|

市場調查報告書

商品編碼

2063406

電信資料貨幣化:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Telecom Data Monetization - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

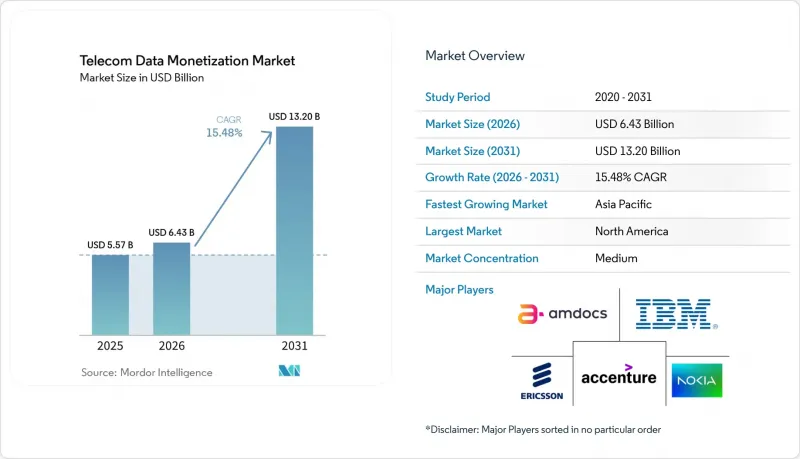

根據 Mordor Intelligence 預測,通訊資料貨幣化市場規模預計將在 2025 年達到 55.7 億美元,在 2026 年達到 64.3 億美元,並在 2031 年達到 132 億美元。

預計從 2026 年到 2031 年,其複合年成長率將達到 15.48%。

本報告按元件(平台和服務)、部署模式(雲端和本地部署)、應用程式(客戶體驗管理、網路管理等)、最終用戶(通訊業者、企業等)和地區進行細分。市場預測以美元計價。

全球電信數據貨幣化市場趨勢及洞察

5G網路帶來的數據量激增

目前,5G用戶產生的流量是 4G用戶的10 到 100 倍,為即時分析提供了前所未有的基礎。 Verizon 透露,到 2025 年,5G 用戶的平均月流量將達到 47GB,是 4G 用戶的兩倍多。 AT&T 的 Aduna API 平台正利用這一流量,在營運的第一年就創造了 1.8 億美元的額外收入。中國移動在其 5G 基地台邊緣節點上每月處理 3.2 Exabyte,從而支援低延遲的工業IoT合約。分析師估計,到 2028 年,邊緣運算帶來的收入流可望佔企業 5G 貨幣化的 40%。

雲端原生貨幣化平台的廣泛應用

雲端原生架構將獲利邏輯與傳統收費系統解耦,並將發布週期從季度縮短至每週。 Proximus 於 2025 年將整個 BSS 系統遷移到諾基亞的 AVA 雲端平台,營運成本降低了 22%,產品發布前置作業時間也大幅縮短至 14 天。 LotusFlare 的平台為Softbank Corporation和台灣大哥大提供了類似的敏捷性,將發佈時間縮短至不到兩週。 Salesforce 和 Amdoc 整合了其 CRM 和 AI 獲利引擎,實現了即時客戶體驗編配,並在六個月內使其淨推薦值 (NPS )提升了 23%。

嚴格的資料隱私和主權法規

自2024年以來,基於GDPR的罰款金額幾乎加倍,而對Meta公司處以12億歐元(14億美元)罰款的判決凸顯了跨境風險。 TikTok因兒童資料外洩被處以3.45億歐元(4.04億美元)的罰款,引發了全行業的審計。沃達豐斥資1.2億英鎊(1.62億美元)以確保在2025年前符合GDPR的要求。雖然隱私增強型計算可以降低風險,但它會增加計算成本並影響專案進度。

細分市場分析

以平台解決方案為主導的通訊資料貨幣化市場佔整個市場的56.53%。儘管服務領域的規模較小,但預計其複合年成長率將達到17.02%,因為通訊業者意識到,聘用稀缺的資料科學人才比與專業供應商簽訂收益分成協議成本更高。Accenture和IBM等公司目前正提供最低收益增值條款,在控制通訊業者資本預算的同時,承擔財務風險。這項轉變凸顯了通訊數據貨幣化產業正朝著基於績效的合約模式發展。

託管分析合約的期限正從三年延長至七年,反映出演算法持續更新的必要性。根據 Amdocs 發布的 2025 年報告,託管服務訂單年增 28%,主要得益於多年期貨幣化合約的推動。通訊業者將此視為應對內部技能短缺的一種手段。全球範圍內,精通業務支撐系統 (BSS) 並擁有高級機器學習專業知識的專家少於 8000 人。同時,供應商在加速創新週期的同時,透過將智慧財產權與訓練模式捆綁在一起,增加了轉換成本。

到2025年,本地部署架構將佔總支出的58.73%,因為銀行、國防和醫療保健產業的主權要求限制了異地處理。然而,受容器化微服務在高峰流量期間彈性擴展的推動,雲端運算在通訊數據貨幣化市場的佔有率預計將以17.66%的複合年成長率成長。 Proximus在遷移後將其上線週期從90天縮短至14天,這表明雲端運算可以減少技術債。

監管正逐步改變市場格局。歐盟資料法要求服務提供者支援無縫工作負載遷移,從而遏制供應商鎖定。在混合模式下,原始用戶識別碼保存在國內資料中心,而匿名化的聚合資料則被傳送到超大規模雲端進行進階處理。這種雙區域架構使通訊業者既能滿足合規要求,又能受益於超大規模資料中心業者雲端平台的成本優勢,從而加速了其應用,不僅吸引了精通IT技術的頂級營運商,也吸引了眾多中型營運商的採用。

區域分析

到2025年,北美將佔總收入的38.91%,並將繼續作為API優先貨幣化的中心。 AT&T的Aduna在第一年就創造了1.8億美元的費用收入,而Verizon的6G創新論壇則推出了概念驗證(PoC),保證了自動駕駛汽車的延遲。加拿大Rogers公司憑藉著與智慧城市相關的契約,資訊服務收入較去年同期成長了19%。 FCC和CCPA監管政策的穩定性正在推動合規性更加明確,並縮短產品上市時間。

預計到2031年,亞太地區的複合年成長率將達到19.03%,位居全球之首。中國移動每月在邊緣運算處理3.2Exabyte,從工業IoT領域創造了280億元人民幣(約39億美元)的收入。 Bharti Airtel的聯合市場正在將位置智慧技術推廣到印度的電子商務和金融領域。同時,日本Softbank Corporation利用LotusFlare將產品發表週期縮短至兩週。韓國SK Telecom和KT共同投資1.2億美元,成立了一個專注於智慧工廠的邊緣運算聯盟。

在歐洲,GDPR合規成本預計到2025年將達到13億歐元(15.3億美元),但五家通訊業者正透過「邊緣連續體」(Edge Continuum)合作計畫來應對這項挑戰。該計畫旨在實現歐盟範圍內的分析,同時保障差分隱私。在中東,成熟的通訊業者正利用5G-Advanced的部署,力爭到2028年實現“超越連接的收入”,相當於總服務收入的25%。在非洲,通訊業者正優先發展金融科技,利用其廣泛的行動支付基礎設施來彌補用戶平均收入(ARPU)的下降。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 5G網路帶來的數據量激增

- 雲端原生貨幣化平台的廣泛應用

- 對個人化客戶體驗的需求日益成長

- 拓展物聯網和邊緣分析的應用場景。

- 通訊業者主導的聯盟型數據市場的興起

- 透過廣泛採用隱私增強計算實現通訊業者間資訊交易。

- 市場限制因素

- 嚴格的資料隱私和主權法規

- 將傳統IT與OSS/BSS整合的複雜性

- 關稅導致硬體成本波動加劇

- 通訊業面臨資料科學人才的獨特短缺問題。

- 產業價值鏈分析

- 監理情勢

- 宏觀經濟因素的影響

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 按組件

- 平台

- 服務

- 部署模式

- 雲

- 現場

- 透過使用

- 客戶經驗管理

- 網管

- 行銷和廣告

- 風險與合規管理

- 最終用戶

- 通訊業者

- 公司

- 政府

- 其他最終用戶

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲

- 其他亞太國家

- 中東和非洲

- 中東

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 土耳其

- 其他中東國家

- 非洲

- 南非

- 埃及

- 奈及利亞

- 其他非洲國家

- 中東

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Accenture plc

- IBM Corporation

- Amdocs Limited

- Telefonaktiebolaget LM Ericsson

- Nokia Corporation

- Huawei Technologies Co., Ltd.

- Cisco Systems, Inc.

- Oracle Corporation

- SAP SE

- Teradata Corporation

- Subex Limited

- Mahindra Comviva Technologies Limited

- Allot Ltd.

- Optiva Inc.

- CSG Systems International, Inc.

- Comarch SA

- VIAVI Solutions Inc.

- NetScout Systems, Inc.

- Openet Telecom Limited

- Tecnotree Corporation

第7章 市場機會與未來展望

According to Mordor Intelligence, the telecom data monetization market size is projected to be USD 5.57 billion in 2025, USD 6.43 billion in 2026, and reach USD 13.20 billion by 2031, growing at a CAGR of 15.48% from 2026 to 2031.

This report is Segmented by Component (Platform and Services), Deployment Mode (Cloud and On-Premises), Application (Customer Experience Management, Network Management, and More), End User (Telecom Operators, Enterprises, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Telecom Data Monetization Market Trends and Insights

Rapid Surge in Data Volume from 5G Networks

5G subscribers now generate 10-100X more traffic than 4G counterparts, offering an unprecedented substrate for real-time analytics. Verizon disclosed that its 5G users averaged 47 GB of monthly consumption in 2025, more than double that of 4G cohorts. AT&T's Aduna API platform capitalized on this traffic by producing USD 180 million of incremental revenue during its first year of operation. China Mobile processed 3.2 exabytes per month at edge nodes fitted to 5G base stations, unlocking low-latency industrial IoT contracts. Analyst estimates indicate that edge-enabled revenue streams could underpin 40% of enterprise 5G monetization by 2028.

Growing Adoption of Cloud-Native Monetization Platforms

Cloud-native stacks decouple monetization logic from legacy billing, cutting release cycles from quarters to weeks. Proximus migrated its entire BSS to Nokia's AVA cloud platform in 2025, trimming operational costs by 22% and slashing product-launch lead times to 14 days. LotusFlare's platform delivered similar agility for SoftBank and Taiwan Mobile, compressing launch timelines to under two weeks. Salesforce and Amdocs unified their CRM and AI monetization engines, enabling real-time journey orchestration that increased net promoter scores by 23% within 6 months.

Stringent Data Privacy and Sovereignty Regulations

GDPR fines have almost doubled since 2024, with Meta's EUR 1.2 billion (USD 1.4 billion) verdict spotlighting cross-border risk. TikTok's EUR 345 million (USD 404 million) penalty over children's data triggered sector-wide audits. Vodafone spent GBP 120 million (USD 162 million) on GDPR compliance in 2025. Privacy-enhancing computation mitigates exposure but inflates compute bills and stretches project timelines.

Other drivers and restraints analyzed in the detailed report include:

- Rising Demand for Personalized Customer Experiences

- Expansion of IoT and Edge Analytics Use-Cases

- Legacy IT and OSS/BSS Integration Complexity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The Telecom data monetization market, attributed to platform solutions, reached 56.53% of the total market value. Services, although smaller, will accelerate at a 17.02% CAGR, as telcos concede that recruiting scarce data-science talent is more costly than revenue-sharing deals with specialist vendors. Accenture and IBM now guarantee minimum uplift clauses, absorbing financial risk while keeping operators' capital budgets in check. The shift underscores how the Telecom data monetization industry is evolving toward outcome-based engagements.

Managed analytics contracts are lengthening from 3 to 7 years, reflecting ongoing algorithm refresh requirements. Amdocs' FY 2025 report showed managed-services bookings rising 28% YoY, driven by multi-year monetization deals. Operators view this as a hedge against internal skills gaps; fewer than 8,000 professionals globally combine BSS fluency with advanced ML expertise. Vendors, in turn, bundle intellectual property rights to trained models, creating switching costs while also accelerating innovation cycles.

On-premises architectures captured 58.73% of 2025 spending because sovereignty mandates in banking, defense, and healthcare discourage off-site processing. Yet the cloud slice of the Telecom data monetization market is projected to grow at 17.66% CAGR, driven by containerized microservices that scale elastically during traffic peaks. Proximus trimmed launch cycles from 90 days to 14 days post-migration, proof that cloud reduces technical debt.

Regulation is gradually tilting the field. The EU Data Act compels providers to support seamless workload porting, curbing vendor lock-in. Hybrid models keep raw subscriber identifiers in national data centers while shipping anonymized aggregates to hyperscale clouds for heavy processing. Such dual-zone architectures allow telcos to meet compliance requirements while enjoying hyperscaler cost curves, accelerating adoption beyond IT-savvy tier-1s into mid-tier carriers.

Geography Analysis

North America contributed 38.91% of 2025 revenue and remains the epicenter of API-first monetization. AT&T's Aduna generated USD 180 million in year-one fees, while Verizon's 6G Innovation Forum produced latency-guaranteed proofs of concept for autonomous vehicles. Canada's Rogers grew data-services revenue 19% YoY, due to smart-city contracts. Regulatory stability under the FCC and CCPA provides clarity on compliance, accelerating time-to-market.

Asia-Pacific will register the highest CAGR of 19.03% through 2031. China Mobile processed 3.2 exabytes monthly at the edge, yielding CNY 28 billion (USD 3.9 billion) in industrial IoT revenue. Bharti Airtel's federated marketplace democratizes location intelligence for the Indian e-commerce and finance sectors, while Japan's SoftBank compressed product launches to two weeks via LotusFlare. Korea's SK Telecom and KT jointly invested USD 120 million in an edge consortium, targeting smart factories.

Europe grapples with soaring GDPR compliance costs of EUR 1.3 billion (USD 1.53 billion) in 2025 but counters with a five-operator federated Edge Continuum that preserves differential privacy while enabling pan-EU analytics. Middle East incumbents, fueled by 5G-Advanced rollouts, aim to achieve beyond-connectivity revenue equal to 25% of total service income by 2028. African carriers prioritize fintech monetization, leveraging ubiquitous mobile payment rails to offset lower ARPU.

- Accenture plc

- IBM Corporation

- Amdocs Limited

- Telefonaktiebolaget LM Ericsson

- Nokia Corporation

- Huawei Technologies Co., Ltd.

- Cisco Systems, Inc.

- Oracle Corporation

- SAP SE

- Teradata Corporation

- Subex Limited

- Mahindra Comviva Technologies Limited

- Allot Ltd.

- Optiva Inc.

- CSG Systems International, Inc.

- Comarch S.A.

- VIAVI Solutions Inc.

- NetScout Systems, Inc.

- Openet Telecom Limited

- Tecnotree Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Surge in Data Volume from 5G Networks

- 4.2.2 Growing Adoption of Cloud-Native Monetization Platforms

- 4.2.3 Rising Demand for Personalized Customer Experiences

- 4.2.4 Expansion of IoT and Edge Analytics Use-Cases

- 4.2.5 Emergence of Telco-Led Federated Data Marketplaces

- 4.2.6 Proliferation of Privacy-Enhancing Computation Enabling Cross-Carrier Insight Trading

- 4.3 Market Restraints

- 4.3.1 Stringent Data Privacy and Sovereignty Regulations

- 4.3.2 Legacy IT AND OSS/BSS Integration Complexity

- 4.3.3 Escalating Tariff-Driven Hardware Cost Volatility

- 4.3.4 Shortage of Telecom-Specific Data Science Talent

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Impact of Macroeconomic Factors

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Platform

- 5.1.2 Services

- 5.2 By Deployment Mode

- 5.2.1 Cloud

- 5.2.2 On-Premises

- 5.3 By Application

- 5.3.1 Customer Experience Management

- 5.3.2 Network Management

- 5.3.3 Marketing and Advertising

- 5.3.4 Risk and Compliance Management

- 5.4 By End User

- 5.4.1 Telecom Operators

- 5.4.2 Enterprises

- 5.4.3 Government

- 5.4.4 Other End Users

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 United Arab Emirates

- 5.5.5.1.2 Saudi Arabia

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Egypt

- 5.5.5.2.3 Nigeria

- 5.5.5.2.4 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Accenture plc

- 6.4.2 IBM Corporation

- 6.4.3 Amdocs Limited

- 6.4.4 Telefonaktiebolaget LM Ericsson

- 6.4.5 Nokia Corporation

- 6.4.6 Huawei Technologies Co., Ltd.

- 6.4.7 Cisco Systems, Inc.

- 6.4.8 Oracle Corporation

- 6.4.9 SAP SE

- 6.4.10 Teradata Corporation

- 6.4.11 Subex Limited

- 6.4.12 Mahindra Comviva Technologies Limited

- 6.4.13 Allot Ltd.

- 6.4.14 Optiva Inc.

- 6.4.15 CSG Systems International, Inc.

- 6.4.16 Comarch S.A.

- 6.4.17 VIAVI Solutions Inc.

- 6.4.18 NetScout Systems, Inc.

- 6.4.19 Openet Telecom Limited

- 6.4.20 Tecnotree Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

數據貨幣化市場-2026-2032年全球市場預測通訊業者資料貨幣化市場:按服務類型、定價模式、部署模式、客戶類型和產業分類-2026-2032年全球市場預測

數據貨幣化市場-2026-2032年全球市場預測通訊業者資料貨幣化市場:按服務類型、定價模式、部署模式、客戶類型和產業分類-2026-2032年全球市場預測 全球電信市場追蹤(2025 年第四季):資本支出減少將有助於提高收益,使利潤率達到近 10 年來的最高水準。通訊業人才追蹤報告(2025 年第四季):預計通訊業就業人數將繼續以每年約 2% 的速度下降——但現在就將其歸咎於人工智慧還為時過早。

全球電信市場追蹤(2025 年第四季):資本支出減少將有助於提高收益,使利潤率達到近 10 年來的最高水準。通訊業人才追蹤報告(2025 年第四季):預計通訊業就業人數將繼續以每年約 2% 的速度下降——但現在就將其歸咎於人工智慧還為時過早。 資料貨幣化市場規模、佔有率、趨勢和預測:按方法論、組織規模、最終用途和地區分類,2026-2034 年

資料貨幣化市場規模、佔有率、趨勢和預測:按方法論、組織規模、最終用途和地區分類,2026-2034 年 數據貨幣化市場:按組件、部署方式、組織規模、產業和地區分類

數據貨幣化市場:按組件、部署方式、組織規模、產業和地區分類 數據貨幣化市場規模、佔有率和趨勢分析報告:按公司規模、方法論、行業、地區和細分市場預測(2026-2033 年)

數據貨幣化市場規模、佔有率和趨勢分析報告:按公司規模、方法論、行業、地區和細分市場預測(2026-2033 年) 全球數據貨幣化市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球數據貨幣化市場規模、佔有率、趨勢和成長分析報告(2026-2034) 資料貨幣化市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、流程、部署模式及最終使用者分類

資料貨幣化市場分析及預測(至2035年):依類型、產品類型、服務、技術、組件、應用、流程、部署模式及最終使用者分類 2026年生命科學公司數據貨幣化解決方案全球市場報告

2026年生命科學公司數據貨幣化解決方案全球市場報告