|

市場調查報告書

商品編碼

2062432

雲端英語學習:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031)Cloud-Based English Language Learning - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

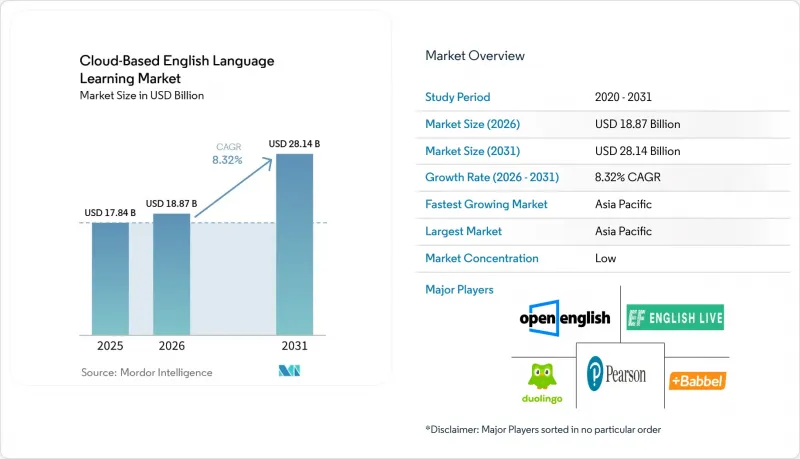

根據 Mordor Intelligence 預測,基於雲端的英語學習市場規模將從 2025 年的 178.4 億美元成長到 2026 年的 188.7 億美元,到 2031 年將達到 281.4 億美元,2026 年至 2031 年的複合年成長率為 8.32%。

本報告按最終用戶(個人學習者、教育機構、企業)、學習模式(基於應用程式的自學課程、線上直播課程等)、平台(行動應用程式、入口網站、虛擬實境)、年齡層(K-12、高等教育、成人)和地區進行細分。市場預測以美元計價。

全球雲端英語學習市場趨勢及洞察

PTE/IELTS 簽證相關考試的數位化準備:儘管移民政策發生變化,但考生人數保持穩定。

根據培生集團的報告,儘管某些出國目的地的政策收緊影響了簽證相關需求,導致2025年PTE學術英語考試的考生人數下降5%,但由於價格調整和續期,收入依然強勁,表明即使處理量減少,盈利能力依然穩健。 PTE認證涵蓋加拿大97%的大學和95%的學院,澳洲、紐西蘭和愛爾蘭的所有大學,以及英國99%的大學,為主要途徑的學術和移民途徑的數位化準備奠定了基礎。培生集團透過PTE Core擴展了產品線,推出了目標赴美留學的考生的PTE Express,並透過使考試設計與特定目的地的政策標準保持一致來擴大其覆蓋範圍。多鄰國英語測驗以實惠的價格在72小時內處理了數十萬考生的成績,擴大了其全球用戶群。這加劇了現有考試機構的競爭壓力,它們需要在保持考試信譽的同時,確保成績發布的速度和透明度。自2026年1月起,ETS將對托福iBT考試進行全面升級,引入自適應模組、更快的成績報告以及人工智慧驅動的學習功能,凸顯考試機構如何將教學融入考前階段,從而創造價值。隨著考試管理和監考向雲端轉移,考試機構正在重新思考其保障體系,以應對大規模身份驗證和安全問題,並透過提供更靈活的居家學習環境,在滿足教育和移民相關標準的前提下,支持基於雲端的英語學習市場。

企業強制提升英語語言技能:高度成熟的專案可使淨利潤翻倍,並將人工智慧採用率提高十倍。

根據EF發布的《2026年成熟度報告》,擁有高度成熟語言計畫的機構,其淨利是成熟度較低機構的兩倍,人工智慧(AI)採用率更是後者的十倍,這使得語言學習不再僅僅是一項可有可無的支出,而是提升營運效率的結構性驅動力。這個商業案例的核心在於人才儲備和市場進入。獲得認證的英語水平與更順暢的跨境業務運營、更高的新市場開拓成功率以及更可靠的跨區域流動性密切相關。 EF的英語程度評量顯示,即使在高分國家,口語和聽力仍然存在持續的差距。這導致預算分配從廣泛的通用內容轉向有針對性的口語練習和基於角色、針對特定業務任務量身定做的課程。預計2020年代後期商務英語方面的額外支出反映了高管們對提供符合歐洲語言共同參考框架(CEFR)的內容、頒發檢驗的認證以及提供將培訓投資與績效結果聯繫起來的群體分析的平台的偏好。 Pearson 的 Communications Coach 與 Microsoft 365 整合,使員工能夠在熟悉的工具中接收回饋,減少工作中意圖與行動之間的摩擦,從而提高採用率。這種以企業為導向的方法將透過增強對合規性評估、與人力資源資訊系統 (HRIS) 整合以及清晰的投資報酬率 (ROI) 報告的需求,使基於雲端的英語學習市場受益,這些報告能夠經受採購和審計審查。

自訂進度課程的完成率較低:雖然 MOOC 的平均留任率影響了其終身價值,但小組模式的完成率卻超過 70%。

自主學習的完成率仍然很低,迫使平台提高獲客成本以維持活躍用戶群,導致獲利速度放緩。結合定期小組學習、社區討論和即時互動的服務提供者報告稱,完成率更高,這使得混合模式在企業培訓中更具吸引力,因為企業培訓對結果檢驗至關重要。雖然 Duolingo 和其他大型應用程式透過微課程和遊戲化循環增強了使用者的日常參與度,但許多學習者仍需要結構化的輔導,才能將練習轉化為在 CEFR(歐洲語言通用參考框架)上的快速進步。線上輔導模式已證明能夠快速提升水平,並且結合人工智慧工具來支持課前和課後複習,為高價、基於結果的服務提供了商業價值。包含每月大量虛擬課程在內的即時課程生態系統提供了“學習連續性”,這僅靠自主學習內容很難實現,尤其是在口語和寫作方面。這些協同效應正在推動基於雲端的英語學習市場朝向混合架構發展,該架構既保持了數位化交付的規模經濟,也提高了完成率和學習成果的可靠性。

細分市場分析

儘管個人學習者在2025年將佔55%的市場佔有率,但企業市場預計到2031年將以17%的複合年成長率成長。這反映出雲端英語學習市場預算分配正轉向以清晰課責、檢驗的成果為導向。 EF的2026年研究表明,更成熟的語言課程與更高的利潤和更快的AI應用相關,從而增強了經營團隊對與歐洲語言共同參考框架(CEFR)等級和工作績效掛鉤的大規模培訓的支持。雇主透過有針對性的英語技能發展獲得了可衡量的收益,例如提高員工海外派遣的流動性,並降低跨境工作中的執行風險。培生集團的Communications Coach透過將學習提示整合到Microsoft 365等日常工具中,提高了人力資源和審計團隊的使用率,並簡化了合規性證明流程。 Preply的企業服務將儀錶板和CEFR追蹤功能與學習與發展(L&D)報告需求相結合,並將培訓時間與績效管理和採購標準連結起來。雲端英語學習市場,尤其是在企業合約方面,受益於能夠聚合需求的多席位協議。同時,零售業的獲利模式仍取決於從免費增值模式轉向付費模式的轉變以及應用程式商店的發展趨勢。

教育機構仍然是企業客戶的大規模群體,隨著英語能力成為大學入學和海外留學的必要條件,其規模還在不斷成長。面向消費者的平台仍然擁有最多的學習者,但與企業帳戶相比,其平均用戶收入較低,這促使企業更加重視基於學習群體的學習體驗和增值服務。企業買家青睞那些將人工智慧驅動的練習、教師指導和可審核的評估相結合的解決方案,這種組合鞏固了雲端英語學習產業在以採購為中心的領域中的地位。未來,最終用戶的組成將取決於供應商如何將績效報告與晉升標準和轉學框架有效連結。如果財務長能夠看到可預測的回報,這將有助於企業提升其在雲端英語學習市場的佔有率。

預計到2025年,基於應用程式的自學課程將佔據60%的市場佔有率,靈活的微學習模式將支援整個雲端英語學習市場中每日學習的頻率。同時,線上直播課程預計將以17.8%的複合年成長率成長,因為企業檢驗即時、便捷的教學方式,以驗證員工在實際情境中的口語和寫作能力。 Duolingo龐大的有效用戶群體證明了其「分散內容循環」模式在培養日常學習習慣方面的強大作用。然而,企業課程仍然要求學員在指定的里程碑節點獲得認證進展和導師認可。 Babbel Live每月提供大量虛擬課程,滿足學員對精心策劃的小組和指導課程的需求,幫助他們朝著晉升和調動等目標穩步前進。由於完成率較低,MOOC(大型開放式網路課程)的市場佔有率仍然較小,這降低了其對希望證明知識轉化為技能的雇主的吸引力。與純粹的自學相比,混合式學習模式結合了人工智慧驅動的預習和複習、定期的教師指導和社區支持,提高了完成率,增強了課程在審查中的可靠性。

對於教育機構和企業而言,混合式教學模式有助於收集和報告符合歐洲語言共同參考框架 (CEFR) 和企業內部工作框架的數據,簡化成本效益論證和合約續約流程。與直播和混合式教學模式相關的雲端英語學習市場規模龐大,反映了其高價策略,而高價策略又與經證實的學習效果和合規性要求相符。另一方面,自主學習應用程式則更注重規模經濟和學習者參與。服務提供者正在實施工作流程功能,例如自動生成的課程總結和複習練習,以彌補直播課程之間的空白,從而提高技能維持率和學習者感知價值。隨著這些模式的融合,雲端英語學習產業將繼續憑藉其經證實的有效性、教師素質以及與組織系統的深度整合來維持自身優勢。

區域分析

預計到2025年,亞太地區將佔據43%的市場佔有率,並在2031年之前保持22%的複合年成長率。這反映了行動優先的學習模式、政府對勞動力發展的政策要求,以及大規模學生湧入高等教育和全球人才流動管道。這些因素使亞太地區成為雲端英語學習市場的主要驅動力,並透過官民合作關係和與教育機構的合約不斷擴大課程覆蓋範圍。培生集團在最新財報中指出,拉丁美洲和中東地區的教育機構業務發展勢頭強勁。報告也指出,由於某些地區的政策變化,PTE考試的考生人數出現短期下降,凸顯了簽證相關類別對地緣政治變化的敏感度。能夠兼顧學術資格認證、居家考試和企業服務的供應商,最能掌握亞太地區多通路成長的機遇,同時有效管理移民敏感細分領域的政策風險。

在北美,企業培訓預算和靈活的訂閱模式是推動企業採用這些解決方案的主要因素,而整合到生產力套件中的企業解決方案因其無縫的用戶體驗而日益普及。 Duolingo 的 2025 年業績里程碑和指導方針強調了其「規模優先」的策略,該策略旨在支持產品系列的持續成長和擴展,而這些產品組合通常為面向消費者的產品設定價格標準。在歐洲,CEFR(歐洲語言通用參考框架)下的法規標準化和明確化為行業發展提供了助力,使服務提供者在成熟的合規性和隱私基礎設施方面擁有強大的優勢,這可能會影響跨境採購標準。英國和其他歐洲國家的大學入學和簽證申請途徑持續支撐著對 PTE 和 TOEFL 準備課程的穩定需求。同時,教育機構也需要雲端原生管理功能和快速成績報告來管理其學生群體。

隨著行動優先技術的普及和年輕人口的成長,中東、非洲和拉丁美洲等新興地區的雲端英語學習市場預計將從小小規模發展壯大,學習者群體也將隨之擴大。供應商與政府部門、大學和大型企業合作,可以加速擴大服務覆蓋範圍,同時滿足特定地區的合規性、身分驗證和評估需求。無論身處何地,行動端、網頁端和虛擬實境平台均可使用,這使得供應商能夠根據當地的基礎架構實際情況調整服務交付方式。同時,評估的可靠性和資料管治原則將成為大規模部署的通用基礎。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 為簽證相關目的而進行的PTE/IELTS備考數位化

- 企業在提升英語技能方面的義務

- GenAI導師提供的可擴展口說練習

- 通訊業者和設備的捆綁銷售正在推動合約數量的成長。

- 行動優先技術在新興市場的普及

- 將CEFR微證納入招募流程

- 市場限制因素

- 自學課程的完成率很低。

- 資料隱私和同意系統

- 應用程式商店費用會降低每位使用者平均收入 (ARPU)。

- 人工智慧幻覺會破壞信任

- 價值供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

- 關於考試輔導夥伴關係(雅思、PTE、托福)的考量

第5章 市場規模與成長預測

- 最終用戶

- 個別學習者

- 學術機構

- 公司/企業

- 不同的學習模式

- 基於應用程式的自學課程

- 線上直播課程

- 大型開放式網路課程(MOOC)

- 混合式/融合課程

- 按平台

- 行動應用

- 網路入口網站

- 虛擬實境/元宇宙教室

- 按年齡層

- K-12

- 高等教育(18-24歲)

- 成年人(25歲以上)

- 按地區

- 北美洲

- 加拿大

- 美國

- 墨西哥

- 南美洲

- 巴西

- 秘魯

- 智利

- 阿根廷

- 其他南美國家

- 歐洲

- 英國

- 德國

- 法國

- 西班牙

- 義大利

- 比荷盧經濟聯盟(比利時、荷蘭、盧森堡)

- 北歐國家(丹麥、芬蘭、冰島、挪威、瑞典)

- 其他歐洲國家

- 亞太地區

- 印度

- 中國

- 日本

- 澳洲

- 韓國

- 東南亞(新加坡、馬來西亞、泰國、印尼、越南、菲律賓)

- 其他亞太國家

- 中東和非洲

- 阿拉伯聯合大公國

- 沙烏地阿拉伯

- 南非

- 奈及利亞

- 其他中東和非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Duolingo

- Pearson(Mondly by Pearson;PTE;Versant)

- Open English

- EF English Live

- Babbel

- Busuu(Chegg)

- Cambly

- Preply

- italki

- Voxy

- goFLUENT

- Speexx

- Learnship

- Hult EF Corporate Education

- Berlitz Virtual Classroom

- EnglishCentral

- Wall Street English(Online)

- Rosetta Stone

- Memrise

- Lingoda

- ELSA Speak

- Speak(AI Tutor)

第7章 市場機會與未來展望

According to Mordor Intelligence, the cloud-Based english language learning market size is expected to grow from USD 17.84 billion in 2025 to USD 18.87 billion in 2026 and is forecast to reach USD 28.14 billion by 2031 at 8.32% CAGR over 2026-2031.

This report is Segmented by End User (Individual Learners, Academic Institutions, and Corporate/Enterprise), Learning Mode (Self-Paced App-Based Courses, Live Online Classes, and More), Platform (Mobile Apps, Web-Based Portals, and Virtual-Reality), Age Group (K-12, Higher-Education, Adults), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Cloud-Based English Language Learning Market Trends and Insights

Visa-Linked PTE/IELTS Prep Digitization: Test-Taker Volumes Stabilize Despite Migration Policy Flux

Pearson reported that PTE Academic volumes declined 5% in 2025 as policy tightening in certain destinations affected visa-linked demand, while sales held steady through price adjustments and renewals, indicating more resilient monetization even with lower throughput. PTE acceptance covers 97% of Canadian universities and 95% of colleges, all Australian, New Zealand, and Irish universities, and 99% of United Kingdom universities, which anchors digital-first preparation for academic and migration pathways in major corridors. Pearson extended the product set with PTE Core and launched PTE Express targeted at United States-bound learners, aligning test design with destination-specific policy criteria to deepen addressability. The Duolingo English Test processed results within 72 hours for hundreds of thousands of candidates at accessible price points and expanded its global acceptance base, increasing competitive pressure on incumbents to match its turnaround speed and transparency while preserving integrity. ETS modernized TOEFL iBT for January 2026 with adaptive sections, faster score reporting, and embedded AI-driven preparation, underscoring how test providers now integrate instruction to capture value upstream of exam day. As test delivery and proctoring shift to the cloud, providers are reworking assurance controls to manage identity verification and security at scale, supporting the Cloud-based English language learning market with more flexible, at-home journeys that still meet institutional and immigration standards.

Corporate English Upskilling Mandates: High-Maturity Programs Yield 2X Net Profit, 10X AI Deployment

EF's 2026 Maturity Report found that organizations with highly mature language programs achieved twice the net profit and deployed AI at ten times the rate of less mature peers, converting language learning from a discretionary line item to a structural driver of operational effectiveness. The business case centers on workforce readiness and market access, where certified English proficiency correlates with smoother cross-border execution, a higher rate of successful new-market entry, and more reliable assignment mobility. EF's proficiency mapping identified persistent gaps in speaking and listening, even in high-scoring countries, which steers budgets toward targeted speaking practice and role-based curriculum aligned with work tasks rather than broad, generic coverage. The projected incremental spend in Business English through the late 2020s reflects executives' preference for platforms that align content with the CEFR, issue verifiable credentials, and provide cohort analytics that link training inputs to performance outcomes. Pearson's Communications Coach integrates with Microsoft 365, so employees receive feedback within familiar tools, improving adoption by reducing the friction between intent and action at work. This enterprise orientation benefits the Cloud-based English language learning market by reinforcing demand for compliance-ready assessments, HRIS integration, and clear ROI reporting that withstands procurement and audit scrutiny.

Low Self-Paced Course Completion: Median MOOC Retention Compresses Lifetime Value, Cohort Models Counter With 70%+ Rates

Completion rates in self-paced formats remain low, forcing platforms to spend more on acquisition to maintain active learner bases and delaying monetization. Providers that combine scheduled cohorts, community discussion, and live touchpoints report higher completion rates, making blended models more attractive for enterprise training where verification matters. Duolingo and other high-scale apps improve daily engagement through micro-lessons and gamification loops, but many learners still need structured coaching to translate practice into rapid CEFR advancement. Marketplace tutoring models document faster level gains within short windows, which supports business cases for higher-priced, outcome-tied offers when paired with AI tools that prepare and reinforce between sessions. Live class ecosystems, including large volumes of virtual sessions each month, offer accountability that self-paced content alone struggles to deliver, especially for speaking and writing. The net effect pushes the Cloud-based English language learning market toward hybrid architectures that raise completion and outcome credibility while preserving the scale benefits of digital delivery.

Other drivers and restraints analyzed in the detailed report include:

- GenAI Tutors Enable Scalable Speaking Practice: Duolingo's "Video Call" Migration Prioritizes Growth Over Yield

- CEFR Micro-Credentials Embedded in Hiring: B2 Baselines and Verifiable Certificates Shape HR Workflows

- Data Privacy and Consent Regimes: Transparency Obligations Raise Compliance Costs and Favor Mature Operators

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Individual learners held a 55% share in 2025, while the enterprise segment is projected to grow at a 17% CAGR through 2031, reflecting budget shifts toward accountable, verifiable outcomes in the Cloud-based English language learning market. EF's 2026 findings that high-maturity language programs correlate with stronger profit and faster AI deployment support executive sponsorship of scaled training tied to CEFR levels and job performance. Employers secure measurable benefits from targeted English upskilling, including more reliable international assignment mobility and fewer execution risks in cross-border roles. Pearson's Communications Coach shows how embedding learning prompts into everyday tools like Microsoft 365 raises usage and simplifies compliance proof points for HR and audit teams. Preply's enterprise offering aligns dashboards and CEFR tracking with L&D reporting needs, linking training hours to performance management and procurement standards. The Cloud-based English language learning market size associated with enterprise contracts benefits from multi-seat agreements that aggregate demand. At the same time, retail monetization still depends on freemium conversion and app-store dynamics.

Academic institutions remain a sizable institutional buyer cohort and continue to expand as English proficiency becomes a career prerequisite for university placement and international study tracks. Consumer platforms continue to serve the largest volume of learners but face lower average revenue per user than business accounts, which deepens strategic emphasis on cohort-based experiences and add-on services. Enterprise buyers gravitate to solutions that blend AI practice with instructor interventions and auditable assessment, a combination that strengthens the Cloud-based English language learning industry's positioning in procurement-heavy categories. Over time, end-user mix will depend on how well vendors align outcome reporting with promotion criteria and mobility frameworks, which could broaden the enterprise slice of the Cloud-based English language learning market as CFOs see predictable returns.

Self-paced app-based courses held 60% share in 2025, confirming that flexible, micro-learning formats anchor daily practice frequency across the Cloud-based English language learning market. At the same time, live online classes are projected to grow at 17.8% CAGR as companies favor synchronous, accessible instruction to verify real-world speaking and writing performance. Duolingo's large active user base illustrates the power of bite-sized content loops that create daily habits. At the same time, enterprise cohorts still require certified progress and instructor sign-off at defined milestones. Babbel Live conducts a large volume of virtual classes each month, meeting demand for curated groups and guided sessions that keep learners on track toward promotion or migration goals. MOOCs remain a smaller slice due to lower completion rates, which reduces their attractiveness for employers requiring proof of transfer from knowledge to performance. Blended formats combine AI-driven preparation and recap with scheduled human interventions and community reinforcement, lifting completion compared with pure self-study and strengthening program credibility in audits.

For institutions and corporations, blended delivery supports data collection and reporting aligned with CEFR or in-house role frameworks, making it easier to justify spend and renewals. The Cloud-based English language learning market size linked to live and blended modes reflects premium pricing that attaches to verified outcomes and compliance needs. At the same time, self-paced apps prioritize scale economics and engagement. Providers are introducing workflow features such as automated lesson summaries and reinforcement exercises to bridge gaps between live sessions, thereby improving skill retention and perceived value. As these models converge, the Cloud-based English language learning industry continues to differentiate on verified impact, teacher quality, and integration depth with institutional systems.

Geography Analysis

Asia-Pacific held 43% share in 2025 and is projected to lead growth at a 22% CAGR through 2031, reflecting mobile-first study patterns, government workforce mandates, and large student cohorts entering higher education and global mobility pipelines. This profile positions APAC as the primary engine of the cloud-based English-language learning market, with public-private partnerships and institutional contracts expanding program reach. Pearson reported strong institutional momentum across Latin America and the Middle East in recent results, and noted short-term PTE volume softness tied to policy changes in specific corridors, underscoring the sensitivity of visa-linked categories to geopolitical shifts. Providers that balance academic credentials, at-home test delivery, and enterprise offerings are best placed to capture APAC's multi-channel growth while managing policy risk in migration-exposed subsegments.

North America's adoption is reinforced by corporate training budgets and strong subscription elasticity, with enterprise solutions that integrate into productivity suites gaining preference for their low-friction user experience. Duolingo's 2025 performance milestones and guidance highlighted a scale-first posture that supports ongoing engagement and broadening of the product portfolio, which often sets pricing references for consumer tiers. Europe benefits from CEFR standardization and regulatory clarity, which plays to the strengths of providers with mature compliance and privacy infrastructure and may influence procurement criteria across borders. University and visa pathways in the United Kingdom and other European destinations continue to underpin steady demand for PTE and TOEFL preparation. At the same time, institutions seek cloud-native administration and faster score reporting to manage cohorts.

The cloud-based English-language learning market in emerging regions of the Middle East and Africa, as well as Latin America, is set to grow from a smaller base as mobile-first adoption and youth demographics expand the learner pool. Vendors partnering with ministries, universities, and large employers can accelerate access and address localized compliance, identity, and assessment needs. Across regions, platform availability in mobile, web, and VR modes allows providers to tailor delivery to infrastructure realities. At the same time, assessment credibility and data governance principles act as common denominators in large-scale deployments.

- Duolingo

- Pearson (Mondly by Pearson

- PTE

- Versant)

- Open English

- EF English Live

- Babbel

- Busuu (Chegg)

- Cambly

- Preply

- italki

- Voxy

- goFLUENT

- Speexx

- Learnship

- Hult EF Corporate Education

- Berlitz Virtual Classroom

- EnglishCentral

- Wall Street English (Online)

- Rosetta Stone

- Memrise

- Lingoda

- ELSA Speak

- Speak (AI Tutor)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Visa-linked PTE/IELTS prep digitization

- 4.2.2 Corporate English upskilling mandates

- 4.2.3 GenAI tutors enable scalable speaking practice

- 4.2.4 Telco/device bundling boosts subscriptions

- 4.2.5 Mobile-first uptake in emerging markets

- 4.2.6 CEFR micro-credentials embedded in hiring

- 4.3 Market Restraints

- 4.3.1 Low self-paced course completion

- 4.3.2 Data privacy and consent regimes

- 4.3.3 App-store commissions reduce ARPU

- 4.3.4 AI hallucinations undermine trust

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

- 4.8 Insights on Test-prep partnerships (IELTS, PTE, TOEFL)

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By End User

- 5.1.1 Individual Learners

- 5.1.2 Academic Institutions

- 5.1.3 Corporate / Enterprise

- 5.2 By Learning Mode

- 5.2.1 Self-paced App-based Courses

- 5.2.2 Live Online Classes

- 5.2.3 Massive Open Online Courses (MOOCs)

- 5.2.4 Blended/Hybrid Programs

- 5.3 By Platform

- 5.3.1 Mobile Apps

- 5.3.2 Web-based Portals

- 5.3.3 Virtual-Reality/Metaverse Classrooms

- 5.4 By Age Group

- 5.4.1 K-12

- 5.4.2 Higher-Education (18-24)

- 5.4.3 Adults (25+)

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 Canada

- 5.5.1.2 United States

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Peru

- 5.5.2.3 Chile

- 5.5.2.4 Argentina

- 5.5.2.5 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Spain

- 5.5.3.5 Italy

- 5.5.3.6 BENELUX (Belgium, Netherlands, Luxembourg)

- 5.5.3.7 NORDICS (Denmark, Finland, Iceland, Norway, Sweden)

- 5.5.3.8 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 India

- 5.5.4.2 China

- 5.5.4.3 Japan

- 5.5.4.4 Australia

- 5.5.4.5 South Korea

- 5.5.4.6 South-East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines)

- 5.5.4.7 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 South Africa

- 5.5.5.4 Nigeria

- 5.5.5.5 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.4.1 Duolingo

- 6.4.2 Pearson (Mondly by Pearson; PTE; Versant)

- 6.4.3 Open English

- 6.4.4 EF English Live

- 6.4.5 Babbel

- 6.4.6 Busuu (Chegg)

- 6.4.7 Cambly

- 6.4.8 Preply

- 6.4.9 italki

- 6.4.10 Voxy

- 6.4.11 goFLUENT

- 6.4.12 Speexx

- 6.4.13 Learnship

- 6.4.14 Hult EF Corporate Education

- 6.4.15 Berlitz Virtual Classroom

- 6.4.16 EnglishCentral

- 6.4.17 Wall Street English (Online)

- 6.4.18 Rosetta Stone

- 6.4.19 Memrise

- 6.4.20 Lingoda

- 6.4.21 ELSA Speak

- 6.4.22 Speak (AI Tutor)

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment

全球外語學習市場規模、佔有率、趨勢和成長分析報告(2026-2034)

全球外語學習市場規模、佔有率、趨勢和成長分析報告(2026-2034) 語言學習和溝通技巧平台市場預測至2034年:按組成部分、學習形式、語言類型、最終用戶、應用和地區分類的全球分析

語言學習和溝通技巧平台市場預測至2034年:按組成部分、學習形式、語言類型、最終用戶、應用和地區分類的全球分析 講師主導語言培訓:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)

講師主導語言培訓:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年) 阿拉伯語學習市場:依學習風格、年齡層、學習目標、定價模式和學習者類型分類-2026-2032年全球市場預測

阿拉伯語學習市場:依學習風格、年齡層、學習目標、定價模式和學習者類型分類-2026-2032年全球市場預測 語言學習應用市場規模、佔有率和成長分析:按語言類型、部署模式、技術類型、收入模式、內容類型、使用者類型和地區分類 - 2026-2033 年產業預測

語言學習應用市場規模、佔有率和成長分析:按語言類型、部署模式、技術類型、收入模式、內容類型、使用者類型和地區分類 - 2026-2033 年產業預測 K-12雙語沉浸式教育市場機會、成長要素、產業趨勢分析及預測(2026-2035年)

K-12雙語沉浸式教育市場機會、成長要素、產業趨勢分析及預測(2026-2035年) 手語應用市場 - 全球產業規模、佔有率、趨勢、機會及預測(按產品類型、應用、訂閱模式、部署模式、地區和競爭格局分類,2021-2031年)兒童數學學習應用市場:依學習形式、平台、定價模式、年齡層、學科重點、連結方式與使用者類型分類-2026-2032年全球預測語言學習市場機會、成長要素、產業趨勢分析及預測(2026-2035年)

手語應用市場 - 全球產業規模、佔有率、趨勢、機會及預測(按產品類型、應用、訂閱模式、部署模式、地區和競爭格局分類,2021-2031年)兒童數學學習應用市場:依學習形式、平台、定價模式、年齡層、學科重點、連結方式與使用者類型分類-2026-2032年全球預測語言學習市場機會、成長要素、產業趨勢分析及預測(2026-2035年) 語言學習市場規模、佔有率和成長分析(按語言、學習方法、最終用戶、應用和地區分類)-2026-2033年產業預測

語言學習市場規模、佔有率和成長分析(按語言、學習方法、最終用戶、應用和地區分類)-2026-2033年產業預測