|

市場調查報告書

商品編碼

2062287

冷噴塗:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Cold Gas Spray Coating - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

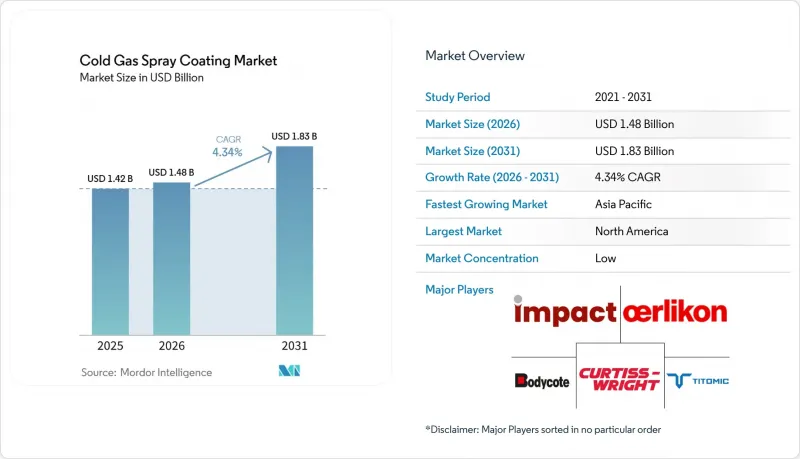

根據 Mordor Intelligence 預測,冷噴塗市場規模將從 2025 年的 14.2 億美元成長到 2026 年的 14.8 億美元,然後在 2031 年達到 18.3 億美元,2026 年至 2031 年的複合年成長率為 4.34%。

本報告按基材(金屬、陶瓷、聚合物和塑膠以及其他基材)、製程(高壓冷噴塗和低壓/中壓冷噴塗)、終端用戶產業(航太與國防、汽車及其他)以及地區(亞太地區、北美地區、歐洲地區、南美地區以及中東和非洲地區)進行細分。市場預測以美元計價。

全球冷氣噴塗市場趨勢及洞察

老舊軍用飛機機隊簡介

目前,冷噴塗技術正被用於修復鋁鎂合金零件,例如齒輪箱、機翼蒙皮和船體面板。這些零件先前需要在維修車間進行焊接或更換。美國海軍在獲得MIL-STD-3021認證後,已將此方法應用於F/A-18和MV-22的結構,使其符合海上作業要求,從而將維護時間從數月縮短至數週。由田納西大學和陸軍研究實驗室共同開發的貨櫃式系統可實現現場維修,無需後方補給即可提高艦隊戰備水準。設備供應商正擴大提供包含噴塗粉末供應的操作人員培訓,以加快現場部署速度。

CSAM認證用於在軌衛星維修

Titomic 和 NASA 正致力於研究受微隕石撞擊影響的衛星匯流排和天線組件。在微重力環境下,熔化修復方法並不安全。國際太空站上的 ASTROBEAT 實驗驗證了固體黏合技術的可行性,而 DNV 於 2026 年 4 月頒發的認證也增強了保險公司對機器人維護計畫融資的信心。如果這項技術成功應用,預計將衛星壽命延長至 25 年,並降低衛星星系更換的頻率。

與HVOF/等離子體方法相比,材料相容性有其局限性

冷噴塗技術對韌性金屬的接著效果顯著,但對碳化鎢鈷合金和氧化鋁等材料的性能較差。這些材料的孔隙率超過15%,黏接強度低於30 MPa。 SAE AMS7057標準明確規定了這些限制,迫使使用者採用結合高速火焰噴塗(HVOF)噴槍和冷噴塗槍的混合系統。然而,此類系統的初始投資超過100萬美元,限制了其應用範圍,目前只有大規模服務商才能採用。

細分市場分析

在2025年的冷噴塗市佔率中,金屬材料佔比高達66.12%。這主要得益於鋁合金6061、7075和2024系列,它們在氮氣流速下能夠有效結合。用於資料中心CPU的銅塗層可提供400 W/m*K的導熱係數,且不會發生氧化,鞏固了其在電子設備溫度控管領域的地位。鈦合金和鎳合金則應用於高利潤的推進系統和渦輪機領域。諾斯羅普·格魯曼公司的冷噴塗推力室經受住了高溫測試,未產生焊接應力。

到2031年,聚合物和塑膠市場將以5.32%的複合年成長率成長,其中PEEK和碳纖維外殼採用鋁皮作為電磁干擾屏蔽層。輕型外殼在冷噴塗市場越來越受歡迎,因為水冷式噴嘴和低於150 度C的氣流可以防止基板變形。陶瓷和玻璃由於其脆性,仍然是小眾領域,但它們可用於匯流排和工具維修,因為中等負載能力就足夠了。

區域分析

北美地區在美國國防部預算和NASA太空維修計畫的支持下,預計到2025年將佔全球銷售額的39.22%。位於戴斯空軍基地的中心正在製定B-1B轟炸機維修流程的標準化方案,以期在全球推廣應用。 Titomic公司位於阿拉巴馬州的AS9100認證生產線為波音和諾斯羅普·格魯曼公司供貨,而CenterLine和Triton公司正在合作開發用於一線維修的低SWaP(尺寸、重量、功耗)設備。聚合物金屬化技術在墨西哥的電動車供應鏈中也逐漸被應用,儘管目前規模較小。

預計到2031年,亞太地區的複合年成長率將達到5.23%。日本等離子技研公司在液化天然氣泵浦維護中實現了30兆帕的黏接強度目標。中國正在推動渦輪葉片更換的本地化,以減少對歐美MRO(維護、修理和大修)服務的依賴。韓國正在將銅噴塗技術引入其電動車逆變器生產線。印度和東南亞國協在汽車和電力行業已出現初步需求,但要實現更廣泛的應用,則需要本地化的氦氣替代品。

歐洲憑藉其航太和汽車產業叢集的支撐,維持著穩定的市場佔有率。荷蘭皇家航太中心於2026年3月以170萬美元的價格購入了Titomic公司的電池。德國弗勞恩霍夫研究所正在研究渦輪機罩的高熵合金粉末,而義大利RINA研究所則提供第三方檢驗,以加快原始設備製造商(OEM)的流程。在南美洲、中東和非洲,受巴西海上石油開發和沿岸地區腐蝕性石化資產帶來的機會驅動,小眾市場正在蓬勃發展。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 老舊軍艦簡介

- CSAM認證用於在軌衛星維修

- 電動車電力電子領域對高性能、低發熱塗層的需求日益成長

- 能夠實現下一代功能的HEA和奈米結構粉末

- 透過氦氣回收和氮氣混合系統,顯著降低營運成本。

- 市場限制因素

- 材料與HVOF/等離子體相容性的局限性

- 全球氦氣供應波動

- 安全關鍵部件認證延誤

- 價值鏈分析

- 波特五力模型

第5章 市場規模與成長預測

- 按基礎材料

- 金屬

- 陶瓷

- 聚合物和塑膠

- 其他基質

- 透過流程

- 高壓冷噴塗(HPCS)

- 低壓和中壓冷噴塗(L/MPCS)

- 按最終用戶行業分類

- 航太/國防

- 車

- 石油和天然氣

- 醫學領域

- 電子設備

- 其他終端用戶產業

- 按地區

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 其他亞太國家

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲國家

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率和排名分析

- 公司簡介

- Bodycote plc

- CenterLine(Windsor)Limited

- CSAT

- Curtiss-Wright Corporation

- Dycomet Europe

- Flame Spray Technologies BV

- HAI Inc.

- Hannecard Roller Coatings, Inc

- Impact Innovations GmbH

- Linde PLC

- OC Oerlikon Management AG

- Plasma Giken Co., Ltd.

- TITOMIC

- Turbine Surface Technologies

- VRC Metal Systems

第7章 市場機會與未來展望

According to Mordor Intelligence, the cold gas spray coating market size is expected to grow from USD 1.42 billion in 2025 to USD 1.48 billion in 2026 and is forecast to reach USD 1.83 billion by 2031 at 4.34% CAGR over 2026-2031.

This report is Segmented by Substrate (Metals, Ceramics, Polymers and Plastics, and Other Substrates), Process (High-Pressure Cold Spray and Low/Medium-Pressure Cold Spray), End-User Industry (Aerospace and Defense, Automotive, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Cold Gas Spray Coating Market Trends and Insights

Adoption Across Aging Military Fleets

Cold spray technology is now used to repair aluminum and magnesium components such as gearboxes, wing skins, and hull panels, which previously required depot-level welding or replacement. The U.S. Navy applies this method to F/A-18 and MV-22 structures following MIL-STD-3021 certification for airworthiness, reducing turnaround times from months to weeks. Containerized systems, developed by the University of Tennessee and the Army Research Laboratory, enable in-theater restoration, improving fleet readiness without the need for retrograde logistics. Equipment suppliers are increasingly bundling operator training with powder supply to accelerate field adoption.

Qualification of CSAM for In-Orbit Satellite Repair

Titomic and NASA are focusing on bus and antenna components affected by micrometeorite impacts, where molten repair methods are unsafe in microgravity. The ASTROBEAT experiment aboard the ISS demonstrated the viability of solid-state bonding, and DNV's April 2026 qualification has provided underwriters with the confidence to finance robotic servicing campaigns. Successful deployment of this technology could extend satellite service life to 25 years, reducing the frequency of constellation replacements.

Limited Material Compatibility vs. HVOF/Plasma

Cold spray technology bonds ductile metals effectively but performs poorly with materials like WC-Co and alumina, where porosities exceed 15%, and bond strength falls below 30 MPa. SAE AMS7057 outlines these limitations, prompting users to adopt hybrid systems that combine HVOF torches with cold spray guns. However, the capital investment for such systems exceeds USD 1 million, limiting adoption to large service bureaus.

Other drivers and restraints analyzed in the detailed report include:

- Demand for High-Performance Low-Heat Coatings on EV Power Electronics

- HEA and Nanostructured Powders Enabling Next-Gen Functionality

- Global Helium-Supply Volatility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Metals accounted for 66.12% of the 2025 cold gas spray coating market share, driven by aluminum grades 6061, 7075, and 2024 that bond effectively at nitrogen velocities. Copper coatings for data-center CPUs provide 400 W/m*K thermal paths without oxidation, enhancing the market's role in electronics thermal management. Titanium and nickel alloys contribute to high-margin propulsion and turbine applications; Northrop Grumman's cold-sprayed thrust chamber passed hot-fire qualification without weld stress.

Polymers and plastics are growing at a 5.32% CAGR through 2031, with PEEK and carbon-fiber housings incorporating aluminum skins for EMI shielding. Water-cooled injectors and gas streams below 150 °C prevent substrate distortion, enabling lightweight enclosures to gain traction in the cold gas spray coating market. Ceramics and glass remain niche due to their brittleness, but are used in busbar and tooling repairs where moderate load adhesion is sufficient.

Geography Analysis

North America held 39.22% of 2025 revenue, supported by Department of Defense budgets and NASA's space-repair programs. The Dyess Air Force Base center has standardized B-1B repairs for global replication. Titomic's AS9100-certified line in Alabama supplies Boeing and Northrop Grumman, while CenterLine and Triton collaborate on low-SWaP units for forward repair. Mexico's EV supply chain is adopting polymer metallization, though on a smaller scale.

Asia-Pacific is expected to grow at a 5.23% CAGR through 2031. Japan's Plasma Giken achieves 30 MPa bond targets for LNG pump maintenance. China is localizing turbine-blade renewals to reduce reliance on Western MROs. South Korea is integrating copper spraying into EV inverter production lines. India and ASEAN countries are showing initial demand in the automotive and power sectors, but require local helium alternatives for broader adoption.

Europe maintains a steady share, supported by aerospace and automotive clusters. The Royal Netherlands Aerospace Center purchased a USD 1.7 million Titomic cell in March 2026. Germany's Fraunhofer is researching HEA powders for turbine shrouds, while RINA's laboratory in Italy provides third-party validation, accelerating OEM processes. South America and the Middle-East and Africa are experiencing niche growth, driven by offshore oil opportunities in Brazil and corrosion-prone petrochemical assets in the Gulf.

- Bodycote plc

- CenterLine (Windsor) Limited

- CSAT

- Curtiss-Wright Corporation

- Dycomet Europe

- Flame Spray Technologies BV

- HAI Inc.

- Hannecard Roller Coatings, Inc

- Impact Innovations GmbH

- Linde PLC

- OC Oerlikon Management AG

- Plasma Giken Co., Ltd.

- TITOMIC

- Turbine Surface Technologies

- VRC Metal Systems

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Adoption across ageing military fleets

- 4.2.2 Qualification of CSAM for in-orbit satellite repair

- 4.2.3 Demand for high-performance low-heat coatings on EV power-electronics

- 4.2.4 HEA and nanostructured powders enabling next-gen functionality

- 4.2.5 Helium-recovery and N2-blend systems slashing operating cost

- 4.3 Market Restraints

- 4.3.1 Limited material compatibility vs. HVOF/plasma

- 4.3.2 Global helium-supply volatility

- 4.3.3 Qualification lag for safety-critical parts

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts

- 5.1 By Substrate

- 5.1.1 Metals

- 5.1.2 Ceramics

- 5.1.3 Polymers and Plastics

- 5.1.4 Other Substrates

- 5.2 By Process

- 5.2.1 High-Pressure Cold Spray (HPCS)

- 5.2.2 Low/Medium-Pressure Cold Spray (L/MPCS)

- 5.3 By End-user Industry

- 5.3.1 Aerospace and Defense

- 5.3.2 Automotive

- 5.3.3 Oil and Gas

- 5.3.4 Medical

- 5.3.5 Electronics

- 5.3.6 Other End-user Industries

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 Bodycote plc

- 6.4.2 CenterLine (Windsor) Limited

- 6.4.3 CSAT

- 6.4.4 Curtiss-Wright Corporation

- 6.4.5 Dycomet Europe

- 6.4.6 Flame Spray Technologies BV

- 6.4.7 HAI Inc.

- 6.4.8 Hannecard Roller Coatings, Inc

- 6.4.9 Impact Innovations GmbH

- 6.4.10 Linde PLC

- 6.4.11 OC Oerlikon Management AG

- 6.4.12 Plasma Giken Co., Ltd.

- 6.4.13 TITOMIC

- 6.4.14 Turbine Surface Technologies

- 6.4.15 VRC Metal Systems

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

冷噴塗塗料市場規模、佔有率和成長分析:按技術、材料、應用、終端用戶產業和地區分類-2026-2033年產業預測

冷噴塗塗料市場規模、佔有率和成長分析:按技術、材料、應用、終端用戶產業和地區分類-2026-2033年產業預測 全球溫度響應塗料市場

全球溫度響應塗料市場 TaC塗層全球市場研究報告,2026年

TaC塗層全球市場研究報告,2026年 2026年全球塗料市場報告

2026年全球塗料市場報告 低溫氣體噴塗市場:商業機會、成長要素、產業趨勢分析及2026-2035年預測氮化鈦塗層市場機會、成長要素、產業趨勢分析及2026-2035年預測。

低溫氣體噴塗市場:商業機會、成長要素、產業趨勢分析及2026-2035年預測氮化鈦塗層市場機會、成長要素、產業趨勢分析及2026-2035年預測。 氮化鈦塗層:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

氮化鈦塗層:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 遊艇塗料市場:2026-2032年全球市場預測(依塗料類型、樹脂類型、技術、船舶類型、應用領域、應用方法、通路和最終用戶分類)耐化學腐蝕塗料市場:商機、成長要素、產業趨勢分析及2026-2035年預測

遊艇塗料市場:2026-2032年全球市場預測(依塗料類型、樹脂類型、技術、船舶類型、應用領域、應用方法、通路和最終用戶分類)耐化學腐蝕塗料市場:商機、成長要素、產業趨勢分析及2026-2035年預測 無氫類類金剛石碳(DLC)塗層市場報告:按類型、應用和地區分類(2026-2034 年)

無氫類類金剛石碳(DLC)塗層市場報告:按類型、應用和地區分類(2026-2034 年)