|

市場調查報告書

商品編碼

2063889

英國電動車充電基礎設施:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)United Kingdom Electric Vehicle Charging Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

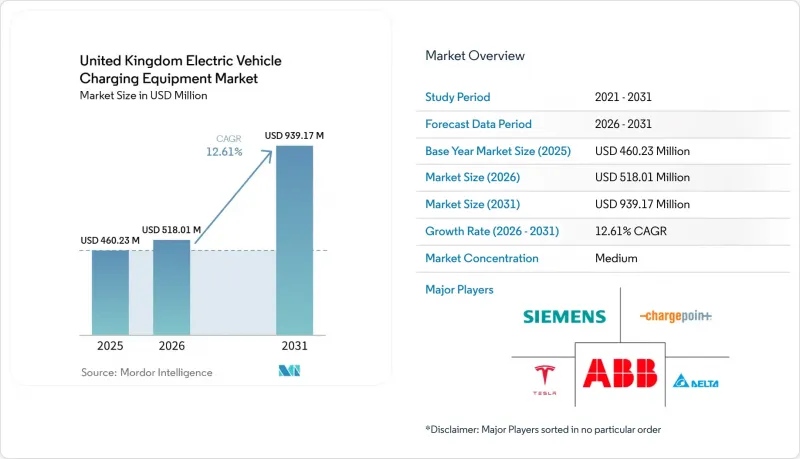

根據 Mordor Intelligence 預測,英國電動車充電基礎設施市場規模將從 2025 年的 4.6023 億美元成長到 2026 年的 5.1801 億美元,到 2031 年將達到 9.3917 億美元,2026 年至 2031 年的複合年成長率為 12.61%。

本報告按充電等級(1級、2級、直流快充、超快充、兆瓦級)、安裝地點(住宅、商業/零售設施、公共/市政設施、交通樞紐)和應用領域(家庭、職場、城市公共區域、高速公路/運輸途中、車隊和倉庫)進行細分。市場規模和預測均以美元計價。

英國電動車充電基礎設施市場趨勢與洞察

電動車普及及零排放汽車強制實施時間表

強制銷售零排放車輛 (ZEV) 的規定要求,到 2025 年,新車中 28% 必須為零排放車輛,到 2030 年這一比例必須達到 80%。歷史上,電池式電動車普及率每提高 1%,公共充電站的數量就會在 18 個月內激增 1.4 倍,從而推動了基礎設施需求的成長。汽車製造商每銷售一輛不合規車輛將面臨 15,000 英鎊的罰款,這促使家用充電樁與新車捆綁銷售。蘇格蘭先前設定的 2030 年分階段淘汰舊車的目標,使得 2024 年 ChargePlace 充電樁的安裝量比前一年成長了 22%。該規定中的靈活積分機制允許製造商累積零排放車輛的剩餘銷售額,導致充電樁安裝量的年度成長不平衡。因此,製造商正與充電樁營運商合作,根據車輛交付量調整充電能力,以平衡供應鏈的需求高峰。

OZEV補貼和稅收優惠

零排放車輛管理局 (OZEV) 為每個住宅充電樁提供高達 350 英鎊的津貼,並承擔高達 15,000 英鎊的職場充電樁成本的 75%。這使得職場硬體的投資回收期從 4.2 年縮短至 2.8 年(到 2024 年)。該公司車輛的實體稅率在 2% 的基礎上繼續維持在電池式電動車(BEV) 的 2%,直至 2025 年,這刺激了企業需求,去年企業用車佔新電動車註冊量的 54%。然而,這項津貼不包括擁有私人車道的獨棟住宅業主,導致公共資金集中在多用戶住宅,並加劇了都市區差距。工資扣除進一步提高了經濟效益,每年可為雇主節省每輛車約 4,800 英鎊。雖然這些獎勵共同促進了電動車的普及,但其實施往往集中在人口稠密的地區。

高昂的安裝成本和併網費用

在都市區安裝快速充電樁的成本在 4 萬至 8 萬英鎊之間。這是因為 50% 至 60% 的預算用於電網維修。超快速充電樁的成本則高達 18 萬英鎊,因為它們需要配電運營商 (DNO) 指定的專用 11 千伏饋送電纜和變壓器。土木工程費用為 1.5 萬至 4 萬英鎊,但在威斯敏斯特等歷史中心,密集的地下管道網路使挖溝作業變得複雜。住宅單元的安裝成本為 800 至 1500 英鎊,但多用戶住宅需要安裝成本為 3000 至 8000 英鎊的負載管理系統,而由此帶來的節能效果有限。這些經濟因素限制了私人投資在交通流量低的地區,因此充電樁的安裝往往集中在交通繁忙的高速公路沿線。

細分市場分析

預計到2031年,功率超過350千瓦的兆瓦級充電樁將以24.9%的複合年成長率成長。 ZEHID計畫將為重型車輛停車場和高速公路樞紐提供資金,使500千瓦時的卡車能夠在30分鐘內完成充電。到2025年,二級充電樁的安裝量將佔總安裝量的51.30%,這主要得益於120萬戶家庭用戶利用「智慧八爪魚Go」計畫提供的夜間7便士優惠電價。 50千瓦至150千瓦的直流快速充電樁在高速公路服務區佔據主導地位,在主要安裝點,每天的使用量超過20次,同時兼顧了處理能力和連接成本。超快速充電樁集中在M25和M6高速公路沿線,特斯拉和Ionity已在這些路段建立了長程走廊充電樞紐。一級充電樁的安裝量佔比不到2%,因為其12小時的充電時間不足以滿足現代60度電池組的需求。

支援3C充電倍率的電池化學成分正在推動高功率充電技術的普及。此外,自2024年起,公開競標中強制要求符合IEC 61851標準,這將加速現有業者的設備升級週期。二級充電的未來成長取決於由LEVI資助的路燈升級項目,該項目將為40%缺乏專用停車位的多用戶住宅提供5.5kW的充電容量。模組化功率堆設計使營運商能夠在利用率提高時無需完全更換充電櫃即可將功率從75kW升級到150kW,從而確保良好的投資回報率(ROI)。超快速充電站正在增加零售合作夥伴的數量,他們透過20分鐘的充電服務來獲利,每次使用可產生4-6英鎊的額外收入。這些趨勢共同促成了英國電動車充電基礎設施市場多層次的功率組合。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 電動車推廣計劃及零排放汽車強制實施計劃

- OZEV補貼和稅收優惠

- 公共資金(LEVI 和快速充電基金)

- 企業車輛電氣化目標

- 動態定價機制能夠實現盈利的智慧充電。

- 二次利用電池,整合充電器

- 市場限制因素

- 安裝和併網成本高昂

- 電力電子供應鏈的限制因素

- 都市區變電站的配電網路營運商等待時間

- 支付系統中的互通性差距

- 供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

- PESTLE分析

- 投資分析

第5章 市場規模與成長預測

- 按充電等級

- 1 級(3 千瓦或以下)

- 2級(3-50千瓦)

- 直流快速充電(50-150千瓦)

- 超快速充電(150-350千瓦)

- 兆瓦級(350千瓦或以上)

- 按安裝位置

- 住宅

- 商業和零售

- 公共/市政

- 交通樞紐(機場、港口)

- 透過使用

- 家用充電

- 職場中充電

- 都市區的公共充電站

- 高速公路/行駛中快速充電

- 車輛和車輛停放場的充電

第6章 競爭情勢

- 市場集中度

- 策略趨勢(併購、聯盟、購電協議)

- 市場佔有率分析(主要公司的市場排名和市場佔有率)

- 公司簡介

- BP Pulse(BP plc)

- Pod Point Group Holdings plc

- InstaVolt Ltd

- Shell Recharge Solutions(Shell plc)

- Osprey Charging Network Ltd

- Gridserve Sustainable Energy Ltd

- Tesla Inc.

- ABB Ltd

- Siemens AG

- ChargePoint Holdings Inc.

- Schneider Electric SE

- Eaton Corporation plc

- Delta Electronics Inc.

- EO Charging

- Rolec Services Ltd

- Wallbox NV

- Robert Bosch GmbH

- Alfen NV

- Fastned BV

- Zaptec ASA

第7章 市場機會與未來展望

According to Mordor Intelligence, the united kingdom electric vehicle charging equipment market size is expected to grow from USD 460.23 million in 2025 to USD 518.01 million in 2026 and is forecast to reach USD 939.17 million by 2031 at 12.61% CAGR over 2026-2031.

This report is Segmented by Charging Level (Level 1, Level 2, DC Fast, Ultra-Fast, and Megawatt Class), Installation Site (Residential, Commercial and Retail, Public Municipal, and Transportation Hubs), and Application (Home, Workplace, Public Urban, Highway Corridor/En-Route, and Fleet and Depot). The Market Sizes and Forecasts are Provided in Terms of Value (USD).

United Kingdom Electric Vehicle Charging Equipment Market Trends and Insights

EV Adoption and ZEV Mandate Timelines

The Zero Emission Vehicle sales mandate requires 28% of new cars to be zero-emission by 2025, and 80% by 2030, escalating infrastructure demand as every percentage point rise in battery-electric penetration historically drives a 1.4-fold jump in public chargepoints within 18 months . Automakers face GBP 15,000 fines per non-compliant vehicle, prompting bundled home-charger offers with new EV sales. Scotland's earlier 2030 phase-out target triggered a 22% annual rise in ChargePlace installations in 2024. The mandate's flex-credit mechanism lets manufacturers bank surplus ZEV sales, creating uneven yearly installation spikes. Manufacturers, therefore, collaborate with charge-point operators to ensure capacity scales with vehicle deliveries, smoothing supply chain peaks .

OZEV Grants and Tax Incentives

The Office for Zero Emission Vehicles offers up to GBP 350 per residential chargepoint and covers 75% of workplace-charger costs to GBP 15,000, cutting the payback period on workplace hardware from 4.2 years to 2.8 years in 2024. Company-car benefit-in-kind rates remain at 2% for battery electrics through 2025, boosting corporate demand that comprised 54% of new EV registrations last year. Yet the grant excludes detached-home owners with private driveways, concentrating public funds in multi-unit dwellings and widening a rural-urban gap. Salary-sacrifice schemes further tip economics, saving employers nearly GBP 4,800 annually per vehicle. Combined, these incentives accelerate uptake but skew deployment toward high-density postcodes.

High Installation and Grid-Connection CAPEX

Rapid chargers cost GBP 40,000-80,000 installed in urban zones because grid upgrades absorb 50%-60% of budgets. Ultra-fast units climb to GBP 180,000 due to dedicated 11 kV feeds and DNO-mandated transformers . Civil works add GBP 15,000-40,000, where congested utilities complicate trenching in historic centers such as Westminster. Residential units cost GBP 800-1,500, but multi-unit dwellings need GBP 3,000-8,000 load-management systems that grant only partial offset. These economics deter private investment in lower-traffic areas, skewing installations toward motorway corridors with higher utilization.

Other drivers and restraints analyzed in the detailed report include:

- Public-Sector Funding (LEVI and Rapid Charging Fund)

- Corporate Fleet Electrification Targets

- Power-Electronics Supply-Chain Constraints

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Megawatt-class chargers exceeding 350 kW will expand at a 24.9% CAGR through 2031 as the ZEHID program funds heavy-duty depots and motorway hubs, enabling 500 kWh trucks to recharge in under 30 minutes. Level 2 hardware accounted for 51.30% of 2025 deployments, driven by 1.2 million home units utilizing 7 pence night rates under Intelligent Octopus Go. DC fast units between 50 kW and 150 kW dominate motorway services, balancing throughput with connection costs and hitting 20-plus daily sessions at prime sites. Ultra-fast chargers cluster along the M25 and M6 where Tesla and Ionity anchor long-distance corridors. Level 1 sockets now account for under 2% of new installs because 12-hour charge times cannot match modern 60 kWh packs.

Battery chemistries accepting 3C charge rates promote higher-power adoption, and IEC 61851 compliance became mandatory in public tenders during 2024, driving refresh cycles among incumbents. Level 2's future growth depends on LEVI-funded lamppost conversions delivering 5.5 kW to apartment streets where 40% of households lack driveways. Modular power-stack designs let operators upgrade 75 kW cabinets to 150 kW as utilization rises without full replacement, protecting ROI. Ultra-fast hubs add retail partners that monetize 20-minute dwell times, earning GBP 4-6 ancillary spend per session. Together, these dynamics sustain a layered power portfolio within the United Kingdom electric vehicle charging equipment market.

List of Companies Covered in this Report:

- BP Pulse (BP plc)

- Pod Point Group Holdings plc

- InstaVolt Ltd

- Shell Recharge Solutions (Shell plc)

- Osprey Charging Network Ltd

- Gridserve Sustainable Energy Ltd

- Tesla Inc.

- ABB Ltd

- Siemens AG

- ChargePoint Holdings Inc.

- Schneider Electric SE

- Eaton Corporation plc

- Delta Electronics Inc.

- EO Charging

- Rolec Services Ltd

- Wallbox NV

- Robert Bosch GmbH

- Alfen NV

- Fastned BV

- Zaptec ASA

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 EV adoption & ZEV mandate timelines

- 4.2.2 OZEV grants & tax incentives

- 4.2.3 Public-sector funding (LEVI & Rapid Charging Fund)

- 4.2.4 Corporate fleet electrification targets

- 4.2.5 Dynamic tariffs enabling profitable smart charging

- 4.2.6 Second-life batteries integrated with chargers

- 4.3 Market Restraints

- 4.3.1 High installation & grid-connection CAPEX

- 4.3.2 Power-electronics supply-chain constraints

- 4.3.3 DNO queue delays at urban substations

- 4.3.4 Payment-system interoperability gaps

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 PESTLE Analysis

- 4.9 Investment Analysis

5 Market Size & Growth Forecasts

- 5.1 By Charging Level

- 5.1.1 Level 1 (Up to 3 kW)

- 5.1.2 Level 2 (3 to 50 kW)

- 5.1.3 DC Fast (50 to 150 kW)

- 5.1.4 Ultra-Fast (150 to 350 kW)

- 5.1.5 Megawatt Class (Above 350 kW)

- 5.2 By Installation Site

- 5.2.1 Residential

- 5.2.2 Commercial and Retail

- 5.2.3 Public Municipal

- 5.2.4 Transportation Hubs (Airports, Ports)

- 5.3 By Application

- 5.3.1 Home Charging

- 5.3.2 Workplace Charging

- 5.3.3 Public Urban Charging

- 5.3.4 Highway Corridor/En-Route Fast Charging

- 5.3.5 Fleet and Depot Charging

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 BP Pulse (BP plc)

- 6.4.2 Pod Point Group Holdings plc

- 6.4.3 InstaVolt Ltd

- 6.4.4 Shell Recharge Solutions (Shell plc)

- 6.4.5 Osprey Charging Network Ltd

- 6.4.6 Gridserve Sustainable Energy Ltd

- 6.4.7 Tesla Inc.

- 6.4.8 ABB Ltd

- 6.4.9 Siemens AG

- 6.4.10 ChargePoint Holdings Inc.

- 6.4.11 Schneider Electric SE

- 6.4.12 Eaton Corporation plc

- 6.4.13 Delta Electronics Inc.

- 6.4.14 EO Charging

- 6.4.15 Rolec Services Ltd

- 6.4.16 Wallbox NV

- 6.4.17 Robert Bosch GmbH

- 6.4.18 Alfen NV

- 6.4.19 Fastned BV

- 6.4.20 Zaptec ASA

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment

電動車公共充電網路市場預測至2034年:按充電樁類型、連接方式、位置、所有權/營運模式和區域分類的全球分析電動車充電機器人市場預測至2034年—按產品類型、充電技術、充電速度、應用、最終用戶和地區分類的全球分析下一代電動車充電網路市場預測:至2034年-全球分析(按充電器類型、輸出功率、連接器類型、車輛型號、安裝類型、連接方式、應用、最終用戶和地區分類)

電動車公共充電網路市場預測至2034年:按充電樁類型、連接方式、位置、所有權/營運模式和區域分類的全球分析電動車充電機器人市場預測至2034年—按產品類型、充電技術、充電速度、應用、最終用戶和地區分類的全球分析下一代電動車充電網路市場預測:至2034年-全球分析(按充電器類型、輸出功率、連接器類型、車輛型號、安裝類型、連接方式、應用、最終用戶和地區分類) 電動車充電站市場(含廣告看板):依廣告形式、充電器類型、安裝位置、網路類型和最終用戶分類,全球預測,2026-2032年電動車充電主動濾波器按充電站類型、濾波器配置、額定輸出功率和最終用戶分類,全球預測,2026-2032年電動車充電濾波器市場按濾波器類型、濾波器拓撲結構、額定電流、應用和最終用戶分類-全球預測,2026-2032年電動車智慧充電控制器市場:按充電等級、模式、通訊技術、交付方式、車輛類型、應用和最終用戶分類-2026-2032年全球預測

電動車充電站市場(含廣告看板):依廣告形式、充電器類型、安裝位置、網路類型和最終用戶分類,全球預測,2026-2032年電動車充電主動濾波器按充電站類型、濾波器配置、額定輸出功率和最終用戶分類,全球預測,2026-2032年電動車充電濾波器市場按濾波器類型、濾波器拓撲結構、額定電流、應用和最終用戶分類-全球預測,2026-2032年電動車智慧充電控制器市場:按充電等級、模式、通訊技術、交付方式、車輛類型、應用和最終用戶分類-2026-2032年全球預測 日本電動車充電設備市場佔有率分析、產業趨勢及統計、成長預測(2026-2031)

日本電動車充電設備市場佔有率分析、產業趨勢及統計、成長預測(2026-2031) 日本電動車充電設備市場規模、佔有率、趨勢及預測(按充電站、最終用途和地區分類,2026-2034年)電動汽車家用充電套件市場預測至2032年:按充電器類型、連接器類型、車輛類型、安裝類型、分銷管道、應用和地區分類的全球分析

日本電動車充電設備市場規模、佔有率、趨勢及預測(按充電站、最終用途和地區分類,2026-2034年)電動汽車家用充電套件市場預測至2032年:按充電器類型、連接器類型、車輛類型、安裝類型、分銷管道、應用和地區分類的全球分析