|

市場調查報告書

商品編碼

1982314

資料中心浸沒式冷卻市場:成長機會、成長要素、產業趨勢分析及2026-2035年預測Data Center Immersion Cooling Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

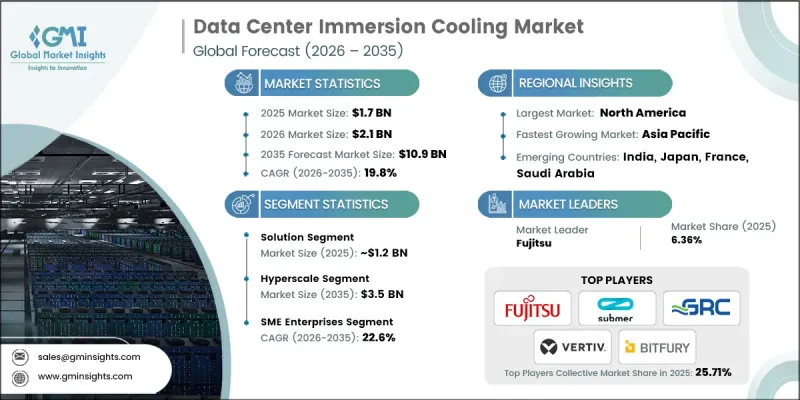

2025 年全球資料中心浸沒式冷卻市場價值 17 億美元,預計到 2035 年將達到 109 億美元,年複合成長率為 19.8%。

在數位轉型加速和下一代運算需求的推動下,市場正經歷快速成長。人工智慧 (AI) 和機器學習工作負載的激增、機架功率密度的不斷提高以及設施整體能源效率提升的壓力,都為這一成長提供了動力。隨著運算負載的持續攀升,傳統的冷卻方式已不再適用,加速了向浸沒式冷卻系統的轉變。不斷上漲的電價和日益增強的環保意識,進一步強化了採用更有效率溫度控管技術的經濟合理性。託管環境和都市區資料中心有限的占地面積也促使營運商採用高密度解決方案。與傳統的風冷系統相比,浸沒式冷卻可以顯著提高每平方英尺的運算密度,使設施營運商能夠在無需大規模投入的情況下,最大限度地利用現有基礎設施。在單相浸沒式冷卻架構中,絕緣液在運作中保持液態,而泵浦和外部熱交換器則有效散發累積的熱負荷。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 17億美元 |

| 預測金額 | 109億美元 |

| 複合年成長率 | 19.8% |

按組件分類,解決方案部分佔據72%的市場佔有率,預計到2025年市場規模將達到12億美元。該部分包括整合式浸沒冷卻系統,其中包括浸沒式冷卻槽、冷卻液管理框架、熱交換單元、監控平台和整合硬體。供應商正日益提供全面、即裝即用的系統,旨在與現有資料中心環境無縫相容。現代解決方案融合了智慧溫度追蹤、自動冷卻液調節以及與設施管理系統的整合,從而提升運行性能並最佳化整體能源利用。

從終端用戶來看,預計到2025年,超大規模資料中心將佔據29.8%的市場佔有率,到2035年將達到35億美元。大型資料中心營運商正在大力投資先進的運算基礎設施,以滿足高效能處理的需求。這些設施在專用空間運行大規模伺服器環境,優先考慮效率、擴充性和長期基礎設施彈性。超大規模業者非常重視整體擁有成本(TCO),在選擇冷卻技術時,會仔細權衡資本支出、營運效率和長期永續性目標。

美國資料中心浸沒式冷卻市場預計到2025年將達到4.542億美元,並在2026年至2035年間以16.9%的複合年成長率成長。主要雲端服務供應商和領先科技公司在美國的擴張推動了對先進冷卻技術的需求成長。隨著數位基礎設施規模的擴大,各組織機構優先考慮經濟高效且節能的溫度控管系統,以維持業務競爭力。美國各地區對永續性和提高能源利用效率的堅定承諾,正在加速浸沒式冷卻解決方案在美國市場的普及。

目錄

第1章:調查方法

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 成本結構

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 將機架功率密度提升到超越傳統風冷極限的水平

- 人工智慧、GPU 和高密度工作負載帶來的溫度控管挑戰日益增加。

- 我們專注於永續性、能源效率和降低PUE。

- 在超大規模和高效能運算環境中擴展部署

- 託管服務供應商和大型企業資料中心正在擴大採用範圍。

- 產業潛在風險與挑戰

- 前期資本投入高,系統設計複雜

- 維護、流體處理和操作標準化的挑戰

- 市場機遇

- 人工智慧、機器學習和超級運算工作負載的快速成長

- 在偏遠地區和惡劣運行環境下擴展邊緣資料中心

- 絕緣液技術的創新和兩相浸沒系統的廣泛應用

- 促進因素

- 成長潛力分析

- 監理情勢

- 北美洲

- 美國能源局(DOE) 能源效率指南

- 美國環保署(EPA)關於化學品和冷媒的法規

- ASHRAE 資料處理環境熱設計指南

- 美國國家消防協會 (NFPA) 標準

- 加拿大自然資源部(NRCan)能源效率框架

- 歐洲

- 歐盟委員會的能源效率指令

- 歐盟資料中心能效行為準則

- REACH法規關於化學物質(介電液)

- 符合歐洲化學品管理局 (ECHA) 的規定

- 歐盟成員國的國家級環境與建築法規

- 亞太地區

- 中國工業與資訊化部資料中心效率政策

- 中國的能源標籤和綠色資料中心計劃

- 日本經濟產業省能源效率計劃

- 印度能源效率局 (BEE) 標準

- 新加坡資訊通訊媒體發展局 (IMDA) 綠色資料中心指南

- 拉丁美洲

- 國家資料中心能源效率計劃

- 工業流體環境合規框架

- 當地建築和電氣安全法規

- 地方基礎設施管理部門推廣的永續發展標準

- 中東和非洲

- 海灣合作理事會永續性與能源多元化舉措

- 沙烏地阿拉伯節能中心(SEEC)的規定

- 阿拉伯聯合大公國綠建築標準和資料中心永續性要求

- 非洲各地的環境監管機構

- 北美洲

- 波特的分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 單相浸沒式冷卻系統

- 兩相浸沒式冷卻技術

- 高密度GPU和AI最佳化的坦克設計

- 與模組化和預製資料中心整合

- 即時熱監控與智慧控制軟體

- 新興技術

- 單相浸沒式冷卻系統

- 兩相浸沒式冷卻技術

- 高密度GPU和AI最佳化的坦克設計

- 與模組化和預製資料中心整合

- 即時熱監控與智慧控制軟體

- 當前技術趨勢

- 成本細分分析

- 浸沒式水槽和圍護系統

- 絕緣液成本

- 水泵、熱交換器和冷卻分配裝置

- 監控軟體

- 安裝、維修和整合成本

- 永續性和環境影響

- 環境影響評估

- 社會影響和對社區的益處

- 公司管治與企業社會責任

- 永續金融與投資趨勢

- 消費者行為分析

- OEM和第三方浸沒式冷卻系統的選擇趨勢

- 選擇資本支出模式或營運支出模式(購買完整系統與浸沒式冷卻服務模式)

- 售後市場和服務趨勢分析

- 浸沒式冷卻系統的維護合約和性能服務水準協議

- 冷卻液更換週期、液體劣化監測和硬體升級

- 對浸沒式水槽及組件的 OEM 和第三方服務及支援提供者進行比較評估。

- 數位化和自動化趨勢分析

- 配備基於物聯網的熱性能監測功能的智慧浸沒式冷卻系統的興起。

- 人工智慧/機器學習在預測流體管理、系統最佳化和故障檢測中的作用。

- 浸沒式冷卻系統的引入、啟動和熱平衡調節的自動化。

- 與資料中心基礎設施管理 (DCIM) 和遙測平台整合。

- 數位雙胞胎在浸沒式冷卻系統性能模擬和維修規劃的應用。

- 超大規模、託管、高效能運算和邊緣環境的案例研究和實際應用。

- 分析可再生能源併網對資料中心浸沒式冷卻設計的影響

- 混合式能源配置(電網+太陽能+電池)中浸沒式冷卻系統的效率

- 浸沒式冷卻基礎設施對系統級直流電和交流電源的影響。

- 與浸沒式冷卻系統和備用儲能系統(鋰離子電池、液流電池)相容

- 智慧逆變器和動態能量路由在冷凍負載管理中的作用

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係和聯盟

- 新產品發布

- 業務拓展計劃及資金籌措

- 品牌比較分析

- 品牌知名度

- 夥伴關係生態系統

- 客戶服務

- 經銷網路的優勢

第5章 市場估計與預測:依組件分類,2022-2035年

- 解決方案

- 冷卻液

- 冷卻架/模組

- 篩選

- 泵浦

- 熱交換器

- 其他

- 服務

- 安裝/維護

- 培訓和諮詢

第6章 市場估算與預測:依冷凍技術分類,2022-2035年

- 單相冷卻

- 兩相冷卻

第7章 市場估計與預測:依冷卻液類型分類,2022-2035年

- 礦物油

- 合成冷卻液

- 含氟冷媒

第8章 市場估算與預測:依組織規模分類,2022-2035年

- 小型企業

- 主要企業

第9章 市場估計與預測:依應用領域分類,2022-2035年

- 超大規模

- 超級計算

- 企業級高效能運算

- 加密貨幣

- 邊緣/5G 運算

- 其他

第10章 市場估價與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 波蘭

- 俄羅斯

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 新加坡

- 馬來西亞

- 印尼

- 泰國

- 拉丁美洲

- 巴西

- 阿根廷

- 智利

- 哥倫比亞

- 中東和非洲(MEA)

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

第11章:公司簡介

- 世界公司

- Asperitas

- Dell Technologies

- Fujitsu

- Green Revolution Cooling(GRC)

- Hewlett Packard Enterprise(HPE)

- Submer

- Supermicro

- Vertiv

- 當地公司

- Asetek

- Bitfury

- DCX Liquid Cooling Company

- Gigabyte Technology

- Inspur

- LiquidCool Solutions

- Midas Immersion Cooling

- 新興企業

- ExaScaler

- Iceotope

- JetCool

- Quanta Cloud Technology(QCT)

- TAICHI Immersion Cooling

The Global Data Center Immersion Cooling Market was valued at USD 1.7 billion in 2025 and is estimated to grow at a CAGR of 19.8% to reach USD 10.9 billion by 2035.

Market growth is entering a high-growth phase, driven by accelerating digital transformation and next-generation computing requirements. Market expansion is fueled by the rapid surge in artificial intelligence and machine learning workloads, increasing rack power densities, and mounting pressure to improve energy efficiency across facilities. As computing intensity continues to escalate, traditional cooling approaches are becoming less viable, accelerating the shift toward immersion-based systems. Rising electricity costs and heightened environmental accountability are further reinforcing the economic case for more efficient thermal management technologies. Limited floor space in colocation environments and urban data facilities is also encouraging operators to adopt high-density solutions. Immersion cooling enables significantly higher compute density per square foot compared to conventional air-cooled systems, allowing facility operators to maximize existing infrastructure without major capital expansion. In single-phase immersion cooling architectures, dielectric fluid remains in a liquid state throughout operation, while pumps and external heat exchangers effectively dissipate accumulated thermal loads.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.7 Billion |

| Forecast Value | $10.9 Billion |

| CAGR | 19.8% |

By component, the solution segment held a 72% share, generating USD 1.2 billion in 2025. This segment encompasses integrated immersion cooling systems, including immersion tanks, coolant management frameworks, thermal exchange units, monitoring platforms, and supporting integration hardware. Vendors are increasingly delivering comprehensive, ready-to-deploy systems designed for seamless compatibility with established data center environments. Modern solutions incorporate intelligent temperature tracking, automated coolant regulation, and connectivity with facility management systems to enhance operational performance and overall energy optimization.

In terms of end users, the hyperscale segment held 29.8% share in 2025 and is forecast to reach USD 3.5 billion by 2035. Large-scale data center operators are heavily investing in advanced computing infrastructure to support high-performance processing demands. These facilities operate extensive server environments within purpose-built spaces, prioritizing efficiency, scalability, and long-term infrastructure resilience. Hyperscale operators place strong emphasis on total cost of ownership, carefully balancing capital expenditures, operating efficiency, and long-term sustainability objectives when selecting cooling technologies.

U.S. Data Center Immersion Cooling Market generated USD 454.2 million in 2025 and is anticipated to grow at a CAGR of 16.9% from 2026 to 2035. Increasing demand for advanced cooling technologies is driven by the expansion of large cloud service providers and major technology enterprises headquartered in the country. As digital infrastructure footprints expand, organizations are prioritizing cost-effective and energy-efficient thermal management systems to maintain operational competitiveness. Strong regional commitments to sustainability and improved power utilization effectiveness are accelerating the adoption of immersion cooling solutions across the U.S. market.

Key participants operating in the Global Data Center Immersion Cooling Market include Vertiv, Dell Technologies, Fujitsu, Submer, Green Revolution Cooling, LiquidCool Solutions, Asperitas, Bitfury, DCX Liquid Cooling Company, and Midas Immersion Cooling. Companies in the data center immersion cooling market are reinforcing their competitive positioning through continuous product innovation, strategic collaborations, and geographic expansion. Industry players are investing in research and development to enhance system reliability, thermal efficiency, and scalability to meet evolving high-density computing requirements. Many firms are introducing modular and turnkey solutions to simplify deployment and accelerate time to market. Strategic alliances with data center operators, colocation providers, and hyperscale customers are strengthening long-term supply agreements and expanding global reach. Businesses are also focusing on interoperability with existing infrastructure to reduce adoption barriers.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.8 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Cooling technique

- 2.2.4 Cooling fluid

- 2.2.5 Organization size

- 2.2.6 Application

- 2.3 TAM analysis, 2026-2035

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing rack power densities exceeding traditional air-cooling limits

- 3.2.1.2 Rising thermal management challenges from AI, GPU, and high-density workloads

- 3.2.1.3 Strong focus on sustainability, energy efficiency, and reduction in PUE

- 3.2.1.4 Growing deployment in hyperscale and high-performance computing environments

- 3.2.1.5 Increasing adoption among colocation providers and large enterprise data centers

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial capital investment and system design complexity

- 3.2.2.2 Maintenance, fluid handling, and operational standardization challenges

- 3.2.3 Market opportunities

- 3.2.3.1 Rapid expansion of AI, ML, and supercomputing workloads

- 3.2.3.2 Growth of edge data centers in remote and harsh operating environments

- 3.2.3.3 Innovation in dielectric fluids and increasing adoption of two-phase immersion systems

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 U.S. Department of Energy (DOE) energy efficiency guidelines

- 3.4.1.2 Environmental Protection Agency (EPA) regulations on chemicals and refrigerants

- 3.4.1.3 ASHRAE thermal guidelines for data processing environments

- 3.4.1.4 National Fire Protection Association (NFPA) standards

- 3.4.1.5 Natural Resources Canada (NRCan) energy efficiency frameworks

- 3.4.2 Europe

- 3.4.2.1 European Commission energy efficiency directives

- 3.4.2.2 EU Code of Conduct for Data Centre Energy Efficiency

- 3.4.2.3 REACH regulation for chemical substances (dielectric fluids)

- 3.4.2.4 European Chemicals Agency (ECHA) compliance

- 3.4.2.5 National environmental and building regulations across EU member states

- 3.4.3 Asia Pacific

- 3.4.3.1 Ministry of Industry and Information Technology (China) data center efficiency policies

- 3.4.3.2 China Energy Label and green data center initiatives

- 3.4.3.3 Ministry of Economy, Trade and Industry (Japan) energy efficiency programs

- 3.4.3.4 Bureau of Energy Efficiency (India) standards

- 3.4.3.5 Singapore Infocomm Media Development Authority (IMDA) green data center guidelines

- 3.4.4 Latin America

- 3.4.4.1 National energy efficiency programs for data centers

- 3.4.4.2 Environmental compliance frameworks for industrial fluids

- 3.4.4.3 Local building and electrical safety regulations

- 3.4.4.4 Sustainability standards promoted by regional infrastructure authorities

- 3.4.5 Middle East & Africa

- 3.4.5.1 GCC sustainability and energy diversification initiatives

- 3.4.5.2 Saudi Energy Efficiency Center (SEEC) regulations

- 3.4.5.3 UAE green building codes and data center sustainability mandates

- 3.4.5.4 National environmental compliance authorities across Africa

- 3.4.1 North America

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.1.1 Single-phase immersion cooling systems

- 3.7.1.2 Two-phase immersion cooling technologies

- 3.7.1.3 High-density GPU and AI-optimized tank designs

- 3.7.1.4 Integration with modular and prefabricated data centers

- 3.7.1.5 Real-time thermal monitoring and intelligent control software

- 3.7.2 Emerging technologies

- 3.7.2.1 Single-phase immersion cooling systems

- 3.7.2.2 Two-phase immersion cooling technologies

- 3.7.2.3 High-density GPU and AI-optimized tank designs

- 3.7.2.4 Integration with modular and prefabricated data centers

- 3.7.2.5 Real-time thermal monitoring and intelligent control software

- 3.7.1 Current technological trends

- 3.8 Cost breakdown analysis

- 3.8.1 Immersion tanks and containment systems

- 3.8.2 Dielectric fluid costs

- 3.8.3 Pumps, heat exchangers, and cooling distribution units

- 3.8.4 Monitoring and control software

- 3.8.5 Installation, retrofitting, and integration costs

- 3.9 Sustainability and environmental impact

- 3.9.1 Environmental impact assessment

- 3.9.2 Social impact & community benefits

- 3.9.3 Governance & corporate responsibility

- 3.9.4 Sustainable finance & investment trends

- 3.10 Consumer behavior analysis

- 3.10.1 Preference for OEM vs third-party immersion cooling systems

- 3.10.2 Preference for CAPEX vs OPEX models (full system purchase vs immersion-as-a-service models)

- 3.11 Analysis of aftermarket and service trends

- 3.11.1 Maintenance contracts and performance SLAs for immersion cooling systems

- 3.11.2 Coolant replacement cycles, fluid degradation monitoring, and hardware upgrades

- 3.11.3 Evaluation of OEM vs third-party service and support providers for immersion tanks and components

- 3.12 Analysis of digitalization and automation trends

- 3.12.1 Rise of smart immersion systems with IoT-based thermal and performance monitoring

- 3.12.2 Role of AI/ML in predictive fluid management, system optimization, and fault detection

- 3.12.3 Automation in immersion cooling system deployment, startup, and thermal balancing

- 3.12.4 Integration with DCIM (Data Center Infrastructure Management) and telemetry platforms

- 3.12.5 Digital twin applications for simulating immersion cooling performance and planning retrofits

- 3.13 Case studies and real-world deployments across hyperscale, colocation, HPC, and edge environments

- 3.14 Analysis of impact of renewable integration on data center immersion cooling design

- 3.14.1 Immersion system efficiency in hybrid energy setups (grid + solar + battery)

- 3.14.2 System-level implications of DC-powered vs AC-powered immersion infrastructure

- 3.14.3 Compatibility of immersion cooling with backup storage systems (lithium-ion, flow batteries)

- 3.14.4 Role of smart inverters and dynamic energy routing in cooling load management

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Key developments

- 4.5.1 Mergers & acquisitions

- 4.5.2 Partnerships & collaborations

- 4.5.3 New product launches

- 4.5.4 Expansion plans and funding

- 4.6 Analysis of brand comparison

- 4.6.1 Brand recognition

- 4.6.2 Partnership ecosystem

- 4.6.3 Customer service

- 4.6.4 Distribution network strength

Chapter 5 Market Estimates & Forecast, By Component, 2022 - 2035 ($Bn)

- 5.1 Key trends

- 5.2 Solution

- 5.2.1 Cooling fluids

- 5.2.2 Cooling racks/modules

- 5.2.3 Filters

- 5.2.4 Pumps

- 5.2.5 Heat exchangers

- 5.2.6 Others

- 5.3 Service

- 5.3.1 Installation & maintenance

- 5.3.2 Training & consulting

Chapter 6 Market Estimates & Forecast, By Cooling Technique, 2022 - 2035 ($Bn)

- 6.1 Key trends

- 6.2 Single phase cooling

- 6.3 Two-phase cooling

Chapter 7 Market Estimates & Forecast, By Cooling Fluid, 2022 - 2035 ($Bn)

- 7.1 Key trends

- 7.2 Mineral oil

- 7.3 Synthetic fluid

- 7.4 Fluorocarbons-based fluid

Chapter 8 Market Estimates & Forecast, By Organization Size, 2022 - 2035 ($Bn)

- 8.1 Key trends

- 8.2 SME

- 8.3 Large enterprises

Chapter 9 Market Estimates & Forecast, By Application, 2022 - 2035 ($Bn)

- 9.1 Key trends

- 9.2 Hyperscale

- 9.3 Supercomputing

- 9.4 Enterprise HPC

- 9.5 Cryptocurrency

- 9.6 Edge/5G computing

- 9.7 Others

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.2.3 Mexico

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Poland

- 10.3.7 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.4.6 Singapore

- 10.4.7 Malaysia

- 10.4.8 Indonesia

- 10.4.9 Thailand

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Argentina

- 10.5.3 Chile

- 10.5.4 Colombia

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 Saudi Arabia

- 10.6.3 South Africa

Chapter 11 Company Profiles

- 11.1 Global players

- 11.1.1 Asperitas

- 11.1.2 Dell Technologies

- 11.1.3 Fujitsu

- 11.1.4 Green Revolution Cooling (GRC)

- 11.1.5 Hewlett Packard Enterprise (HPE)

- 11.1.6 Submer

- 11.1.7 Supermicro

- 11.1.8 Vertiv

- 11.2 Regional players

- 11.2.1 Asetek

- 11.2.2 Bitfury

- 11.2.3 DCX Liquid Cooling Company

- 11.2.4 Gigabyte Technology

- 11.2.5 Inspur

- 11.2.6 LiquidCool Solutions

- 11.2.7 Midas Immersion Cooling

- 11.3 Emerging players

- 11.3.1 ExaScaler

- 11.3.2 Iceotope

- 11.3.3 JetCool

- 11.3.4 Quanta Cloud Technology (QCT)

- 11.3.5 TAICHI Immersion Cooling

雙相液冷式伺服器市場報告:趨勢、預測與競爭分析(至2035年)

雙相液冷式伺服器市場報告:趨勢、預測與競爭分析(至2035年) 全球兩相浸沒式冷卻液市場(按流體類型、系統類型、流動技術、應用和最終用戶產業分類)預測(2026-2032年)泵送式兩相冷凍系統市場(按最終用戶、應用、泵類型、蒸發器設計、分銷管道和冷媒類型分類),全球預測,2026-2032年

全球兩相浸沒式冷卻液市場(按流體類型、系統類型、流動技術、應用和最終用戶產業分類)預測(2026-2032年)泵送式兩相冷凍系統市場(按最終用戶、應用、泵類型、蒸發器設計、分銷管道和冷媒類型分類),全球預測,2026-2032年 資料中心浸沒式冷卻:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)資料中心氟化冷卻劑市場:依流體組成、相態、冷卻方式、部署配置和應用分類-全球預測,2026-2032年資料中心浸沒式冷卻液市場按冷卻液化學成分、介電類型、流體類型、資料中心類型、應用和最終用戶產業分類 - 全球預測(2026-2032 年)資料中心綠色冷卻劑市場:按冷卻劑類型、資料中心規模、部署模式、最終用戶產業和銷售管道,全球預測,2026-2032年

資料中心浸沒式冷卻:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)資料中心氟化冷卻劑市場:依流體組成、相態、冷卻方式、部署配置和應用分類-全球預測,2026-2032年資料中心浸沒式冷卻液市場按冷卻液化學成分、介電類型、流體類型、資料中心類型、應用和最終用戶產業分類 - 全球預測(2026-2032 年)資料中心綠色冷卻劑市場:按冷卻劑類型、資料中心規模、部署模式、最終用戶產業和銷售管道,全球預測,2026-2032年 全球兩相資料中心浸沒式冷卻市場:市場規模、佔有率、成長率、產業分析、依類型、應用和地區劃分的分析以及未來預測(2026-2034)

全球兩相資料中心浸沒式冷卻市場:市場規模、佔有率、成長率、產業分析、依類型、應用和地區劃分的分析以及未來預測(2026-2034) 全球資料中心浸入式冷卻液市場(至 2032 年)按技術(單相 vs. 雙相)、資料中心類型(超大規模、AI/ML、加密貨幣挖礦)、類型(礦物油、氟碳基液體、合成液體)和地區分類資料中心浸入式冷卻市場(按組件、技術類型、資料中心規模、部署類型和最終用戶分類)- 全球預測,2025 年至 2030 年

全球資料中心浸入式冷卻液市場(至 2032 年)按技術(單相 vs. 雙相)、資料中心類型(超大規模、AI/ML、加密貨幣挖礦)、類型(礦物油、氟碳基液體、合成液體)和地區分類資料中心浸入式冷卻市場(按組件、技術類型、資料中心規模、部署類型和最終用戶分類)- 全球預測,2025 年至 2030 年