|

市場調查報告書

商品編碼

2063332

無變壓器UPS:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)Transformerless UPS - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

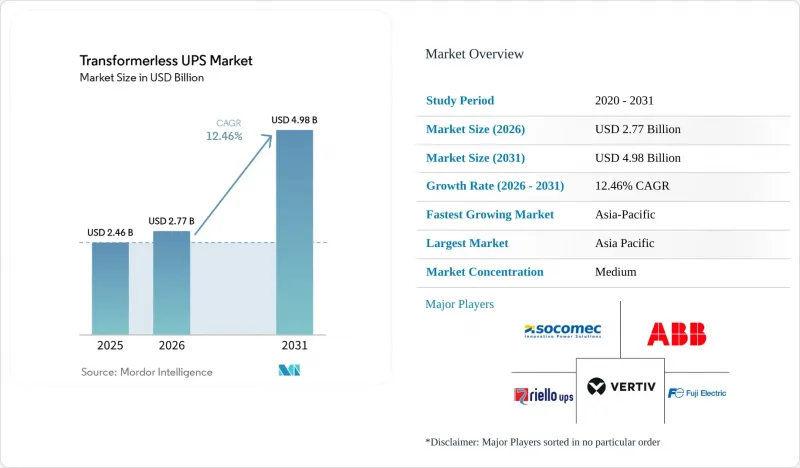

據 Mordor Intelligence 稱,2025 年無變壓器 UPS 市值為 24.6 億美元,預計到 2031 年將達到 49.8 億美元,而 2026 年為 27.7 億美元,2026 年至 2031 年預測期內的複合年成長率為 12.46%。

本報告外形規格(機架式、塔式、模組化)和地區(北美等)進行細分。市場預測以美元(USD)計價。

全球無變壓器UPS市場趨勢及洞察

擴展超大規模資料中心的容量

無變壓器UPS市場與目前的資料中心建設週期密切相關。這是因為新建的AI園區在規劃時就假定了更高的機架密度、更快的電力波動以及比傳統企業設施更低的電壓不穩定性接受度。亞馬遜於2026年4月宣布對其位於密西西比州的資料中心投資250億美元,顯示大規模的基礎設施投資仍在持續湧入新的數位容量。這對UPS供應商來說意義重大,因為高密度AI機房需要能夠快速響應、在高負載下保持效率,並且能夠適應因冷卻和開關設備需求而已經捉襟見肘的機房的保護系統。 Vertiv於2024年12月推出了一款緊湊型、高功率密度的UPS平台,專為大型資料中心設計,額定功率從250kW到1250kW不等,這表明供應商的藍圖已經開始轉向在更少的機櫃中處理更大的保護負載。 Piller也為Nebius集團在芬蘭的擴建計畫提供了200多台UPS設備。該站點已擴容至 75 兆瓦,目標 PUE 值設定在 1.1 的低水平,這反映了目前部署規模對採購決策的影響。隨著越來越多的專案向超大規模、託管和以人工智慧為中心的園區發展,無變壓器 UPS 市場越來越傾向於採用能夠支援高密度、高動態運算環境的快速響應、高頻電源架構。

人們越來越關注能源效率和總擁有成本(TCO)。

無變壓器UPS市場的擴張部分源於這樣一個事實:能源損耗正逐漸成為一個既關乎財務又關乎系統韌性的挑戰,而不再僅僅是設施團隊在安裝後需要解決的次要技術難題。 Vertiv公司報告稱,其PowerUPS 9000平台實現了高達97.5%的雙轉換效率,這反映瞭如今大型關鍵環境中對性能的期望標準,在這些環境中,電力成本和熱負荷都是重要的考慮因素。 Centiel公司表示,其PremiumTower S2在VFI模式下效率高達97.1%,在其15年的設計壽命內無需定期更換零件,從而支持了採購決策從單純基於初始成本轉向基於生命週期的決策。美國能源局關於寬能隙電力電子技術的框架也強調了先進的電力電子技術如何提高工業和併網應用的效率、功率密度和系統性能,進一步支持了新型無變壓器設計的技術可行性。從實際角度來看,這意味著無變壓器UPS市場的買家在採購時會比以往更加嚴格地權衡功率損耗、冷卻需求、維護週期和運行特性。在歐洲,歐盟生態設計指令進一步強化了這個趨勢,為許多超過10 kVA的裝置設定了嚴格的採購基準值。

系統和電池的初始投資成本高

高昂的初始成本仍然是無變壓器UPS市場的主要障礙,尤其是在涉及鋰離子電池櫃的專案中,採購價格往往是首要考慮因素,而非長期營運經濟效益。中小企業、分散式通訊業者和預算受限的機構通常面臨優先考慮初始投資最低方案的核准流程,即便更有效率的系統在整個資產生命週期中表現更佳。醫療保健產業的情況更為突出。 NFPA 99和NFPA 110對關鍵電氣系統和緊急電源提出了嚴格的性能要求,導致專案預算遠超過UPS硬體本身的成本,使得小型醫院網路更難獲得資金核准。小規模,即使鋰離子電池具有低更換頻率、快速充電、降低冷卻需求和減少維護等優勢,在預算限制和分散採購權限的限制下,這些優勢仍然難以令人信服。這種障礙在南美洲、非洲和東南亞部分地區尤其突出。這是因為,與成熟市場相比,這些地區的電池供應鏈、資金籌措方案和長期設施規劃往往不夠完善。即使營運商採取全生命週期視角,如果初始部署方案的成本超過設施核准的資本預算上限,無變壓器UPS市場也可能錯失短期訂單。

細分市場分析

到2025年,10-100 kVA功率段的無變壓器UPS將佔無變壓器UPS市場佔有率的44.02%,成為商業建築、邊緣節點、中型企業資料中心、電信基地台以及各種重複更換需求的核心。此功率段適用於需要足夠容錯能力,但又無需承擔大規模設備所需的空間、設計複雜性和資金負擔的項目。因此,無論在成熟或新興的部署環境中,它都至關重要。此外,此功率段也與許多企業和通訊業者的實際運作情況非常契合,這些系統的運作時間通常低於尖峰負載,因此能夠受益於其卓越的部分負載效率和易於管理的安裝要求。雖然10 kVA以下的功率段產品仍應用於分散式分店和小規模設施,但其小規模、效率低,限制了其影響力,因為整個無變壓器UPS市場的採購重點正在轉向生命週期成本、密度和性能。

預計到2031年,100 kVA以上的UPS市場將以12.68%的複合年成長率成長,這主要得益於人工智慧資料中心、大規模託管機房以及工業關鍵負載向兆瓦級保護需求的轉變。 Vertiv的PowerUPS 9000單機功率為250-1250 kW,並可擴展至5 MW。這表明供應商正致力於開發大規模的保護型負載模組,這些模組具有更高的機櫃密度,並適用於大規模數位化園區。一項針對500 kW SiC三相UPS的同行評審研究也表明,最佳化的濾波器和散熱設計能夠實現具有實際商業性意義的高容量運行,有助於推動向大規模無變壓器平台發展的技術進程。市場成熟度和商業產品的技術檢驗表明,隨著無變壓器UPS市場向高密度計算、大規模工業自動化和大規模關鍵設施方向發展,高功率UPS的重要性將進一步提升。

預計到2025年,三相系統將佔銷售額的66.23%,繼續在大型資料中心、工業廠房和大型商業設施的部署中發揮核心作用。在這些設施中,均衡的配電和高密度負載處理是標準設計假設。這種主導地位反映了關鍵基礎設施的現有架構,因為大型設施已經依賴優先考慮三相拓撲結構的電氣佈線佈局,強調效率、穩定性和與上下游設備的便利整合。歐洲和其他成熟市場的監管和報告環境也使這一領域受益,這些市場越來越重視更有效率的電力基礎設施。這使得在新計畫和更新周期中採用過時和低效的設備變得難以合理化。事實上,在無變壓器UPS市場,當專案規模超過小規模房間級、分公司級或單機櫃備份需求時,三相平台仍然是預設選擇。

預計到2031年,單相系統將以12.91%的複合年成長率成長,成為單相系統中成長最快的領域,這表明其在分散式數位基礎設施中的應用將會增加,而非在關鍵應用中減少。這一成長主要由5G小型基地台、邊緣運算節點、分店以及小型企業場所等驅動,在這些場所,三相電源要么不可用,要么容量過大,無法滿足實際需求。現代單相設計透過提高功率因數、提供綠能和更高的效率,縮小了傳統性能差距,從而提高了小型但對性能要求仍然較高的應用的可靠性。隨著部署範圍從少數大規模站點擴展到眾多小型站點和偏遠地區,單相產品正在擴大無變壓器UPS市場,而不是取代現有的三相系統。

區域分析

預計到2025年,亞太地區將佔據43.54%的市場佔有率,其無變壓器UPS市場預計到2031年將以12.55%的複合年成長率成長,使其成為當前預測中規模最大且成長最快的地區。這一地位反映了中國數位基礎設施規劃、日本半導體製造業的復甦以及印度數位公共基礎設施計畫的綜合影響,所有這些舉措都推動了資料中心、通訊和工業領域對高效緊湊型電源保護的新需求。該地區也受惠於便利的碳化矽(SiC)及相關電力電子價值鏈,這提高了製造成本效益,並隨著採購週期的縮短,減輕了前置作業時間壓力。這項價值鏈優勢意義重大,因為隨著大規模資料中心和通訊專案規模的擴大,買家越來越重視準時可靠性、靈活配置和成本控制。基於這些原因,亞太地區無變壓器UPS市場預計將在整個預測期內保持主要成長動力。

北美是無變壓器UPS市場第二大需求中心,主要得益於超大規模營運的擴張、電網投資以及對大型資料中心園區的持續資本投入。 2026年4月,亞馬遜宣佈在密西西比州投資250億美元建設資料中心,顯示該地區仍有大規模新的關鍵電力基礎設施正在規劃中。伊頓公司的一份報告顯示,美國私營公用事業公司計劃在未來五年內投資約4,000億美元進行電網升級,以滿足資料中心日益成長的電力需求,凸顯了數位基礎設施成長對整個系統產生的廣泛影響。歐洲仍然是一個重要的商業市場,因為能源效率法規和升級週期,尤其是在資料中心和工業領域(這些領域對營運損耗和報告義務的要求更為嚴格),持續推動商業性、高效系統的普及。因此,儘管規模不如亞太地區,歐洲在高階需求方面仍佔據核心地位。

儘管南美洲、中東和非洲的市場規模在絕對值上仍然相對較小,但5G的部署、資料中心的擴張以及電網的不穩定性正在形成與成熟地區不同的需求模式,這些地區往往更青睞緊湊高效的備用電源架構,使其具有重要的戰略意義。巴西和阿根廷仍然是南美洲的主要需求中心,而阿拉伯聯合大公國和沙烏地阿拉伯則因國家主導的數位基礎設施項目和人工智慧相關設施的建設,對三相電源的需求不斷成長。在非洲,通訊業者需要在有限的機櫃空間內實現更持久的備用電源。 UPTECH銷售的無變壓器UPS產品兼具緊湊的尺寸、高效的性能和電信級的可靠性。雖然這些新興地區目前尚未主導銷售主導地位,但它們將擴大無變壓器UPS市場的潛在基本客群,並在整個預測期內強化對更廣泛產品系列的需求。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 擴展超大規模資料中心的容量

- 重點在於提高能源效率和降低總擁有成本。

- 對更高功率密度和小型化的需求日益成長。

- 引入模組化UPS以實現分階段容量擴展

- 提高碳化矽功率級的效率

- 利用併網型UPS最佳化成本

- 市場限制因素

- 系統和電池的初始投資成本較高

- 高湧入電流和傳統環境中的負載相容性有其限制。

- 網路連接電力控制系統的網路安全風險

- 寬能隙半導體供應集中

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 額定功率

- 小於 10 千伏安

- 10~100 kVA

- 超過100千伏安

- 按階段

- 單相

- 三相

- 按最終用戶行業分類

- 資料中心

- 工業製造

- 商業建築

- 醫療機構

- 溝通

- 其他終端用戶產業

- 按外形規格

- 機架安裝型

- 塔

- 模組化的

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 其他亞太國家

- 中東

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 土耳其

- 以色列

- 其他中東國家

- 非洲

- 南非

- 埃及

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Socomec Group SA

- ABB Ltd.

- Riello Elettronica SpA

- Vertiv Group Corporation

- Fuji Electric Co., Ltd.

- Kehua Data Co., Ltd.

- Cyber Power Systems(USA), Inc.

- Centiel AG

- Borri SpA

- AEG Power Solutions BV

- Piller Group GmbH

- East Group Co., Ltd.

- INVT Power System(Shenzhen)Co., Ltd.

- Salicru SA

- BlueWalker GmbH

- BPC Energy Limited

- N1 Critical Technologies, Inc.

- Shenzhen EverExceed Industrial Co., Ltd.

- Kohler Uninterruptible Power Ltd.

- Santak Electronic(Shenzhen)Co., Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the transformerless UPS market size was valued at USD 2.46 billion in 2025 and is estimated to grow from USD 2.77 billion in 2026 to reach USD 4.98 billion by 2031, at a CAGR of 12.46% during the forecast period 2026-2031.

This report is Segmented by Power Rating (Less Than 10 KVA, 10-100 KVA, and Greater Than 100 KVA), Phase (Single-Phase, and Three-Phase), End-User Industry (Data Centers, Industrial Manufacturing, Commercial Buildings, Healthcare Facilities, Telecom, and More), Form Factor (Rack-Mounted, Tower, and Modular), and Geography (North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Transformerless UPS Market Trends and Insights

Hyperscale Data Center Capacity Expansion

The transformerless UPS market is closely tied to the current data center build cycle, because new AI campuses are being planned around higher rack density, faster power swings, and much lower tolerance for voltage instability than earlier enterprise facilities. Amazon announced in April 2026 that it will invest USD 25 billion in Mississippi data centers, which shows that very large-scale infrastructure commitments are still flowing into new digital capacity. This matters for UPS vendors because dense AI rooms require protection systems that can respond quickly, remain efficient under heavy load, and fit into power rooms already under pressure from cooling and switchgear requirements. Vertiv's December 2024 launch of a compact, high-power-density UPS platform for large data centers, with ratings from 250 kW to 1,250 kW, demonstrated that supplier roadmaps are already shifting toward larger protected loads in fewer cabinets. Piller also supplied more than 200 UPS units for Nebius Group's expansion in Finland, where the site is being expanded to 75 MW with a target PUE as low as 1.1, which reflects the deployment scale now shaping procurement decisions. As more projects move toward hyperscale, colocation, and AI-focused campuses, the transformerless UPS market is increasingly aligning with fast-response, high-frequency power architectures that can support dense, highly dynamic compute environments.

Rising Energy Efficiency And Total Cost Of Ownership Focus

The transformerless UPS market is also expanding because energy loss is now a financial issue alongside resilience, rather than a secondary technical consideration left for facility teams to solve after installation. Vertiv reported up to 97.5% double-conversion efficiency for its PowerUPS 9000 platform, which reflects the performance threshold now expected in large, critical environments where power costs and thermal loads are both under review. Centiel stated that PremiumTower S2 achieves up to 97.1% efficiency in VFI mode and avoids scheduled component replacements over a design life exceeding 15 years, supporting the move toward lifecycle-based procurement rather than first-cost decisions alone. The U.S. Department of Energy's wide-bandgap power electronics framework also highlighted how advanced power electronics can improve efficiency, power density, and system performance across industrial and grid-connected applications, which supports the technology case for newer transformerless designs. In practical terms, this means buyers in the transformerless UPS market are now weighing power loss, cooling demand, maintenance cycles, and operating profile with greater discipline than in earlier procurement cycles. In Europe, the EU Ecodesign Directive has reinforced that direction by setting a practical procurement floor for many installations above 10 kVA.

High Upfront System And Battery Capex

Upfront costs remain a real brake on the transformerless UPS market, especially when lithium-ion battery cabinets are added to projects that are still being judged mainly on acquisition price rather than long-term operating economics. Smaller enterprises, distributed telecom operators, and budget-constrained institutions often face approval processes that reward the lowest initial capital request, even when a more efficient system would perform better across the asset life. The issue becomes sharper in healthcare, where NFPA 99 and NFPA 110 set strict requirements for essential electrical systems and emergency power performance, raising the total project budget beyond UPS hardware alone and making capital approval more difficult for smaller hospital networks. That means the case for lithium-ion, lower replacement frequency, faster recharge, reduced cooling demand, and less maintenance labor, can still lose against short-budget planning and fragmented procurement authority. The barrier is most visible in South America, Africa, and parts of Southeast Asia, where battery supply depth, financing options, and long-horizon facility planning are often less developed than in mature markets. Even when operators accept the lifecycle argument, the transformerless UPS market can still lose near-term orders if the initial package exceeds the capital threshold a site can approve.

Other drivers and restraints analyzed in the detailed report include:

- Growing Preference For High Power Density And Reduced Footprint

- Modular UPS Adoption For Staged Capacity Expansion

- Load Compatibility Limits In High-Inrush And Legacy Environments

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The 10-100 kVA segment accounted for 44.02% of the transformerless UPS market in 2025, making it the volume center of demand across commercial buildings, edge nodes, mid-size enterprise data centers, telecom base stations, and a wide base of repeat replacement activity. This range fits projects that need meaningful resilience without the space commitment, engineering complexity, and capital burden associated with much larger installations, which is why it remains relevant across both mature and emerging deployment settings. It also aligns well with the practical operating profile of many enterprise and telecom sites, where systems spend long periods below peak load, thereby benefiting from strong partial-load efficiency and manageable installation requirements. The less than 10 kVA range still serves distributed branch offices and small facilities, but its smaller scale and lower efficiency limit its influence as procurement priorities shift toward lifecycle cost, density, and performance across the broader transformerless UPS market.

The more than 100 kVA segment is projected to grow at a 12.68% CAGR through 2031, supported by AI data center buildouts, large colocation halls, and industrial critical loads moving into megawatt-scale protection requirements. Vertiv's PowerUPS 9000 supports 250-1,250 kW per unit and scales to 5 MW, which shows how suppliers are targeting larger protected load blocks with higher cabinet density and a stronger fit for large digital campuses. Peer-reviewed research on a 500 kW SiC-based three-phase UPS also showed that an optimized filter and heat-dissipation design can support large-capacity operation with credible commercial relevance, helping validate the technical path for larger transformerless platforms. That combination of commercial product readiness and technical validation suggests that the upper power tier will continue to gain weight as the transformerless UPS market shifts toward high-density compute, large industrial automation, and larger critical facilities.

Three-phase systems held 66.23% of the revenue share in 2025, keeping them at the center of deployment in large data centers, industrial plants, and major commercial facilities, where balanced power distribution and higher-density load support are standard design assumptions. That lead reflects the installed architecture of critical infrastructure, because large facilities already depend on electrical layouts that favor three-phase topology for efficiency, stability, and straightforward integration with upstream and downstream equipment. The segment also benefits from a regulatory and reporting environment that increasingly rewards more efficient power infrastructure in Europe and other mature markets, making older, low-efficiency equipment harder to justify in new projects and replacement cycles. In practice, this keeps three-phase platforms as the default choice whenever projects move beyond smaller room-level, branch-level, or single-cabinet backup requirements in the transformerless UPS market.

Single-phase systems are projected to grow at a 12.91% CAGR through 2031, making them the fastest-growing phase segment and signaling wider use in distributed digital infrastructure rather than a retreat from critical applications. Growth comes from 5G small cells, edge computing nodes, branch facilities, and compact enterprise sites where three-phase supply is either unavailable or oversized relative to the installation's actual demand profile. Modern single-phase designs have narrowed earlier performance gaps through better output power factor, cleaner power delivery, and higher efficiency, thereby improving their credibility in smaller yet still sensitive applications. As deployment expands across many compact or remote sites instead of a few very large ones, single-phase products are broadening the transformerless UPS market rather than displacing the installed base of three-phase systems.

Geography Analysis

Asia-Pacific held a 43.54% share in 2025, and the regional transformerless UPS market is forecast to grow at a 12.55% CAGR through 2031, keeping the region as both the largest and the fastest-growing geography in the current outlook. This position reflects the combined effect of China's digital infrastructure programs, Japan's semiconductor-fab revival, and India's Digital Public Infrastructure agenda, all of which support new demand for efficient, compact power protection across data center, telecom, and industrial settings. The region also benefits from closer access to SiC and related power-electronics supply chains, which improves manufacturing economics and can reduce lead-time pressure as procurement cycles tighten. That supply chain advantage matters because buyers in large data center and telecom programs are placing more value on delivery reliability, flexible configuration, and cost discipline as project size continues to increase. For these reasons, the transformerless UPS market in Asia-Pacific is likely to remain the main growth engine through the forecast period.

North America forms the second major demand center in the transformerless UPS market, supported by hyperscale expansion, grid investment, and continued capital spending on large data center campuses. Amazon said in April 2026 that it would invest USD 25 billion in Mississippi data centers, signaling that significant new critical power infrastructure is still being planned in the region. Eaton reported that U.S. investor-owned utilities plan around USD 400 billion in grid upgrades over 5 years in response to rising data center power demand, underscoring the broader system impacts now surrounding digital infrastructure growth. Europe remains commercially important because efficiency regulations and replacement cycles continue to favor modern, high-efficiency systems, especially in data center and industrial settings, where operating losses and reporting obligations are taken more seriously. That keeps Europe central to premium demand, even if it does not match Asia-Pacific's scale.

South America, the Middle East, and Africa remain smaller in absolute terms, but they are strategically important because 5G rollout, colocation buildout, and grid instability are creating demand patterns that differ from mature regions and often favor compact, efficient backup architectures. Brazil and Argentina remain the main South American demand centers, while the United Arab Emirates and Saudi Arabia are generating larger three-phase requirements through state-backed digital infrastructure programs and AI-linked facility development. In Africa, telecom applications remain central because operators need longer backup capability within constrained cabinets, and UPTECH markets transformerless UPS products that combine compact size, efficiency, and telecom-grade reliability. These frontier regions will not define current revenue leadership, but they do widen the addressable base of the transformerless UPS market and strengthen the case for broader product portfolios across the forecast period.

- Socomec Group S.A.

- ABB Ltd.

- Riello Elettronica S.p.A.

- Vertiv Group Corporation

- Fuji Electric Co., Ltd.

- Kehua Data Co., Ltd.

- Cyber Power Systems (USA), Inc.

- Centiel AG

- Borri S.p.A.

- AEG Power Solutions B.V.

- Piller Group GmbH

- East Group Co., Ltd.

- INVT Power System (Shenzhen) Co., Ltd.

- Salicru S.A.

- BlueWalker GmbH

- BPC Energy Limited

- N1 Critical Technologies, Inc.

- Shenzhen EverExceed Industrial Co., Ltd.

- Kohler Uninterruptible Power Ltd.

- Santak Electronic (Shenzhen) Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Hyperscale Data Center Capacity Expansion

- 4.2.2 Rising Energy Efficiency and Total Cost of Ownership Focus

- 4.2.3 Growing Preference for High Power Density and Reduced Footprint

- 4.2.4 Modular UPS Adoption for Staged Capacity Expansion

- 4.2.5 Silicon Carbide Power Stage Efficiency Gains

- 4.2.6 Grid-Interactive Ups Use for Tariff Optimization

- 4.3 Market Restraints

- 4.3.1 High Upfront System and Battery Capex

- 4.3.2 Load Compatibility Limits in High-Inrush and Legacy Environments

- 4.3.3 Cybersecurity Exposure of Network-Connected Power Controls

- 4.3.4 Wide-Bandgap Semiconductor Supply Concentration

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Power Rating

- 5.1.1 Less than 10 kVA

- 5.1.2 10-100 kVA

- 5.1.3 Greater than 100 kVA

- 5.2 By Phase Type

- 5.2.1 Single-Phase

- 5.2.2 Three-Phase

- 5.3 By End-user Industry

- 5.3.1 Data Centers

- 5.3.2 Industrial Manufacturing

- 5.3.3 Commercial Buildings

- 5.3.4 Healthcare Facilities

- 5.3.5 Telecom

- 5.3.6 Other End-user Industries

- 5.4 By Form Factor

- 5.4.1 Rack-mounted

- 5.4.2 Tower

- 5.4.3 Modular

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 Turkey

- 5.5.5.4 Israel

- 5.5.5.5 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Egypt

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Socomec Group S.A.

- 6.4.2 ABB Ltd.

- 6.4.3 Riello Elettronica S.p.A.

- 6.4.4 Vertiv Group Corporation

- 6.4.5 Fuji Electric Co., Ltd.

- 6.4.6 Kehua Data Co., Ltd.

- 6.4.7 Cyber Power Systems (USA), Inc.

- 6.4.8 Centiel AG

- 6.4.9 Borri S.p.A.

- 6.4.10 AEG Power Solutions B.V.

- 6.4.11 Piller Group GmbH

- 6.4.12 East Group Co., Ltd.

- 6.4.13 INVT Power System (Shenzhen) Co., Ltd.

- 6.4.14 Salicru S.A.

- 6.4.15 BlueWalker GmbH

- 6.4.16 BPC Energy Limited

- 6.4.17 N1 Critical Technologies, Inc.

- 6.4.18 Shenzhen EverExceed Industrial Co., Ltd.

- 6.4.19 Kohler Uninterruptible Power Ltd.

- 6.4.20 Santak Electronic (Shenzhen) Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

不斷電系統(UPS) 市場:2026-2032 年全球市場預測(依 UPS 系統類型、容量、相數、安裝類型、應用和銷售管道)

不斷電系統(UPS) 市場:2026-2032 年全球市場預測(依 UPS 系統類型、容量、相數、安裝類型、應用和銷售管道) 可再生能源供應鏈解決方案市場預測至2034年—按解決方案類型、部署模式、技術、應用、最終用戶和地區分類的全球分析

可再生能源供應鏈解決方案市場預測至2034年—按解決方案類型、部署模式、技術、應用、最終用戶和地區分類的全球分析 UPS全球市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

UPS全球市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 不斷電系統(UPS):市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031)2026年關鍵電力領域十大成長機遇

不斷電系統(UPS):市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031)2026年關鍵電力領域十大成長機遇 不斷電系統(UPS)市場機會、成長要素、產業趨勢分析及2026-2035年預測

不斷電系統(UPS)市場機會、成長要素、產業趨勢分析及2026-2035年預測 機架式 UPS 市場:依產品類型、容量、應用、最終用戶和地區分類。

機架式 UPS 市場:依產品類型、容量、應用、最終用戶和地區分類。 無變壓器UPS市場報告:按組件、輸出、終端用戶產業及地區分類(2026-2034年)

無變壓器UPS市場報告:按組件、輸出、終端用戶產業及地區分類(2026-2034年) 2026年全球汽車不斷電系統(UPS)(車載UPS)市場報告不斷電系統(UPS)市場:按容量、類型、應用和地區分類

2026年全球汽車不斷電系統(UPS)(車載UPS)市場報告不斷電系統(UPS)市場:按容量、類型、應用和地區分類