的救護車遙測和基於人工智慧的分診技術的典範,這些技術將影像診斷時間從15分鐘縮短至25秒。不同地區的隱私法律差異推動了對統一通訊即服務(UCaaS)架構中可自訂資料儲存位置以及自帶設備(BYOC)的需求。本地系統整合商提供的打包合規諮詢服務降低了中型診所採用這些技術的門檻。

在歐洲,受電子健康舉措和歐洲健康數據空間內跨境數據共用目標的推動,市場正保持著穩定的中等個位數成長。法國的遠距醫療立法正在擴大醫療專業人員遠距辦公的範圍,從而增加了對安全視訊通訊管道的需求。 GDPR 的要求促使人們對混合部署模式產生興趣,在這種模式下,通訊資料保留在本地資料中心。供應商的產品藍圖擴大提及「符合 Schrems II 標準」的架構,旨在贏得公立醫院的青睞。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 新冠疫情後遠端醫療的擴展

- UCaaS 成本降低營運支出模型

- 與電子病歷和臨床工作流程的整合

- 基於5G邊緣運算的AR手術整合

- 符合 HIPAA 標準的合規即服務包

- 人工智慧驅動的臨床記錄和工作流程自動化

- 市場限制因素

- 資料安全和 HIPAA 相關問題

- 傳統PBX和數位化進程的延遲

- 以價值為導向的醫療保健模式給預算帶來了壓力。

- 由於垂直整合的統一通訊技術棧,導致廠商鎖定。

- 重要法規結構的評估

- 產業價值鏈分析

- 技術展望

- 波特五力模型

- 主要用例和案例研究

- 宏觀經濟因素對市場的影響

- 投資分析

第5章 市場區隔

- 按部署模式

- 公共雲端

- 私有雲端

- 混合雲端

- 按組件

- 語音通訊/音訊

- 統一通訊

- 會議

- 協作工具

- 客服中心整合

- 透過使用

- 臨床溝通與協作

- 遠端醫療和虛擬護理

- 行政和計費

- 協調緊急應變

- 病人參與和投入

- 按組織規模

- 大公司

- 小型企業

- 最終用戶

- 醫院

- 診所和醫生診所

- 門診手術中心

- 長期照護機構

- 診斷和影像中心

- 居家醫療護理

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲和紐西蘭

- 其他亞太國家

- 中東和非洲

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 奈及利亞

- 埃及

- 其他非洲國家

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- RingCentral, Inc.

- 8x8, Inc.

- Verizon Communications Inc.

- Comcast Corporation

- Vonage Holdings Corp.(Telefonaktiebolaget LM Ericsson)

- Intrado Corporation

- Star2Star Communications, LLC

- International Business Machines Corporation

- ALE International SAS(Alcatel-Lucent Enterprise)

- Cisco Systems, Inc.

- Microsoft Corporation

- Google LLC(Google Cloud)

- Zoom Video Communications, Inc.

- Avaya LLC

- Mitel Networks Corporation

- Fuze, Inc.

- Dialpad, Inc.

- NEC Corporation

- Twilio Inc.

- Genesys Telecommunications Laboratories, Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, unified communications-as-a-Service in Healthcare market size in 2026 is estimated at USD 5.83 billion, growing from 2025 value of USD 5.22 billion with 2031 projections showing USD 10.11 billion, growing at 11.62% CAGR over 2026-2031.

This report is Segmented by Deployment Model (Public Cloud, Private, Cloud, and Hybrid Cloud), Component (Telephony / Voice, Unified Messaging, and More), Application (Clinical Communications and Collaboration, and More), Organization Size (Large Enterprises, and More), End-User (Hospitals, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Insights and Trends of Unified Communications-as-a-Service Market In Healthcare

Tele-health Expansion Post-COVID-19

Elevated telehealth volumes have stabilized, pushing providers to consolidate voice, video, and remote-monitoring traffic onto single platforms. Average cost per encounter in virtual care is falling by up to 17%, and caregivers report higher job satisfaction when workflows remain inside one secure environment. Providers now contract "virtualist" physicians who practice exclusively online, requiring continuous, HIPAA-grade connectivity for hand-offs and escalations. Integration of predictive analytics and AI-driven triage elevates tele-consultations from episodic events to longitudinal care pathways. Demand for contextual messaging within electronic health records (EHRs) grows in parallel, underpinning fresh opportunities for UCaaS vendors that can certify interoperability.

Cost-Saving OPEX Model of UCaaS

Switching from capital-intensive PBX hardware to subscription-based UCaaS frees cash for patient-centric investments. A 40-site community health network saved USD 350,000 annually after migrating 2,000 employees to RingCentral, an outcome echoed across multi-facility systems looking to trim support overhead. The operating-expense structure removes large refresh cycles, aligning expenses with fluctuating patient volumes. CFOs under pressure from value-based reimbursement find predictable monthly fees preferable to lumpy capital outlays. Smaller practices benefit most because cloud providers assume maintenance, security patching, and disaster recovery, lowering the personnel barrier to enterprise-class communications.

Data Security and HIPAA Concerns Create Adoption Barriers

Encrypting data at rest and in transit, enforcing granular access controls, and signing business-associate agreements add cost and delay. Smaller clinics report six-to-twelve-month project slippage while security teams validate cloud architectures and map data flows. Breach penalties can exceed USD 1.5 million per incident, elevating risk perception and driving preference for incumbents with long compliance track records. Multi-tenant clouds intensify worries about co-mingling patient records, spurring interest in hybrid and dedicated instances despite higher price points.

Other drivers and restraints analyzed in the detailed report include:

- Integration with EHR & Clinical Workflows

- 5G Edge-Enabled AR Surgical Collaboration

- Legacy PBX and Low Digital Readiness Constrain Migration

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Public Cloud dominated 2025 with 45.10% share of the Unified Communications-as-a-Service in Healthcare market, reflecting preference for on-demand scalability and automatic software updates. Large integrated-delivery networks tap global data centers to support geographically dispersed care teams, while start-ups exploit pay-as-you-go pricing to sidestep capital outlays. Hybrid Cloud trajectories are set to compound at 16.70% CAGR, the fastest within the deployment category, as privacy policies and data-sovereignty laws force providers to retain clinical databases in local vaults. The Unified Communications-as-a-Service in Healthcare market size for Hybrid Cloud is projected to reach USD 6.62 billion by 2031. Providers typically host call-detail records and recordings on-premises while offloading real-time workloads to the cloud. The arrangement mitigates latency for on-site emergency codes and integrates with elevators, alarms, and medical-device gateways that remain behind hospital firewalls.

Demand for Private Cloud remains niche, concentrated in academic medical centers conducting high-risk clinical trials or operating under national defense constraints. These deployments attract higher total cost due to dedicated hardware and carrier circuits. Nonetheless, managed-service options that bundle security appliances and 24X7 monitoring are lowering entry barriers. Some providers adopt a phased approach: migrate non-clinical departments such as HR and billing to Public Cloud first, then shift patient-facing workloads once governance models mature.

Telephony/Voice retained 26.60% share in 2025, underlining voice's enduring role for code calls, consults, and switchboard operations. However, Collaboration Tools hold the growth spotlight with an 17.90% CAGR. Across multidisciplinary team huddles, clinicians now prefer persistent chat rooms, file-share spaces, and video huddle portals embedded inside their EHR cockpit. The Unified Communications-as-a-Service in Healthcare market share for Collaboration Tools is forecast to exceed 31.80% by 2031. Vendors differentiate by embedding note-taking AI, automatic language translation, and virtual whiteboards that map directly to patient records.

Unified Messaging converges voicemail, email, and SMS into one queue, easing information scatter. Conferencing solutions integrate high-definition camera carts and stethoscope peripherals for virtual rounding. Contact-Center Integration remains pivotal to omni-channel patient engagement, routing lab results, appointment reminders, and pharmacy queries through a unified queue. Momentum here climbs as providers emphasize consumer-grade experience to retain patients under value-based reimbursement.

Geography Analysis

North America contributed 35.90% of 2025 revenue, driven by entrenched HIPAA mandates, EHR ubiquity, and aggressive AI pilots. Microsoft's DAX Copilot is live in 400+ provider networks, generating 9.5 million encounter notes and validating clinical-grade speech recognition at scale. Providers leverage mature broadband and 5G coverage for in-unit teleconsults and cross-facility resource pooling. Federal flexibilities for telehealth reimbursement, extended through 2026, further entrench cloud reliance.

Asia-Pacific leads in growth momentum at 13.40% CAGR. Public-sector smart-hospital pilots in Thailand, South Korea, and China exemplify 5G-enabled ambulance telemetry and AI-based triage that slash imaging turnaround from 15 minutes to 25 seconds. Regionally diverse privacy laws cultivate demand for configurable data-residency settings and bring-your-own-carrier options inside UCaaS stacks. Local system integrators bundle compliance consultancy, making adoption less daunting for mid-tier clinics.

Europe holds steady mid-single-digit growth underpinned by eHealth initiatives and cross-border data-sharing goals in the European Health Data Space. France's tele-consult legislation expanded remote-work eligibility for clinicians, fueling demand for secure video channels. GDPR obligations push interest in hybrid deployments, where communication payloads remain inside regional data centers. Vendor roadmaps increasingly reference "Schrems-II ready" architectures to court public hospitals.

- RingCentral, Inc.

- 8x8, Inc.

- Verizon Communications Inc.

- Comcast Corporation

- Vonage Holdings Corp. (Telefonaktiebolaget LM Ericsson)

- Intrado Corporation

- Star2Star Communications, LLC

- International Business Machines Corporation

- ALE International SAS (Alcatel-Lucent Enterprise)

- Cisco Systems, Inc.

- Microsoft Corporation

- Google LLC (Google Cloud)

- Zoom Video Communications, Inc.

- Avaya LLC

- Mitel Networks Corporation

- Fuze, Inc.

- Dialpad, Inc.

- NEC Corporation

- Twilio Inc.

- Genesys Telecommunications Laboratories, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Tele-health expansion post-COVID-19

- 4.2.2 Cost-saving OPEX model of UCaaS

- 4.2.3 Integration with EHR and clinical workflows

- 4.2.4 5G edge-enabled AR surgical collaboration

- 4.2.5 Compliance-as-a-Service bundles for HIPAA

- 4.2.6 AI-driven clinical documentation and workflow automation

- 4.3 Market Restraints

- 4.3.1 Data security and HIPAA concerns

- 4.3.2 Legacy PBX and low digital readiness

- 4.3.3 Budget squeeze from value-based care

- 4.3.4 Vendor lock-in with vertical UC stacks

- 4.4 Evaluation of Critical Regulatory Framework

- 4.5 Industry Value Chain Analysis

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Key Use Cases and Case Studies

- 4.9 Impact on Macroeconomic Factors of the Market

- 4.10 Investment Analysis

5 MARKET SEGMENTATION

- 5.1 By Deployment Model

- 5.1.1 Public Cloud

- 5.1.2 Private Cloud

- 5.1.3 Hybrid Cloud

- 5.2 By Component

- 5.2.1 Telephony / Voice

- 5.2.2 Unified Messaging

- 5.2.3 Conferencing

- 5.2.4 Collaboration Tools

- 5.2.5 Contact-Center Integration

- 5.3 By Application

- 5.3.1 Clinical Communications and Collaboration

- 5.3.2 Tele-health and Virtual Care

- 5.3.3 Administrative and Billing

- 5.3.4 Emergency Response Coordination

- 5.3.5 Patient Outreach and Engagement

- 5.4 By Organization Size

- 5.4.1 Large Enterprises

- 5.4.2 Small and Medium Enterprises

- 5.5 By End-User

- 5.5.1 Hospitals

- 5.5.2 Clinics and Physician Offices

- 5.5.3 Ambulatory Surgical Centers

- 5.5.4 Long-Term Care Facilities

- 5.5.5 Diagnostic and Imaging Centers

- 5.5.6 Home Healthcare Agencies

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Australia and New Zealand

- 5.6.4.6 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 Saudi Arabia

- 5.6.5.1.2 United Arab Emirates

- 5.6.5.1.3 Turkey

- 5.6.5.1.4 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Nigeria

- 5.6.5.2.3 Egypt

- 5.6.5.2.4 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 RingCentral, Inc.

- 6.4.2 8x8, Inc.

- 6.4.3 Verizon Communications Inc.

- 6.4.4 Comcast Corporation

- 6.4.5 Vonage Holdings Corp. (Telefonaktiebolaget LM Ericsson)

- 6.4.6 Intrado Corporation

- 6.4.7 Star2Star Communications, LLC

- 6.4.8 International Business Machines Corporation

- 6.4.9 ALE International SAS (Alcatel-Lucent Enterprise)

- 6.4.10 Cisco Systems, Inc.

- 6.4.11 Microsoft Corporation

- 6.4.12 Google LLC (Google Cloud)

- 6.4.13 Zoom Video Communications, Inc.

- 6.4.14 Avaya LLC

- 6.4.15 Mitel Networks Corporation

- 6.4.16 Fuze, Inc.

- 6.4.17 Dialpad, Inc.

- 6.4.18 NEC Corporation

- 6.4.19 Twilio Inc.

- 6.4.20 Genesys Telecommunications Laboratories, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

整合通訊市場:按組件、解決方案、部署類型、組織規模、應用和最終用戶產業分類-2026-2032年全球市場預測

整合通訊市場:按組件、解決方案、部署類型、組織規模、應用和最終用戶產業分類-2026-2032年全球市場預測 工業製造領域工人技術:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)

工業製造領域工人技術:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031) 整合通訊市場機會、成長要素、產業趨勢分析及2026-2035年預測整合通訊(UC)硬體:市場佔有率分析、產業趨勢和統計數據以及成長預測(2026-2031 年)

整合通訊市場機會、成長要素、產業趨勢分析及2026-2035年預測整合通訊(UC)硬體:市場佔有率分析、產業趨勢和統計數據以及成長預測(2026-2031 年) 整合通訊市場-全球產業規模、佔有率、趨勢、機會、預測:按產品、解決方案、組織規模、應用、地區和競爭對手分類,2021-2031年

整合通訊市場-全球產業規模、佔有率、趨勢、機會、預測:按產品、解決方案、組織規模、應用、地區和競爭對手分類,2021-2031年 整合通訊(UC) 和商務耳機市場預測至 2034 年—按產品類型、類別、價格、分銷管道、應用、最終用戶和地區分類的全球分析

整合通訊(UC) 和商務耳機市場預測至 2034 年—按產品類型、類別、價格、分銷管道、應用、最終用戶和地區分類的全球分析 整合通訊即服務 (UCaaS) 市場報告:按解決方案類型、組織規模、部署類型、產業和地區分類 (2026–2034)

整合通訊即服務 (UCaaS) 市場報告:按解決方案類型、組織規模、部署類型、產業和地區分類 (2026–2034) 2026年全球通訊與協作市場報告整合通訊和商務耳機市場規模:按產品、類型、價格、分銷管道、應用、最終用途和地區分類(2026-2034 年)整合通訊市場報告:按組件、產品、組織規模、最終用戶和地區分類(2026-2034 年)

2026年全球通訊與協作市場報告整合通訊和商務耳機市場規模:按產品、類型、價格、分銷管道、應用、最終用途和地區分類(2026-2034 年)整合通訊市場報告:按組件、產品、組織規模、最終用戶和地區分類(2026-2034 年)