|

市場調查報告書

商品編碼

2062464

生質壓塊:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031 年)Biomass Briquette - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

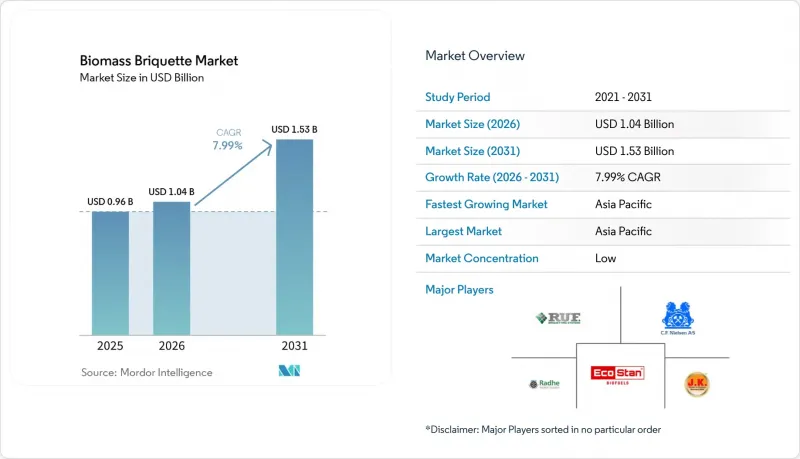

根據 Mordor Intelligence 預測,生質壓塊市場規模將從 2025 年的 9.6 億美元成長到 2026 年的 10.4 億美元,到 2031 年將達到 15.3 億美元,2026 年至 2031 年的複合年成長率為 7.99%。

本報告按類型(農業用煤球、木質煤球等)、原料(鋸末、稻殼、甘蔗渣等)、應用(發電、工業過程加熱、商業和公共供暖等)以及地區(北美、歐洲、亞太、南美、中東和非洲)進行細分。市場預測以美元計價。

全球生質能壓塊市場趨勢與洞察

政府有義務在燃煤發電廠混燒煤炭

印度、印尼和波蘭目前強制燃煤發電廠生質能燃料摻混比例為5%至10%(基於能量含量),以確保煤球供應商的銷售量穩定。光是在印度,到2025年3月,生質燃料摻混量就將達到164,976公噸;印尼國家電力公司(PLN)的目標是到2028年實現每年320萬噸的摻混量。在波蘭,生質燃料摻混比例超過5%的部分,每超過1個百分點,即可獲得每兆瓦時15歐元的補貼。 ISO 17225-8測試正逐漸成為事實上的品質標準。

固體生質燃料鍋爐的維修正在迅速增加。

在英國、丹麥和加拿大,工業和區域供熱業者正逐步淘汰傳統的燃煤和燃油鍋爐,這主要得益於碳定價機制和補貼,光是英國就獲得了總額達1.2億英鎊的補貼。沃旭能源(Orsted)斥資4億英鎊維修的Avedor鍋爐計畫每年減少了120萬噸煤炭的使用量。加拿大的《無污染燃料法規》現在為改用認證煤球的工業供熱用戶提供碳權額度。

東南亞低價液化天然氣供應過剩

現貨液化天然氣價格跌破每百萬英熱單位10美元,迫使泰國和菲律賓的工業企業繼續使用天然氣直至2026年初,從而推遲了向煤球鍋爐的過渡。亞洲開發銀行的一項調查顯示,越南62%的工廠在天然氣價格跌破每百萬英熱單位9美元時凍結了維修計畫。

細分市場分析

熱解預計將以10.3%的複合年成長率成長,顯著高於生質能煤球市場的平均值。這反映了電力公司對疏水性高能量產品的需求,這些產品可以直接在現有煤炭輸送機中重複使用。預計2031年,熱解生質能煤球市場規模將達4.5億美元,主要受高熱值產品出口至歐洲和東北亞的推動。農業煤球維持每噸100-130美元的成本優勢,預計到2025年將佔生質煤球市場42.3%的佔有率。

由於木質煤球的灰分含量僅0.5%至2.0%,且燃燒特性可預測,因此在高級住宅供暖市場需求仍強勁。含有10%至20%木炭粉的混合煤球因其易燃且煙霧少,在非洲家庭中廣受歡迎。而藻類煤球等新興煤球類型,由於面臨廢棄物收集和監管方面的挑戰,目前仍處於試驗階段。

區域分析

預計到2025年,亞太地區將佔全球銷售額的48.9%,並以每年8.8%的速度成長,主要得益於印度5%至7%的混燒限制以及中國逐步淘汰小規模燃煤發電廠。印尼的目標是到2028年實現每年320萬噸稻殼混合燃料的目標,而日本即使海運成本高達每噸35至50美元,也進口熱處理煤球以獲得上網電價補貼。

歐洲則位居第二,主要得益於英國1.2億英鎊的鍋爐維修補助和丹麥的Avedore改造計畫。碳邊境調節措施(CBAM)嵌入式碳排放報告機制鼓勵使用高能量密度的熱處理產品,而北歐國家則利用林業殘餘物進行區域供熱,實現了超過80%的溫室氣體減排。

北美地區正在擴張,這主要得益於美國東南部向日本和韓國出口鋸末煤球,以及加拿大「無污染燃料法規」對從天然氣轉向清潔燃料的工業供熱用戶給予獎勵。南美洲的成長則得益於巴西甘蔗渣的過剩以及哥倫比亞對咖啡渣的利用。在中東和非洲,使用米糠和花生殼煤球的清潔烹飪計畫仍然佔據主導地位。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 政府有義務在燃煤發電廠混燒煤炭

- 用於固體生質燃料的鍋爐改造正在迅速增加。

- 撒哈拉以南非洲的農村電氣化項目

- 歐盟碳邊境調節機制(CBAM)的外溢效應

- 商業規模烘焙技術的突破性進展

- 航運業向低硫固態燃料過渡

- 市場限制因素

- 東南亞廉價液化天然氣供應過剩

- 低密度煤球洲內物流成本高昂

- 對小型家用爐灶顆粒物排放更嚴格的標準。

- 來自顆粒出口產業的競爭性需求

- 供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

第5章 市場規模與成長預測

- 按類型

- 農業用煤球

- 木質煤球

- 熱處理煤球

- 木炭混合煤球

- 其他

- 按成分

- 鋸末

- 稻殼

- 渣

- 花生殼

- 椰子殼和椰皮

- 玉米秸稈、葉子和稻草

- 林業剩餘物

- 混合農業廢棄物

- 透過使用

- 發電

- 工業製程加熱

- 商業和公共設施的供暖

- 住宅暖氣和熱水供應

- 烹飪燃料

- 其他

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 英國

- 德國

- 法國

- 西班牙

- 北歐國家

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 東南亞國協

- 其他亞太國家

- 南美洲

- 巴西

- 阿根廷

- 哥倫比亞

- 其他南美國家

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

- 埃及

- 其他中東和非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢(併購、聯盟、購電協議)

- 市場佔有率分析(主要公司的市場排名和佔有率)

- 公司簡介

- Radhe Industrial Corporation

- CF Nielsen A/S

- RUF Briquetting Systems

- Biomass Briquettes UK Ltd

- ECOSTAN

- Jay Khodiyar Machine Tools

- Weima Maschinenbau

- Advance Hydrau-Tech

- Maxton Industrial Co.

- Lehra Fuel Tech

- Shreenithi Engineering Works

- Ronak Engineering

- Biomass Secure Power Inc.

- Verdo Energy

- Energis Oy

- SC Rika Ecofuel SRL

- Vyncke NV

- Zhengzhou Fusmar Machinery

- Jiangsu Yongli Machinery

- FEECO International

第7章 市場機會與未來展望

According to Mordor Intelligence, the biomass briquette market size is projected to expand from USD 0.96 billion in 2025 and USD 1.04 billion in 2026 to USD 1.53 billion by 2031, registering a CAGR of 7.99% between 2026 and 2031.

This report is Segmented by Type (Agro Briquettes, Wood Briquettes, and More), Raw Material (Sawdust, Rice Husk, Bagasse, and More), Application (Power Generation, Industrial Process Heating, Commercial and Institutional Heating, and More), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Biomass Briquette Market Trends and Insights

Government Co-firing Mandates in Coal Plants

India, Indonesia, and Poland now stipulate biomass blends of 5%-10% by energy content at coal stations, creating predictable offtake volumes for briquette suppliers. India alone co-fired 164,976 metric tons by March 2025, while Indonesia's PLN targets 3.2 million metric tons annually by 2028. Poland tops up each percentage point above 5% with a EUR 15 per MWh subsidy. ISO 17225-8 testing is emerging as the de facto quality gate.

Surge in Boiler Retrofits for Solid Biofuels

Industrial and district-heating operators in the United Kingdom, Denmark, and Canada are converting legacy coal and oil boilers, spurred by carbon-pricing schemes and subsidy pools totaling GBP 120 million in the UK alone. Orsted's GBP 400 million Avedore retrofit eliminated 1.2 million metric tons of coal a year. Canada's Clean Fuel Regulations now extend credits to industrial heat users that shift to certified briquettes.

Low-priced LNG Glut in Southeast Asia

Spot LNG below USD 10 per MMBtu kept Thai and Philippine industries on gas through early 2026, delaying briquette boiler conversions. An Asian Development Bank survey showed 62% of Vietnamese plants mothballed retrofits when gas slipped under USD 9 per MMBtu.

Other drivers and restraints analyzed in the detailed report include:

- Rural Electrification Programs in Sub-Saharan Africa

- EU Carbon Border Adjustment Mechanism Spill-over

- High Intra-continental Logistics Cost for Low-density Briquettes

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Torrefied Briquettes are on course to expand at a 10.3% CAGR, far above the biomass briquette market average, reflecting utilities' need for hydrophobic, high-energy products that slipstream into existing coal conveyors. The biomass briquette market size for torrefied variants is projected to reach USD 450 million by 2031, commanded by high-heating-value shipments to Europe and Northeast Asia. Agro Briquettes remain cost-advantaged at USD 100-130 per metric ton and held 42.3% of the biomass briquette market share in 2025.

Wood Briquettes continue to serve premium residential heat markets thanks to 0.5%-2.0% ash and predictable combustion profiles. Charcoal-Blend Briquettes, with 10%-20% charcoal fines, are popular among African households for fast ignition and reduced smoke. Emerging categories such as algae-based briquettes remain pilot-scale until waste-collection and regulatory hurdles are cleared.

Geography Analysis

Asia-Pacific accounted for 48.9% of 2025 revenue and will expand at 8.8% annually, anchored by India's 5%-7% co-firing rule and China's small-coal-unit retirements. Indonesia targets 3.2 million t/y rice-husk blends by 2028, and Japan imports torrefied briquettes to earn feed-in-tariff credits despite USD 35-50 per metric ton ocean freight.

Europe ranks second, propelled by GBP 120 million in UK boiler-retrofit grants and Denmark's Avedore conversion. CBAM's embedded-carbon reporting favors high-energy torrefied products, while Nordic countries channel forestry residues into district heating for >80% GHG savings.

North America advances on the back of southeastern U.S. sawdust briquette exports to Japan and South Korea and Canada's Clean Fuel Regulations, which credit industrial heat users who switch from natural gas. South America's growth is led by Brazil's bagasse surplus and Colombia's coffee-husk initiatives. The Middle East and Africa remain dominated by clean-cooking programs using rice-husk and groundnut-shell briquettes.

- Radhe Industrial Corporation

- C.F. Nielsen A/S

- RUF Briquetting Systems

- Biomass Briquettes UK Ltd

- ECOSTAN

- Jay Khodiyar Machine Tools

- Weima Maschinenbau

- Advance Hydrau-Tech

- Maxton Industrial Co.

- Lehra Fuel Tech

- Shreenithi Engineering Works

- Ronak Engineering

- Biomass Secure Power Inc.

- Verdo Energy

- Energis Oy

- SC Rika Ecofuel SRL

- Vyncke NV

- Zhengzhou Fusmar Machinery

- Jiangsu Yongli Machinery

- FEECO International

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Government co-firing mandates in coal plants

- 4.2.2 Surge in boiler retrofits for solid biofuels

- 4.2.3 Rural electrification programs in Sub-Saharan Africa

- 4.2.4 EU Carbon Border Adjustment Mechanism (CBAM) spill-over

- 4.2.5 Commercial-scale torrefaction breakthroughs

- 4.2.6 Maritime sector's switch to low-sulfur solid fuels

- 4.3 Market Restraints

- 4.3.1 Low-priced LNG glut in Southeast Asia

- 4.3.2 High intra-continental logistics cost for low-density briquettes

- 4.3.3 Stricter particulate-matter norms on small household stoves

- 4.3.4 Competing demand from pellet export industry

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Type

- 5.1.1 Agro Briquettes

- 5.1.2 Wood Briquettes

- 5.1.3 Torrefied Briquettes

- 5.1.4 Charcoal-Blend Briquettes

- 5.1.5 Others

- 5.2 By Raw Material

- 5.2.1 Sawdust

- 5.2.2 Rice Husk

- 5.2.3 Bagasse

- 5.2.4 Groundnut (Peanut) Shells

- 5.2.5 Coconut Husk and Shell

- 5.2.6 Corn Stover and Straw

- 5.2.7 Forestry Residues

- 5.2.8 Mixed Agricultural Waste

- 5.3 By Application

- 5.3.1 Power Generation

- 5.3.2 Industrial Process Heating

- 5.3.3 Commercial and Institutional Heating

- 5.3.4 Residential Space and Water Heating

- 5.3.5 Cooking Fuel

- 5.3.6 Others

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 United Kingdom

- 5.4.2.2 Germany

- 5.4.2.3 France

- 5.4.2.4 Spain

- 5.4.2.5 Nordic Countries

- 5.4.2.6 Russia

- 5.4.2.7 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 ASEAN Countries

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Colombia

- 5.4.4.4 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 United Arab Emirates

- 5.4.5.2 Saudi Arabia

- 5.4.5.3 South Africa

- 5.4.5.4 Egypt

- 5.4.5.5 Rest of Middle East and Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Radhe Industrial Corporation

- 6.4.2 C.F. Nielsen A/S

- 6.4.3 RUF Briquetting Systems

- 6.4.4 Biomass Briquettes UK Ltd

- 6.4.5 ECOSTAN

- 6.4.6 Jay Khodiyar Machine Tools

- 6.4.7 Weima Maschinenbau

- 6.4.8 Advance Hydrau-Tech

- 6.4.9 Maxton Industrial Co.

- 6.4.10 Lehra Fuel Tech

- 6.4.11 Shreenithi Engineering Works

- 6.4.12 Ronak Engineering

- 6.4.13 Biomass Secure Power Inc.

- 6.4.14 Verdo Energy

- 6.4.15 Energis Oy

- 6.4.16 SC Rika Ecofuel SRL

- 6.4.17 Vyncke NV

- 6.4.18 Zhengzhou Fusmar Machinery

- 6.4.19 Jiangsu Yongli Machinery

- 6.4.20 FEECO International

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

生質能顆粒燃料市場預測至2034年:按原料、應用和地區分類的全球分析

生質能顆粒燃料市場預測至2034年:按原料、應用和地區分類的全球分析 2026年全球生質能市場報告

2026年全球生質能市場報告 生質壓塊市場:依原料類型、產品類型、應用、終端用戶產業及地區分類

生質壓塊市場:依原料類型、產品類型、應用、終端用戶產業及地區分類 矽膠壓塊市場規模、佔有率和成長分析:按產品類型、等級、形狀、材料、最終用途行業、分銷管道和地區分類 - 2026-2033 年行業預測

矽膠壓塊市場規模、佔有率和成長分析:按產品類型、等級、形狀、材料、最終用途行業、分銷管道和地區分類 - 2026-2033 年行業預測 日本生質能市場規模、佔有率、趨勢和預測:按原料、應用和地區分類,2026-2034年

日本生質能市場規模、佔有率、趨勢和預測:按原料、應用和地區分類,2026-2034年 生質壓塊市場-全球產業規模、佔有率、趨勢、機會及按類型、應用、地區和競爭格局分類的預測(2021-2031年)生質能顆粒燃料市場-全球產業規模、佔有率、趨勢、機會及預測(依來源、類型、應用、地區及競爭格局分類,2021-2031年)

生質壓塊市場-全球產業規模、佔有率、趨勢、機會及按類型、應用、地區和競爭格局分類的預測(2021-2031年)生質能顆粒燃料市場-全球產業規模、佔有率、趨勢、機會及預測(依來源、類型、應用、地區及競爭格局分類,2021-2031年) 全球生物質顆粒市場:市場規模、佔有率、成長率、產業分析、依類型、應用和地區劃分的分析以及未來預測(2026-2034)

全球生物質顆粒市場:市場規模、佔有率、成長率、產業分析、依類型、應用和地區劃分的分析以及未來預測(2026-2034) 生質能市場規模、佔有率和成長分析(按產品類型、原料來源、技術、最終用戶、原料和地區分類)-2026-2033年產業預測

生質能市場規模、佔有率和成長分析(按產品類型、原料來源、技術、最終用戶、原料和地區分類)-2026-2033年產業預測 生質能顆粒燃料市場規模、佔有率和成長分析(按來源、類型、最終用戶和地區分類)—2026-2033年產業預測

生質能顆粒燃料市場規模、佔有率和成長分析(按來源、類型、最終用戶和地區分類)—2026-2033年產業預測