|

市場調查報告書

商品編碼

2064015

歐洲高功率LED構裝:市佔率分析、產業趨勢與統計及成長預測(2026-2031年)Europe High-Power LED Package - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

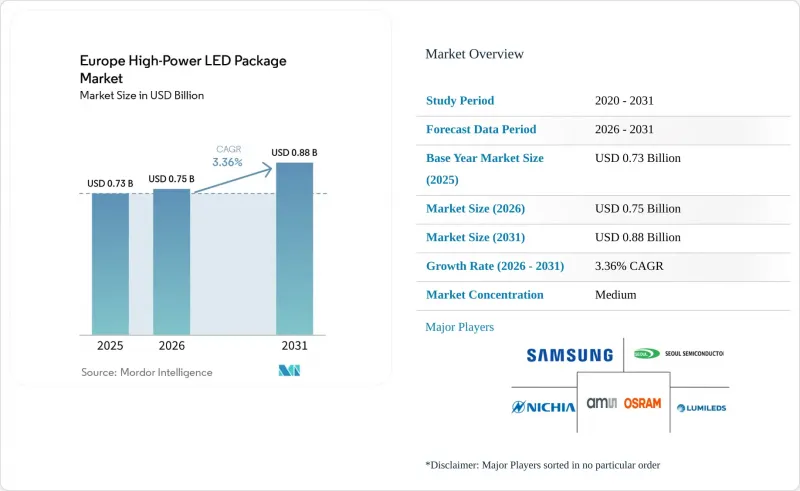

據 Mordor Intelligence 稱,2025 年歐洲高功率LED構裝市場價值為 7.3 億美元,預計到 2031 年將達到 8.8 億美元,而 2026 年為 7.5 億美元,預測期(2026-2031 年)的複合年成長率為 3.36%。

本報告按輸出功率範圍(1W–3W、3W–10W、10W以上)、封裝架構(單晶片封裝、多晶片封裝等)、應用領域(通用照明、汽車照明、顯示器和背光等)以及國家(英國、德國等)進行細分。市場預測以美元計價。

歐洲高功率LED構裝市場趨勢與洞察

高功率封裝的 $/lm(每流明成本)急劇下降。

中國氮化鎵晶圓的過剩供應,加上磷光體轉換效率的提升,導致高功率LED構裝價格每年下降約15%。歐洲照明製造商正轉向減少發光元件數量並採用更高亮度元件的設計,雖然降低了元件成本,但也壓縮了供應商的利潤空間。擁有磷光體知識產權的垂直整合供應商能夠承受晶圓價格的波動,而通用組裝商則面臨產品同質化的直接挑戰。 Lumileds公司於2025年2月推出的LUXEON HL2X-V產品清楚地展現了這一轉變,其在85°C的結溫下實現了200 lm/W的發光效率,從而降低了工業高棚照明維修的系統成本。採購部門越來越重視「每流明成本」而非表面發光效率,導致合約週期縮短,設計變更速度加快。

中國和日本汽車LED燈採用率的快速成長。

預計到2025年,中國乘用車LED燈的普及率將超過70%。在日本,用於超薄頭燈的微型LED陣列已於2025年3月獲得批准。歐洲汽車製造商目前正採用這些架構以滿足歐盟安全標準並區分其高階產品,板載晶片(COB)模組也正在整合到區域供應鏈中。 Polbia的子公司海拉宣布,其照明部門2023年的銷售額達到30億歐元(33.9億美元),並憑藉其氮化鎵碳化矽封裝技術(可將電動車能耗降低40%)佔據了歐洲高階頭燈市場25%的佔有率。然而,亞洲的成本標準正在影響歐洲的談判,迫使供應商在滿足更嚴格的等級標準和可靠性指標的同時,適應亞太地區的單位經濟效益。

激烈的競爭導致利潤率下降。

中國晶圓代工廠產能運轉率超過85%,其定價比歐洲價格低30%,導致毛利率低於永續水準。 2025年8月,Lumileds以2.39億美元的價格出售給三安光電,這清楚地表明了上游工程晶圓整合的生存優勢。因此,歐洲供應商正退守AEC-Q102認證的汽車封裝、園藝頻譜和超高顯色指數博物館模組等細分市場。然而,產量下降限制了固定成本的消化,從而形成利潤率持續承壓和防禦性整合的惡性循環。

細分市場分析

功率超過10W的LED封裝產品將以3.98%的複合年成長率成長,直到2031年,超過目前主導歐洲高功率LED構裝市場的低功率產品。 1W-3W頻寬在2025年將佔據47.13%的市場佔有率,在成本和尺寸親和性是關鍵採購因素的通用照明維修應用中仍然很受歡迎。然而,隨著大多數大規模倉庫和辦公大樓在2025年前完成LED改造並進入更換週期,此功率段的成長速度正在放緩。 3W-10W功率段的產品適用於汽車日間行車燈和路燈,可在流明輸出和可控熱負載之間取得平衡。

GaN-on-SiC基板和雙相蒸氣腔技術的突破使得即使在200 W/cm²的光通量下,結溫也能保持在125 度C以下,從而使功率超過10 W的模組得以廣泛應用於體育場館泛光照明和港口起重機照明燈具。 Lumileds公司的LUXEON HL2X-V便是這項變革的典範,其發光效率提高了12%,熱阻也顯著降低。 IEC 62471標準規定了高藍光成分頻譜的驅動電流上限,這限制了絕對效率。因此,供應商正在調整磷光體配方,以滿足風險等級1的要求,同時保持目標亮度。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 高功率封裝價格(美元/公升)急劇下降

- 中國和日本汽車LED燈採用率的快速成長。

- 東協各國強制推行節能措施

- 將工業照明昇等為高棚LED照明。

- 溫度控管技術的重大進步使得功率輸出達到 10 瓦或以上的封裝成為可能*

- 印度針對氮化鎵矽基LED代工廠的生產相關獎勵*

- 市場限制因素

- 激烈的競爭導致利潤率下降。

- 藍寶石基板供應不穩定

- 限制驅動電流的光生物安全標準

- 廢舊產品回收系統不完善*

- 監理情勢

- 宏觀經濟因素的影響

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 輸出範圍

- 1 W~3 W

- 3 W~10 W

- 超過10瓦

- 以建築學為例

- 單晶片封裝(SMD/分離式)

- 多晶片封裝(SMD)

- COB(板載晶片)

- 其他(CSP、覆晶、混合模組)

- 透過使用

- 一般照明

- 汽車照明

- 顯示器和背光

- 特殊/小眾

- 歐洲國家

- 英國

- 德國

- 法國

- 其他歐洲國家

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Nichia Corporation

- ams-OSRAM AG

- Seoul Semiconductor Co., Ltd.

- Lumileds Holding BV

- Samsung Electronics Co., Ltd.

- Cree LED, Inc.

- Everlight Electronics Co., Ltd.

- LG Innotek Co., Ltd.

- Lextar Electronics Corporation

- Broadcom Inc.

- Brightek Optoelectronic Co., Ltd.

- Dominant Opto Technologies Sdn. Bhd.

- Stanley Electric Co., Ltd.

- Lite-On Technology Corporation

- Refond Optoelectronics Co., Ltd.

- Hongli Zhihui Group Co., Ltd.

- NationStar Optoelectronics Co., Ltd.

- TDK Electronics AG

- Wurth Elektronik GmbH & Co. KG

- Vishay Intertechnology, Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the europe high-Power lED package market size was valued at USD 0.73 billion in 2025 and is estimated to grow from USD 0.75 billion in 2026 to reach USD 0.88 billion by 2031, at a CAGR of 3.36% during the forecast period (2026-2031).

This report is Segmented by Power Range (1 W To 3 W, 3 W To 10 W, and Above 10 W), Architecture (Single-Die Packages, Multi-Die Packages, and More), Application (General Lighting, Automotive Lighting, Display and Backlighting, and More), and Country (United Kingdom, Germany, and More). The Market Forecasts are Provided in Terms of Value (USD).

Europe High-Power LED Package Market Trends and Insights

Rapid Decline in $/lm for High-Power Packages

High-power LED package prices are falling roughly 15% a year as oversupply in China's gallium-nitride wafer capacity converges with efficiency gains in phosphor conversion. European luminaire makers are redesigning fixtures around fewer, brighter emitters, cutting bill-of-materials costs but shrinking supplier margins. Vertically integrated vendors that own phosphor IP can absorb wafer volatility, whereas merchant assemblers face immediate commoditization. Lumileds' LUXEON HL2X-V, launched February 2025, underscores this shift by delivering 200 lm W-1 at 85 °C junction temperature and lowering system cost for industrial high-bay retrofits. Procurement teams increasingly emphasize dollar-per-lumen benchmarks over headline efficacy, tightening contract cycles and accelerating design revisions.

Soaring Automotive LED Penetration in China and Japan

LED penetration in Chinese passenger cars topped 70% in 2025, and Japan cleared micro-LED arrays for ultrathin headlamps in March 2025. European automakers are now importing these architectures to meet EU safety rules and differentiate premium trims, bringing chip-on-board modules into regional supply chains. Hella, part of Forvia, cited lighting revenue of EUR 3 billion (USD 3.39 billion) for 2023 and a 25% share of Europe's premium headlamp segment, on the back of gallium-nitride-on-silicon-carbide packages that cut EV energy draw by 40%. Asian cost baselines, however, frame European negotiations, forcing suppliers to match APAC unit economics while meeting stricter binning and reliability metrics.

Margin Erosion from Intense Price Competition

Chinese foundries running at 85%+ utilization undercut European pricing by up to 30%, compressing gross margins below sustainable thresholds. Lumileds' August 2025 sale to San'an Optoelectronics for USD 239 million illustrated the survival advantage of upstream wafer integration. European vendors, therefore, retreat to niches such as AEC-Q102-qualified automotive packages, horticulture spectra, and ultra-high-CRI museum modules. Yet lower volume limits fixed-cost absorption, creating a feedback loop of continuing margin pressure and defensive consolidation.

Other drivers and restraints analyzed in the detailed report include:

- Energy-Efficiency Mandates Across ASEAN

- Industrial Retrofits to High-Bay LED Fixtures

- Volatile Sapphire Substrate Supply

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Above-10-W packages are advancing at a 3.98% CAGR to 2031, outpacing lower-power classes that currently dominate the Europe high-power LED package market. The 1 W-3 W bracket, which held a 47.13% share in 2025, remains popular for general lighting retrofits, where cost and form-factor familiarity drive purchasing. Growth, however, is flattening as most large warehouses and offices have completed LED conversions by 2025 and now enter replacement cycles. Packages in the 3 W-10 W tier support automotive daytime running lamps and streetlights, balancing lumen output against manageable heat loads.

Technology breakthroughs in GaN-on-SiC substrates and two-phase vapor chambers now keep junction temperatures below 125 °C at 200 W cm-2 flux, enabling above-10-W modules to invade stadium floodlighting and port-crane luminaires. Lumileds' LUXEON HL2X-V exemplifies this shift, pairing 12% higher efficacy with reduced thermal resistance. IEC 62471 rules that cap drive currents for blue-rich spectra impose limits on absolute efficacy, prompting suppliers to tweak phosphor blends to meet Risk Group 1 while preserving target brightness.

List of Companies Covered in this Report:

- Nichia Corporation

- ams-OSRAM AG

- Seoul Semiconductor Co., Ltd.

- Lumileds Holding B.V.

- Samsung Electronics Co., Ltd.

- Cree LED, Inc.

- Everlight Electronics Co., Ltd.

- LG Innotek Co., Ltd.

- Lextar Electronics Corporation

- Broadcom Inc.

- Brightek Optoelectronic Co., Ltd.

- Dominant Opto Technologies Sdn. Bhd.

- Stanley Electric Co., Ltd.

- Lite-On Technology Corporation

- Refond Optoelectronics Co., Ltd.

- Hongli Zhihui Group Co., Ltd.

- NationStar Optoelectronics Co., Ltd.

- TDK Electronics AG

- Wurth Elektronik GmbH & Co. KG

- Vishay Intertechnology, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Decline in $/lm for High-Power Packages

- 4.2.2 Soaring Automotive LED Penetration in China and Japan

- 4.2.3 Energy-Efficiency Mandates Across ASEAN

- 4.2.4 Industrial Retrofits to High-Bay LED Fixtures

- 4.2.5 Thermal-Management Breakthroughs Enabling 10 W+ Packages*

- 4.2.6 India's PLI Incentives for GaN-on-SiC LED Foundries*

- 4.3 Market Restraints

- 4.3.1 Margin Erosion from Intense Price Competition

- 4.3.2 Volatile Sapphire Substrate Supply

- 4.3.3 Photobiological Safety Norms Limiting Drive Current

- 4.3.4 Inadequate End-of-Life Recycling Streams*

- 4.4 Regulatory Landscape

- 4.5 Impact of Macroeconomic Factors

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS

- 5.1 By Power Range

- 5.1.1 1 W - 3 W

- 5.1.2 3 W - 10 W

- 5.1.3 Above 10 W

- 5.2 By Architecture

- 5.2.1 Single-die Packages (SMD / Discrete)

- 5.2.2 Multi-die Packages (SMD)

- 5.2.3 COB (Chip-on-Board)

- 5.2.4 Others (CSP, Flip-chip, Hybrid Modules)

- 5.3 By Application

- 5.3.1 General Lighting

- 5.3.2 Automotive Lighting

- 5.3.3 Display and Backlighting

- 5.3.4 Specialty / Niche

- 5.4 By Europe

- 5.4.1 United Kingdom

- 5.4.2 Germany

- 5.4.3 France

- 5.4.4 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Nichia Corporation

- 6.4.2 ams-OSRAM AG

- 6.4.3 Seoul Semiconductor Co., Ltd.

- 6.4.4 Lumileds Holding B.V.

- 6.4.5 Samsung Electronics Co., Ltd.

- 6.4.6 Cree LED, Inc.

- 6.4.7 Everlight Electronics Co., Ltd.

- 6.4.8 LG Innotek Co., Ltd.

- 6.4.9 Lextar Electronics Corporation

- 6.4.10 Broadcom Inc.

- 6.4.11 Brightek Optoelectronic Co., Ltd.

- 6.4.12 Dominant Opto Technologies Sdn. Bhd.

- 6.4.13 Stanley Electric Co., Ltd.

- 6.4.14 Lite-On Technology Corporation

- 6.4.15 Refond Optoelectronics Co., Ltd.

- 6.4.16 Hongli Zhihui Group Co., Ltd.

- 6.4.17 NationStar Optoelectronics Co., Ltd.

- 6.4.18 TDK Electronics AG

- 6.4.19 Wurth Elektronik GmbH & Co. KG

- 6.4.20 Vishay Intertechnology, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space And Unmet-Need Assessment