|

市場調查報告書

商品編碼

2063881

印度最後一公里配送:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)India Last Mile Delivery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

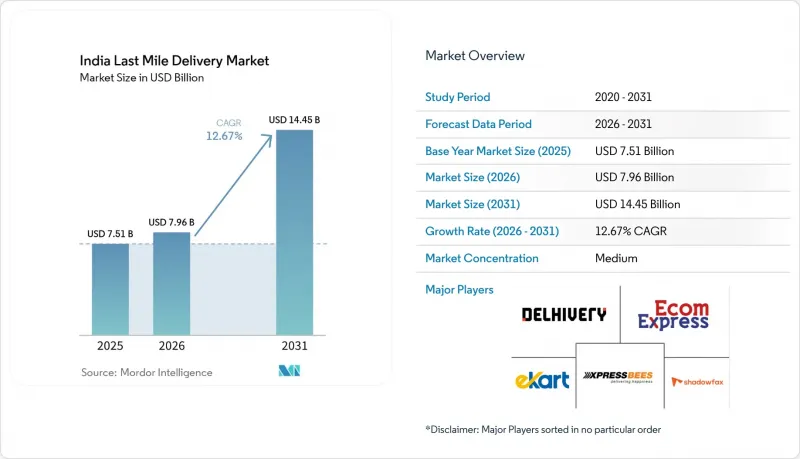

根據 Mordor Intelligence 預測,印度最後一公里配送市場規模將從 2025 年的 75.1 億美元和 2026 年的 79.6 億美元成長到 2031 年的 144.5 億美元,2026 年至 2031 年的複合年成長率為 12.67%。

本報告按服務類型(當日達、特快專遞、標準配送)、經營模式(B2B、B2C、C2C)、終端用戶行業(電商零售、時尚生活、美容、健康與個人護理、家居家具、家電等)以及地區(北部、中部、西部、東部、南部)進行細分。市場預測以美元計價。

印度最後一公里配送市場的趨勢與洞察

二、三線城市電子商務GMV爆炸性成長

預計到2025年,區域城市(二線和三線城市)的商品交易總額(GMV)將增加42%,顯著超過大都會圈的成長速度。這主要歸功於遍遠地區智慧型手機普及率超過61%,以及在地化應用程式降低了首次購物者的進入門檻。 Flipkart旗下的Ekart服務將其郵遞區號覆蓋範圍從19,000個擴大到23,500個,從而縮小了齋浦爾、勒克瑙和維沙卡帕特南兩日達的覆蓋範圍。同時,ElasticRun的Kirana網路模式在北方邦和比哈爾邦將最後一公里配送成本降低了30%。小包裹集中度的提高降低了對中心輻射式配送系統的依賴,從而可以開通直達貨車路線。然而,仍有40%的地址缺乏標準化的門牌號碼,導致每次停靠延誤8-12分鐘。因此,印度的末端配送市場正將重點轉向引入智慧引擎,以提高首次配送成功率。能夠解決本地地理編碼問題的承運商將能夠在需求成長最快的地區贏得客戶忠誠度。

快速交易和暗店的迅速擴張

隨著 Blinkit、Zepto 和 Swiggy Instamart 競相承諾 10-15 分鐘內送達,到 2026 年 3 月,暗店數量已達 1489 家,15 個月內成長了 67%。 Zepto 在 2025 年完成的 10 億美元資金籌措以及 Blinkit 被 Zomato 收購,進一步增強了投資者的信心,他們認為高訂單頻率可以彌補小規模訂單規模的不足。安德里和科拉曼加拉地區 35% 的房地產溢價凸顯了在地化位置的戰略價值。家電品類的拓展已將平均訂單價值提升至 485 盧比(5.13 美元),部分微型市場的利潤率也已轉正。印度食品安全與標準局 (FSSAI) 關於生鮮食品溫度記錄的草案可能會成為合規障礙,這將有利於擁有低溫運輸能力的平台。

大都會圈快速商業的飽和與價格競爭

截至2026年3月,孟買、新德里(NCR)和班加羅爾的線上雜貨購物滲透率超過38%,接近韓國的成熟水平,但獲客成本較去年同期上漲62%。 2025-2026會計年度的總現金消耗達320億盧比(33.86億美元),毛利率從上年的18%下降至11%。由於消費者越來越傾向於購買折扣商品,平均訂單價值降至440盧比(4.66美元),阻礙了品類擴大策略。競爭委員會已對涉嫌不公平定價展開調查,加劇了市場的不確定性。儘管各平台都在將業務轉移到人口密度較低、配送時間較短(20-30分鐘)的一線城市,但獲利能力仍難以預測。

細分市場分析

預計到2025年,標準配送將以58.19%的市佔率佔據印度末端配送市場的榜首,但到2031年,當日達配送的複合年成長率預計將達到14.32%,成為成長最快的配送方式。標準配送在2025年的主導地位得益於其適用於非生鮮產品品類,這類商品可承受3-5天的配送時間。而快遞則填補了時尚類訂單的空白,這類訂單對隔日達的需求至關重要,但高昂的費用又使得當日達難以實現。承運商正在投資人工智慧分類線,例如Delhivery位於班加羅爾的物流中心,該中心每天處理120萬個小包裹。這些變化將逐步推動印度末端配送市場朝向更快速的服務層級發展,同時又不會淘汰性價比高的標準配送服務。

如今,網路差異化取決於暗店密度和數據驅動的配送時段分配。亞馬遜的Prime Now在2025年完成了4,200萬次配送,維持了35%的溢價,印度消費者願意為此支付溢價以避免缺貨。 2025年假期季節期間,Blue Dart快遞在二線城市的配送量激增,凸顯了農村地區對可預測的次日達服務日益成長的需求。隨著人工智慧驅動的動態路線規劃日益普及,能夠在成本和速度之間取得最佳平衡的承運商將在印度的最後一公里配送市場中贏得更多佔有率。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 二、三線城市電子商務GMV爆炸性成長

- 快速交易和暗店的迅速擴張

- 國家物流政策與走廊發展

- 人工智慧驅動的配送路線最佳化和履約最佳化

- 電動摩托車共享服務釋放了大量的運輸能力。

- 簡化與ULIP開放API資料平台的合規流程

- 市場限制因素

- Metro QuickCommerce 市場飽和及價格戰

- 二層和三層資料RTO率高:地址品質差異

- 都市區交通擁擠和停車位短缺導致成本增加

- 由於電動車充電基礎設施不足和資金籌措。

- 法律規範

- 價值鍊和通路分析

- 技術創新前景

- 波特五力模型

- 關於倉庫和物流中心的考量

- 關於冷藏最後一公里配送的注意事項。

- 逆向/退貨物流洞察

- 地緣政治事件對供應鏈轉移的影響

第5章 市場規模及成長預測(價值,2026-2031 年)

- 按服務

- 當日送達

- 快遞

- 標準配送

- 按經營模式

- 企業對企業 (B2B) 交易

- Business-to-Consumer(B2C)

- 消費者對消費者(C2C)交易

- 按最終用戶行業分類

- 電子商務零售

- 時尚與生活風格

- 美容、健康、個人護理

- 住宅和家具

- 家用電子電器和家用電器

- 醫療保健和醫療用品

- 其他

- 按地區

- 北

- 中部

- 西方

- 東方

- 南

第6章 競爭情勢

- 市場集中度

- 關鍵策略趨勢

- 市佔率分析

- 公司簡介

- Delhivery

- Ecom Express

- Xpressbees

- Shadowfax

- Ekart Logistics

- Loadshare Networks

- ElasticRun

- Dunzo

- Borzo

- Porter

- Blue Dart Express

- DTDC Express

- Allcargo Gati

- Safexpress

- Mahindra Logistics

- TCI Express

- FedEx India

- DHL eCommerce

- Aramex India

- Amazon Transportation Services

- Reliance Retail Logistics

- India Post

第7章 市場機會與未來展望

According to Mordor Intelligence, the india last mile delivery market size is projected to expand from USD 7.51 billion in 2025 and USD 7.96 billion in 2026 to USD 14.45 billion by 2031, registering a CAGR of 12.67% between 2026 to 2031.

This report is Segmented by Service (Same-Day Delivery, Express Delivery, Standard Delivery), by Business Model (B2B, B2C, C2C), by End User Industry (E-Commerce Retail, Fashion and Lifestyle, Beauty, Wellness and Personal Care, Home and Furniture, Consumer Electronics and Appliances, and More), and by Region (North, Central, West, East, South). Market Forecasts are Provided in Terms of Value (USD).

India Last Mile Delivery Market Trends and Insights

Explosive E-Commerce GMV Surge in Tier-2/3 Cities

Tier-2 and Tier-3 GMV expanded by 42% in 2025, far outstripping metro growth, as smartphone penetration crossed 61% in rural areas and vernacular apps lowered entry barriers for first-time buyers. Flipkart's Ekart expanded its pin-code coverage from 19,000 to 23,500, compressing the two-day delivery coverage across Jaipur, Lucknow, and Visakhapatnam. At the same time, ElasticRun's kirana network model has reduced last-mile costs by 30% in Uttar Pradesh and Bihar. Parcel density now justifies direct truck routes, reducing reliance on hubs and spokes, though 40% of addresses still lack standardized building numbers, adding 8-12 minutes per stop. The Indian last-mile delivery market is therefore pivoting to adopt intelligent engines to improve first-attempt success rates. Carriers that crack rural geocoding will secure loyalty in the fastest-growing demand pockets.

Rapid Expansion of Quick-Commerce and Dark Stores

Dark-store count hit 1,489 by March 2026, up 67% in fifteen months as Blinkit, Zepto, and Swiggy Instamart raced to maintain 10-15-minute delivery promises. Funding inflows Zepto's USD 1 billion in 2025 and Blinkit's integration within Zomato underscore investor confidence that high order frequency offsets smaller baskets. Real estate premiums of 35% in Andheri and Koramangala highlight the strategic value of hyperlocal nodes. Category expansion into electronics lifted average order values to INR 485 (USD 5.13), pushing contribution margins positive in select micro-markets. Draft FSSAI norms on temperature logs for perishables are likely to create compliance hurdles, favoring platforms with cold-chain readiness.

Metro Quick-Commerce Saturation and Discount Wars

Penetration among online grocery shoppers crossed 38% in Mumbai, Delhi-NCR, and Bengaluru by March 2026, near maturity levels seen in South Korea, driving customer-acquisition costs up 62% year on year. The collective cash burn of INR 3,200 (USD 33.86) crore in FY 2025-26 slashed gross margins to 11%, down from 18% a year earlier. Average order values fell to INR 440 (USD 4.66) as consumers cherry-picked discount SKUs, undermining category-expansion strategies. The Competition Commission has opened a probe into alleged predatory pricing, stoking uncertainty. Platforms are pivoting toward Tier-1 cities where density is lower and delivery promises can stretch to 20-30 minutes, but the economics remain unproven.

Other drivers and restraints analyzed in the detailed report include:

- National Logistics Policy and Corridor Build-Out

- AI-Driven Routing and Fulfillment Optimization

- High RTO Rates from Tier-2/3 Address Quality Gaps

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Standard delivery led with 58.19% of the Indian last-mile delivery market share in 2025, while same-day delivery is projected to post the highest 14.32% CAGR through 2031. Standard delivery's 2025 lead rests on its suitability for non-perishable categories that tolerate 3-5-day windows. Express delivery bridges the gap for fashion orders where next-day delivery matters but premium fees deter same-day uptake. Carriers are channeling capex into AI sortation lines, such as Delhivery's Bengaluru gateway, which handles 1.2 million parcels daily. These shifts will gradually shift the India last-mile delivery market toward faster tiers without erasing the cost-efficient standard segment.

Network differentiation now hinges on dark-store density and data-driven slot-allocation. Amazon's Prime Now processed 42 million shipments in 2025, sustaining a 35% price premium that Indian consumers are willing to pay to avoid stockouts. Blue Dart's Tier-2 express surge during the 2025 festive season underscores the hinterland's appetite for a predictable next-day service. As AI-enabled dynamic routing proliferates, carriers that balance cost and speed will capture incremental market share in India's last-mile delivery market.

List of Companies Covered in this Report:

- Delhivery

- Ecom Express

- Xpressbees

- Shadowfax

- Ekart Logistics

- Loadshare Networks

- ElasticRun

- Dunzo

- Borzo

- Porter

- Blue Dart Express

- DTDC Express

- Allcargo Gati

- Safexpress

- Mahindra Logistics

- TCI Express

- FedEx India

- DHL eCommerce

- Aramex India

- Amazon Transportation Services

- Reliance Retail Logistics

- India Post

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Explosive E-Commerce GMV Surge in Tier-2/3 Cities

- 4.2.2 Rapid Expansion of Quick-Commerce and Dark Stores

- 4.2.3 National Logistics Policy and Corridor Build-Out

- 4.2.4 AI-Driven Routing and Fulfilment Optimization

- 4.2.5 Electric 2-Wheeler-as-a-Service Unlocking Gig Capacity

- 4.2.6 ULIP Open-API Data Platform Streamlining Compliance

- 4.3 Market Restraints

- 4.3.1 Metro Quick-Commerce Saturation and Discount Wars

- 4.3.2 High RTO Rates from Tier-2/3 Address Quality Gaps

- 4.3.3 Urban Congestion & Parking Shortages Inflating Costs

- 4.3.4 Sparse EV-Charging/Financing Slowing Green Fleets

- 4.4 Regulatory Framework

- 4.5 Value Chain and Distribution Channel Analysis

- 4.6 Technology Innovations Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Rivalry Among Competitors

- 4.8 Insights on Warehousing & Distribution Centers

- 4.9 Insights on Refrigerated Last-Mile Delivery

- 4.10 Reverse / Return Logistics Insights

- 4.11 Impact of Geo-Political Events on Supply Chain Shifts

5 Market Size & Growth Forecasts (Value, 2026-2031)

- 5.1 By Service

- 5.1.1 Same-day Delivery

- 5.1.2 Express Delivery

- 5.1.3 Standard Delivery

- 5.2 By Business Model

- 5.2.1 Business-to-Business (B2B)

- 5.2.2 Business-to-Consumer (B2C)

- 5.2.3 Customer-to-Consumer (C2C)

- 5.3 By End User Industry

- 5.3.1 E-commerce Retail

- 5.3.2 Fashion and Lifestyle

- 5.3.3 Beauty, Wellness and Personal Care

- 5.3.4 Home and Furniture

- 5.3.5 Consumer Electronics and Appliances

- 5.3.6 Healthcare and Medical Supplies

- 5.3.7 Others

- 5.4 By Region

- 5.4.1 North

- 5.4.2 Central

- 5.4.3 West

- 5.4.4 East

- 5.4.5 South

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Delhivery

- 6.4.2 Ecom Express

- 6.4.3 Xpressbees

- 6.4.4 Shadowfax

- 6.4.5 Ekart Logistics

- 6.4.6 Loadshare Networks

- 6.4.7 ElasticRun

- 6.4.8 Dunzo

- 6.4.9 Borzo

- 6.4.10 Porter

- 6.4.11 Blue Dart Express

- 6.4.12 DTDC Express

- 6.4.13 Allcargo Gati

- 6.4.14 Safexpress

- 6.4.15 Mahindra Logistics

- 6.4.16 TCI Express

- 6.4.17 FedEx India

- 6.4.18 DHL eCommerce

- 6.4.19 Aramex India

- 6.4.20 Amazon Transportation Services

- 6.4.21 Reliance Retail Logistics

- 6.4.22 India Post

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

2034年全球首末公里出行市場預測-按交通方式、動力系統、服務模式、預訂平台、應用、最終用戶和地區分類的全球分析

2034年全球首末公里出行市場預測-按交通方式、動力系統、服務模式、預訂平台、應用、最終用戶和地區分類的全球分析 最後一公里配送市場規模、佔有率和趨勢分析報告:按服務、技術、應用、地區和細分市場預測(2026-2033 年)2034年最後一公里低溫運輸配送市場預測-全球分析(依配送類型、車輛類型、溫度範圍、包裝類型、技術、應用、最終用戶和地區分類)電動最後一公里配送車輛市場規模、佔有率和趨勢分析報告:按車輛類型、負載容量、應用、地區和細分市場預測(2026-2033 年)全球最後一公里連結市場預測(至2034年)-按運輸方式、技術、最終用戶和地區分類的分析都市區最後一公里配送市場預測至2034年-按服務類型、配送方式、車輛類型、技術、目的地、應用和區域分類的全球分析

最後一公里配送市場規模、佔有率和趨勢分析報告:按服務、技術、應用、地區和細分市場預測(2026-2033 年)2034年最後一公里低溫運輸配送市場預測-全球分析(依配送類型、車輛類型、溫度範圍、包裝類型、技術、應用、最終用戶和地區分類)電動最後一公里配送車輛市場規模、佔有率和趨勢分析報告:按車輛類型、負載容量、應用、地區和細分市場預測(2026-2033 年)全球最後一公里連結市場預測(至2034年)-按運輸方式、技術、最終用戶和地區分類的分析都市區最後一公里配送市場預測至2034年-按服務類型、配送方式、車輛類型、技術、目的地、應用和區域分類的全球分析 末端配送軟體市場規模、佔有率和成長分析:按部署模式、應用、關鍵功能、企業規模、技術、銷售管道和地區分類-2026年至2033年產業預測

末端配送軟體市場規模、佔有率和成長分析:按部署模式、應用、關鍵功能、企業規模、技術、銷售管道和地區分類-2026年至2033年產業預測 2026年人工智慧驅動的最後一公里配送全球市場報告

2026年人工智慧驅動的最後一公里配送全球市場報告 自動駕駛最後一公里配送市場:依服務類型、推進方式、配送距離、組件和最終用戶產業分類-2026-2032年全球市場預測食品低溫運輸最後一公里配送市場:依運輸方式、服務類型、溫度區域、配送方式及最終用戶分類-2026-2032年全球市場預測

自動駕駛最後一公里配送市場:依服務類型、推進方式、配送距離、組件和最終用戶產業分類-2026-2032年全球市場預測食品低溫運輸最後一公里配送市場:依運輸方式、服務類型、溫度區域、配送方式及最終用戶分類-2026-2032年全球市場預測