|

市場調查報告書

商品編碼

2062435

講師主導語言培訓:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)Instructor-led Language Training - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

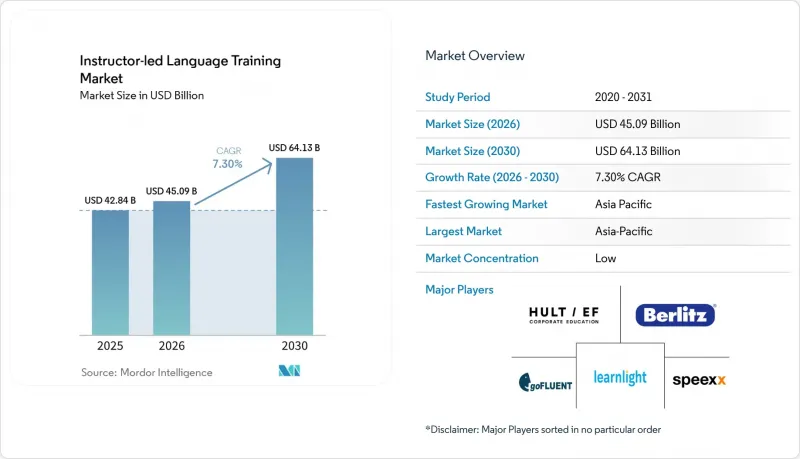

根據 Mordor Intelligence 預測,到 2025 年,由教師主導的語言培訓市場規模將達到 428.4 億美元;到 2026 年將達到 450.9 億美元;到 2030 年將達到 641.3 億美元。

預計從 2026 年到 2030 年,其複合年成長率將達到 7.30%。

本報告按交付方式(現場課堂培訓、虛擬直播課堂、混合式學習等)、最終用戶(企業、教育機構、政府和國防機構等)、語言(英語、中文、西班牙語、法語等)和地區(北美、南美、歐洲等)進行細分。市場預測以美元計價。

全球教師主導語言培訓市場的趨勢與洞察

企業全球化需要多語言團隊

跨國公司持續推動語言能力標準的標準化,以減少跨境營運中的摩擦,並將學習成果與歐洲語言共同參考框架(CEFR)等級掛鉤,用於招募和調動決策。企業負責人更傾向於選擇能夠將培訓整合到其人力資源系統中的供應商。這意味著供應商的選擇不僅取決於培訓方法,還取決於系統整合的深度,因為課程註冊與工作要求、完成情況追蹤和審計合規性息息相關。將課程設計與認證評量標準保持一致,能夠使訓練到認證的過渡更加順暢,尤其是在各大考試機構不斷完善與CEFR的對應關係之後。企業也積極應對合規性主導的需求。對於受監管的溝通和安全協議,檢驗的語言能力至關重要,因此即使非監管技能已轉向線上,付費的講師主導課程仍然保留。這些趨勢正在推動講師主導語言培訓市場的高階細分領域發展,企業級報告和CEFR級別的課責是該領域的基本要求。

移民的湧入增加了對當地語言的需求。

隨著有史以來規模最大的移民湧入經合組織國家,各國政府正將預算分配給以教師主導的英語和當地語言教育,旨在促進社會融合和提高就業能力。在美國,難民安置計畫已獲得教育資金,用於支援由認證教師指導的成人英語課程和就業輔助語言服務。各州計畫為難民抵達後一年內提供的固定期限的教師主導語言支援計畫提供資金,並透過社區學院和非營利組織維持委託服務的提供。難民教育最佳實踐指南也建議對識字程度較低的學習者進行雙語教學和麵對面輔導,提倡以人主導的教學方法,而非自學模組。在此政策背景下,政府已製定了針對以社會融合為重點的課程的多年期契約,並在教師主導的語言培訓市場中建立了穩定的容量規劃。

與應用程式相比,每個學習者的成本更高。

與應用程式訂閱相比,教師主導課程的每位學員成本更高,這給價格敏感的市場中自費學習者帶來了壓力。即使企業資助高階課程,當宏觀經濟情勢惡化時,潛在學員往往會推遲入學或轉向成本較低的課程。為了應對這種情況,培訓機構開始轉向線上授課,這可以降低差旅和場地成本,一些機構還表示,透過將學生群體轉移到線上,實現了規模經濟效益,從而降低了成本。一些面向低收入地區的培訓計畫也在嘗試將定價與教材成本掛鉤,並利用人工智慧技術來減少教師的時間。儘管做出了這些努力,但與自學應用程式之間的價值差距仍然阻礙了教師主導語言培訓市場在短期內發生轉變。

細分市場分析

2025年,面授和混合式教學模式合計佔總收入的47.36%,但預計到2031年,虛擬直播課堂的複合年成長率將達到15.48%。這反映出以教師主導的語言培訓市場正逐步轉向擴充性的主導課程模式。混合式課程將定期研討會與結構化的自主學習相結合,以保持可預測的學習進度,並確保教師履行其在專業學習方面的職責。虛擬直播課堂是那些需要跨地區提供一致課程,並能根據招聘和合規需求快速添加課程的機構的首選。在這些課堂環境中,母語教師利用人工智慧驅動的角色扮演和語音辨識來模擬真實的溝通場景,從而增強學員的自信心和語言能力。這種即時互動與人工智慧支援的結合如今已成為一項關鍵的差異化優勢,並推動著以教師主導的語言培訓產業繼續專注於提升會話品質和可衡量的學習成果。

與人力資源系統的深度整合至關重要,因為買家希望將培訓與績效管理、人事變動和合規性儀錶板連結起來。為 SAP SuccessFactors 等平台提供現成連接器的供應商能夠加速分散式團隊的部署,並減輕管理負擔。私人課程(一對一教學)仍然是一個強勁的細分市場,因為高階主管和重考者重視一對一課程的專注性,而且市場平台正在擴展基於時區和興趣的匹配功能。沉浸式課程繼續為尋求強化提升的學習者提供服務,但他們面臨物流和簽證方面的挑戰,這可能會促使企業轉向虛擬替代方案。這種細分趨勢意味著虛擬直播課堂仍然是成長的核心,而面授形式在講師主導的語言培訓市場中仍然發揮著策略性作用。

區域分析

預計到2025年,亞太地區將以41.78%的市佔率引領主導語言培訓市場,並在2031年之前以13.75%的複合年成長率持續成長。這一成長主要得益於企業英語需求、大規模的技術服務業勞動力以及對考試輔導的強勁需求。國際學生流動性的增強持續推動著對需要結構化、主導支援的認證和學術課程的需求。政府對符合歐洲語言共同參考框架(CEFR)且經濟實惠的資格認證的認可,使得公共部門和教師培訓計畫能夠更經濟地容納大規模學生。在日本,由人工智慧驅動的虛擬課程正與企業合作,為需要符合CEFR目標的結構化教學的企業學員提供服務。這些因素正在推動亞太地區向混合式主導課程模式的廣泛轉變,以滿足合規性和職業發展的需求。

在歐洲,多語言教育體系和標準化能力檢驗的需求持續推動著這一穩步發展勢頭。企業負責人越來越依賴能夠跨地區註冊員工並根據歐洲語言共同參考框架(CEFR)基準值追蹤學習進度的整合平台,包括在德語市場的大規模部署。航空英語仍然是受監管培訓的重要組成部分,因為歐洲當局製定了能力有效期並創建了可預測的再認證週期。歐洲的資料本地化規範和隱私期望也影響供應商的選擇,因為客戶需要安全的託管服務和合規的控制措施來提供線上課程。這種環境使得講師主導的學習(包括面授和線上學習)在全部區域的組織學習中繼續紮根發展。

在北美,市場需求保持穩定,這得益於企業培訓預算和政府資助的成人英語課程綜合計畫。連結全球大規模教師網路和學習者的平台持續吸引投資,為消費者拓展一對一學習選擇,同時也為企業提供補充式團體學習。在中東和非洲,夥伴關係以教科書價格提供人工智慧輔助教學,旨在擴大傳統中心式教學模式在基礎設施和預算限制下難以實施的地區的覆蓋範圍。這些趨勢表明,不同地區的企業、公眾和消費者需求以多種組合形式存在,並持續影響教師主導的語言培訓市場。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 企業全球化需要多語言團隊

- 移民增加導致對當地語言的需求上升

- 與考試輔導的整合正在促進付費面授訓練服務的發展。

- 混合職場環境有利於虛擬直播課程的發展。

- 航空和醫療領域的技能需求正在推動ILT的發展。

- 與 LMS 整合可實現擴充性的ILT。

- 市場限制因素

- 與使用應用程式相比,每個學習者的成本更高。

- 合格的母語教師短缺

- 關於錄製直播課程的隱私合規限制

- 旅行簽證政策的改變阻礙了新兵訓練營的發展。

- 價值供應鏈分析

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 透過串流媒體模式

- 面授培訓

- 虛擬直播課堂(線上)

- 混合式學習

- 沉浸式訓練營

- 私人輔導

- 最終用戶

- 公司

- 學術機構

- 政府/國防

- 個人/移民

- 考試準備提供者

- 按語言

- 英語

- 中文(國語)

- 西班牙語

- 法語

- 德文

- 日本人

- 其他

- 按地區

- 北美洲

- 加拿大

- 美國

- 墨西哥

- 南美洲

- 巴西

- 秘魯

- 智利

- 阿根廷

- 其他南美國家

- 歐洲

- 英國

- 德國

- 法國

- 西班牙

- 義大利

- 比荷盧經濟聯盟

- 北歐的

- 其他歐洲國家

- 亞太地區

- 印度

- 中國

- 日本

- 澳洲

- 韓國

- 東南亞

- 其他亞太國家

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

- 奈及利亞

- 其他中東和非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Hult EF Corporate Education(EF)

- Berlitz Corporation

- goFLUENT

- Learnlight

- Speexx

- Wall Street English

- British Council

- International House World Organisation

- inlingua

- Kaplan International Languages

- ELS Language Centers

- ILSC Education Group

- Open English

- Preply

- italki

- Lingoda

- Cambly

- Voxy

- Babbel Live(Babbel for Business)

- Busuu for Business

- Eton Institute

- Goethe-Institut

- Learnlight

- Lingoda

第7章 市場機會與未來展望

According to Mordor Intelligence, the instructor-led language training market size is projected to be USD 42.84 billion in 2025, USD 45.09 billion in 2026, and reach USD 64.13 billion by 2030, growing at a CAGR of 7.30% from 2026 to 2030.

This report is Segmented by Delivery Mode (On-Site Classroom Training, Virtual Live Classroom, Blended Learning, and More), End User (Corporates, Academic Institutions, Government & Defense, and More), Language (English, Mandarin Chinese, Spanish, French, and More), and Geography (North America, South America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Instructor-led Language Training Market Trends and Insights

Corporate Globalization Requiring Multilingual Teams

Multinational organizations continue to standardize language benchmarks to reduce friction in cross-border operations, and they anchor learning outcomes to CEFR levels for hiring and mobility decisions . Corporate buyers favor providers that integrate training into HR systems, so enrolments align to job-role thresholds, completion tracking, and audit readiness, which ties vendor selection to integration depth as much as to pedagogy. Aligning course design with recognized assessments makes the transition from training to certification smoother, especially as major tests refine CEFR mapping. Enterprises also respond to compliance-driven needs, where regulated communication and safety protocols prioritize verified proficiency, which sustains paid instructor-led programs even as unregulated skills move online. These preferences reinforce a premium segment of the instructor-led language training market where enterprise-grade reporting and CEFR-level accountability are non-negotiable.

Migration Inflows Raising Local Language Demand

Record migration inflows into OECD economies channel government budgets into instructor-led English and local language instruction for integration and employability . In the United States, refugee resettlement programs earmark education funding that supports adult English classes and employment-linked language services delivered by certified instructors. State-level programs fund time-bound, instructor-led language support during the first year of arrival, which sustains contracted delivery across community colleges and nonprofit providers. Best-practice guidelines for refugee education also point to bilingual instruction and live facilitation for low-literacy learners, which supports a human-led approach over self-paced modules. This policy backdrop anchors multi-year procurement for integration-focused classes and stabilizes capacity planning in the instructor-led language training market.

Higher Per-Learner Costs Than Apps

Instructor-led courses command higher per-learner costs than app subscriptions, which puts pressure on adoption among self-funded learners in price-sensitive markets. Even as enterprises fund premium formats, individual candidates often defer enrolment or switch to lower-cost options when macro conditions tighten. Providers counter with virtual delivery that reduces travel and facility expenses, and some report material cost advantages at scale when moving cohorts online. Targeted programs in lower-income regions also experiment with pricing tied to textbook-equivalent costs, enabled by AI-supported delivery that scales instructor time. Despite these steps, the value gap with self-paced apps remains a near-term brake on conversion in the instructor-led language training market.

Other drivers and restraints analyzed in the detailed report include:

- Exam-Prep Tie-Ins Boosting Paid ILT

- Hybrid Workplaces Favor Virtual Live Classes

- Shortage of Certified Native Instructors

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

On-site classroom and blended formats together accounted for 47.36% of revenue in 2025, while virtual live classrooms are forecast to grow at a 15.48% CAGR through 2031, reflecting a measured shift toward scalable, instructor-led online cohorts within the instructor-led language training market. In blended programs, learners combine scheduled workshops with structured self-study to maintain a predictable cadence and ensure instructor accountability for working adults. Virtual live classrooms earn preference when organizations require consistent delivery across regions and the ability to add cohorts quickly based on hiring or compliance needs. In these environments, native-speaking instructors use AI-enabled role-play and voice recognition to simulate realistic communication tasks that build confidence and speed to competence. This mix of live facilitation and AI support is now a key differentiator, keeping the instructor-led language training industry focused on quality of interaction and measurable outcomes.

The depth of HR system integrations also matters because buyers want training to plug into performance management, talent mobility, and compliance dashboards. Providers that support off-the-shelf connectors for platforms like SAP SuccessFactors accelerate implementations for distributed teams and reduce administrative overhead. Private tutoring remains a resilient niche because executives and exam retakers value the focus of one-to-one sessions, and marketplaces scale matches across time zones and interests. Immersion programs continue to serve learners who want concentrated progress, but they face logistics and visa-related headwinds that can push organizations toward virtual alternatives. This segmentation pattern keeps virtual live classrooms central to growth while in-person formats retain strategic roles in the instructor-led language training market.

Geography Analysis

Asia-Pacific led the instructor-led language training market with a 41.78% share in 2025 and is projected to grow at a 13.75% CAGR through 2031, driven by corporate English requirements, large technology services workforces, and strong exam-prep demand. International student mobility continues to contribute to demand for certification and pathway programs that require structured, instructor-led support. Ministries that approve cost-effective CEFR-aligned credentials make large cohorts more affordable for the public sector and teacher training programs. In Japan, enterprise partnerships are scaling AI-powered virtual lessons to serve corporate learners who need structured coaching aligned with CEFR goals. These factors underpin a broad shift toward hybrid instructor-led delivery that meets both compliance and career advancement needs across APAC.

Europe maintains steady momentum supported by multilingual education systems and enterprise demand for standardized proficiency verification. Corporate buyers are increasing their reliance on integrated platforms that enroll and track employees against CEFR thresholds across regions, including large-scale deployments in German-speaking markets. Aviation English remains a staple of regulated training as European authorities enforce proficiency validity periods that create predictable recertification cycles. European data-localization norms and privacy expectations also shape vendor selection because clients require secure hosting and compliance-ready controls for live-class delivery. This environment keeps in-person and virtual instructor-led formats embedded in organizational learning across the region.

North America shows stable demand patterns anchored by corporate learning budgets and government-funded integration programs that support adult English classes. Marketplaces that connect large tutor networks with learners worldwide continue to attract investment, expanding one-to-one options for consumers and complementing enterprise-focused cohorts. In the Middle East and Africa, partnerships that deliver AI-supported instruction at textbook-equivalent prices aim to widen access where infrastructure or budgets limit traditional center-based models. These patterns show region-specific mixes of corporate, public, and consumer demand that continue to shape the instructor-led language training market.

- Hult EF Corporate Education (EF)

- Berlitz Corporation

- goFLUENT

- Learnlight

- Speexx

- Wall Street English

- British Council

- International House World Organisation

- inlingua

- Kaplan International Languages

- ELS Language Centers

- ILSC Education Group

- Open English

- Preply

- italki

- Lingoda

- Cambly

- Voxy

- Babbel Live (Babbel for Business)

- Busuu for Business

- Eton Institute

- Goethe-Institut

- Learnlight

- Lingoda

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Corporate globalization requiring multilingual teams

- 4.2.2 Migration inflows raising local language demand

- 4.2.3 Exam-prep tie-ins boosting paid ILT

- 4.2.4 Hybrid workplaces favor virtual live classes

- 4.2.5 Aviation, healthcare proficiency mandates drive ILT

- 4.2.6 LMS integrations enable scalable ILT

- 4.3 Market Restraints

- 4.3.1 Higher per-learner costs than apps

- 4.3.2 Shortage of certified native instructors

- 4.3.3 Live-class recording privacy compliance constraints

- 4.3.4 Travel visa volatility curbs boot-camps

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Delivery Mode

- 5.1.1 On-site Classroom Training

- 5.1.2 Virtual Live Classroom (Online)

- 5.1.3 Blended Learning

- 5.1.4 Immersion Boot-camps

- 5.1.5 Private Tutoring

- 5.2 By End User

- 5.2.1 Corporates

- 5.2.2 Academic Institutions

- 5.2.3 Government & Defense

- 5.2.4 Individuals / Migrants

- 5.2.5 Exam-Prep Providers

- 5.3 By Language

- 5.3.1 English

- 5.3.2 Mandarin Chinese

- 5.3.3 Spanish

- 5.3.4 French

- 5.3.5 German

- 5.3.6 Japanese

- 5.3.7 Others

- 5.4 By Region

- 5.4.1 North America

- 5.4.1.1 Canada

- 5.4.1.2 United States

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Peru

- 5.4.2.3 Chile

- 5.4.2.4 Argentina

- 5.4.2.5 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 United Kingdom

- 5.4.3.2 Germany

- 5.4.3.3 France

- 5.4.3.4 Spain

- 5.4.3.5 Italy

- 5.4.3.6 BENELUX

- 5.4.3.7 NORDICS

- 5.4.3.8 Rest of Europe

- 5.4.4 APAC

- 5.4.4.1 India

- 5.4.4.2 China

- 5.4.4.3 Japan

- 5.4.4.4 Australia

- 5.4.4.5 South Korea

- 5.4.4.6 South East Asia

- 5.4.4.7 Rest of APAC

- 5.4.5 Middle East & Africa

- 5.4.5.1 United Arab Emirates

- 5.4.5.2 Saudi Arabia

- 5.4.5.3 South Africa

- 5.4.5.4 Nigeria

- 5.4.5.5 Rest of Middle East & Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.4.1 Hult EF Corporate Education (EF)

- 6.4.2 Berlitz Corporation

- 6.4.3 goFLUENT

- 6.4.4 Learnlight

- 6.4.5 Speexx

- 6.4.6 Wall Street English

- 6.4.7 British Council

- 6.4.8 International House World Organisation

- 6.4.9 inlingua

- 6.4.10 Kaplan International Languages

- 6.4.11 ELS Language Centers

- 6.4.12 ILSC Education Group

- 6.4.13 Open English

- 6.4.14 Preply

- 6.4.15 italki

- 6.4.16 Lingoda

- 6.4.17 Cambly

- 6.4.18 Voxy

- 6.4.19 Babbel Live (Babbel for Business)

- 6.4.20 Busuu for Business

- 6.4.21 Eton Institute

- 6.4.22 Goethe-Institut

- 6.4.23 Learnlight

- 6.4.24 Lingoda

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment

全球外語學習市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球外語學習市場規模、佔有率、趨勢和成長分析報告(2026-2034) 語言學習和溝通技巧平台市場預測至2034年:按組成部分、學習形式、語言類型、最終用戶、應用和地區分類的全球分析

語言學習和溝通技巧平台市場預測至2034年:按組成部分、學習形式、語言類型、最終用戶、應用和地區分類的全球分析 雲端英語學習:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)

雲端英語學習:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031) 阿拉伯語學習市場:依學習風格、年齡層、學習目標、定價模式和學習者類型分類-2026-2032年全球市場預測

阿拉伯語學習市場:依學習風格、年齡層、學習目標、定價模式和學習者類型分類-2026-2032年全球市場預測 語言學習應用市場規模、佔有率和成長分析:按語言類型、部署模式、技術類型、收入模式、內容類型、使用者類型和地區分類 - 2026-2033 年產業預測

語言學習應用市場規模、佔有率和成長分析:按語言類型、部署模式、技術類型、收入模式、內容類型、使用者類型和地區分類 - 2026-2033 年產業預測 K-12雙語沉浸式教育市場機會、成長要素、產業趨勢分析及預測(2026-2035年)

K-12雙語沉浸式教育市場機會、成長要素、產業趨勢分析及預測(2026-2035年) 手語應用市場 - 全球產業規模、佔有率、趨勢、機會及預測(按產品類型、應用、訂閱模式、部署模式、地區和競爭格局分類,2021-2031年)兒童數學學習應用市場:依學習形式、平台、定價模式、年齡層、學科重點、連結方式與使用者類型分類-2026-2032年全球預測語言學習市場機會、成長要素、產業趨勢分析及預測(2026-2035年)

手語應用市場 - 全球產業規模、佔有率、趨勢、機會及預測(按產品類型、應用、訂閱模式、部署模式、地區和競爭格局分類,2021-2031年)兒童數學學習應用市場:依學習形式、平台、定價模式、年齡層、學科重點、連結方式與使用者類型分類-2026-2032年全球預測語言學習市場機會、成長要素、產業趨勢分析及預測(2026-2035年) 語言學習市場規模、佔有率和成長分析(按語言、學習方法、最終用戶、應用和地區分類)-2026-2033年產業預測

語言學習市場規模、佔有率和成長分析(按語言、學習方法、最終用戶、應用和地區分類)-2026-2033年產業預測