|

市場調查報告書

商品編碼

2063277

汽車通訊技術:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Automotive Communication Technology - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

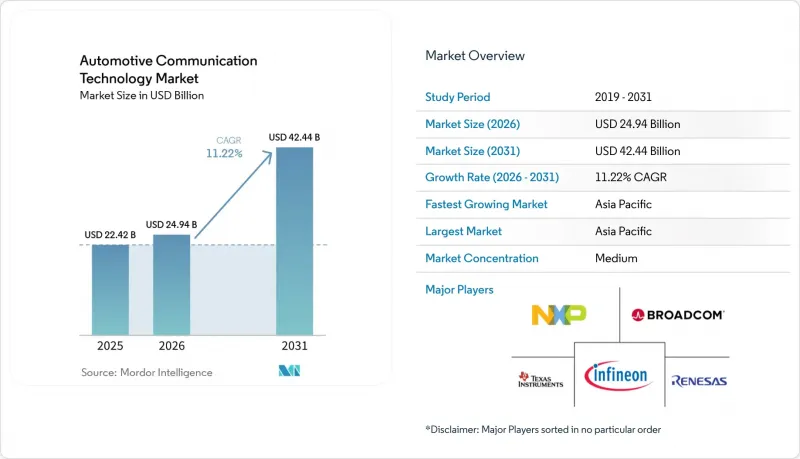

根據 Mordor Intelligence 預測,汽車通訊技術市場規模將從 2025 年的 224.2 億美元成長到 2026 年的 249.4 億美元,到 2031 年將達到 424.4 億美元,2026 年至 2031 年的複合年成長率為 11.2%。

本報告按總線模組(本地互連網路 (LIN)、控制器區域網路 (CAN) 等)、應用(動力傳動系統、車身控制和舒適性等)、通訊方式(車聯網 (V2X) 等)、車輛類型、推進系統、分銷管道和地區進行細分。市場預測以美元 (USD) 為單位。

全球汽車通訊技術市場趨勢及洞察

高級駕駛輔助系統(ADAS)的整合正在穩步推進。

攝影機、雷達和LiDAR陣列正在迅速擴展,它們產生的資料量已經超過了傳統匯流排在安全關鍵延遲限制下的傳輸能力。集中式域控制器現在能夠即時融合感測器輸入,推動汽車通訊技術市場向支援時間敏感型網路的乙太網路骨幹網路發展。全球新車評估協定越來越重視需要微秒確定性的自動轉向功能,而通訊效能也直接體現在碰撞測試結果中。組件製造商正在積極回應,推出將 CAN-XL、10BASE-T1S 和硬體安全加速器整合到單一晶片系統晶片(SoC) 收發器。隨著 ADAS 成為入門級車型的標配,頻寬需求的成長速度超過了車輛平均售價的成長速度,網路效率已成為影響 OEM 利潤率的關鍵因素。

需要乙太網路骨幹網路的基於區域的電子電氣架構的興起

在分區設計中,數十個分散式電控系統被整合到位於特定區域的少量運算節點中。這種重新佈局縮短了線束長度,簡化了電源分配,並將網路安全防禦集中在少數幾個網路入侵點上。歐洲和北美的高階OEM廠商已經檢驗了早期的分區原型,將線束重量減少了約三分之一,並提高了電池式電動車的能源效率。這種架構轉變的驅動力是多Gigabit乙太網路的普及,它現在可以透過單條雙絞線傳輸來確定性控制流量和資訊娛樂流。提供內建功能安全和時間感知整形功能的交換晶片的供應商正在被多個車型系列採用,從而加速了汽車通訊技術市場的整合。

高速網路檢驗高成本且複雜

在電磁應力和網路攻擊下驗證混合協議車載網路的安全性需要耗費大量時間進行實驗室檢驗。法規結構(OEM) 必須購買專用錯誤注入測試台,並對不熟悉乙太網路確定性的檢驗工程師進行再培訓。諸如聯合國規則 155 等監管框架增加了對持續威脅監控的要求,測試範圍遠遠超出了以往以 CAN 總線為中心的測試項目。中小型汽車製造商面臨不成比例的成本負擔,導致功能部署延遲,並暫時放緩了汽車通訊技術市場的銷售成長。雖然協作檢驗中心正在湧現以分擔設備負載,但統一最佳實踐仍面臨挑戰。

細分市場分析

2025年,控制器區域網路(CAN)繼續保持其在汽車通訊技術市場的主導地位,市場佔有率高達41.22%。這充分體現了CAN在車身和傳統動力傳動系統領域的強大影響力。預計到2031年,汽車乙太網路將以12.84%的最高複合年成長率成長,凸顯其作為下一代區域控制器骨幹網路的重要地位。目前,開發人員正在將CAN-XL與10BASE-T1S整合,以使閘道器能夠在向全乙太網路過渡的過程中轉換關鍵訊息。這種混合方案確保了平台的連續性,並允許OEM廠商在無需完全重新佈線的情況下部署高級功能。因此,提供混合協議交換器的硬體供應商是建立成本最佳化平台藍圖的關鍵合作夥伴。

乙太網路和CAN匯流排的共存正在重塑汽車通訊技術市場的供應商生態系統。一級系統整合商必須透過將乙太網路鏈路上的時間感知整形與CAN流量的閘道緩衝相結合,來證明其確定性。測試設備製造商正在透過將幀搶佔探測和CAN錯誤注入模組整合到單一主機中來應對這一挑戰,從而降低實驗室的複雜性。網路安全審計機構也正在調整其應對措施。分區網路透過減少防火牆安裝點的數量來簡化對聯合國規則155的合規性,但同時也提高了每個閘道器容錯能力的要求。

截至2025年,動力傳動系統通訊將佔汽車通訊技術市場佔有率的36.08%,但安全性和ADAS(高級駕駛輔助系統)預計將以13.15%的複合年成長率推動市場成長。這種轉變源自於緊急轉向和車道維持功能的強制實施,這些功能需要確定性的感測器融合。採用TSN調度技術的乙太網路骨幹網路可確保感知資料在微秒級的時間視窗內到達操作邏輯,從而將通訊效能提升到足以挽救生命的水平。供應商正競相將TSN硬體模組整合到微控制器中,以確保在監管過渡期限之前獲得設計上的認可。由此產生的良性創新循環正在使ADAS網路成為更廣泛的電子架構變革的領先指標。

外部V2X數據流與車載感測器套件的融合正在推動汽車通訊技術市場軟體堆疊的重構。網域控制器曾經僅用於攝影機融合,如今則分析來自路側設備的憑證鍊和威脅遙測數據,從而整合了網路安全和感知功能。地方道路管理部門正在試點依賴資料包視窗保證交付的綠燈優先通行方案,這增加了對確定性網路的需求。因此,動力傳動系統工程師正在採用乙太網路技術,透過將再生煞車和溫度控管子系統與ADAS輸入同步,來最大限度地減少電動車的能量損耗。

區域分析

預計到2025年,亞太地區將佔據全球汽車通訊技術市場47.14%的佔有率,並在2031年之前以12.06%的複合年成長率持續成長。這主要得益於中國大規模的車路雲互聯示範項目,以及韓國將智慧型運輸系統(ITS)整合到國家碰撞測試中的舉措。中國強制性的GB 44495標準要求基於認證的V2X安全,這促使整車製造商(OEM)採用以太網骨幹網,從而在國內創造了巨大的商機。在日本,政府主導的試點計畫透過將技術回饋納入採購標準,加快了供應商的準備工作。韓國的雙模V2X平台透過連接蜂巢網路和專用短程通訊(DSRC)車輛,緩解了轉型過程中的挑戰。印度豪華車型開始採用100BASE-T1技術,預示著該技術將逐步走向主流應用。

在歐洲和北美,儘管部署速度較慢,但根據聯合國第155號和第156號條例,協調性更強。這兩項條例將網路安全和軟體更新管理納入了型號核准清單。美國聯邦通訊委員會(FCC)決定開放5.9 GHz頻段用於蜂窩車聯網(V2X),消除了頻寬的不確定性,使原始設備製造商(OEM)能夠最終確定其單模無線產品藍圖。德國供應商對IEEE工作小組有著顯著的影響力,體現了歐洲在延遲和安全觀點,並影響全球乙太網路標準。儘管其他地區的監管存在差異,英國仍遵守聯合國條例,從而維持了跨區域零件的兼容性。北美的測試走廊,例如密西根州道路測試場地,提供了真實世界的數據,縮短了檢驗週期。

在新興地區,企業並未自行製定標準,而是採用進口的電氣架構,雖然降低了檢驗成本,但也延緩了特定區域功能集的實施。巴西的組裝廠已經在使用整合乙太網路閘道的歐盟標準平台,而阿拉伯聯合大公國僅強制要求豪華轎車採用V2X技術。南非的出口基地正在整合乙太網路以迎合歐洲出口市場,儘管當地買家仍然偏愛基本的CAN總線。俄羅斯汽車製造商保持與CAN-FD的兼容性,以確保未來能夠重新融入西方供應鏈。在所有非核心地區,汽車通訊技術市場的成長主要依靠技術滲透,而非高調的試驗計畫。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- ADAS(進階駕駛輔助系統)整合方面的進展

- 對高頻寬資訊娛樂的需求日益成長

- 需要乙太網路骨幹網路的基於區域的電子電氣架構的興起

- 原始設備製造商向軟體定義汽車和OTA通訊的轉型

- 嚴格的排放氣體和安全法規正在推動電子設備的廣泛應用。

- 在確定性汽車乙太網路中採用時間敏感網路 (TSN)

- 市場限制因素

- 高速網路檢驗成本高成本且複雜

- 汽車用多GigabitPHY半導體供不應求

- V2X協定中的網路安全漏洞

- 傳統 CAN/LIN 與新型乙太網路之間互通性的挑戰。

- 價值供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

第5章 市場規模與成長預測

- 總線模組

- 本地互連網路(LIN)

- 控制器區域網路(CAN)

- FlexRay

- 媒體導向系統傳輸(MOST)

- 汽車乙太網路

- 透過使用

- 動力傳動系統

- 身體控制和舒適度

- 資訊娛樂和通訊

- 安全/ADAS

- 依溝通類型

- Vehicle-to-Vehicle(V2V)

- Vehicle-to-Infrastructure(V2I)

- Vehicle-to-Everything(V2X)

- 車輛類型

- 搭乘用車

- 輕型商用車

- 中型和大型商用車輛

- 依推進類型

- 內燃機(ICE)

- 電池式電動車(BEV)

- 混合動力電動車(HEV)

- 插電式混合動力車(PHEV)

- 燃料電池汽車(FCEV)

- 透過分銷管道

- 目的地設備製造商 (OEM)

- 售後市場

- 按地區

- 北美洲

- 美國

- 加拿大

- 其他北美國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 英國

- 德國

- 西班牙

- 義大利

- 法國

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 印度

- 中國

- 日本

- 韓國

- 其他亞太國家

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 土耳其

- 埃及

- 南非

- 其他中東和非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- NXP Semiconductors NV

- Broadcom Inc.

- Texas Instruments Inc.

- Infineon Technologies AG

- Renesas Electronics Corporation

- Robert Bosch GmbH

- Continental AG

- Denso Corporation

- Qualcomm Incorporated

- STMicroelectronics NV

- Microchip Technology Inc.

- Aptiv plc

- HARMAN International

- Vector Informatik GmbH

- Molex LLC(Koch Industries)

- TE Connectivity plc

- ON Semiconductor Corporation

- Analog Devices, Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the automotive communication technology market size is expected to grow from USD 22.42 billion in 2025 to USD 24.94 billion in 2026 and is forecast to reach USD 42.44 billion by 2031 at an 11.22% CAGR over 2026-2031.

This report is Segmented by Bus Module (Local Interconnect Network (LIN), Controller Area Network (CAN), and More), Application (Powertrain, Body Control and Comfort, and More), Communication Type (Vehicle-To-Everything (V2X) and More), Vehicle Type, Propulsion Type, Distribution Channel, and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Automotive Communication Technology Market Trends and Insights

Rising Integration of Advanced Driver-Assistance Systems (ADAS)

Cameras, radar, and lidar arrays are scaling rapidly, and the data they generate exceeds what legacy buses can transport within safety-critical latency windows. Centralized domain controllers now fuse perception inputs in real time, pushing the automotive communication technology market toward Ethernet backbones that support time-sensitive networking. Global New Car Assessment protocols increasingly award points for automated steering features that require microsecond-level determinism, embedding communication performance directly into crash-test outcomes. Component makers reply with system-on-chip transceivers that combine CAN-XL, 10BASE-T1S, and hardware security accelerators on a single die. As ADAS becomes standard even in entry-level trims, bandwidth demand expands faster than average vehicle selling prices, making network efficiency pivotal to OEM margins.

Emergence of Zonal E/E Architectures Requiring Ethernet Backbones

Zonal designs collapse dozens of distributed electronic control units into a handful of regionally placed compute nodes. This re-layout shortens harnesses, simplifies power distribution, and concentrates cybersecurity defenses at a few network ingress points. Premium OEMs in Europe and North America have validated early zonal prototypes that reduce wiring mass by roughly one-third, improving energy efficiency in battery-electric vehicles. The architectural shift dovetails with the adoption of multi-gigabit Ethernet, as a single twisted pair can now carry both deterministic control traffic and infotainment streams. Suppliers that deliver switch silicon with built-in functional safety and time-aware shaping win design slots across multiple vehicle lines, catalyzing consolidation inside the automotive communication technology market.

High Cost and Complexity of Validating High-Speed Networks

Proving that a mixed-protocol vehicle network remains safe under electromagnetic stress and cyberattack involves time-consuming lab campaigns. OEMs must purchase specialized error-injection benches and retrain validation engineers unfamiliar with Ethernet determinism. Regulatory frameworks such as UN Regulation 155 add continuous threat-monitoring requirements, extending test scopes well past those of earlier CAN-centric programs. Smaller automakers face disproportionate cost burdens, which delay feature introductions and temporarily restrain volume growth in the automotive communication technology market. Collaborative validation hubs are emerging to share equipment loads, but best-practice harmonization remains elusive.

Other drivers and restraints analyzed in the detailed report include:

- OEM Shift Toward Software-Defined Vehicles and OTA Communication

- Adoption of Time-Sensitive Networking (TSN) for Deterministic Automotive Ethernet

- Limited Supply of Automotive-Grade Multi-Gig PHY Semiconductors

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Controller Area Network retained the largest 41.22% of the automotive communication technology market share in 2025, a testament to its entrenched presence in body and legacy powertrain domains. Automotive Ethernet is forecast to record the fastest CAGR of 12.84% through 2031, underscoring its role as the spine of next-generation zone controllers. Developers now integrate CAN-XL alongside 10BASE-T1S so that gateways can translate critical messages during staged migrations toward full Ethernet. This hybrid approach safeguards platform continuity and lets OEMs roll out advanced features without wholesale rewiring. Hardware vendors that supply mixed-protocol switches are therefore indispensable allies for cost-optimized platform roadmaps.

The coexistence of Ethernet and CAN reshapes supplier ecosystems inside the automotive communication technology market. Tier-1 system integrators must demonstrate determinism by combining time-aware shaping on Ethernet links with gateway buffering for CAN traffic. Test-equipment makers respond by bundling frame-preemption probes and CAN error-injection modules into single consoles, reducing laboratory complexity. Cybersecurity auditors also adjust: a zonal network permits firewalling at fewer ingress points, simplifying compliance with UN Regulation 155 yet raising the stakes for each gateway's resilience.

Powertrain communication commanded a 36.08% of the automotive communication technology market share in 2025, but safety and advanced driver-assistance systems are projected to lead growth with a 13.15% CAGR. This inversion springs from mandates for emergency steering and lane-keeping that require deterministic sensor fusion. Ethernet backbones with TSN scheduling ensure that perception data reaches actuation logic within microsecond windows, elevating communication performance to life-critical status. Suppliers race to embed TSN hardware blocks into microcontrollers to secure design wins ahead of regulation-driven cut-over dates. The resulting innovation loop positions ADAS networking as the bellwether for broader electronic-architecture change.

Convergence between external V2X feeds and on-board sensor suites is reshaping software stacks in the automotive communication technology market. Domain controllers once dedicated to camera fusion now parse certificate chains and threat telemetry from roadside units, blending cybersecurity with perception. Local road agencies pilot green-light priority schemes that rely on guaranteed packet-delivery windows, reinforcing demand for deterministic networks. As a corollary, powertrain engineers adopt Ethernet to synchronize regenerative braking and thermal subsystems with ADAS inputs, minimizing energy loss in electric vehicles.

Geography Analysis

Asia-Pacific commanded a 47.14% of the automotive communication technology market share in 2025 and is expected to expand at a 12.06% CAGR through 2031, propelled by China's large-scale vehicle-road-cloud pilots and South Korea's integration of cooperative intelligent transport systems into national crash tests. China's mandatory GB 44495 rule requires certificate-based V2X security and pushes OEMs toward Ethernet backbones, creating a vast domestic pipeline of opportunities. Japan's ministry-backed pilots feed technical feedback into procurement standards, accelerating supplier readiness. South Korea's dual-mode V2X platform eases transition pains by bridging cellular and DSRC vehicles. India's premium models begin to specify 100BASE-T1, foreshadowing gradual mainstream diffusion.

Europe and North America adopt a more coordinated, but slower, rollout under the umbrella of UN Regulations 155 and 156, which embed cybersecurity and software-update management into type-approval checklists. The FCC's decision to clear the 5.9 GHz band for cellular V2X removed spectrum uncertainty, permitting OEMs to finalize single-mode radio roadmaps. Germany's supplier base exerts outsized influence on IEEE working groups, injecting European latency and safety perspectives into global Ethernet standards. The United Kingdom follows UN regulations despite regulatory divergence elsewhere, preserving cross-channel parts interchangeability. North American test corridors, such as Michigan's open-road labs, provide real-world data that shorten validation cycles.

Emerging regions adopt imported electrical architectures rather than crafting bespoke standards, saving validation costs but deferring the implementation of localized feature sets. Brazil's assembly plants build on EU-spec platforms that already contain Ethernet gateways, while the United Arab Emirates mandates V2X only for premium limousine fleets. South African export hubs are integrating Ethernet to serve European destination markets, even though local buyers still favor basic CAN. Russian carmakers maintain CAN-FD compatibility to ensure eventual reintegration with Western supply chains. Across all non-core geographies, the automotive communication technology market grows via technology trickle-down rather than headline-grabbing pilot programs.

- NXP Semiconductors N.V.

- Broadcom Inc.

- Texas Instruments Inc.

- Infineon Technologies AG

- Renesas Electronics Corporation

- Robert Bosch GmbH

- Continental AG

- Denso Corporation

- Qualcomm Incorporated

- STMicroelectronics N.V.

- Microchip Technology Inc.

- Aptiv plc

- HARMAN International

- Vector Informatik GmbH

- Molex LLC (Koch Industries)

- TE Connectivity plc

- ON Semiconductor Corporation

- Analog Devices, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Integration of Advanced Driver-Assistance Systems (ADAS)

- 4.2.2 Increasing Demand for High-Bandwidth Infotainment

- 4.2.3 Emergence of Zonal E/E Architectures Requiring Ethernet Backbones

- 4.2.4 OEM Shift Toward Software-Defined Vehicles and OTA Communication

- 4.2.5 Stringent Emission and Safety Regulations Boosting Electronic Content

- 4.2.6 Adoption of Time-Sensitive Networking (TSN) for Deterministic Automotive Ethernet

- 4.3 Market Restraints

- 4.3.1 High Cost and Complexity of Validating High-Speed Networks

- 4.3.2 Limited Supply of Automotive-Grade Multi-Gig PHY Semiconductors

- 4.3.3 Cyber-Security Vulnerabilities in V2X Protocols

- 4.3.4 Legacy CAN/LIN and New Ethernet Interoperability Challenges

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Bus Module

- 5.1.1 Local Interconnect Network (LIN)

- 5.1.2 Controller Area Network (CAN)

- 5.1.3 FlexRay

- 5.1.4 Media-Oriented Systems Transport (MOST)

- 5.1.5 Automotive Ethernet

- 5.2 By Application

- 5.2.1 Powertrain

- 5.2.2 Body Control and Comfort

- 5.2.3 Infotainment and Communication

- 5.2.4 Safety and ADAS

- 5.3 By Communication Type

- 5.3.1 Vehicle-to-Vehicle (V2V)

- 5.3.2 Vehicle-to-Infrastructure (V2I)

- 5.3.3 Vehicle-to-Everything (V2X)

- 5.4 By Vehicle Type

- 5.4.1 Passenger Vehicles

- 5.4.2 Light Commercial Vehicles

- 5.4.3 Medium and Heavy Commercial Vehicles

- 5.5 By Propulsion Type

- 5.5.1 Internal Combustion Engine (ICE)

- 5.5.2 Battery Electric Vehicle (BEV)

- 5.5.3 Hybrid Electric Vehicle (HEV)

- 5.5.4 Plug-in Hybrid Electric Vehicle (PHEV)

- 5.5.5 Fuel-Cell Electric Vehicle (FCEV)

- 5.6 By Distribution Channel

- 5.6.1 Original Equipment Manufacturer (OEM)

- 5.6.2 Aftermarket

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Rest of North America

- 5.7.2 South America

- 5.7.2.1 Brazil

- 5.7.2.2 Argentina

- 5.7.2.3 Rest of South America

- 5.7.3 Europe

- 5.7.3.1 United Kingdom

- 5.7.3.2 Germany

- 5.7.3.3 Spain

- 5.7.3.4 Italy

- 5.7.3.5 France

- 5.7.3.6 Russia

- 5.7.3.7 Rest of Europe

- 5.7.4 Asia-Pacific

- 5.7.4.1 India

- 5.7.4.2 China

- 5.7.4.3 Japan

- 5.7.4.4 South Korea

- 5.7.4.5 Rest of Asia-Pacific

- 5.7.5 Middle East and Africa

- 5.7.5.1 United Arab Emirates

- 5.7.5.2 Saudi Arabia

- 5.7.5.3 Turkey

- 5.7.5.4 Egypt

- 5.7.5.5 South Africa

- 5.7.5.6 Rest of Middle East and Africa

- 5.7.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 NXP Semiconductors N.V.

- 6.4.2 Broadcom Inc.

- 6.4.3 Texas Instruments Inc.

- 6.4.4 Infineon Technologies AG

- 6.4.5 Renesas Electronics Corporation

- 6.4.6 Robert Bosch GmbH

- 6.4.7 Continental AG

- 6.4.8 Denso Corporation

- 6.4.9 Qualcomm Incorporated

- 6.4.10 STMicroelectronics N.V.

- 6.4.11 Microchip Technology Inc.

- 6.4.12 Aptiv plc

- 6.4.13 HARMAN International

- 6.4.14 Vector Informatik GmbH

- 6.4.15 Molex LLC (Koch Industries)

- 6.4.16 TE Connectivity plc

- 6.4.17 ON Semiconductor Corporation

- 6.4.18 Analog Devices, Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

汽車通訊技術市場:按通訊方式、組件、車輛類型、應用、最終用戶、國家和地區分類-全球產業分析、市場規模、市場佔有率及2026年至2033年預測

汽車通訊技術市場:按通訊方式、組件、車輛類型、應用、最終用戶、國家和地區分類-全球產業分析、市場規模、市場佔有率及2026年至2033年預測 汽車通訊市場:按通訊方式、網路協定、組件、應用和車輛類型分類-2026-2032年全球市場預測

汽車通訊市場:按通訊方式、網路協定、組件、應用和車輛類型分類-2026-2032年全球市場預測 汽車通訊技術市場預測至2034年:全球分析(按通訊方式、車輛類型、通訊網路、推進系統、應用、最終用戶和地區分類)

汽車通訊技術市場預測至2034年:全球分析(按通訊方式、車輛類型、通訊網路、推進系統、應用、最終用戶和地區分類) 全球汽車通訊技術市場

全球汽車通訊技術市場 2026年全球拖車鉤線束模組市場報告2026年全球汽車通訊技術市場報告

2026年全球拖車鉤線束模組市場報告2026年全球汽車通訊技術市場報告 下一代汽車無線通訊技術及汽車通訊模組產業(2026)

下一代汽車無線通訊技術及汽車通訊模組產業(2026) 汽車安全元件(eSE)市場規模、佔有率及預測:依 eSE 架構、安全認證(通用標準)、應用(數位金鑰、支付)和整合劃分 - 全球預測(2026-2036)全球汽車安全元件晶片市場:依車輛類型、安全應用、整合類型、最終用戶、技術、安全功能和地區劃分-市場規模、趨勢分析、行業趨勢、機會分析和預測(2026-2035 年)

汽車安全元件(eSE)市場規模、佔有率及預測:依 eSE 架構、安全認證(通用標準)、應用(數位金鑰、支付)和整合劃分 - 全球預測(2026-2036)全球汽車安全元件晶片市場:依車輛類型、安全應用、整合類型、最終用戶、技術、安全功能和地區劃分-市場規模、趨勢分析、行業趨勢、機會分析和預測(2026-2035 年) 汽車通訊技術市場機會、成長要素、產業趨勢分析及預測(2026年至2035年)

汽車通訊技術市場機會、成長要素、產業趨勢分析及預測(2026年至2035年)