|

市場調查報告書

商品編碼

2062355

再生基礎油:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Recycled Base Oil - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

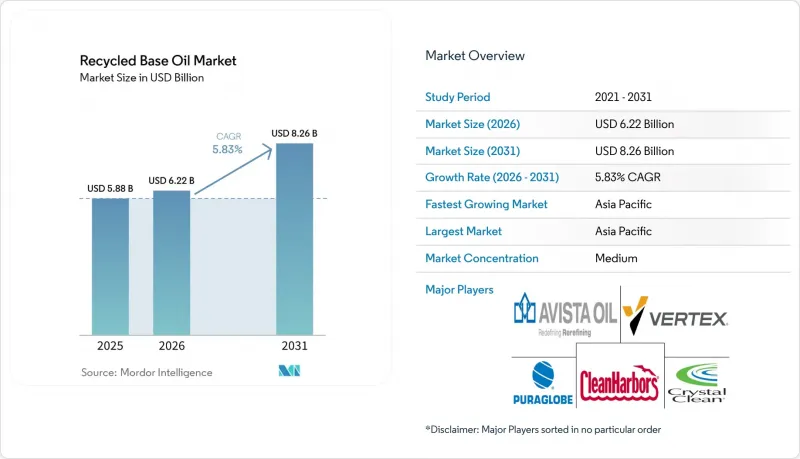

據 Mordor Intelligence 稱,2025 年再生基礎油市場價值為 58.8 億美元,預計到 2031 年將從 2026 年的 62.2 億美元成長至 82.6 億美元,預測期(2026-2031 年)複合年成長率為 5.83%。

本報告按原料來源(例如,廢舊汽車和引擎油)、精煉製程(例如,加氫處理和加氫精煉)、應用領域(例如,潤滑油和潤滑脂、金屬加工液)、終端用戶產業(例如,汽車和運輸設備的原始設備製造商/售後市場)以及地區(例如,亞太地區、北美地區)進行細分。市場預測以美元計價。

全球再生基礎油市場趨勢與洞察

加強法規,強制使用再生成分

州和國家層級的法規正在重新定義公共和私人車輛潤滑油的規格。加州要求州政府機構採購的潤滑油必須含有至少25%的精煉成分,這是美國的強制性要求。此舉符合美國環保署(EPA)的《綜合採購指南》。同時,科羅拉多和愛爾蘭分別於2024年和2025年推出了類似的法規。歐盟委員會報告稱,到2025年,61%的回收廢油將被重新製成基礎油,比例較歷史平均(少於50%)顯著提高,反映出歐盟政策正大力轉向閉合迴路回收。聯邦貿易委員會(FTC)更新的標籤標準要求明確揭露回收成分,從而減少「綠色清洗,並提高認證煉油商在採購過程中的競爭力。總而言之,這些措施擴大了目標需求,並保護了合規煉油商免受商品化帶來的價格壓力。

與I/II類基礎油相比具有成本優勢

2025年全年,精煉的II類基礎油價格將顯著優於原油。這是因為煉油商避免了原油蒸餾成本,並能利用輕餾分的餘熱進行回收。 PurePath的薄膜加氫處理系統每桶可降低10%至30%的生產成本,並透過整合式蒸氣回收系統進一步節省能源。在亞太地區,由於進口原油需繳納更高的運費和關稅附加費,這種成本優勢更為顯著。考慮到歐盟排放交易體系(EU ETS)等碳定價機制以及亞洲的試點項目,煉油商實現的37%至82%的生命週期二氧化碳減量將直接提高利潤率。

發展中地區缺乏再加工能力

新興經濟體正在產生大量廢油,但缺乏足夠的加氫基礎設施。例如,截至2024年,中國70.9萬噸名義加工能力的運轉率率僅11.5%。這是因為小規模酸和粘土加工廠無法滿足更嚴格的許可要求。同樣,在印度,預計2025年將產生300萬至400萬噸廢油,但只有50萬噸能夠由合法的再煉廠進行加工,大部分廢油被加工成低價值燃料或出口。即使有了YUNITCO在延布的20萬噸擴建計畫和計畫中的10萬噸開羅工廠,這些計畫也只能處理全部區域不到15%的廢油總量,凸顯了加工能力持續短缺的問題。

細分市場分析

到2025年,在成熟的經銷商和快修店回收網路的支持下,廢舊汽車和引擎油將佔再生基礎油市場佔有率的46.22%。相較之下,脂肪酸餾分和其他生質油預計到2031年將以5.88%的複合年成長率成長,成為原料中成長最快的。這一成長主要得益於低碳燃料標準的推行,該標準將可再生組分貨幣化,並促進聯合加工試驗。在中國,儘管危險廢棄物追蹤已擴展到鋼鐵和電力行業,但90%的廢油仍然來自引擎油。

將10-30%的生質油與精煉礦物基礎油(RRBO)混合的先導計畫正在生產符合API II/III類標準並可獲得加州低碳燃料標準(LCFS)積分的混合基礎油。如果積分價值超過每噸二氧化碳當量50美元,這些先導計畫可望實現商業化規模生產。變壓器油和船用油等特殊油品透過重新用於閉合迴路應用可供公共產業公司和航運公司進行審計。

至2025年,氫處理/氫精煉將佔再生基礎油市場佔有率的48.13%,預計到2031年將以6.03%的複合年成長率成長。這一成長主要得益於對氫處理設備的投資,這些設備能夠改善飽和烴含量和黏度指數,使其達到III類標準。雖然酸粘土法在注重成本的市場中仍然普遍存在,但日益嚴格的硫含量法規正迫使這些工藝逐步淘汰。 PURAGLOBE的「薄膜+氫處理」製程樹立了新的品質標準,實現了黏度指數超過120和硫含量低於10ppm。

Clean Harbors公司斥資2.1億至2.2億美元對其無溶劑瀝青廠維修,預計到2028年將生產600N重質基礎油,從而開拓重質柴油和齒輪油市場。 YUNITCO和其他印度煉油商正在採用氫處理流程,以避免使用過時的中性黏度體系,並符合歐盟6潤滑油標準。

區域分析

預計到2025年,亞太地區將佔全球銷售額的34.77%,並在2031年之前以6.22%的複合年成長率成長。在中國,2025年回收了510.8萬噸廢油(價值134.95億元人民幣/18.9億美元),預計到2026年將達到532.2萬噸(價值142.31億元人民幣/19.9億美元)。這項成長主要得益於危險廢棄物數位化追蹤系統和國營企業合資企業的發展。在印度,根據HPCL-嘉實多和印度石油再能源永續發展公司於2026年簽署的合作備忘錄,目標是安裝5萬至10萬噸II+類加氫處理設備,以降低對進口的依賴。

北美市場已趨於成熟,但我們仍致力於提升產品品質。 Clean Harbors公司預計2025年將處理2.43億加侖原油,並正在投資生產高黏度600N產品。 Vertex Energy公司計劃於2025年11月在其位於阿拉巴馬州莫比爾的工廠推出III類VTX-R4和VTX-R6產品,以滿足原始設備製造商(OEM)的碳排放法規要求。

歐洲61%的回收率反映了監管壓力。 Puraglobe的HyLube3技術支援根據與殼牌公司簽訂的為期12年的非公開銷售協議供應III類基礎油,進一步提升了該地區對高品質再生基礎油的關注度。

中東和非洲正努力解決產能不足的問題。 YUNITCO公司計劃在2026年將其位於延布的工廠產能擴建至20萬噸,並在2027年之前在開羅新計畫,這是該地區最大的投資項目,但即便如此,也只能處理海灣國家和北非地區不到15%的廢油。在南美洲,巴西Lwart公司投資10億雷亞爾,計劃將其年產能擴建至3.6億公升,象徵著該地區為此做出的努力,但其鄰國仍依賴進口。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 加強有關強制使用再生材料的法規

- 成本優勢:與初榨 I/II 基礎油相比

- OEM廠商的範圍3排放目標有利於RRBO

- 利用薄膜氫化處理技術對第三族RRBOs進行應用

- 政府車輛GPP再生材料含量要求

- 市場限制因素

- 發展中地區缺乏再加工能力

- 生物基酯類和PAGs替代品的威脅

- 根據《巴塞爾協議》對廢油出口實施限制

- 價值鏈分析

- 監理情勢

- 波特五力模型

第5章 市場規模與成長預測

- 按原料

- 二手汽車和引擎油

- 用於廠內製程和工業用途的油品

- 脂肪酸餾分和生質油

- 其他廢油(船用油、變壓器油等)

- 透過純化過程

- 氫氣處理/氫氣純化

- 酸和粘土處理

- 樹脂脫蠟和脫色

- 其他獨家流程(Revivoil、Vaxon 等)

- 透過使用

- 潤滑劑和潤滑脂混合物

- 金屬加工液(切削、成型)

- 油壓油和變壓器油

- 工業機械潤滑油

- 其他用途(橡膠加工、加工油)

- 按最終用戶行業分類

- 汽車和運輸設備OEM/售後市場

- 工業製造和重型機械

- 發電和公共產業

- 油田和鑽井服務

- 船舶/航運

- 其他終端用戶產業(鐵路、航空、國防)

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 東南亞國協

- 其他亞太國家

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲國家

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率和排名分析

- 公司簡介

- AVISTA OIL Deutschland GmbH

- CLEAN HARBORS, INC.

- Crystal Clean, Inc

- Exxon Mobil Corporation

- GFL Environmental Inc.

- Hemraj Petrochem Pvt. Ltd.

- Hydrodec Group

- Lwart Environmental Solutions

- Oil Salvage Ltd

- PURAGLOBE

- Shell plc

- Slicker Recycling

- Southern Oil

- Universal Lubricants

- Valvoline

- Vertex Energy

第7章 市場機會與未來展望

According to Mordor Intelligence, the recycled base oil market size was valued at USD 5.88 billion in 2025 and is estimated to grow from USD 6.22 billion in 2026 to reach USD 8.26 billion by 2031, at a CAGR of 5.83% during the forecast period (2026-2031).

This report is Segmented by Feedstock Source (Used Motor/Engine Oil, and More), Refining Process (Hydrotreating/Hydro-refining, and More), Application (Lubricant and Grease Blending, Metal-Working Fluids, and More), End-User Industry (Automotive and Transportation OEM/Aftermarket, and More), and Geography (Asia-Pacific, North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Recycled Base Oil Market Trends and Insights

Increasing Regulations Mandating Recycled Content

State and national regulations are redefining lubricant specifications for public and private fleets. California requires state agencies to purchase lubricants containing at least 25% re-refined content, aligning with the U.S. EPA Comprehensive Procurement Guideline, while Colorado and Ireland introduced similar statutes in 2024 and 2025, respectively The European Commission reported that 61% of collected waste oil was regenerated into base stock in 2025, a significant increase from historical averages below 50%, reflecting a strong policy shift toward closed-loop regeneration. Updated FTC labeling standards now mandate explicit recycled-content disclosure, reducing greenwashing and improving the competitiveness of certified re-refiners in procurement processes. Collectively, these measures expand addressable demand and protect compliant re-refiners from commoditized pricing pressures.

Cost Advantage vs. Virgin Group I/II Base Oils

Throughout 2025, re-refined Group II oils traded at a noticeable discount compared to virgin counterparts, as re-refiners avoid crude-distillation costs and utilize heat recovery from light distillates. PurePath's thin-film hydrotreaters report 10-30% lower manufacturing costs per barrel, with additional energy savings through integrated vapor recovery. The cost advantage is more pronounced in Asia-Pacific, where imported virgin oils incur freight and tariff premiums. When carbon pricing mechanisms, such as the EU ETS and pilot schemes in Asia, are factored in, the lifecycle CO2 reductions of 37-82% achieved by re-refiners directly enhance margins.

Insufficient Re-Refining Capacity in Developing Regions

Emerging economies generate significant volumes of waste oil but lack adequate hydrotreating infrastructure. For example, China's nominal capacity of 709,000 tons operated at only 11.5% utilization in 2024, as small acid-clay plants failed to meet stricter permitting requirements. Similarly, India generated 3-4 million tons of waste oil in 2025, but formal re-refiners could process only 500,000 tons, leaving the majority to low-value fuel or export streams. Even with YUNITCO's 200,000-ton Yanbu expansion and a planned 100,000-ton Cairo facility, these projects will address less than 15% of regional waste oil generation, underscoring persistent capacity shortfalls.

Other drivers and restraints analyzed in the detailed report include:

- OEM Scope-3 Carbon-Cut Targets Favoring RRBO

- Thin-Film Hydrotreating Unlocking Group III RRBO

- Substitution Threat from Bio-Based Esters and PAGs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Used motor and engine oil accounted for 46.22% of the recycled base oil market share in 2025, supported by established dealership and quick-lube collection networks. In comparison, fatty-acid distillates and other bio-oils are projected to grow at a 5.88% CAGR through 2031, representing the fastest growth among feedstocks. This increase is driven by low-carbon fuel standards that monetize renewable-content credits and encourage co-processing trials. China's waste-oil stream remains 90% engine-oil-derived as hazardous-waste tracking expands to steel and power industries.

Pilot blending 10-30% bio-oil with mineral re-refined base oil (RRBO) is producing hybrid base oils that meet API Group II/III specifications while qualifying for California LCFS credits. These pilot projects could scale commercially if credit values exceed USD 50 per ton CO2-equivalent. Specialty streams, such as transformer and marine oils, command premium margins when repurposed into closed-loop applications that utilities and shipping companies can audit.

Hydrotreating/hydro-refining accounted for 48.13% of the recycled base oil market size in 2025 and is expected to grow at a 6.03% CAGR through 2031. This growth is supported by investments in hydrogen units that enhance saturates and viscosity index to meet Group III standards. While acid-clay processes persist in cost-sensitive markets, they face increasing shutdown pressures due to tightening sulfur regulations. PURAGLOBE's thin-film-plus-hydrotreat process has set a new quality benchmark, achieving a viscosity index above 120 and sulfur levels below 10 ppm.

Clean Harbors' USD 210-220 million solvent de-asphalting retrofit is expected to produce 600N heavy base oil by 2028, opening opportunities in heavy-duty diesel and gear-oil markets. YUNITCO and Indian refiners are bypassing outdated neutral-clay systems and adopting hydrotreatment processes to align with Euro 6 lubricant standards.

Geography Analysis

Asia-Pacific generated 34.77% of global revenue in 2025 and will ascend at a 6.22% CAGR through 2031. China collected 5.108 million tons of waste oil valued at CNY 13.495 billion (USD 1.89 billion) in 2025, with projections of 5.322 million tons worth CNY 14.231 billion (USD 1.99 billion) in 2026. This growth is driven by digital hazardous-waste tracking and state-owned enterprise (SOE) joint ventures. India's 2026 MOUs between HPCL-Castrol and Indian Oil-Re Sustainability aim to establish 50,000-100,000-ton Group II+ hydrotreaters to reduce import dependency.

North America, while a mature market, is focusing on quality improvements. Clean Harbors processed 243 million gallons in 2025 and is investing in high-viscosity 600N production. Vertex Energy introduced Group III grades VTX-R4 and VTX-R6 in November 2025 from its Mobile, Alabama facility, targeting OEM carbon mandates.

Europe's 61% regeneration rate reflects regulatory pressures. PURAGLOBE's HyLube3 technology anchors Group III supply under a 12-year Shell offtake agreement, supporting the region's focus on high-quality recycled base oils.

The Middle-East and Africa hinge on capacity gap closures. YUNITCO's Yanbu expansion to 200,000 tons by 2026 and a 100,000-ton Cairo greenfield project by 2027 represent the region's largest investments but still address less than 15% of Gulf and North African waste-oil generation. In South America, Brazil's BRL 1 billion expansion by Lwart to 360 million liters per year highlights regional efforts, though neighboring countries remain reliant on imports.

- AVISTA OIL Deutschland GmbH

- CLEAN HARBORS, INC.

- Crystal Clean, Inc

- Exxon Mobil Corporation

- GFL Environmental Inc.

- Hemraj Petrochem Pvt. Ltd.

- Hydrodec Group

- Lwart Environmental Solutions

- Oil Salvage Ltd

- PURAGLOBE

- Shell plc

- Slicker Recycling

- Southern Oil

- Universal Lubricants

- Valvoline

- Vertex Energy

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing regulations mandating recycled content

- 4.2.2 Cost advantage vs. virgin Group I/II base oils

- 4.2.3 OEM Scope-3 carbon-cut targets favouring RRBO

- 4.2.4 Thin-film hydrotreating unlocking Group III RRBO

- 4.2.5 Government fleet GPP recycled-content mandates

- 4.3 Market Restraints

- 4.3.1 Insufficient re-refining capacity in developing regions

- 4.3.2 Substitution threat from bio-based esters and PAGs

- 4.3.3 Basel-driven restrictions on used-oil exports

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Forces

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Feedstock Source

- 5.1.1 Used Motor/Engine Oil

- 5.1.2 In-Plant Process and Industrial Oils

- 5.1.3 Fatty-Acid Distillates and Bio-oils

- 5.1.4 Other Waste Oils (Marine, Transformer etc.)

- 5.2 By Refining Process

- 5.2.1 Hydrotreating/Hydro-refining

- 5.2.2 Acid-Clay Treating

- 5.2.3 Resin De-wax/De-color

- 5.2.4 Other Proprietary Processes (Revivoil, Vaxon, etc.)

- 5.3 By Application

- 5.3.1 Lubricant and Grease Blending

- 5.3.2 Metal-working Fluids (Cutting, Forming)

- 5.3.3 Hydraulic and Transformer Oils

- 5.3.4 Industrial Machinery Lubrication

- 5.3.5 Other Applications (Rubber Process, Process Oils)

- 5.4 By End-user Industry

- 5.4.1 Automotive and Transportation OEM/Aftermarket

- 5.4.2 Industrial Manufacturing and Heavy Equipment

- 5.4.3 Power Generation and Utilities

- 5.4.4 Oilfield and Drilling Services

- 5.4.5 Marine and Shipping

- 5.4.6 Other End-user Industries (Rail, Aviation, Defense)

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 ASEAN Countries

- 5.5.1.6 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 AVISTA OIL Deutschland GmbH

- 6.4.2 CLEAN HARBORS, INC.

- 6.4.3 Crystal Clean, Inc

- 6.4.4 Exxon Mobil Corporation

- 6.4.5 GFL Environmental Inc.

- 6.4.6 Hemraj Petrochem Pvt. Ltd.

- 6.4.7 Hydrodec Group

- 6.4.8 Lwart Environmental Solutions

- 6.4.9 Oil Salvage Ltd

- 6.4.10 PURAGLOBE

- 6.4.11 Shell plc

- 6.4.12 Slicker Recycling

- 6.4.13 Southern Oil

- 6.4.14 Universal Lubricants

- 6.4.15 Valvoline

- 6.4.16 Vertex Energy

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

高性能工業潤滑油市場預測至2034年-按產品類型、基礎油、劑型、通路、應用、最終用戶和地區分類的全球分析

高性能工業潤滑油市場預測至2034年-按產品類型、基礎油、劑型、通路、應用、最終用戶和地區分類的全球分析 基礎油市場:2026-2032年全球市場預測(依產品等級、基礎油類型、應用、終端用戶產業及銷售管道)

基礎油市場:2026-2032年全球市場預測(依產品等級、基礎油類型、應用、終端用戶產業及銷售管道) 基礎油市場規模、佔有率、成長及全球產業分析:按類型、應用和地區的洞察,2026-2034年的預測

基礎油市場規模、佔有率、成長及全球產業分析:按類型、應用和地區的洞察,2026-2034年的預測 基油市場分析及預測(至2035年):類型、產品、應用、技術、最終用戶、形態、材質類型、製程、設備

基油市場分析及預測(至2035年):類型、產品、應用、技術、最終用戶、形態、材質類型、製程、設備 基礎油:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

基礎油:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 基礎油市場報告:按類型、組別、應用和地區分類(2026-2034年)

基礎油市場報告:按類型、組別、應用和地區分類(2026-2034年) 2026年全球基油市場報告

2026年全球基油市場報告 全球基礎油市場按類別、應用和地區分類-預測(至2030年)

全球基礎油市場按類別、應用和地區分類-預測(至2030年) 基礎油市場規模、佔有率和趨勢分析報告:按產品、應用、地區和細分市場預測(2026-2033 年)

基礎油市場規模、佔有率和趨勢分析報告:按產品、應用、地區和細分市場預測(2026-2033 年) 基礎油市場 - 全球產業規模、佔有率、趨勢、競爭格局、機會及預測(按原料、類型、應用、最終用途、地區和競爭情況分類,2021-2031年)

基礎油市場 - 全球產業規模、佔有率、趨勢、競爭格局、機會及預測(按原料、類型、應用、最終用途、地區和競爭情況分類,2021-2031年)