|

市場調查報告書

商品編碼

2064016

美國高功率LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)United States High-Power LED Package - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

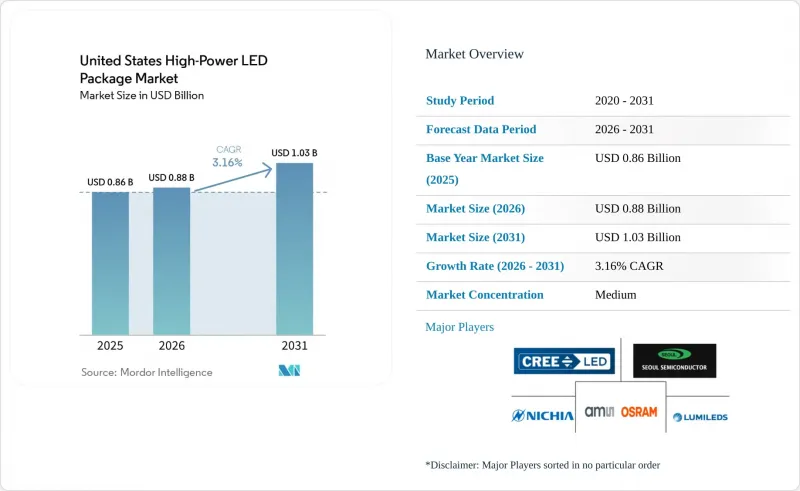

Mordor Intelligenceによると、米国の高功率LED構裝市場規模は、2025年の8億6,000万米ドルから2026年には8億8,000万米ドルに拡大し、2031年までに10億3,000万米ドルに達すると予測されており、2026年から2031年にかけてCAGR3.16%で成長すると見込まれています。

本報告依輸出功率範圍(1W–3W、3W–10W、10W以上)、封裝架構(單晶片封裝、多晶片封裝、COB等)和應用領域(通用照明、汽車照明、顯示器和背光等)進行分類。市場預測以美元(USD)計價。

美國高功率LED構裝市場趨勢與洞察。

小型高功率LED在園藝照明領域的應用迅速成長。

在環境可控農業領域,採用效率超過 80% 的緊湊型LED構裝正在重塑垂直農業的經濟格局。這些先進的封裝可達到超過 2000 µmol m⁻²s⁻¹ 的光合有效輻射通量密度,而第二代發送器有效輻射通量密度更是高達 4.1 µmol J⁻¹。因此,生產者可以減少所需的照明設備數量,提高效率並降低空調負荷,投資回收期縮短至 18 個月以內,高性能 LED 成為永續室內農業的基石。

能源效率法規推動了商業建築維修的需求。

美國能源局已將通用照明燈具的最低標準設定為每瓦45流明。在加州,第24號法案開放式替代性爭議解決(ADR)規則與一項廣泛的公用事業回扣計劃相結合,已成功獎勵了該州78%的人口。這些措施顯著加快了向聯網照明設備的過渡,這些設備現在通常包含3至10瓦的組件,並具備需量反應功能。即使第179D條規定的稅收抵扣預計將於2026年6月到期,這種轉變仍將有助於更快地收回初始成本。

功率超過 10W 時,溫度控管的挑戰會限制可靠性。

10ワットの閾值を超えるパッケージは、窒化アルミニウム(AlN)や窒化ケイ素(Si3N4)のような高度な基板がなければ放熱が非線形になるため、重大な溫度控管上の課題に直面します。これらの基板がない場合、接合部温度の上昇により、10 度C上昇するごとに発光効率が約5%低下する恐れがあり、これは要求の厳しい用途における性能を直接損なうことになります。また、この熱的ストレスは長期的な信頼性も損ない、LM-80試験では望ましい50,000時間のL90寿命を予測できないことが多いため、基板の選択は効率と耐久性の両方を決定づける重要な要素となります。

細分市場分析

截至2025年,1W-3W封裝產品佔據了美國高功率LED構裝市場48.77%的佔有率,這主要得益於下照燈和射燈等應用,這些應用優先考慮成熟的封裝尺寸和價格競爭力。然而,成長正在向更高功率等級轉移。隨著垂直農業和矩陣式頭燈對更高光子密度的需求,10W以上功率等級的LED頻寬產品預計到2031年將以3.58%的複合年成長率成長。美國10W以上高功率LED構裝的市場規模受惠於其溢價,抵銷了氮化鋁基基板材料成本40-60%的成長。

加州和亞利桑那州的環境控制種植者願意加大設備投入,因為即使發光效率僅提高1個百分點,也能每年節省8000至12000美元的能源成本。汽車原始設備製造商(OEM)也呈現類似的趨勢;特斯拉2026年的矩陣系統將採用數十個高亮度晶片,以實現無眩光的光通量,這是低功率裝置無法實現的。因此,能夠確保高導電性基板並符合AEC-Q102標準的供應商,相對於通用封裝製造商而言,正獲得競爭優勢。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 產業供應鏈分析

- 市場促進因素

- 小型高功率LED在園藝照明領域的應用迅速成長。

- 節能法規推動商業建築維修需求

- 降低高導熱基板的成本

- 透過覆晶架構的進步實現了高流明密度。

- 汽車自我調整頭燈法規(FMVSS-108 更新版)

- 智慧控制和整合高功率LED模組於路燈照明

- 市場限制因素

- 功率超過 10 瓦時的溫度控管挑戰:可靠性限制

- CSP和覆晶封裝相關的專利訴訟風險

- 氮化鎵晶片價格波動

- OLED 的廣泛應用減緩了 LCD 背光的更換週期。

- 監理情勢

- 技術展望

- 宏觀經濟因素的影響

- 波特五力分析

第5章 市場規模與成長預測

- 輸出範圍

- 1 W~3 W

- 3 W~10 W

- 超過10瓦

- 以建築學為例

- 單晶片封裝(SMD/分離式)

- 多晶片封裝(SMD)

- COB(板載晶片)

- 其他(CSP、覆晶、混合模組)

- 透過使用

- 一般照明

- 汽車照明

- 顯示器和背光

- 特殊/小眾

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Nichia Corporation

- Cree LED, an SGH Company

- Lumileds Holding BV

- Osram Opto Semiconductors GmbH

- Seoul Semiconductor Co., Ltd.

- Samsung Electronics Co., Ltd.

- LG Innotek Co., Ltd.

- Everlight Electronics Co., Ltd.

- Luminus Devices, Inc.

- Bridgelux, Inc.

- Lite-On Technology Corporation

- Toyoda Gosei Co., Ltd.

- Epistar Corporation

- Dominant Opto Technologies Sdn. Bhd.

- Edison Opto Corporation

- Citizen Electronics Co., Ltd.

- ProPhotonix Limited

- Crystal IS Inc.

- TT Electronics plc

- Advanced Optoelectronic Technology Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the united states high-power LED package market size is expected to increase from USD 0.86 billion in 2025 to USD 0.88 billion in 2026 and reach USD 1.03 billion by 2031, growing at a CAGR of 3.16% over 2026-2031.

This report is Segmented by Power Range (1 W To 3 W, 3 W To 10 W, and Above 10 W), Architecture (Single-Die Packages, Multi-Die Packages, COB, and More), and Application (General Lighting, Automotive Lighting, Display and Backlighting, and More). The Market Forecasts are Provided in Terms of Value (USD).

United States High-Power LED Package Market Trends and Insights

Surge In Miniaturized High-Power LED Adoption For Horticulture Lighting

In controlled-environment agriculture, the shift toward compact LED packages with wall-plug efficiencies above 80% is reshaping vertical farming economics. These advanced packages deliver photosynthetic photon flux densities exceeding 2,000 µmol m-2 s-1, while second-generation emitters now achieve an impressive 4.1 µmol J-1. As a result, growers can reduce the number of fixtures required, lower HVAC loads due to improved efficiency, and realize payback periods of less than 18 months, making high-performance LEDs a cornerstone of sustainable indoor farming.

Energy-Efficiency Mandates Driving Retrofit Demand In Commercial Buildings

The Department of Energy has set a minimum standard of 45 lumens per watt for general-service lamps. In California, Title 24's open-ADR rules, combined with widespread utility rebates, have successfully incentivized 78% of the state's population. These measures have led to a significant pivot towards networked luminaires. These advanced luminaires now commonly integrate 3 to 10-watt packages equipped with demand-response capabilities. This shift is enabling quicker recovery of initial costs, even with the impending June 2026 expiration of Section 179D deductions.

Thermal Management Challenges Above 10 W Limiting Reliability

Packages that cross the 10-watt threshold face significant thermal management challenges, as heat dissipation becomes non-linear without advanced substrates like aluminum nitride (AlN) or silicon nitride (Si3N4). When these substrates are absent, the elevated junction temperatures can cause luminous efficacy to decline by roughly 5% for every 10 °C increase, which directly undermines performance in demanding applications. This thermal stress also compromises long-term reliability, with LM-80 testing often failing to project the desired 50,000-hour L90 lifetime, making substrate choice a critical determinant of both efficiency and durability.

Other drivers and restraints analyzed in the detailed report include:

- Declining Cost Of High Thermal Conductivity Substrates

- Advances In Flip-Chip Architecture Enabling Higher Lumen Density

- Patent Litigation Risk Around CSP And Flip-Chip Packages

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Packages of 1 W-3 W retained 48.77% of the United States high-power LED package market share in 2025, anchored in downlights and troffers that value mature footprints and price competition. Growth, however, is shifting upward: the above 10 W band is on a 3.58% CAGR trajectory to 2031 as vertical farms and matrix headlamps demand superior photon density. The United States high-power LED package market size for the above 10 W class benefits from premium pricing that offsets the 40-60% material uplift tied to aluminum nitride substrates.

Controlled-environment cultivators in California and Arizona tolerate higher capex because a single-percentage-point jump in efficacy can shave USD 8,000-12,000 from annual energy bills. Automotive OEMs echo this dynamic, Tesla's 2026 matrix system deploys dozens of high-flux dies to paint glare-free beams, a feature impossible with lower-wattage devices. Suppliers that can secure high-conductivity substrates and meet AEC-Q102 grades are therefore outpacing commodity package makers.

List of Companies Covered in this Report:

- Nichia Corporation

- Cree LED, an SGH Company

- Lumileds Holding B.V.

- Osram Opto Semiconductors GmbH

- Seoul Semiconductor Co., Ltd.

- Samsung Electronics Co., Ltd.

- LG Innotek Co., Ltd.

- Everlight Electronics Co., Ltd.

- Luminus Devices, Inc.

- Bridgelux, Inc.

- Lite-On Technology Corporation

- Toyoda Gosei Co., Ltd.

- Epistar Corporation

- Dominant Opto Technologies Sdn. Bhd.

- Edison Opto Corporation

- Citizen Electronics Co., Ltd.

- ProPhotonix Limited

- Crystal IS Inc.

- TT Electronics plc

- Advanced Optoelectronic Technology Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Industry Supply-Chain Analysis

- 4.3 Market Drivers

- 4.3.1 Surge in Miniaturized High-Power LED Adoption for Horticulture Lighting

- 4.3.2 Energy-Efficiency Mandates Driving Retrofit Demand in Commercial Buildings

- 4.3.3 Declining Cost of High Thermal Conductivity Substrates

- 4.3.4 Advances in Flip-Chip Architecture Enabling Higher Lumen Density

- 4.3.5 Automotive Adaptive Headlamp Regulations (FMVSS-108 Updates)

- 4.3.6 Integration of Smart Controls with High-Power LED Modules in Street Lighting

- 4.4 Market Restraints

- 4.4.1 Thermal Management Challenges Above 10 W Limiting Reliability

- 4.4.2 Patent Litigation Risk Around CSP and Flip-Chip Packages

- 4.4.3 Volatility in Gallium Nitride Wafer Pricing

- 4.4.4 Slowdown in LCD Backlight Replacement Cycle Due to OLED Penetration

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Power Range

- 5.1.1 1 W - 3 W

- 5.1.2 3 W - 10 W

- 5.1.3 Above 10 W

- 5.2 By Architecture

- 5.2.1 Single-die Packages (SMD / Discrete)

- 5.2.2 Multi-die Packages (SMD)

- 5.2.3 COB (Chip-on-Board)

- 5.2.4 Others (CSP, Flip-Chip, Hybrid Modules)

- 5.3 By Application

- 5.3.1 General Lighting

- 5.3.2 Automotive Lighting

- 5.3.3 Display and Backlighting

- 5.3.4 Specialty / Niche

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Nichia Corporation

- 6.4.2 Cree LED, an SGH Company

- 6.4.3 Lumileds Holding B.V.

- 6.4.4 Osram Opto Semiconductors GmbH

- 6.4.5 Seoul Semiconductor Co., Ltd.

- 6.4.6 Samsung Electronics Co., Ltd.

- 6.4.7 LG Innotek Co., Ltd.

- 6.4.8 Everlight Electronics Co., Ltd.

- 6.4.9 Luminus Devices, Inc.

- 6.4.10 Bridgelux, Inc.

- 6.4.11 Lite-On Technology Corporation

- 6.4.12 Toyoda Gosei Co., Ltd.

- 6.4.13 Epistar Corporation

- 6.4.14 Dominant Opto Technologies Sdn. Bhd.

- 6.4.15 Edison Opto Corporation

- 6.4.16 Citizen Electronics Co., Ltd.

- 6.4.17 ProPhotonix Limited

- 6.4.18 Crystal IS Inc.

- 6.4.19 TT Electronics plc

- 6.4.20 Advanced Optoelectronic Technology Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment