|

市場調查報告書

商品編碼

2063897

自動化需量反應管理系統:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)Automated Demand Response Management System - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

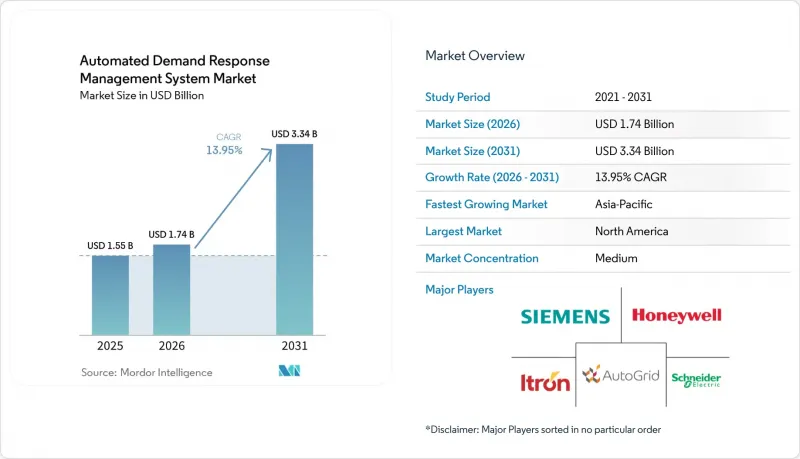

根據 Mordor Intelligence 預測,自動化需量反應管理系統市場規模將從 2025 年的 15.5 億美元和 2026 年的 17.4 億美元成長到 2031 年的 33.4 億美元,2026 年至 2031 年的年複合成長率(CAGR)為 13.95%。

本報告按解決方案(自動化災難復原管理和分析平台等)、通訊技術(有線等)、部署模式(本地部署、雲端部署)、最終用戶產業(住宅等)以及地區(北美、歐洲、亞太、南美、中東和非洲)進行細分。市場預測以美元計價。

全球自動化需量反應管理系統市場趨勢及洞察

動態電價的推廣

分時電價和即時電價意味著客戶更容易受到批發價格波動的影響,促使企業在用電高峰時段自動降低用電量。南加州愛迪生公司2024年的軟性定價試點計畫證明了大規模自動化預冷恆溫器的可行性,參與家庭的電費因此降低了12%。紐西蘭2025年的電價改革要求所有零售商在2027年前提供動態定價選項,以促進商業場所冷氣和暖通空調負載的轉變。英國的「敏捷」計畫在2024-2025年進行的電網服務檢查中,夜間用電需求下降了9%,這表明快速響應和透明收費系統相結合的方法行之有效。聚合商正在採用基於機器學習的定價預測來預測需求高峰,進一步提高客戶的節能效果和參與率。

全國部署先進計量基礎設施(AMI)

預計到2024年,美國智慧電錶普及率將達到88%,高於2019年的50%。智慧電錶將為電力公司提供五分鐘間隔的價格訊號和負載檢驗所需的間隔資料。聯合愛迪生公司在紐約市的部署已使雙向通訊普及率達到98%,為依賴安全韌體更新的住宅專案鋪平了道路。歐盟智慧電錶指令和中國國家電網的強制升級也在推動類似的升級,但由於資金投資的限制,地方合作社和地方政府公共產業進展緩慢。高解析度數據使人工智慧模型能夠分解家用電器的負載並最佳化調度,這是以往每月抄表數據無法實現的。

雙向災害應變 (DR) 通訊中的網路安全漏洞

NIST IR 8473 列出了 37 種可能導致電力傳輸訊號劫持和用電資料外洩的攻擊場景,促使電力公司要求採用基於憑證的身份驗證和設備級異常檢測。國際能源總署 (IEA) 的數據顯示,2024 年能源領域的網路安全事件增加了 25%,其中一些事件的目標是需量反應(DR) 平台。 IEEE 的一項研究發現,62% 的部署仍然缺乏完整的端對端加密,這導致穿透測試的要求越來越高,採購流程中也需要加入資料外洩保險條款。

細分市場分析

到2025年,隨著公用事業公司將自動化需量反應管理和分析平台與現有SCADA系統整合,這些平台將佔總收入的41.4%。隨著公用事業公司將ISO(獨立系統營運商)調度、訂閱和結算業務外包給第三方專業公司,預計到2031年,服務領域自動化需量反應管理系統的市場規模將以15.3%的複合年成長率成長。託管服務供應商透過聯合整合恆溫器、電池和電動車充電器等設備,在降低每個終端成本的同時,也承擔效能風險。像EnergyHub收購後的產品組合這樣的承包服務,目前已覆蓋超過250萬個分散式能源(DER),這是大多數公共產業內部無法實現的規模。

服務業的成長也反映出監管機構對公平結果的要求。專案管理者正利用聚合商的客服中心和數位入口網站快速招募弱勢群體。儘管垂直整合的公共產業仍在探索自身的分散式能源資源管理系統(DERMS)以防止收入流失,但與之競爭的零售供應商更傾向於與市場清算價格掛鉤的績效合約。因此,平台供應商正將諮詢、整合和結算服務打包成綜合訂閱服務。

儘管無線網狀網路在2025年將佔據42.8%的部署佔有率,但隨著公共產業更傾向於選擇符合AMI安全要求的通訊業者網路,蜂窩協議預計將以17.4%的複合年成長率成長。蜂窩自動化需量反應管理系統(DERMS)的市場佔有率得益於基於SIM卡的金鑰配置,該配置無需部署昂貴的閘道器即可滿足CPUC的加密規則。 NB-IoT模組價格低於5美元,電池壽命超過10年,使得每個住宅終端的月均成本低於2美元,這對於大規模部署至關重要。

根據《感測器研究》雜誌的報導,LoRa混合系統已實現94%的資料包投遞率,但在與收費後端整合方面仍面臨挑戰。同時,在PRIME標準已相當成熟的歐洲,電力線通訊(PLC)仍是一個小眾市場。由於延遲限制,高價值的頻率控制仍由有線乙太網路和光纖提供,而5分鐘調度服務則由蜂巢終端處理。因此,公共產業正在採用分層架構,將本地高速環路與透過LTE-M提供的雲端分析結合。

區域分析

北美地區預計到2025年將佔全球收入的47.1%,並擁有最完善的集中式和分散式能源(DER)法規結構。加州已在2025年至2027年間撥款超過2億美元用於需量反應(DR),目標是新增1吉瓦的彈性容量,並強制要求60%的參與者來自服務不足的地區。 ERCOT在2024年註冊了3200兆瓦的經濟型需量反應容量,但由於擔心多日熱浪期間的備用電源問題,住宅部門的貢獻仍低於10%。加拿大安大略省獨立系統營運商(Ontario ISO)已向需量反應資源開放了2024年的容量競標,墨西哥在蒙特雷啟動了分時電價試點項目,這表明需量反應模式預計將在美國以外的整個大陸範圍內推廣。

亞太地區是成長最快的地區,預計複合年成長率將達到16.7%。中國的國家虛擬電廠(VPP)計畫在初夏運作期間將調整發電量超過1兆瓦,並計畫在2030年推廣至全國,目前正獲得政府支持。印度中央電力局計畫在2030年新增27吉瓦的電池儲能容量和20吉瓦的抽水蓄能容量。 AutoGrid與PTC India的合作將利用人工智慧編配,整合靈活的暖氣、通風和空調(HVAC)以及電動車(EV)負載。日本已取消其供需調整市場的最低競標規模限制,將住宅用電容量納入其中。同時,韓國和東協正在進行工業需量反應試點項目,採用固定固定費率機制,並計劃在2028年過渡到動態定價模式。

在歐洲,一項名為「需量反應網路規範」的草案旨在2027年實現遙測技術的標準化。然而,由於補償門檻的差異,跨境聚合仍然十分複雜。在英國,「敏捷定價」政策使2024年至2025年間晚間高峰用電需求降低了9%。德國將頻率維持的最低競標要求從1兆瓦降至100千瓦,使聚合電池儲能得以參與。北歐國家正利用其超過95%的智慧電錶普及率,將熱泵運作與風力發電預測連結起來。相較之下,南歐和東歐由於高級計量基礎設施(AMI)部署有限而面臨挑戰,塞爾維亞和黑山的部署率均低於20%。儘管戰時電網面臨諸多挑戰,烏克蘭仍已向六家儲能聚合商發放了許可證。

其他好處

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 動態電價的推廣

- 全國部署先進計量基礎設施(AMI)

- 分散式能源(DER)與微電網的整合需要即時柔軟性。

- 電力公司正在推動降低尖峰負載,以避免昂貴的容量升級。

- 透過人工智慧驅動的預測性負荷分析提高需量反應項目的投資報酬率

- 擴展基於區塊鏈的交易能源試點項目

- 市場限制因素

- 雙向災難復原通訊中的網路安全漏洞

- 各州和地區有不同的監管要求

- 過多的事件通知會導致客戶疲勞和選擇退出的風險。

- 缺乏開放的、廠商中立的ADRMS標準

- 供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

第5章 市場規模與成長預測

- 透過解決方案

- 自動化災難復原管理與分析平台

- DR 控制和整合軟體

- 客戶註冊和互動門戶

- 服務(諮詢、整合、託管災難復原)

- 透過通訊技術

- 有線(PLC、乙太網路)

- 無線(Wi-Sun、ZigBee、RF Mesh)

- 蜂窩網路(LTE-M、NB-IoT、5G)

- 按部署模式

- 現場

- 基於雲端的

- 按最終用戶行業分類

- 住宅

- 商業

- 產業

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 北歐國家

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- ASEAN

- 其他亞太國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

- 埃及

- 其他中東和非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢(併購、聯盟、購電協議)

- 市場佔有率分析(主要公司的市場排名和佔有率)

- 公司簡介

- ABB Ltd

- AutoGrid Systems Inc.

- C3.ai Inc.

- Cisco Systems Inc.

- Eaton Corporation plc

- Enel X Srl

- General Electric Company

- Hitachi Energy Ltd.

- Honeywell International Inc.

- Itron Inc.

- Johnson Controls International plc

- Landis+Gyr Group AG

- Mitsubishi Electric Corporation

- Oracle Corporation

- Schneider Electric SE

- Siemens AG

- Tata Power DDL

- Tendril(Uplight)

- Virtual Peaker Inc.

- Yokogawa Electric Corporation

第7章 市場機會與未來展望

According to Mordor Intelligence, the automated demand response management system market size is projected to expand from USD 1.55 billion in 2025 and USD 1.74 billion in 2026 to USD 3.34 billion by 2031, registering a CAGR of 13.95% between 2026 to 2031.

This report is Segmented by Solution (Automated DR Management and Analytics Platforms, and More), Communication Technology (Wired, and More), Deployment Model (On-Premise, Cloud-Based), End-User Industry (Residential, and More), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Automated Demand Response Management System Market Trends and Insights

Proliferation of Dynamic Electricity Tariffs

Time-of-use and real-time pricing are exposing customers to wholesale volatility, rewarding automated curtailment during peak periods. Southern California Edison's 2024 Flexible Pricing Pilot cut enrolled household bills by 12% and proved that pre-cooling thermostats can be automated at scale . New Zealand's 2025 tariff reforms require every retailer to offer a dynamic option by 2027, pushing commercial portfolios to shift refrigeration and HVAC loads . The United Kingdom's Agile program saw a 9% drop in evening demand during 2024-2025 grid-service trials, validating the role of fast dispatch paired with transparent tariffs. Aggregators embed machine-learning price forecasts to anticipate spikes, which further increases customer savings and enrollment.

Nationwide Roll-out of Advanced Metering Infrastructure (AMI)

Smart-meter penetration in the United States reached 88% in 2024, up from 50% in 2019, giving utilities the interval data needed for five-minute price signals and load verification. Consolidated Edison's rollout across New York achieved 98% two-way communication, clearing the path for residential programs that rely on secure firmware updates. The EU smart-meter directive and China's State Grid mandate are driving similar upgrades, although rural cooperatives and municipal utilities lag due to capex constraints. High-resolution data lets AI models disaggregate appliance loads and fine-tune dispatch, which was impossible under monthly reads.

Cyber-security Vulnerabilities in Two-way DR Communications

NIST IR 8473 cataloged 37 attack scenarios that could hijack dispatch signals or exfiltrate usage data, prompting utilities to demand certificate-based authentication and device-level anomaly detection . The International Energy Agency reported a 25% increase in energy-sector cyber incidents in 2024, several of which targeted demand-response platforms. IEEE surveys found 62% of installations still lack full end-to-end encryption, pushing procurement cycles to include mandatory penetration testing and breach-insurance clauses.

Other drivers and restraints analyzed in the detailed report include:

- Integration of DERs and Micro-grids Requiring Real-Time Flexibility

- AI-enabled Predictive Load Analytics Improving DR Program ROI

- Fragmented Regulatory Mandates Across States and Regions

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, Automated DR Management & Analytics Platforms accounted for 41.4% of revenue as utilities integrated with existing SCADA. The Automated Demand Response Management System market size for Services is projected to expand at a 15.3% CAGR to 2031 as utilities shift ISO scheduling, enrollment, and settlement tasks to third-party specialists. Managed-service vendors pool device integration across thermostats, batteries, and EV chargers, lowering per-endpoint cost while assuming performance risk. Turnkey offerings like EnergyHub's post-acquisition portfolio now cover over 2.5 million DERs, a scale most utilities cannot match internally.

Services growth also reflects regulatory pressure to deliver equity outcomes; program administrators leverage aggregator call centers and digital portals to recruit disadvantaged communities quickly. Vertically integrated utilities still explore proprietary DERMS to avoid revenue leakage, but competitive retail suppliers prefer performance-based contracts tied to market clearing prices. As a result, platform vendors are bundling consulting, integration, and settlement into unified subscriptions.

Wireless mesh held 42.8% of 2025 deployments, yet cellular protocols are forecast to grow at 17.4% CAGR as utilities favor carrier networks that meet AMI security mandates. Automated Demand Response Management System market share for cellular is bolstered by SIM-based key provisioning that satisfies CPUC encryption rules without costly gateway rollouts. NB-IoT's sub-USD 5 modules and decade-long battery life bring residential per-endpoint costs below USD 2 monthly, critical for mass enrollment.

Studies in Sensors showed 94% packet delivery for LoRa hybrids but flagged integration gaps with billing back-ends, while PLC remains niche in Europe where PRIME standards persist. Latency constraints channel high-value frequency regulation to wired Ethernet or fiber, leaving 5-minute dispatch services to cellular endpoints. Utilities are therefore adopting tiered architectures that combine on-premise fast loops with cloud analytics delivered via LTE-M.

Geography Analysis

North America accounted for 47.1% of 2025 revenue and hosts the most sophisticated regulatory framework for aggregated DERs. California budgeted over USD 200 million for demand response between 2025 and 2027, targeting 1 GW of new flexible capacity while mandating that 60% of participants come from disadvantaged communities. ERCOT registered 3,200 MW of economic DR capacity in 2024, yet residential contributions remain below 10% due to backup-power concerns during multi-day heat waves. Canada's Ontario ISO opened its 2024 capacity auction to DR resources, and Mexico launched time-of-use pilots in Monterrey, signaling continental expansion beyond the United States.

Asia-Pacific is the fastest growing region, with a forecast CAGR of 16.7%. China's national virtual-power-plant program dispatched more than 1 MW during its first summer and has state backing to scale nationwide by 2030. India's Central Electricity Authority calls for 27 GW of battery storage and 20 GW of pumped hydro by 2030; AutoGrid's partnership with PTC India will use AI orchestration to aggregate flexible HVAC and EV loads. Japan dropped minimum bid sizes in balancing markets to include residential capacity, while South Korea and ASEAN economies are piloting industrial DR under flat tariffs that may evolve into dynamic pricing by 2028.

In Europe, the draft Network Code on Demand Response aims to standardize telemetry by 2027. However, variations in compensation floors continue to complicate cross-border aggregation. In the United Kingdom, the Agile tariff reduced evening peak demand by 9% during 2024-2025. Germany has lowered its minimum frequency-containment bid requirement from 1 MW to 100 kW, enabling the participation of aggregated batteries. Nordic countries utilize over 95% smart-meter penetration to synchronize heat-pump dispatch with wind energy forecasts. In contrast, Southern and Eastern Europe face challenges due to limited advanced metering infrastructure (AMI) deployment, with Serbia and Montenegro reporting rollout rates below 20%. Despite wartime grid challenges, Ukraine has licensed six storage aggregators.

- ABB Ltd

- AutoGrid Systems Inc.

- C3.ai Inc.

- Cisco Systems Inc.

- Eaton Corporation plc

- Enel X S.r.l.

- General Electric Company

- Hitachi Energy Ltd.

- Honeywell International Inc.

- Itron Inc.

- Johnson Controls International plc

- Landis+Gyr Group AG

- Mitsubishi Electric Corporation

- Oracle Corporation

- Schneider Electric SE

- Siemens AG

- Tata Power DDL

- Tendril (Uplight)

- Virtual Peaker Inc.

- Yokogawa Electric Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Proliferation of dynamic electricity tariffs

- 4.2.2 Nationwide roll-out of advanced metering infrastructure (AMI)

- 4.2.3 Integration of DERs & micro-grids requiring real-time flexibility

- 4.2.4 Utility push for peak-load shaving to avoid costly capacity additions

- 4.2.5 AI-enabled predictive load analytics improving DR program ROI

- 4.2.6 Growth of transactive energy pilots leveraging blockchain

- 4.3 Market Restraints

- 4.3.1 Cyber-security vulnerabilities in two-way DR communications

- 4.3.2 Fragmented regulatory mandates across states & regions

- 4.3.3 Customer fatigue & opt-out risk due to event over-notification

- 4.3.4 Scarcity of open, vendor-agnostic ADRMS standards

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Solution

- 5.1.1 Automated DR Management and Analytics Platforms

- 5.1.2 DR Control and Aggregation Software

- 5.1.3 Customer Enrollment and Engagement Portals

- 5.1.4 Services (Consulting, Integration, Managed DR)

- 5.2 By Communication Technology

- 5.2.1 Wired (PLC, Ethernet)

- 5.2.2 Wireless (Wi-Sun, ZigBee, RF Mesh)

- 5.2.3 Cellular (LTE-M, NB-IoT, 5G)

- 5.3 By Deployment Model

- 5.3.1 On-premise

- 5.3.2 Cloud-based

- 5.4 By End-user Industry

- 5.4.1 Residential

- 5.4.2 Commercial

- 5.4.3 Industrial

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 NORDIC Countries

- 5.5.2.6 Russia

- 5.5.2.7 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 ASEAN Countries

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 South Africa

- 5.5.5.4 Egypt

- 5.5.5.5 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 ABB Ltd

- 6.4.2 AutoGrid Systems Inc.

- 6.4.3 C3.ai Inc.

- 6.4.4 Cisco Systems Inc.

- 6.4.5 Eaton Corporation plc

- 6.4.6 Enel X S.r.l.

- 6.4.7 General Electric Company

- 6.4.8 Hitachi Energy Ltd.

- 6.4.9 Honeywell International Inc.

- 6.4.10 Itron Inc.

- 6.4.11 Johnson Controls International plc

- 6.4.12 Landis+Gyr Group AG

- 6.4.13 Mitsubishi Electric Corporation

- 6.4.14 Oracle Corporation

- 6.4.15 Schneider Electric SE

- 6.4.16 Siemens AG

- 6.4.17 Tata Power DDL

- 6.4.18 Tendril (Uplight)

- 6.4.19 Virtual Peaker Inc.

- 6.4.20 Yokogawa Electric Corporation

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment

全球需量反應市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球需量反應市場規模、佔有率、趨勢和成長分析報告(2026-2034) 自動需量反應(Auto:DR) 市場預測至 2034 年-按電力公司類型、專案類型、部署模式、技術、最終用戶和地區分類的全球分析需量反應市場預測至2034年—按專案類型、部署模式、技術、最終用戶和地區分類的全球分析

自動需量反應(Auto:DR) 市場預測至 2034 年-按電力公司類型、專案類型、部署模式、技術、最終用戶和地區分類的全球分析需量反應市場預測至2034年—按專案類型、部署模式、技術、最終用戶和地區分類的全球分析 需量反應管理系統市場:按組件、類型、通訊技術、程序類型、應用和最終用戶分類-2026-2032年全球市場預測需量反應和負載管理解決方案市場預測——按解決方案類型、技術、應用、最終用戶和地區分類的全球分析——2034年

需量反應管理系統市場:按組件、類型、通訊技術、程序類型、應用和最終用戶分類-2026-2032年全球市場預測需量反應和負載管理解決方案市場預測——按解決方案類型、技術、應用、最終用戶和地區分類的全球分析——2034年 需量反應市場機會、成長要素、產業趨勢分析及2026-2035年預測。

需量反應市場機會、成長要素、產業趨勢分析及2026-2035年預測。 亞太地區需量反應管理系統:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)

亞太地區需量反應管理系統:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年) 2026年全球分散式能源資源(DER)安全合規市場報告2026年全球需量反應(DR)市場報告2026年全球需量反應管理系統市場報告

2026年全球分散式能源資源(DER)安全合規市場報告2026年全球需量反應(DR)市場報告2026年全球需量反應管理系統市場報告