|

市場調查報告書

商品編碼

2063375

非洲資料中心浸沒式冷卻液:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)Africa Data Center Immersion Cooling Fluid - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

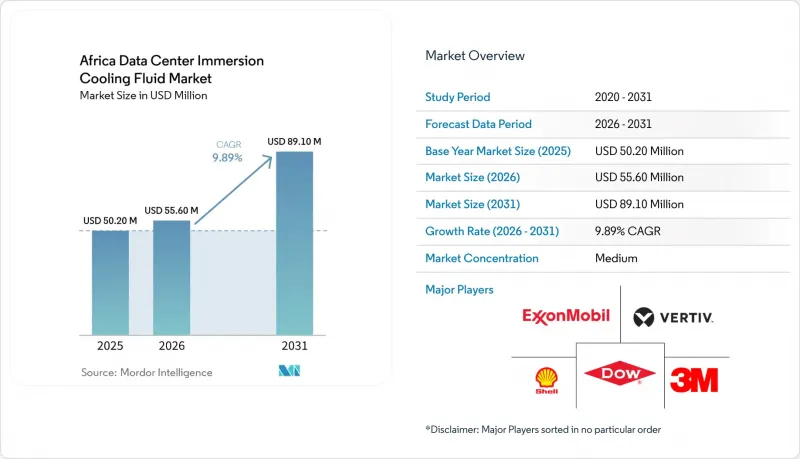

據 Mordor Intelligence 稱,非洲資料中心浸沒式冷卻劑市場預計將從 2025 年的 5,020 萬美元和 2026 年的 5,560 萬美元成長到 2031 年的 8,910 萬美元,2026 年至 2031 年的複合年成長率為 9.89%。

本報告按流體類型(例如礦物油和合成烴)、相態類型(單相和兩相)、資料中心類型(例如雲端服務供應商和託管資料中心)、終端用戶產業(例如IT/ITES和銀行、金融服務和保險業)以及地區(例如巴西和阿根廷)進行細分。市場預測以美元計價。

非洲資料中心浸沒式冷卻液市場趨勢與洞察

約翰內斯堡和內羅畢走廊超大規模設施的擴張

目前,非洲最活躍的兩大資料中心走廊正受到Teraco公司4.42億美元的設施擴建工程和Equinix公司3.9億美元的進軍計畫的雙重推動。這兩個項目都配備了液冷機房,可容納超過100kW的機架。高光纖密度、營運商機房以及接近性海底光纜的優勢,使得營運商能夠保證與歐洲樞紐的延遲低於40毫秒,這對於GPU訓練工作負載至關重要。專案融資機構要求PUE值低於1.2,這使得液冷成為事實上的標準架構。設備OEM廠商也順應此投資趨勢,在豪登省和基安布省建立預庫存設施,以縮短流體系統的前置作業時間。這種集聚效應降低了絕緣體供應商的物流成本,即使在二線城市開發區也能承接大規模合約。

電費上漲將加速整體擁有成本的最佳化。

2024年,奈及利亞A級電價飆升至225奈拉/度數(0.14美元/度),三級設施的營運成本將增加30%以上。肯亞的商業電價更高,達到0.202美元/kWh。在南非,Eskom公司預計2025年的電價上漲將使大型電力用戶的平均負擔增加18.7%。液冷技術透過降低伺服器風扇功耗和消除冷卻器機組負荷,可減少40-50%的能源需求,使綜合PUE值降至接近1.05。這可以將投資回收期縮短2-3年。目前,財務長們已將電價上漲情境納入投資備忘錄,並普遍認為,在資產使用壽命的第四年之後,液冷是最具成本效益的選擇。電價上漲也促使人們對現場太陽能+電池微電網的興趣日益濃厚。由於浸沒式冷卻技術減少了空調設備的安裝面積,因此對相關設備的投資也隨之減少。

由於本地配製的特殊絕緣液短缺,導致進口量激增。

在撒哈拉以南非洲地區,僅有兩家工廠擁有符合ISO認證的絕緣油調配生產線,迫使大多數買家進口成品,而每個ISO罐的運費超過3,000美元。關稅依HS編碼的不同,稅率在5%到10%之間,外匯短缺常常導致清關延誤數週,使貨架運作。小規模企業無法滿足最低訂購量,被迫支付比合約價格高出15%到20%的現貨溢價。國內化工生產商曾考慮合約調配協議,但由於原料純度要求高,除非能保證一定數量的訂單,否則不願投資。在本地產能提升之前,供應風險和飆升的接收成本可能會阻礙價格敏感型大都會圈的普及。

細分市場分析

到2025年,礦物油將憑藉其價格優勢和廣泛的供應,佔據非洲資料中心浸沒式冷卻液市場48.0%的最大市場佔有率。儘管生物酯類成本較高,但由於資產管理公司對永續性揭露的審查日益嚴格,其在該領域的複合年成長率將達到11.9%。隨著無PFAS(全氟烷基和多氟烷基物質)強制性要求在採購框架中不斷擴大,生物酯類在非洲資料中心浸沒式冷卻液市場的規模預計將迅速成長。合成烴類產品主要針對高溫應用領域,而含氟產品則在PFAS禁令實施後市佔率正在下降。

生物酯供應商,例如TotalEnergies(旗下擁有BioLife品牌)和嘉吉(旗下擁有NatureCool品牌),正在向超大規模業者強調生物酯的可生物分解性優勢。 Chemors與Navin Fluorine於2025年5月達成的合作,將使Opteon的生產設施更靠近非洲大陸。當地的化合物生產商正在探索棕櫚油衍生的原料以降低進口成本,但資金籌措挑戰仍然存在。

到2025年,單相設計將佔非洲資料中心浸沒式冷卻液市場73.5%的銷售額,並構成該市場的基礎,滿足那些尋求更簡單部署方案的企業的需求。目前佔比較小的雙相系統預計將以每年11.7%的速度成長,因為它們能夠實現超過100kW的GPU機架密度。如果超大規模人工智慧叢集大規模採用這種拓樸結構,到2030年,非洲資料中心浸沒式冷卻液市場中雙相流體的市場規模可能會翻倍。

江森自控於2025年9月推出的模組化空調機組(CDU)透過提供即插即用的擴充性,解決了人們對複雜性的擔憂。在拉各斯和內羅畢的初步試點部署表明,與風冷式和冷空氣循環(CRAH)維修相比,該系統可降低20%的總擁有成本(TCO)。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 在約翰尼斯堡和內羅畢走廊建設超大規模設施

- 電費上漲將加速整體擁有成本的最佳化。

- 開普敦和薩赫勒地區嚴重缺水,推動了液冷技術的使用。

- 面向金融科技和電子商務的泛非人工智慧/機器學習叢集

- 資料中心稅收優惠(例如,肯亞投資促進法)

- 向不含 PFAS 的生物酯基液壓油過渡,以用於 ESG 報告

- 市場限制因素

- 由於國內生產的特殊介電混合物短缺,進口量正在增加。

- 與傳統空氣冷卻系統相比,初始資本支出 (CAPEX) 增加

- 非洲浸沒式冷卻缺乏安全標準

- 全球逐步淘汰 PFAS 相關的供應鏈風險

- 價值供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

第5章 市場規模與成長預測

- 按流體類型

- 礦物油

- 合成烴

- 含氟液體

- 生物基酯

- 按階段

- 單相

- 兩相

- 依資料中心類型

- 雲端服務供應商

- 搭配

- 本地部署/企業級/邊緣部署

- 按最終用戶行業分類

- IT/ITES

- BFSI

- 衛生保健

- 政府/國防

- 媒體與娛樂

- 其他最終用戶

- 國家

- 南非

- 奈及利亞

- 肯亞

- 埃及

- 摩洛哥

- 其他非洲國家

第6章 競爭情勢

- 市佔率分析

- 公司簡介

- 3M

- The Dow Chemical Company

- Exxon Mobil Corporation

- Shell plc

- The Chemours Company

- Cargill Incorporated

- Castrol Limited(BP)

- FUCHS SE

- The Lubrizol Corporation

- Engineered Fluids Inc.

- Submer Technologies SL

- Asperitas

- Iceotope Technologies

- LiquidStack

- Green Revolution Cooling

- Vertiv

- Schneider Electric

- Dell Technologies

- Supermicro

- Asetek

- FluoroCool

- BitCool

- DCX-The Liquid Cooling Co.

- Allied Control Ltd.

- Giga Cooling

第7章 市場機會與未來展望

According to Mordor Intelligence, the africa data center immersion cooling fluid market size is projected to expand from USD 50.20 million in 2025 and USD 55.60 million in 2026 to USD 89.10 million by 2031, registering a CAGR of 9.89% between 2026 to 2031.

This report is Segmented by Fluid Type (Mineral Oil and Synthetic Hydrocarbon, and More), Phase Type (Single-Phase and Two-Phase), Data Center Type (Cloud Service Providers and Colocation, and More), End-User Industry (IT/ITES and BFSI, and More), and Geography (Brazil and Argentina, and More). The Market Forecasts are Provided in Terms of Value (USD).

Africa Data Center Immersion Cooling Fluid Market Trends and Insights

Hyperscale build-outs in Johannesburg and Nairobi corridors

Africa's two most active data-center corridors are now anchored by Teraco's USD 442 million facility expansion and Equinix's USD 390 million entry plan, both of which specify immersion-ready halls capable of 100 kW-plus racks. High fiber density, carrier hotels, and submarine-cable proximity let operators guarantee sub-40 ms latency to European hubs, a prerequisite for GPU training workloads. Project lenders insist on PUE targets under 1.2, effectively locking in liquid cooling as the baseline architecture. Equipment OEMs follow the investment, placing forward-stock depots in Gauteng and Kiambu counties to shorten lead times for fluid systems. The clustering effect lowers logistics costs for dielectric suppliers, making bulk contracts viable for secondary metro builds.

Rising electricity tariffs driving TCO optimization

Nigeria's Band A tariff leap to NGN 225/kWh (USD 0.14/kWh) in 2024 pushed operating expenditure up by more than 30% for Tier III facilities. Kenya's commercial tariff sits even higher at USD 0.202/kWh, while South Africa's 2025 Eskom hike averages 18.7% on large-power users. Immersion cooling cuts server-fan draw and eliminates chiller loads, shrinking energy needs 40-50% and pushing blended PUE close to 1.05, which in turn shaves two to three years off payback periods. CFOs now build tariff-inflation scenarios into investment memos, often finding liquid cooling the least-cost option beyond year 4 of asset life. The tariff pressure also boosts interest in on-site solar-plus-battery microgrids, whose capex aligns naturally with immersion's reduced HVAC footprint.

Scarce local blending of specialty dielectrics inflating imports

Only two sub-Saharan facilities possess ISO-certified blending lines for dielectric fluids, forcing most buyers to import finished product at freight rates exceeding USD 3,000 per ISO tank. Duties range between 5-10% depending on HS code classification, and forex shortages often delay customs clearance by weeks, leaving racks idle. Smaller operators cannot meet minimum-order quantities, paying spot premiums of 15-20% over contract pricing. Domestic chemical firms have considered toll-blending agreements, yet high feedstock purity requirements deter investment without guaranteed take-or-pay volumes. Until local capacity improves, supply risk and elevated landed cost will cap adoption in price-sensitive metros.

Other drivers and restraints analyzed in the detailed report include:

- Severe water stress in Cape Town and Sahel favoring liquid cooling

- Pan-African AI/ML clusters for fintech and e-commerce

- Higher up-front CAPEX vs. legacy air cooling

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Mineral oil secured the highest 48.0% share of the Africa data center immersion cooling fluid market in 2025, owing to favorable pricing and broad availability. Bio-esters, though costlier, post the segment's quickest 11.9% CAGR as asset managers scrutinize sustainability disclosures. The Africa data center immersion cooling fluid market size for bio-esters is projected to climb sharply as PFAS-free mandates spread across procurement frameworks. Synthetic hydrocarbons target niche high-heat applications, while fluorocarbon products trend downward following PFAS prohibitions.

Bio-ester suppliers such as TotalEnergies (BioLife) and Cargill (NatureCool) pitch biodegradability advantages to hyperscale bidders, and Chemours' May 2025 alliance with Navin Fluorine adds Opteon production closer to the continent. Local formulators explore palm-derivative feedstocks to cut import bills, though financing hurdles persist.

Single-phase designs represented 73.5% of 2025 revenue, anchoring the Africa data center immersion cooling fluid market share among operators seeking straightforward rollout. Two-phase installations, while only a minority today, are forecast to grow 11.7% annually as they enable GPU rack densities exceeding 100 kW. The Africa data center immersion cooling fluid market size for two-phase fluids could double by 2030 if hyperscale AI clusters adopt the topology at scale.

Johnson Controls' September 2025 modular CDU launch mitigates complexity fears by offering plug-and-play expansion; early pilots in Lagos and Nairobi demonstrate 20% TCO savings versus air-cooled plus CRAH retrofits.

List of Companies Covered in this Report:

- 3M

- The Dow Chemical Company

- Exxon Mobil Corporation

- Shell plc

- The Chemours Company

- Cargill Incorporated

- Castrol Limited (BP)

- FUCHS SE

- The Lubrizol Corporation

- Engineered Fluids Inc.

- Submer Technologies S.L.

- Asperitas

- Iceotope Technologies

- LiquidStack

- Green Revolution Cooling

- Vertiv

- Schneider Electric

- Dell Technologies

- Supermicro

- Asetek

- FluoroCool

- BitCool

- DCX - The Liquid Cooling Co.

- Allied Control Ltd.

- Giga Cooling

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Hyperscale build-outs in Johannesburg and Nairobi corridors

- 4.2.2 Rising electricity tariffs driving TCO optimisation

- 4.2.3 Severe water-stress in Cape Town and Sahel favouring liquid cooling

- 4.2.4 Pan-African AI/ML clusters for fintech and e-commerce

- 4.2.5 Data-centre tax incentives (e.g., Kenya Investment Promotion Act)

- 4.2.6 Shift to PFAS-free bio-ester fluids for ESG reporting

- 4.3 Market Restraints

- 4.3.1 Scarce local blending of specialty dielectrics inflating imports

- 4.3.2 Higher up-front CAPEX vs. legacy air cooling

- 4.3.3 Absence of African immersion-cooling safety standards

- 4.3.4 Supply-chain risk amid global PFAS phase-out

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE and GROWTH FORECASTS

- 5.1 By Fluid Type

- 5.1.1 Mineral Oil

- 5.1.2 Synthetic Hydrocarbon

- 5.1.3 Fluorocarbon-based Fluids

- 5.1.4 Bio-based Esters

- 5.2 By Phase Type

- 5.2.1 Single-Phase

- 5.2.2 Two-Phase

- 5.3 By Data Center Type

- 5.3.1 Cloud Service Providers

- 5.3.2 Colocation

- 5.3.3 On-Premise / Enterprise / Edge

- 5.4 By End-User Industry

- 5.4.1 IT / ITES

- 5.4.2 BFSI

- 5.4.3 Healthcare

- 5.4.4 Government and Defense

- 5.4.5 Media and Entertainment

- 5.4.6 Other End-Users

- 5.5 By Country

- 5.5.1 South Africa

- 5.5.2 Nigeria

- 5.5.3 Kenya

- 5.5.4 Egypt

- 5.5.5 Morocco

- 5.5.6 Rest of Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Market Share Analysis

- 6.2 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.2.1 3M

- 6.2.2 The Dow Chemical Company

- 6.2.3 Exxon Mobil Corporation

- 6.2.4 Shell plc

- 6.2.5 The Chemours Company

- 6.2.6 Cargill Incorporated

- 6.2.7 Castrol Limited (BP)

- 6.2.8 FUCHS SE

- 6.2.9 The Lubrizol Corporation

- 6.2.10 Engineered Fluids Inc.

- 6.2.11 Submer Technologies S.L.

- 6.2.12 Asperitas

- 6.2.13 Iceotope Technologies

- 6.2.14 LiquidStack

- 6.2.15 Green Revolution Cooling

- 6.2.16 Vertiv

- 6.2.17 Schneider Electric

- 6.2.18 Dell Technologies

- 6.2.19 Supermicro

- 6.2.20 Asetek

- 6.2.21 FluoroCool

- 6.2.22 BitCool

- 6.2.23 DCX - The Liquid Cooling Co.

- 6.2.24 Allied Control Ltd.

- 6.2.25 Giga Cooling

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

雙相液冷式伺服器市場報告:趨勢、預測與競爭分析(至2035年)

雙相液冷式伺服器市場報告:趨勢、預測與競爭分析(至2035年) 全球兩相浸沒式冷卻液市場(按流體類型、系統類型、流動技術、應用和最終用戶產業分類)預測(2026-2032年)泵送式兩相冷凍系統市場(按最終用戶、應用、泵類型、蒸發器設計、分銷管道和冷媒類型分類),全球預測,2026-2032年

全球兩相浸沒式冷卻液市場(按流體類型、系統類型、流動技術、應用和最終用戶產業分類)預測(2026-2032年)泵送式兩相冷凍系統市場(按最終用戶、應用、泵類型、蒸發器設計、分銷管道和冷媒類型分類),全球預測,2026-2032年 資料中心浸沒式冷卻市場:成長機會、成長要素、產業趨勢分析及2026-2035年預測

資料中心浸沒式冷卻市場:成長機會、成長要素、產業趨勢分析及2026-2035年預測 資料中心浸沒式冷卻:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)資料中心氟化冷卻劑市場:依流體組成、相態、冷卻方式、部署配置和應用分類-全球預測,2026-2032年資料中心浸沒式冷卻液市場按冷卻液化學成分、介電類型、流體類型、資料中心類型、應用和最終用戶產業分類 - 全球預測(2026-2032 年)資料中心綠色冷卻劑市場:按冷卻劑類型、資料中心規模、部署模式、最終用戶產業和銷售管道,全球預測,2026-2032年

資料中心浸沒式冷卻:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)資料中心氟化冷卻劑市場:依流體組成、相態、冷卻方式、部署配置和應用分類-全球預測,2026-2032年資料中心浸沒式冷卻液市場按冷卻液化學成分、介電類型、流體類型、資料中心類型、應用和最終用戶產業分類 - 全球預測(2026-2032 年)資料中心綠色冷卻劑市場:按冷卻劑類型、資料中心規模、部署模式、最終用戶產業和銷售管道,全球預測,2026-2032年 全球兩相資料中心浸沒式冷卻市場:市場規模、佔有率、成長率、產業分析、依類型、應用和地區劃分的分析以及未來預測(2026-2034)

全球兩相資料中心浸沒式冷卻市場:市場規模、佔有率、成長率、產業分析、依類型、應用和地區劃分的分析以及未來預測(2026-2034) 全球資料中心浸入式冷卻液市場(至 2032 年)按技術(單相 vs. 雙相)、資料中心類型(超大規模、AI/ML、加密貨幣挖礦)、類型(礦物油、氟碳基液體、合成液體)和地區分類

全球資料中心浸入式冷卻液市場(至 2032 年)按技術(單相 vs. 雙相)、資料中心類型(超大規模、AI/ML、加密貨幣挖礦)、類型(礦物油、氟碳基液體、合成液體)和地區分類