|

市場調查報告書

商品編碼

2063231

廢棄電池:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Battery Scrap - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

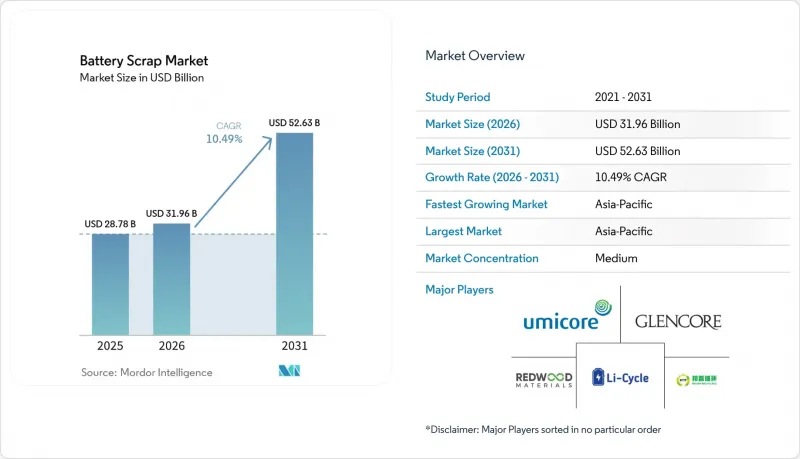

根據 Mordor Intelligence 預測,電池廢料市場規模將從 2025 年的 287.8 億美元和 2026 年的 319.6 億美元成長到 2031 年的 526.3 億美元,2026 年至 2031 年的複合年成長率為 10.49%。

本報告按類型(鉛酸電池、鋰離子電池、鎳基電池和其他化學電池)、應用(汽車、工業電力、家用電子電器等)、最終用戶(專用回收設施、OEM回收、公共產業等)和地區(北美、歐洲、亞太、南美以及中東和非洲)進行細分。市場預測以美元計價。

全球廢電池市場趨勢及洞察

與電動車相關的廢棄鋰離子電池數量正在迅速增加。

隨著2015年至2020年間首批量產電動車電池開始報廢,鋰離子電池廢料量正快速成長。預計到2024年,全球電動車電池需求將接近1太瓦時(TWh),2030年將超過3太瓦時,但2023年全球回收量僅300吉瓦時(GWh),凸顯了結構性供不應求。中國計劃在2024年處理超過50萬噸廢棄鋰離子電池,並計劃透過格林美電子(GEM)新建的荊門生產線,到2026年實現年處理能力30萬噸。廣東博普回收有限公司預計到2024年,鎳、鈷、錳的回收率將達到99.6%,鋰的回收率將達到96.5%,材料成本將比開採產品降低15-20%。預計電池廢料將從2025年的約200吉瓦時(GWh)增加到2030年的超過1太瓦時(TWh),這將使廢料成為正極材料製造商的重要供應來源。區域性原料短缺預計將為那些與汽車製造商、電池製造商和電力公司儘早達成回收協議的回收公司帶來顯著收益。

歐盟、中國和印度的強制生產者責任法

生產者延伸責任制(EPR)架構要求製造商承擔回收再利用的成本,加速建立正規的逆向物流。歐盟電池法規規定,到2027年,鈷、銅和鎳的回收率必須達到63%,回收效率必須達到90%;從2031年起,鈷、鉛、鋰和鎳的最低迴收率分別必須達到16%、85%和6%。中國工業和資訊化部要求電動車製造商建立回收路線並記錄可追溯性數據,並推動汽車製造商與大型回收企業(如GEM和Brunp)建立合作關係。印度修訂後的《電池廢棄物管理條例》(有效期至2025年)將回收目標提高到2026-2027年的90%,並規定到2030-2031年,回收率必須達到20%。這些政策已經淘汰了非正規的回收經營者,引導回收工作流向通過 ISO 14001 認證的設施,並將廢棄電池市場轉變為工業規模的業務。

廢棄電池組逆向物流效率低下

廢棄電池組的收集和運輸仍然分散且成本高昂。聯合國3480和ADR分類要求使用專門的包裝和標籤,導致單位物流成本比非危險材料高出40-60%。設計上的不一致迫使回收商要麼投資客製化拆解工具,要麼接受僅靠破碎線回收率較低的現狀。印度2024年實施的石墨出口限制已成為缺乏國內精煉能力的小規模回收商的瓶頸。同時,在印度尼西亞,約30-40%的鉛酸電池廢料仍在非正規部門處理,不受監管。由於歐盟要到2027年2月才會實施全面的電池護照系統,可追溯性資料仍然分散。在逆向物流標準統一之前,原料收整合本可能會抑制廢舊電池市場的成長。

細分市場分析

到2025年,鉛酸電池將佔流通總量的61.2%,支撐著電池廢料市場的規模,北美和歐洲的回收率超過99%。然而,隨著電動車報廢數量的增加,預計到2031年,鋰離子電池的流通量將以22.3%的複合年成長率激增。濕式提煉的金屬回收率可達90-95%,但每個商業選址需要2億至5億美元的投資。另一方面,乾式提煉的資本密集度較低,但回收率可達80-85%。隨著混合動力汽車轉向鋰離子電池,鎳氫電池在電池廢料市場的佔有率正在萎縮,但航太和國防領域對鎳鎘回收的需求仍然存在。

直接正極再生技術正在革新鋰離子電池加工流程,它無需對材料進行完全拆解,並將成本降低30-40%。 Ascend Elements公司位於喬治亞的氫化正極再生生產線實現了91%的回收率,只需幾週即可將回收材料重新註入電池生產廠,從而縮短了營運資金週轉週期。 ReCell中心的初步試驗表明,NMC 811正極可以從NMC 622廢料中再生,但磷酸鐵鋰(LFP)和鎳鈷鋁(Ni-CoB-Al)電池仍需單獨的加工流程。隨著磷酸鐵鋰電池(LFP)的普及,到2031年,企業能否在廢棄電池市場保持市場佔有率,將取決於它們是否擁有靈活且能夠處理多種化學體系的工廠。

區域分析

亞太地區將主導電池廢棄物市場,預計到2025年將佔據全球49.3%的市場佔有率,並預計在2031年之前以13.3%的複合年成長率成長。光是中國就控制全球80%的回收產能,其中GEM公司新建的5萬噸生產線使總產能達到30萬噸,並根據合約向寧德時代和比亞迪供貨。印度修訂後的《電池廢棄物管理條例》設定了到2026-2027年將回收率提高到90%的目標,但執法力度不一致以及禁止出口黑色殘渣(黑色廢料)的規定,給小規模回收商帶來了挑戰。日本和韓國繼續保持技術領先地位,鬆一高新技術公司位於新萬金的600噸鈷廠奠定了該地區濕法冶煉技術的基礎,而住友商事株式會社則與日產汽車合作回收聆風電池組。

由於嚴格的監管,歐洲市場規模位居第二。 Northvolt 的「Revolt」工廠預計到 2025 年處理能力將達到 5 萬噸,並爭取到 2030 年達到 12.5 萬噸。歐盟電池護照將於 2027 年 2 月起強制實施,該護照包含QR碼追溯功能和回收成分披露,這將為垂直整合型企業帶來競爭優勢。在《通貨膨脹控制法案》(IRA) 的獎勵下,北美正在迎頭趕上。 Redwood 和 Ascend Elements 都計劃在 2025 年擴大其商業生產線,但由於成本超支,儘管 Glencore 已在其阿拉巴馬州工廠投資 2 億美元,但仍不得不暫時關閉其位於羅徹斯特的工廠。

南美洲、中東和非洲地區仍在發展中。巴西的靈活燃料汽車(FFV)車隊為鉛酸電池提供了穩定的來源,但由於電動車(EV)普及率低,對鋰離子電池的投資被推遲。沙烏地阿拉伯和阿拉伯聯合大公國正在考慮將回收納入其多元化策略,但原料仍短缺。在埃及,非正規經營者處理了全國一半以上的鉛酸電池,但預計2024年的一項法規草案將推動建立官方回收機制。由於區域差異,預計在國內設施擴大規模之前,黑電池的跨境貿易將會增加。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 電動車用鋰離子電池的出貨量激增,如今已進入報廢階段。

- 歐盟、中國和印度都制定了生產者責任法。

- 黑錠現貨價格上漲提高了回收商的利潤率。

- 原始設備製造商(例如特斯拉和Redwood)的閉合迴路收購協議

- 人工智慧輔助的廢棄物分類技術提高了回收率。

- 由於固定倉儲設施。

- 市場限制因素

- 低效率的廢舊包裝逆向物流體系

- 鈷鎳價格的波動給經銷商的利潤帶來了壓力。

- 電池化學技術的快速變化會帶來技術鎖定風險。

- 消防安全責任推高了保險費。

- 供應鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 按類型

- 鉛酸蓄電池廢料

- 鋰離子電池廢料

- 鎳基電池廢料

- 其他化學相關產品(鎳鎘電池、鋅空氣電池、固態電池(商業化前))

- 透過使用

- 車

- 工業電力

- 家用電子產品

- 固定式能源儲存系統

- 航太/國防

- 其他細分應用領域(醫療、海事、採礦)

- 最終用戶

- 專用回收設施

- OEM(製造商召回)

- 公共產業及發電廠

- 外部廢棄物管理公司

- 非官方/小規模收藏家

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 北歐國家

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 東南亞國協

- 其他亞太國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

- 埃及

- 其他中東和非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢(併購、聯盟、購電協議)

- 市場佔有率分析(主要公司的市場排名和佔有率)

- 公司簡介

- Umicore

- Li-Cycle

- Redwood Materials

- Glencore

- GEM Co., Ltd.

- Guangdong Brunp Recycling

- TES(Sims Lifecycle Services)

- Retriev Technologies

- Fortum Battery Solutions

- Ganfeng Lithium

- Stena Recycling

- Duesenfeld

- SungEel HiTech

- American Battery Technology Co.

- RecycLiCo Battery Materials

- Accurec Recycling

- Envirostream Australia

- Battery Solutions LLC

- Raw Materials Co.

- Highpower Technology

- Inobat Recycling

- EcoGraf

- Tenova

第7章 市場機會與未來展望

According to Mordor Intelligence, the battery scrap market size is projected to expand from USD 28.78 billion in 2025 and USD 31.96 billion in 2026 to USD 52.63 billion by 2031, registering a CAGR of 10.49% between 2026 and 2031.

This report is Segmented by Type (Lead-Acid, Lithium-Ion, Nickel-Based, Other Chemistries), Application (Automotive, Industrial Motive-Power, Consumer Electronics, and More), End-User (Dedicated Recycling Facilities, OEM Take-Back, Utilities, and More), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Battery Scrap Market Trends and Insights

Soaring EV-Linked Li-ion Volumes Hitting End-of-Life

The first mass-market EV batteries installed between 2015 and 2020 have begun retiring, creating a rapid upswing in lithium-ion scrap. Global EV battery demand stood near 1 TWh in 2024 and is forecast to exceed 3 TWh by 2030, yet worldwide recycling capacity totaled only 300 GWh in 2023, underscoring a structural supply imbalance . China processed more than 500,000 tons of spent Li-ion cells in 2024 and targets 300,000 tons of annual throughput by 2026 through GEM's new Jingmen line. Guangdong Brunp Recycling reported 99.6% recovery of nickel, cobalt, and manganese and 96.5% of lithium in 2024, keeping material costs 15-20% below mined equivalents. Battery retirements are forecast to climb from roughly 200 GWh in 2025 to more than 1 TWh in 2030, transforming scrap into a front-line supply source for cathode producers. Regional feedstock tightness is set to reward recyclers who lock in offtake early with automakers, cell makers, and utilities.

Mandatory Producer-Responsibility Laws in EU, China, India

Extended producer responsibility (EPR) frameworks now obligate manufacturers to fund collection and recycling, accelerating formal reverse-logistics build-outs. The EU Battery Regulation mandates 63% collection by 2027 and 90% recycling efficiency for cobalt, copper, and nickel by 2027, with recycled-content floors of 16% cobalt, 85% lead, and 6% lithium and nickel taking effect from 2031 . China's Ministry of Industry and Information Technology requires EV producers to establish take-back channels and log traceability data, stimulating partnerships between automakers and large recyclers such as GEM and Brunp. India's Battery Waste Management Rules, amended through 2025, lift recovery targets to 90% by 2026-2027 and introduce recycled-content mandates rising to 20% by 2030-2031. These policies marginalize informal collectors and channel volumes toward ISO 14001-certified facilities, pushing the battery scrap market toward industrial-scale operations.

Inefficient Global Reverse-Logistics for End-of-Life Packs

Collection and transport of spent packs remain fragmented and costly. UN 3480 and ADR classifications demand specialized packaging and labeling, inflating per-unit logistics costs by 40-60% over non-hazardous goods. Design heterogeneity forces recyclers to invest in bespoke disassembly tooling or accept lower yields from shredding-only lines. India's 2024 black-mass export restriction created bottlenecks for small collectors who lack domestic refining, while Indonesia's informal sector still handles around 30-40% of lead-acid scrap outside regulatory oversight. A comprehensive battery passport system will not arrive in the EU until February 2027, keeping traceability data siloed. Until reverse-logistics standards converge, feedstock aggregation costs will temper the growth of the battery scrap market.

Other drivers and restraints analyzed in the detailed report include:

- Growing Black-Mass Spot Prices Improving Recycler Margins

- OEM "Closed-Loop" Offtake Contracts

- Volatile Cobalt & Nickel Prices Eroding Re-Seller Profits

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Lead-acid batteries supplied 61.2% of 2025 flows, anchoring the battery scrap market size with recovery rates above 99% in North America and Europe. Lithium-ion volumes, however, are projected to surge at a 22.3% CAGR to 2031 as EV retirements accelerate. Hydrometallurgical refiners deliver 90-95% metal recovery but need USD 200-500 million per commercial hub, whereas pyrometallurgical operators accept 80-85% yields for lower capital intensity. The battery scrap market share for nickel-metal-hydride cells is shrinking as hybrid vehicles transition to Li-ion, yet aerospace and defense preserve a niche demand for nickel-cadmium recycling.

Direct-cathode-regeneration is disrupting lithium-ion processing by eliminating full material breakdown and cutting costs by 30-40%. Ascend Elements' Hydro-to-Cathode line in Georgia achieves 91% recovery and reintroduces material into cell plants within weeks, shrinking working-capital cycles. ReCell Center pilots show NMC 622 scrap can regenerate NMC 811, though LFP and nickel-cobalt-aluminum variants still require separate flows. As LFP adoption rises, flexible multi-chemistry plants will determine which players retain battery scrap market share through 2031.

Geography Analysis

Asia-Pacific dominated the battery scrap market size with 49.3% of 2025 volumes and is forecast to have a 13.3% CAGR through 2031. China alone controls 80% of global recycling capacity; GEM's new 50,000-ton line pushes its total to 300,000 tons and supplies CATL and BYD under contract. India's amended Battery Waste Management Rules raise recovery targets to 90% by 2026-2027, but uneven enforcement and black-mass export bans challenge small collectors. Japan and South Korea remain technology leaders: SungEel HiTech's 600-ton cobalt plant in Saemangeum anchors regional hydrometallurgical expertise, and Sumitomo partners with Nissan on Leaf pack recycling.

Europe ranks second by value thanks to stringent regulation. Northvolt's Revolt plant reached 50,000 tons throughput in 2025 and aims for 125,000 tons by 2030. The EU Battery Passport, mandatory from February 2027, embeds QR-code traceability and recycled-content disclosure, tilting competitive advantage toward vertically integrated players. North America is catching up under the Inflation Reduction Act incentives: Redwood and Ascend Elements both scaled commercial lines in 2025, while Li-Cycle paused its Rochester hub amid cost overruns despite Glencore's USD 200 million investment in an Alabama spoke.

South America and the Middle East & Africa remain nascent. Brazil's flex-fuel car parc creates steady lead-acid flows, yet low EV penetration defers lithium-ion investment. Saudi Arabia and the UAE are evaluating recycling as part of diversification agendas, but feedstock remains scarce. Egypt's informal operators handle over half of national lead-acid volumes, with 2024 draft rules set to push formal take-back schemes. Regional disparity suggests cross-border trade in black mass will rise until domestic hubs reach scale.

- Umicore

- Li-Cycle

- Redwood Materials

- Glencore

- GEM Co., Ltd.

- Guangdong Brunp Recycling

- TES (Sims Lifecycle Services)

- Retriev Technologies

- Fortum Battery Solutions

- Ganfeng Lithium

- Stena Recycling

- Duesenfeld

- SungEel HiTech

- American Battery Technology Co.

- RecycLiCo Battery Materials

- Accurec Recycling

- Envirostream Australia

- Battery Solutions LLC

- Raw Materials Co.

- Highpower Technology

- Inobat Recycling

- EcoGraf

- Tenova

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Soaring EV-linked Li-ion volumes hitting end-of-life

- 4.2.2 Mandatory producer-responsibility laws in EU, China, India

- 4.2.3 Growing black-mass spot prices improving recycler margins

- 4.2.4 OEM "closed-loop" offtake contracts (e.g., Tesla-Redwood)

- 4.2.5 AI-enabled scrap-stream triage boosting recovery yields

- 4.2.6 Stationary-storage repurposing delaying recycle flows

- 4.3 Market Restraints

- 4.3.1 Inefficient global reverse-logistics for end-of-life packs

- 4.3.2 Volatile cobalt & nickel prices eroding re-seller profits

- 4.3.3 Technology-lock risk from rapid cell-chemistry shifts

- 4.3.4 Fire-safety liabilities inflating insurance premiums

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Type

- 5.1.1 Lead-Acid Battery Scrap

- 5.1.2 Lithium-ion Battery Scrap

- 5.1.3 Nickel-based Battery Scrap

- 5.1.4 Other Chemistries (NiCd, Zn-air, Solid-state pre-commercial)

- 5.2 By Application

- 5.2.1 Automotive

- 5.2.2 Industrial Motive-Power

- 5.2.3 Consumer Electronics

- 5.2.4 Stationary Energy-Storage Systems

- 5.2.5 Aerospace and Defense

- 5.2.6 Other Niche Uses (medical, maritime, mining)

- 5.3 By End-User

- 5.3.1 Dedicated Recycling Facilities

- 5.3.2 Original Equipment Manufacturers (OEM Take-Back)

- 5.3.3 Utilities and Power Producers

- 5.3.4 Third-party Waste-Management Firms

- 5.3.5 Informal/Small-scale Collectors

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 NORDIC Countries

- 5.4.2.6 Russia

- 5.4.2.7 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 ASEAN Countries

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 South Africa

- 5.4.5.4 Egypt

- 5.4.5.5 Rest of Middle East and Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Umicore

- 6.4.2 Li-Cycle

- 6.4.3 Redwood Materials

- 6.4.4 Glencore

- 6.4.5 GEM Co., Ltd.

- 6.4.6 Guangdong Brunp Recycling

- 6.4.7 TES (Sims Lifecycle Services)

- 6.4.8 Retriev Technologies

- 6.4.9 Fortum Battery Solutions

- 6.4.10 Ganfeng Lithium

- 6.4.11 Stena Recycling

- 6.4.12 Duesenfeld

- 6.4.13 SungEel HiTech

- 6.4.14 American Battery Technology Co.

- 6.4.15 RecycLiCo Battery Materials

- 6.4.16 Accurec Recycling

- 6.4.17 Envirostream Australia

- 6.4.18 Battery Solutions LLC

- 6.4.19 Raw Materials Co.

- 6.4.20 Highpower Technology

- 6.4.21 Inobat Recycling

- 6.4.22 EcoGraf

- 6.4.23 Tenova

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

金屬廢料回收市場:2026-2032年全球市場預測(依材料、廢棄物來源、回收設施、加工步驟、回收技術及最終用途產業分類)

金屬廢料回收市場:2026-2032年全球市場預測(依材料、廢棄物來源、回收設施、加工步驟、回收技術及最終用途產業分類) 金屬廢料回收市場:依金屬類型、來源、應用和地區分類

金屬廢料回收市場:依金屬類型、來源、應用和地區分類 2026-2034年全球鉛酸蓄電池廢棄物市場規模、佔有率、趨勢與成長分析報告金屬廢料回收市場規模、佔有率、成長及全球產業分析:按類型和應用分類,區域洞察及2026-2034年預測

2026-2034年全球鉛酸蓄電池廢棄物市場規模、佔有率、趨勢與成長分析報告金屬廢料回收市場規模、佔有率、成長及全球產業分析:按類型和應用分類,區域洞察及2026-2034年預測 金屬廢料回收:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

金屬廢料回收:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 2026年全球廢金屬回收市場報告

2026年全球廢金屬回收市場報告 廢金屬回收市場規模、佔有率和成長分析(按金屬類型、廢料來源、最終用途產業和地區分類)—產業預測(2026-2033 年)

廢金屬回收市場規模、佔有率和成長分析(按金屬類型、廢料來源、最終用途產業和地區分類)—產業預測(2026-2033 年) 鉛酸蓄電池廢棄物市場-全球產業規模、佔有率、趨勢、機會和預測,按電池類型(富液式、密封式)、產品類型(鉛酸、硫酸)、來源(汽車、UPS)、地區和競爭格局分類,2020-2030年預測

鉛酸蓄電池廢棄物市場-全球產業規模、佔有率、趨勢、機會和預測,按電池類型(富液式、密封式)、產品類型(鉛酸、硫酸)、來源(汽車、UPS)、地區和競爭格局分類,2020-2030年預測 全球金屬廢料回收市場:預測至2032年-依金屬類型、來源、回收方法、技術、最終用戶及地區進行分析

全球金屬廢料回收市場:預測至2032年-依金屬類型、來源、回收方法、技術、最終用戶及地區進行分析 2025-2029年全球廢金屬回收市場

2025-2029年全球廢金屬回收市場