|

市場調查報告書

商品編碼

2063983

農藥添加劑:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Agrochemical Additives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

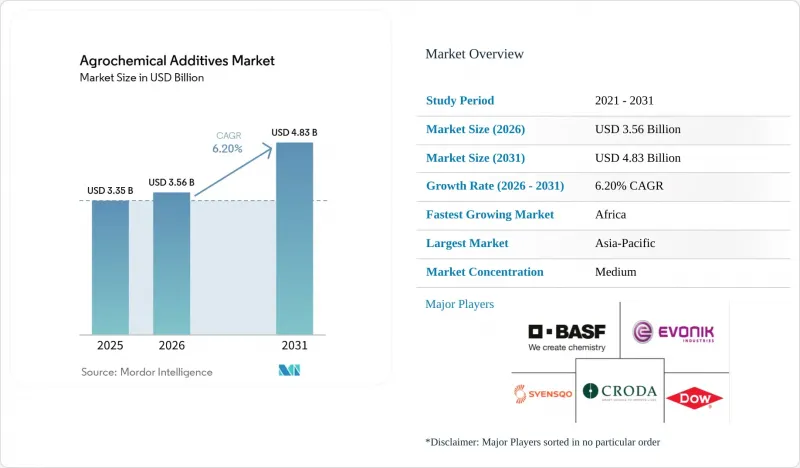

根據 Mordor Intelligence 預測,農藥添加劑市場規模將從 2025 年的 33.5 億美元成長到 2026 年的 35.6 億美元,到 2031 年將達到 48.3 億美元,2026 年至 2031 年的複合年預計成長率為 6.2%。

本報告按添加劑類型(界面活性劑、分散劑等)、形態(液體和固體)、應用領域(農藥、肥料等)、作物類型(穀物、水果和蔬菜等)以及地區(北美、南美、歐洲、亞太、中東和非洲)進行細分。市場預測以美元計價。

全球農藥添加劑市場趨勢及洞察

對提高作物產量的需求不斷成長

聯合國糧食及農業組織(糧農組織)的數據凸顯了人們對提高作物產量日益成長的需求。糧農組織報告預測,全球糧食產量將從2024年的28.49億噸增加至2025年的29.11億噸,年增2.1%。這一成長主要由單產提高而非耕地擴張所驅動,反映出農業生產正朝著提高效率的方向發展。生產力的提升依賴於精密農業和投入最佳化,其中農藥添加劑在提高農藥效力、養分吸收和施用效率方面發揮著至關重要的作用。這一趨勢正在推動農藥添加劑市場需求的成長。

精準噴塗和奈米製劑的快速普及

精準噴灑技術因其能夠提高噴灑精度和工作效率而迅速普及。印度阿拉哈巴德資訊技術研究所的研究人員報告稱,到2025年,基於無人機的噴灑系統將實現高達95%的噴灑覆蓋率,並將漂移減少近80%,凸顯了定向噴灑方法的優勢。要達到如此高的性能水平,需要最佳化黏度、穩定性和噴霧特性的配方,因此對先進添加劑和奈米配方的需求日益成長。此外,隨著無人機噴灑的日益普及,對與現代農業設備相容的高精度配方技術的需求也日益成長。

監管機構正在加強對乙氧基化壬基酚的監管。

鑑於壬基酚乙氧基化物對環境和健康造成的廣泛影響,監管機構正在加強對其的控制。在2025年的一項研究中,Toxics Link在40種受測產品中的15種中檢測到了壬基酚乙氧基化物。產品中的濃度最高達到957毫克/公斤,河水中的濃度更是創下70微克/公升的歷史新高,凸顯了污染的嚴重性。隨著這些事實的曝光,人們對該化合物的內分泌干擾效應及其在環境中的持久性日益擔憂,導致監管審查力度加大。因此,製造商正轉向更安全的產品配方。這種轉變增加了合規成本,延長了核准時間,並抑制了市場成長。

細分市場分析

2025年,界面活性劑在農藥添加劑市場中佔據最大佔有率,達到44%,其主導地位主要歸功於其在提高噴霧覆蓋率和確保農藥製劑穩定性方面發揮的關鍵作用。界面活性劑在乳化劑、濃縮劑和懸浮劑中的廣泛應用,支撐了主要農業區穩定的市場需求。隨著法規更加關注噴霧效率和環境安全,漂移抑制劑的重要性日益凸顯。精準噴霧技術的日益普及進一步增加了對能夠改善液滴控制的功能性添加劑的需求,凸顯了高性能化學品在現代製劑策略中的重要作用。

預計從2026年到2031年,噴霧漂移抑制劑市場將以9.5%的複合年成長率(CAGR)實現最高增速,這主要得益於日益嚴格的監管要求,旨在最大限度地減少噴霧漂移並提高噴塗精度。包括無人機和精密噴塗設備在內的先進噴塗技術的快速普及,正在推動對黏度調節聚合物的需求。這些聚合物不僅能確保噴塗效果,還能滿足嚴格的環保標準。此外,永續發展趨勢正在推動可生物分解和環保添加劑的創新。這種向符合監管要求的專業解決方案的轉變正在改變市場競爭格局,並賦予高性能添加劑系統優勢。

預計2025年,液體製劑將佔據農藥添加劑市場高達61%的佔有率。這主要歸功於其快速分散、易於操作以及與最新噴灑系統的兼容性。這些製劑是大規模農業作業的首選,因為它們可以與大容量噴霧器和精準施藥技術無縫整合。機械化程度的提高和葉面噴布技術的普及進一步增強了這一優勢,因為均勻混合和一致施用對於最佳化農藥和養分分佈的性能至關重要。

預計液體製劑將保持最快的成長勢頭,在2026年至2031年的預測期內,其複合年成長率將達到6.8%,這主要得益於精密農業和無人機噴灑系統的進步。同時,固態製劑因其穩定性好、運輸難度較低等優點,在種子加工和物流敏感地區越來越受歡迎。此外,包裝減少和保存期限延長等環境因素也促進了固態製劑的逐步普及。然而,由於液體製劑操作高效且與不斷發展的農業技術相容,預計仍將繼續保持主導地位。

區域分析

亞太地區在農業現代化快速推進和精準技術廣泛應用的驅動下,預計2025年將佔據全球農藥添加劑市場34%的佔有率。中國和印度等國正透過政策支援和技術整合,大力推動農業機械化,並促進投入品的高效利用。該地區廣闊的耕地和對提高生產力日益成長的需求,推動了對高性能解決方案的需求。此外,不斷擴大的本地生產和政府主導的各項舉措,正在加強區域供應鏈,並促進先進農業技術的應用。

預計2026年至2031年間,非洲市場將以7.8%的複合年成長率(CAGR)實現最高成長,主要得益於農業生產力投資的增加和農業投入品獲取管道的改善。普惠金融計畫和補貼相關措施正在推動小規模農戶社區採用現代農業投入品。此外,人們對高效投入品利用和作物保護意識的提高也推動了市場需求。同時,南美洲市場在大規模商業農業和先進作物管理技術的廣泛應用支撐下,持續展現強勁的成長潛力。

北美憑藉著高技術普及率和完善的農業體系,佔據著舉足輕重的地位。根據美國農業部(USDA)預測,到2024年,美國可耕地總面積將達到3.28億英畝,凸顯了集約農業的規模和農業資源的永續利用。如此龐大的農業基礎,正推動著對以性能增強配方為基礎的作物保護解決方案的持續需求。歐洲市場監管嚴格,但創新驅動力強勁;而中東市場則在節水措施和環境友善農業的推動下,實現了溫和成長。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 對更高作物產量的需求日益成長

- 精準噴塗和奈米製劑的快速普及

- 政府補助正轉向佐劑最佳化配方。

- 擴大抗Glyphosate作物的種植,需要使其與化學肥料相容。

- 無人機葉面噴布的廣泛應用需要使用低黏度添加劑。

- 將排碳權化以減少化學肥料添加劑的使用

- 市場限制因素

- 加強對乙氧基化壬基酚的監管。

- 環氧乙烷和醇乙氧基化物原料價格波動

- 農民對高價生物基助劑的抗拒情緒

- 農業化學品經銷商的整合給添加劑的利潤率帶來了壓力。

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 按添加劑類型

- 界面活性劑

- 分散劑

- 乳化劑

- 消泡劑

- 漂移抑制劑

- 其他

- 按形式

- 液體

- 固體的

- 透過使用

- 殺蟲劑

- 肥料

- 種子處理

- 土壤改良劑

- 按作物類型

- 穀類和穀類食品

- 水果和蔬菜

- 油籽/豆類

- 其他

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 其他北美國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 法國

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 澳洲

- 其他亞太國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他中東國家

- 非洲

- 南非

- 肯亞

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- BASF SE

- Evonik Industries AG

- Croda International Plc

- Dow Inc.

- Syensqo SA

- Stepan Company

- Clariant AG

- Nouryon Holding BV

- Huntsman International LLC

- Ingevity Corporation

- Sasol Limited

- Innospec Inc.

- LEVACO Chemicals GmbH

- Precision Laboratories LLC

第7章 市場機會與未來展望

According to Mordor Intelligence, the agrochemical additives market size is projected to grow from USD 3.35 billion in 2025 to USD 3.56 billion in 2026 and is projected to reach USD 4.83 billion by 2031, registering a CAGR of 6.2% during 2026-2031.

This report is Segmented by Additive Type (Surfactants, Dispersants, and More), by Form (Liquid and Solid), by Application (Pesticides, Fertilizers, and More), by Crop Type (Cereals and Grains, Fruits and Vegetables, and More), and by Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Agrochemical Additives Market Trends and Insights

Growing Demand for Higher Crop Yield Intensification

The increasing demand for higher crop yield intensification is highlighted by data from the Food and Agriculture Organization (FAO), which reports that global cereal production rose from 2,849 million metric tons in 2024 to 2,911 million metric tons in 2025, representing a 2.1% year-on-year increase. This growth is primarily attributed to improved yields rather than the expansion of cultivated land, reflecting a focus on efficiency-driven farming practices. These productivity improvements rely on precision agriculture and optimized input usage, where agrochemical additives play a critical role in enhancing pesticide effectiveness, nutrient absorption, and spray efficiency. This trend is contributing to rising demand in the agrochemical additives market.

Rapid Uptake of Precision Spraying and Nano-Formulations

Precision spraying technologies are experiencing significant adoption due to their capability to improve application accuracy and operational efficiency. Researchers from the Indian Institute of Information Technology, Allahabad, reported that UAV-based spraying systems achieved up to 95% spray coverage efficiency while reducing drift by nearly 80% as of 2025, emphasizing the advantages of targeted application methods. This level of performance necessitates formulations with optimized viscosity, stability, and spray characteristics, thereby increasing the demand for advanced additives and nano-formulations. Additionally, the expanding use of drone-based spraying is driving the need for precision-grade formulation technologies that are compatible with modern agricultural equipment.

Increasing Regulatory Scrutiny on Ethoxylated Nonylphenols

Regulatory bodies are tightening their grip on ethoxylated nonylphenols, given their prevalent environmental footprint and the health hazards they pose. In a 2025 investigation, Toxics Link uncovered nonylphenol ethoxylates in 15 of the 40 products tested. Concentrations peaked at 957 mg/kg in products and reached 70 µg/L in river water, underscoring the severity of contamination. Such revelations amplify worries about endocrine disruption and the compounds' longevity in the environment, leading to heightened regulatory vigilance. Consequently, manufacturers are pivoting towards safer product formulations. This shift increases compliance costs, lengthens approval timelines, and restrains market growth.

Other drivers and restraints analyzed in the detailed report include:

- Government Subsidy Shift Toward Adjuvant-Optimized Formulations

- Expansion of Glyphosate-Tolerant Crops Needing Adjuvant Compatibility

- Volatility in Ethylene Oxide and Alcohol-Ethoxylate Feedstock Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The surfactants segment held the largest 44% share of the agrochemical additives market in 2025, maintaining its dominance due to its critical role in enhancing spray coverage and ensuring formulation stability in pesticide applications. Their widespread use in emulsifiable concentrates and suspension systems supports consistent demand in major agricultural regions. With a regulatory focus on spray efficiency and environmental safety, the importance of drift-control agents has increased. The growing adoption of precision spraying technologies has further boosted the demand for functional additives that improve droplet control, emphasizing the role of performance-oriented chemistries in modern formulation strategies.

The drift control agents segment is projected to grow at the fastest CAGR of 9.5% during 2026-2031, driven by stricter regulatory requirements to minimize spray drift and enhance application accuracy. The rapid adoption of advanced spraying technologies, including drones and precision tools, is fueling demand for viscosity-modifying polymers. These polymers not only ensure effectiveness but also meet stringent environmental standards. Furthermore, sustainability trends are fostering innovation in biodegradable and eco-friendly additives. This shift toward specialized, regulation-compliant solutions is transforming the competitive landscape, favoring high-performance additive systems.

Liquid formulations accounted for the largest 61% of the agrochemical additives market share in 2025, driven by their rapid dispersion, ease of handling, and compatibility with modern spraying systems. These formulations are the preferred choice in large-scale agricultural operations due to their seamless integration with high-capacity sprayers and precision technologies. Their dominance is further supported by increasing mechanization and the adoption of foliar application methods, where uniform mixing and consistent delivery are essential for optimizing performance in pesticide and nutrient applications.

Liquid formulations are anticipated to maintain the fastest growth trajectory, registering a CAGR of 6.8% during the forecast period 2026-2031, fueled by advancements in precision agriculture and drone-based spraying systems. Meanwhile, solid formulations are gaining popularity in seed treatment and regions sensitive to logistics due to their stability and reduced transportation challenges. Environmental factors, such as packaging reduction and improved shelf life, are also contributing to the gradual adoption of solid formats. However, liquids are projected to maintain their leading position owing to their operational efficiency and compatibility with evolving agricultural technologies.

Geography Analysis

Asia-Pacific held the largest 34% agrochemical additives market share in 2025, supported by rapid agricultural modernization and the widespread adoption of precision technologies. Countries such as China and India are advancing mechanized farming and promoting efficient input utilization through policy support and technology integration. The region's extensive cultivation base and growing emphasis on productivity enhancement are sustaining demand for performance-focused solutions. Additionally, the expansion of local manufacturing and government-supported initiatives is bolstering regional supply chains and facilitating the adoption of advanced agricultural practices.

Africa market size is projected to grow at the fastest 7.8% CAGR from 2026 to 2031, driven by increasing investments in agricultural productivity and improved access to farming inputs. Financial inclusion programs and subsidy-linked initiatives are enhancing the adoption of modern farming inputs among smallholder communities. Furthermore, rising awareness of efficient input usage and crop protection is driving demand. Meanwhile, South America continues to exhibit strong growth potential, supported by large-scale commercial farming and the growing adoption of advanced crop management techniques.

North America holds a prominent position due to its high level of technological adoption and well-structured agricultural systems. According to the United States Department of Agriculture (USDA), the total cropland used for crops in the United States was 328 million acres in 2024, highlighting the scale of intensive farming and consistent input utilization. This extensive cultivation base drives steady demand for crop protection solutions reliant on performance-enhancing formulations. Europe remains a regulated but innovation-focused market, while the Middle East exhibits gradual growth, supported by water-efficiency initiatives and controlled-environment agriculture.

- BASF SE

- Evonik Industries AG

- Croda International Plc

- Dow Inc.

- Syensqo SA

- Stepan Company

- Clariant AG

- Nouryon Holding B.V.

- Huntsman International LLC

- Ingevity Corporation

- Sasol Limited

- Innospec Inc.

- LEVACO Chemicals GmbH

- Precision Laboratories LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing demand for higher crop yield intensification

- 4.2.2 Rapid uptake of precision spraying and nano-formulations

- 4.2.3 Government subsidy shift toward adjuvant-optimized formulations

- 4.2.4 Expansion of glyphosate-tolerant crops needing adjuvant compatibility

- 4.2.5 Rising drone-based foliar application requiring low-viscosity additives

- 4.2.6 Carbon-credit monetization for fertilizer reduction via additives

- 4.3 Market Restraints

- 4.3.1 Increasing regulatory scrutiny on ethoxylated nonylphenols

- 4.3.2 Volatility in ethylene oxide and alcohol-ethoxylate feedstock costs

- 4.3.3 Farmer reluctance toward premium bio-based adjuvants

- 4.3.4 Ag-chem distributor consolidation squeezing additive margins

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value, USD)

- 5.1 By Additive Type

- 5.1.1 Surfactants

- 5.1.2 Dispersants

- 5.1.3 Emulsifiers

- 5.1.4 Antifoaming Agents

- 5.1.5 Drift Control Agents

- 5.1.6 Others

- 5.2 By Form

- 5.2.1 Liquid

- 5.2.2 Solid

- 5.3 By Application

- 5.3.1 Pesticides

- 5.3.2 Fertilizers

- 5.3.3 Seed Treatment

- 5.3.4 Soil Conditioners

- 5.4 By Crop Type

- 5.4.1 Cereals and Grains

- 5.4.2 Fruits and Vegetables

- 5.4.3 Oilseeds and Pulses

- 5.4.4 Others

- 5.5 By Region

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.1.4 Rest of North America

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 France

- 5.5.3.3 Russia

- 5.5.3.4 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Australia

- 5.5.4.4 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Kenya

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 BASF SE

- 6.4.2 Evonik Industries AG

- 6.4.3 Croda International Plc

- 6.4.4 Dow Inc.

- 6.4.5 Syensqo SA

- 6.4.6 Stepan Company

- 6.4.7 Clariant AG

- 6.4.8 Nouryon Holding B.V.

- 6.4.9 Huntsman International LLC

- 6.4.10 Ingevity Corporation

- 6.4.11 Sasol Limited

- 6.4.12 Innospec Inc.

- 6.4.13 LEVACO Chemicals GmbH

- 6.4.14 Precision Laboratories LLC

7 Market Opportunities and Future Outlook

農藥市場:全球市場按產品類型、性質、作物類型、配方和應用進行預測 - 2026-2032年農藥儲槽市場:2026-2032年全球市場預測(依儲槽類型、材質、容量、運作模式、壓力類型、移動性、應用、最終用戶和通路分類)

農藥市場:全球市場按產品類型、性質、作物類型、配方和應用進行預測 - 2026-2032年農藥儲槽市場:2026-2032年全球市場預測(依儲槽類型、材質、容量、運作模式、壓力類型、移動性、應用、最終用戶和通路分類) 農藥市場規模、佔有率、趨勢和預測:按肥料類型、農藥類型、作物類型和地區分類,2026-2034年

農藥市場規模、佔有率、趨勢和預測:按肥料類型、農藥類型、作物類型和地區分類,2026-2034年 農藥市場:依產地、產品類型、作物類型、應用及地區分類

農藥市場:依產地、產品類型、作物類型、應用及地區分類 農業化學品市場規模、佔有率和趨勢分析報告:按產品、應用、地區和細分市場分類的預測(2026-2033 年)

農業化學品市場規模、佔有率和趨勢分析報告:按產品、應用、地區和細分市場分類的預測(2026-2033 年) 全球農業化學品儲罐市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球農業化學品儲罐市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 2026年全球農藥市場報告氟嘧啶市場:2026-2032年全球市場預測(按劑型、作物類型、施用方法、分銷管道和最終用戶分類)

2026年全球農藥市場報告氟嘧啶市場:2026-2032年全球市場預測(按劑型、作物類型、施用方法、分銷管道和最終用戶分類) 銅肥市場規模、佔有率和成長分析:按產品類型、配方類型、應用類型、最終用戶和地區分類 - 2026-2033 年產業預測

銅肥市場規模、佔有率和成長分析:按產品類型、配方類型、應用類型、最終用戶和地區分類 - 2026-2033 年產業預測 作物保護市場分析及預測(至2035年):依類型、產品類型、應用、技術、形式、最終用戶、服務、實施類型、功能及解決方案分類

作物保護市場分析及預測(至2035年):依類型、產品類型、應用、技術、形式、最終用戶、服務、實施類型、功能及解決方案分類