|

市場調查報告書

商品編碼

1928981

汽車通訊技術市場機會、成長要素、產業趨勢分析及預測(2026年至2035年)Automotive Communication Technology Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

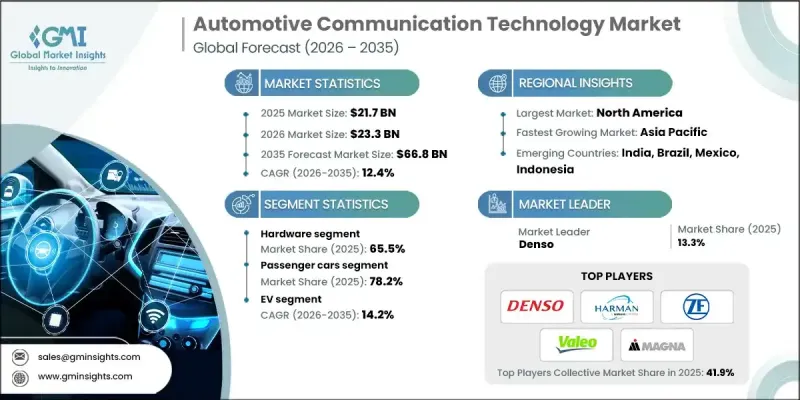

全球汽車通訊技術市場預計到 2025 年將達到 217 億美元,到 2035 年將達到 668 億美元,年複合成長率為 12.4%。

市場擴張的驅動力在於汽車向聯網汽車和數據密集型汽車的轉型。汽車製造商和供應商正在加速採用相關技術,使車輛能夠彼此通訊、與基礎設施通訊以及與雲端服務通訊。這包括遠端資訊處理控制單元和網路模組等實體組件,以及支援互聯服務的軟體平台。下一代互聯解決方案正在開發中,以滿足日益成長的數據需求並提升車內體驗。相關人員正在全球範圍內協調標準和通訊協定,以確保車輛符合不同市場的安全、性能和合規性要求。從傳統網路向以乙太網路為基礎的系統過渡,以及採用區域架構,有助於管理現代車輛中日益增多的感測器、攝影機和控制器。車隊營運商和汽車製造商正在利用遠端資訊處理和即時數據來最佳化維護、提高效率並降低營運成本,從而提升互聯技術的價值。

| 市場覆蓋範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測年份 | 2026-2035 |

| 起始值 | 217億美元 |

| 預測金額 | 668億美元 |

| 複合年成長率 | 12.4% |

預計到2025年,硬體部分將佔汽車通訊市場佔有率的65.5%。硬體在汽車通訊中仍然至關重要,包括電子控制單元(ECU)、收發器、線束、閘道器、感測器、連接器等。隨著車輛整合更多用於高級駕駛輔助系統(ADAS)、資訊娛樂系統和動力傳動系統管理的先進電子系統,對強大通訊硬體的需求日益成長。這些組件無法被軟體取代,對於可靠的車載網路和資料流至關重要。

預計到2025年,乘用車市場將佔據78.2%的市場佔有率,到2035年市場規模將達到495億美元。該細分市場主導,是因為乘用車是大規模生產的,並且能夠快速採用新的通訊技術。諸如V2X、車載資訊系統和先進的車載網路等功能正逐漸成為標配或中檔配置,從而提升了大眾市場車輛的安全性能、資訊娛樂系統和駕駛輔助功能。

美國汽車通訊技術市場預計到2025年將達到55億美元。美國的一大趨勢是車聯網(V2X)通訊技術的日益普及,該技術允許車輛與基礎設施、其他車輛和網路交換資訊。這項技術正被大力推廣,旨在提升安全性和交通管理水平,並得到了智慧城市計畫和試驗計畫的支持。汽車製造商和科技公司在推廣V2X技術的同時,也保留了CAN和LIN等傳統汽車通訊協定以及以乙太網路為基礎的新型系統。

目錄

第1章調查方法

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 成本結構

- 每個階段的附加價值

- 影響價值鏈的因素

- 中斷

- 產業影響因素

- 促進要素

- 車輛電氣化和軟體定義車輛的進展

- 擴展ADAS(高級駕駛輔助系統)的整合

- 車載資訊娛樂和互聯功能的需求日益成長

- 向自動駕駛和半自動駕駛汽車的過渡

- 產業潛在風險與挑戰

- 網路整合和互通性的複雜性

- 網路安全和資料隱私問題

- 市場機遇

- V2X(車聯網)通訊的發展

- 擴大5G相容汽車網路的應用

- 不斷擴大的電動和自動駕駛商用車

- 人工智慧驅動的車載數據處理的整合

- 促進要素

- 成長潛力分析

- 監管環境

- 北美洲

- 美國汽車工程師協會 (SAE) J2735

- 電氣及電子工程師學會(IEEE)

- 專用短程通訊(DSRC)通訊協定

- 歐洲

- 歐洲電訊標準協會(ETSI)

- 蜂窩車聯網(C-V2X)通訊標準

- 亞太地區

- 車輛網路通訊協定(中國)

- 汽車業標準 140(AIS 140,印度)

- 拉丁美洲

- 電訊建議

- ISO 21217

- 中東和非洲

- SHC 801 - 自動駕駛車輛要求

- 國家電動車政策

- 北美洲

- 波特分析

- PESTEL 分析

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 成本細分分析

- 永續性和環境影響

- 環境影響評估

- 社會影響力和社區服務

- 公司管治與企業社會責任

- 永續金融與投資趨勢

- 案例研究

- 未來前景與機遇

- 汽車電子電氣架構的演變

- 分散式、領域特定和區域特定架構

- 對車載網路通訊協定的影響

- 降低了ECU和線束的複雜性

- OEM藍圖時間表(2025-2035)

- 通訊協定效能基準測試

- 軟體定義車輛(SDV)可行性分析

第4章 競爭情勢

- 介紹

- 公司市佔率分析

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 戰略展望矩陣

- 重大進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 企業擴張計畫和資金籌措

第5章 按組件分類的市場估算與預測,2022-2035年

- 硬體

- 收發器

- 連接器和電纜

- 閘道器和網域控制器

- 軟體

- 服務

第6章 依總線模組分類的市場估算與預測,2022-2035年

- 本地互連網路(LIN)

- 控制器區域網路(CAN)

- FlexRay

- 面向媒體的系統傳輸(MOST)

- 乙太網路

第7章 依連接方式分類的市場估計與預測,2022-2035年

- 車載/內部通訊技術

- 對外通訊技術

第8章 按車輛類型分類的市場估算與預測,2022-2035年

- 搭乘用車

- 掀背車

- SUV

- 轎車

- 商用車輛

- 輕型商用車(LCV)

- MCV

- 重型商用車(HCV)

第9章 依車輛類型分類的市場估計與預測,2022-2035年

- 經濟

- 中型車

- 奢華

第10章 依推進方式分類的市場估計與預測,2022-2035年

- 內燃機(ICE)

- 電動車(EV)

- 混合

第11章 按應用領域分類的市場估算與預測,2022-2035年

- 動力傳動系統和底盤

- 身體控制和舒適度

- 資訊娛樂和車載資訊系統

- 安全/ADAS

- 其他

第12章 依銷售管道分類的市場估計與預測,2022-2035年

- OEM

- 售後市場

第13章 2022-2035年各地區市場估算與預測

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐國家

- 比荷盧經濟聯盟

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- ANZ

- 新加坡

- 馬來西亞

- 印尼

- 越南

- 泰國

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 哥倫比亞

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

第14章:公司簡介

- 世界公司

- Robert Bosch

- Continental

- NXP Semiconductors

- Infineon

- Denso

- Qualcomm

- STMicroelectronics

- Texas Instruments

- Renesas Electronics

- Intel

- Harman International

- Broadcom

- ON Semiconductor

- ZF Friedrichshafen

- Valeo

- Magna

- Mitsubishi Electric

- Aptiv

- Yazaki

- Autoliv

- 當地公司

- Vector Informatik

- Melexis

- TTTech Auto

- Autotalks

- Cohda Wireless

- LG Electronics

- Lear Corporation

- Delphi Technologies

- 新興企業

- iWave Systems

- Marben Products

- Danlaw

- Ficosa Internacional

The Global Automotive Communication Technology Market was valued at USD 21.7 billion in 2025 and is estimated to grow at a CAGR of 12.4% to reach USD 66.8 billion by 2035.

The market's expansion is driven by the shift toward connected and data-intensive vehicles. Automakers and suppliers are increasingly adopting technologies that enable vehicles to communicate with each other, infrastructure, and cloud-based services. This includes both physical components, such as telematics control units and network modules, and software platforms that support connected services. Next-generation connectivity solutions are being developed to handle growing data requirements and enhance in-vehicle experiences. Industry stakeholders are aligning standards and communication protocols globally to ensure vehicles meet safety, performance, and compliance requirements across different markets. The move from legacy networks to high-speed Ethernet-based systems, along with zonal architectures, helps manage the increasing number of sensors, cameras, and controllers in modern vehicles. Fleet operators and automakers are leveraging telematics and real-time data to optimize maintenance, improve efficiency, and reduce operating costs, reinforcing the value of connected technologies.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $21.7 Billion |

| Forecast Value | $66.8 Billion |

| CAGR | 12.4% |

The hardware segment held a 65.5% share in 2025. Hardware remains critical to automotive communication, encompassing ECUs, transceivers, wiring harnesses, gateways, sensors, and connectors. As vehicles incorporate advanced electronic systems for ADAS, infotainment, and powertrain management, the need for robust communication hardware has intensified. These components cannot be replaced by software and are essential for reliable in-vehicle networking and data flow.

The passenger cars segment accounted for 78.2% share in 2025 and is expected to reach USD 49.5 billion by 2035. The segment leads because passenger vehicles are produced in large volumes and rapidly adopt new communication technologies. Features like V2X, telematics, and advanced in-vehicle networking are becoming standard or mid-range options, enhancing safety, infotainment, and driver assistance across mass-market vehicles.

U.S. Automotive Communication Technology Market reached USD 5.5 billion in 2025. A key trend in the U.S. is the increasing deployment of vehicle-to-everything (V2X) communication, allowing vehicles to exchange information with infrastructure, other vehicles, and networks. This technology is being promoted to enhance safety and traffic management, supported by smart city initiatives and pilot programs. Automakers and tech companies are advancing V2X while still maintaining traditional in-vehicle protocols such as CAN, LIN, and newer Ethernet-based systems.

Major companies in the Global Automotive Communication Technology Market include Mitsubishi Electric, Yazaki, Aptiv, Harman International, Lear, ZF Friedrichshafen, Magna, Valeo, Denso, and Autoliv. To strengthen presence, companies in the Automotive Communication Technology Market are focusing on innovation in high-speed connectivity, telematics, and in-vehicle networking solutions. They are investing heavily in R&D to improve system reliability, data handling, and integration with ADAS and infotainment systems. Strategic partnerships with automakers and semiconductor providers help accelerate adoption and expand global reach. Firms are standardizing protocols, offering modular platforms, and aligning with regulatory requirements to enhance cross-market compatibility. Additionally, companies are leveraging software updates, predictive maintenance, and real-time data analytics to increase client retention, optimize vehicle performance, and ensure long-term competitiveness in a rapidly evolving connected vehicle landscape.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.8 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Bus Module

- 2.2.4 Connectivity

- 2.2.5 Vehicle

- 2.2.6 Vehicle Class

- 2.2.7 Propulsion

- 2.2.8 Application

- 2.2.9 Sales Channel

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising vehicle electrification and software-defined vehicles

- 3.2.1.2 Growing integration of advanced driver assistance systems (ADAS)

- 3.2.1.3 Increasing demand for in-vehicle infotainment and connectivity

- 3.2.1.4 Shift toward autonomous and semi-autonomous vehicles

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Complexity of network integration and interoperability

- 3.2.2.2 Cybersecurity and data privacy concerns

- 3.2.3 Market opportunities

- 3.2.3.1 Growth of vehicle-to-everything (V2X) communication

- 3.2.3.2 Increasing adoption of 5G-enabled automotive networks

- 3.2.3.3 Expansion of electric and autonomous commercial vehicles

- 3.2.3.4 Integration of AI-driven in-vehicle data processing

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 Society of Automotive Engineers (SAE) J2735

- 3.4.1.2 Institute of Electrical and Electronics Engineers (IEEE)

- 3.4.1.3 Dedicated Short Range Communications (DSRC) Protocol

- 3.4.2 Europe

- 3.4.2.1 European Telecommunications Standards Institute (ETSI)

- 3.4.2.2 Cellular Vehicle-to-Everything (C-V2X) Communication Standard

- 3.4.3 Asia Pacific

- 3.4.3.1 Vehicle Network Communication Protocol (China)

- 3.4.3.2 Automotive Industry Standard 140 (AIS 140, India)

- 3.4.4 Latin America

- 3.4.4.1 International Telecommunication Union Recommendation

- 3.4.4.2 ISO 21217

- 3.4.5 Middle East & Africa

- 3.4.5.1 SHC 801 - Autonomous Vehicles Requirements

- 3.4.5.2 The National Electric Vehicles Policy

- 3.4.1 North America

- 3.5 Porter';s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Cost breakdown analysis

- 3.9 Sustainability and environmental impact

- 3.9.1 Environmental impact assessment

- 3.9.2 Social impact & community benefits

- 3.9.3 Governance & corporate responsibility

- 3.9.4 Sustainable finance & investment trends

- 3.10 Case studies

- 3.11 Future outlook & opportunities

- 3.12 Evolution of Automotive E/E Architectures

- 3.12.1 Distributed, Domain and Zonal architectures

- 3.12.2 Impact on in-vehicle networking protocols

- 3.12.3 Reduction in ECUs & wiring harness complexity

- 3.12.4 OEM roadmap timelines (2025-2035)

- 3.13 Communication Protocol Performance Benchmarking

- 3.14 Software-Defined Vehicle (SDV) Enablement Analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Component, 2022 - 2035 ($Bn)

- 5.1 Key trends

- 5.2 Hardware

- 5.2.1 Transceivers

- 5.2.2 Connectors & Cables

- 5.2.3 Gateways & Domain Controllers

- 5.3 Software

- 5.4 Services

Chapter 6 Market Estimates & Forecast, By Bus Module, 2022 - 2035 ($Bn)

- 6.1 Key trends

- 6.2 Local Interconnect Network (LIN)

- 6.3 Controller Area Network (CAN)

- 6.4 FlexRay

- 6.5 Media Oriented Systems Transport (MOST)

- 6.6 Ethernet

Chapter 7 Market Estimates & Forecast, By Connectivity, 2022 - 2035 ($Bn)

- 7.1 Key trends

- 7.2 In-vehicle/Internal communication technology

- 7.3 External communication technology

Chapter 8 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Bn)

- 8.1 Key trends

- 8.2 Passenger cars

- 8.2.1 Hatchback

- 8.2.2 SUV

- 8.2.3 Sedan

- 8.3 Commercial vehicles

- 8.3.1 LCV

- 8.3.2 MCV

- 8.3.3 HCV

Chapter 9 Market Estimates & Forecast, By Vehicle Class, 2022 - 2035 ($Bn)

- 9.1 Key trends

- 9.2 Economy

- 9.3 Mid-range

- 9.4 Luxury

Chapter 10 Market Estimates & Forecast, By Propulsion, 2022 - 2035 ($Bn)

- 10.1 Key trends

- 10.2 ICE

- 10.3 EV

- 10.4 Hybrid

Chapter 11 Market Estimates & Forecast, By Application, 2022 - 2035 ($Bn)

- 11.1 Key trends

- 11.2 Powertrain & Chassis

- 11.3 Body Control & Comfort

- 11.4 Infotainment & Telematics

- 11.5 Safety & ADAS

- 11.6 Others

Chapter 12 Market Estimates & Forecast, By Sales Channel, 2022 - 2035 ($Bn)

- 12.1 Key trends

- 12.2 OEM

- 12.3 Aftermarket

Chapter 13 Market Estimates & Forecast, By Region, 2022 - 2035 ($Bn)

- 13.1 Key trends

- 13.2 North America

- 13.2.1 US

- 13.2.2 Canada

- 13.3 Europe

- 13.3.1 Germany

- 13.3.2 UK

- 13.3.3 France

- 13.3.4 Italy

- 13.3.5 Spain

- 13.3.6 Russia

- 13.3.7 Nordics

- 13.3.8 Benelux

- 13.4 Asia Pacific

- 13.4.1 China

- 13.4.2 India

- 13.4.3 Japan

- 13.4.4 South Korea

- 13.4.5 ANZ

- 13.4.6 Singapore

- 13.4.7 Malaysia

- 13.4.8 Indonesia

- 13.4.9 Vietnam

- 13.4.10 Thailand

- 13.5 Latin America

- 13.5.1 Brazil

- 13.5.2 Mexico

- 13.5.3 Argentina

- 13.5.4 Colombia

- 13.6 MEA

- 13.6.1 South Africa

- 13.6.2 Saudi Arabia

- 13.6.3 UAE

Chapter 14 Company Profiles

- 14.1 Global companies

- 14.1.1 Robert Bosch

- 14.1.2 Continental

- 14.1.3 NXP Semiconductors

- 14.1.4 Infineon

- 14.1.5 Denso

- 14.1.6 Qualcomm

- 14.1.7 STMicroelectronics

- 14.1.8 Texas Instruments

- 14.1.9 Renesas Electronics

- 14.1.10 Intel

- 14.1.11 Harman International

- 14.1.12 Broadcom

- 14.1.13 ON Semiconductor

- 14.1.14 ZF Friedrichshafen

- 14.1.15 Valeo

- 14.1.16 Magna

- 14.1.17 Mitsubishi Electric

- 14.1.18 Aptiv

- 14.1.19 Yazaki

- 14.1.20 Autoliv

- 14.2 Regional companies

- 14.2.1 Vector Informatik

- 14.2.2 Melexis

- 14.2.3 TTTech Auto

- 14.2.4 Autotalks

- 14.2.5 Cohda Wireless

- 14.2.6 LG Electronics

- 14.2.7 Lear Corporation

- 14.2.8 Delphi Technologies

- 14.3 Emerging companies

- 14.3.1 iWave Systems

- 14.3.2 Marben Products

- 14.3.3 Danlaw

- 14.3.4 Ficosa Internacional

汽車通訊技術市場:按通訊方式、組件、車輛類型、應用、最終用戶、國家和地區分類-全球產業分析、市場規模、市場佔有率及2026年至2033年預測

汽車通訊技術市場:按通訊方式、組件、車輛類型、應用、最終用戶、國家和地區分類-全球產業分析、市場規模、市場佔有率及2026年至2033年預測 汽車通訊市場:按通訊方式、網路協定、組件、應用和車輛類型分類-2026-2032年全球市場預測

汽車通訊市場:按通訊方式、網路協定、組件、應用和車輛類型分類-2026-2032年全球市場預測 汽車通訊技術市場預測至2034年:全球分析(按通訊方式、車輛類型、通訊網路、推進系統、應用、最終用戶和地區分類)

汽車通訊技術市場預測至2034年:全球分析(按通訊方式、車輛類型、通訊網路、推進系統、應用、最終用戶和地區分類) 全球汽車通訊技術市場

全球汽車通訊技術市場 2026年全球拖車鉤線束模組市場報告

2026年全球拖車鉤線束模組市場報告 汽車通訊技術:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)2026年全球汽車通訊技術市場報告

汽車通訊技術:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)2026年全球汽車通訊技術市場報告 下一代汽車無線通訊技術及汽車通訊模組產業(2026)

下一代汽車無線通訊技術及汽車通訊模組產業(2026) 汽車安全元件(eSE)市場規模、佔有率及預測:依 eSE 架構、安全認證(通用標準)、應用(數位金鑰、支付)和整合劃分 - 全球預測(2026-2036)全球汽車安全元件晶片市場:依車輛類型、安全應用、整合類型、最終用戶、技術、安全功能和地區劃分-市場規模、趨勢分析、行業趨勢、機會分析和預測(2026-2035 年)

汽車安全元件(eSE)市場規模、佔有率及預測:依 eSE 架構、安全認證(通用標準)、應用(數位金鑰、支付)和整合劃分 - 全球預測(2026-2036)全球汽車安全元件晶片市場:依車輛類型、安全應用、整合類型、最終用戶、技術、安全功能和地區劃分-市場規模、趨勢分析、行業趨勢、機會分析和預測(2026-2035 年)