|

市場調查報告書

商品編碼

2027497

耐化學腐蝕塗料市場:商機、成長要素、產業趨勢分析及2026-2035年預測Chemical Resistant Coating Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

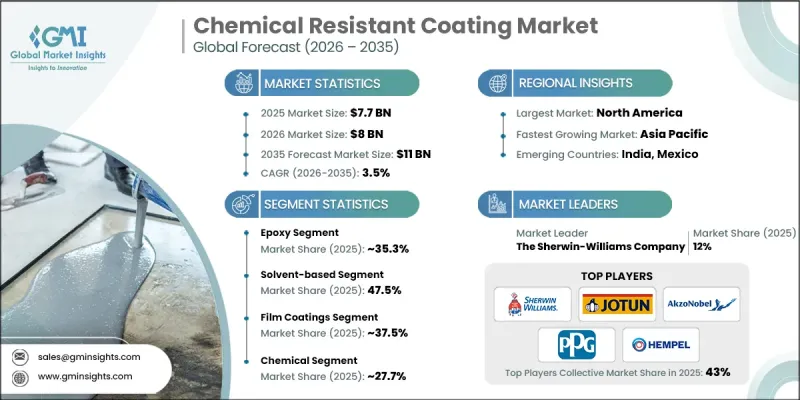

2025 年全球耐化學塗料市場價值為 77 億美元,預計到 2035 年將達到 110 億美元,年複合成長率為 3.5%。

市場成長的驅動力在於各行業對耐用防護解決方案日益成長的需求,這些解決方案能夠抵禦腐蝕性化學品的侵蝕,並延長關鍵資產的使用壽命。這些塗層的功能已超越了基本的防護,如今已成為製造業、能源和重工業等行業維持營運效率、最大限度減少運作以及延長設備壽命的必要手段。市場動態受到人們對永續性和負責任的工業實踐日益成長的關注的顯著影響。企業優先考慮符合環保標準的塗層解決方案,這些方案在維持高性能標準的同時,還能減少排放。製造商正在轉向創新產品開發策略,專注於兼顧耐久性和成本效益的環保配方。此外,北美透過先進的研發能力和工業現代化,持續推動創新,從而能夠開發出針對複雜運作條件量身定做的專用塗層技術。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 77億美元 |

| 預計金額 | 110億美元 |

| 複合年成長率 | 3.5% |

預計到2025年,環氧塗料的市佔率將達到35.3%,並將以3.4%的複合年成長率成長至2035年。這些塗料因其卓越的附著力、強大的阻隔保護性能以及耐化學腐蝕、機械損傷和耐熱衝擊等優點而廣受認可。其結構強度使其成為保護需要持續長期防護的關鍵工業設備的可靠選擇。結合環氧樹脂和聚氨酯技術的塗料系統具有更高的柔軟性、抗衝擊性和耐磨性,使其適用於涉及動態結構和複雜表面的應用。此外,矽基配方在長期暴露於高溫、氧化和惡劣大氣條件下的環境中繼續發揮至關重要的作用,因為它們即使在極端溫度下也能保持穩定性。

預計到2025年,溶劑型塗料市佔率將達到47.5%,並在2026年至2035年間以3.3%的複合年成長率成長。其卓越的成膜性能、優異的附著力和在化學腐蝕環境下的耐久性,是該領域持續佔據主導地位的關鍵因素。這些塗料系統尤其適用於需要可靠防護腐蝕性物質和應對溫度波動的應用。同時,隨著企業越來越重視永續性和合規性,對水性塗料的需求也不斷成長。這些塗料在保持高效能的同時,還能減少排放,提高職場的安全性,並有助於實現環境目標。粉末塗料也透過提供高效環保的塗裝解決方案,最大限度地減少材料浪費,並帶來長期的營運效益,從而鞏固了其在市場上的地位。

預計2025年,北美耐化學腐蝕塗料市場佔有率將達到35%,展現出強勁的成長潛力。憑藉完善的工業基礎、現代化的製造基礎設施和嚴格的環境法規,該地區已成為先進塗料技術的領先中心。這些因素促進了高性能、環保塗料系統的應用,使企業能夠在滿足安全標準的同時提高營運效率。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 中斷

- 影響產業的因素

- 促進因素

- 工業應用領域的需求不斷成長

- 嚴格的環境法規

- 擴大基礎建設

- 產業潛在風險與挑戰

- 高昂的生產成本

- 原物料價格波動

- 市場機遇

- 重工業向粉末塗裝技術的過渡

- 永續和生物基樹脂的開發

- 促進因素

- 成長潛力分析

- 監理情勢

- 波特五力分析

- PESTEL 分析

- 價格趨勢

- 按地區

- 依樹脂類型

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 專利趨勢

- 貿易統計(HS編碼)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續計劃

- 減少廢棄物策略

- 生產中的能源效率

- 環保意識的舉措

- 考慮碳足跡

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估算與預測:依樹脂類型分類,2022-2035年

- 環氧樹脂

- 聚酯纖維

- 螢光樹脂

- 聚氨酯

- 其他樹脂

第6章 市場估計與預測:依技術分類,2022-2035年

- 溶劑型

- 水溶液

- 粉末塗裝

- 其他

第7章 市場估計與預測:依薄膜厚度分類,2022-2035年

- 薄膜塗層

- 中等厚度塗層

- 高耐久性塗層

- 超厚膜系統

第8章 市場估算與預測:依最終使用者分類,2022-2035年

- 化學

- 化工廠

- 石油化工設施

- 化肥生產

- 其他

- 石油和天然氣

- 船

- 建築和基礎設施

- 其他

第9章 市場估計與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 其他歐洲地區

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲地區

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 其他中東和非洲地區

第10章:公司簡介

- The Sherwin-Williams Company

- Jotun A/S

- AkzoNobel NV

- PPG Industries, Inc.

- Hempel A/S

- Axalta Coating Systems

- RPM International Inc.

- Kansai Paint Co., Ltd.

- Nippon Paint Holdings Co., Ltd.

- Asian Paints Limited

- Carboline Company

- Tnemec Company, Inc.

The Global Chemical Resistant Coating Market was valued at USD 7.7 billion in 2025 and is estimated to grow at a CAGR of 3.5% to reach USD 11 billion by 2035.

Market growth is driven by the increasing need across industries for durable protective solutions that can withstand aggressive chemical exposure and extend the service life of critical assets. These coatings have evolved beyond basic protection and are now essential in maintaining operational efficiency, minimizing maintenance interruptions, and improving equipment longevity across sectors such as manufacturing, energy, and heavy engineering. Market dynamics are strongly influenced by the growing emphasis on sustainability and responsible industrial practices. Companies are prioritizing environmentally compliant coating solutions that reduce emissions while maintaining high performance standards. Manufacturers are shifting toward innovative product development strategies that focus on eco-friendly formulations capable of delivering durability and cost efficiency. In addition, North America continues to foster innovation through advanced research capabilities and industrial modernization, enabling the development of specialized coating technologies tailored for complex operating conditions.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $7.7 Billion |

| Forecast Value | $11 Billion |

| CAGR | 3.5% |

The epoxy-based coatings accounted for 35.3% share in 2025 and is expected to grow at a CAGR of 3.4% through 2035. These coatings are widely recognized for their superior adhesion, strong barrier protection, and resistance to chemical, mechanical, and thermal stress. Their structural strength makes them a reliable choice for safeguarding essential industrial equipment that requires consistent and long-term protection. Coating systems that combine epoxy and polyurethane technologies offer enhanced flexibility, impact resistance, and abrasion protection, making them suitable for applications involving dynamic structures and complex surfaces. In addition, silicone-based formulations continue to play an important role in environments exposed to prolonged heat, oxidation, and demanding atmospheric conditions due to their stability under extreme temperatures.

The solvent-based coatings segment held 47.5% share in 2025 and is anticipated to grow at a CAGR of 3.3% from 2026 to 2035. Their strong film-forming capabilities, excellent adhesion, and durability in chemically aggressive environments contribute to their continued dominance. These systems are particularly suited for operations that require reliable protection against corrosive substances and fluctuating temperature conditions. At the same time, water-based coatings are gaining traction as organizations increasingly focus on sustainability and regulatory compliance. These alternatives offer reduced emissions while maintaining effective performance, improving workplace safety, and supporting environmental goals. Powder coatings are also strengthening the market landscape by minimizing material waste and delivering efficient, environmentally responsible coating solutions with long-term operational benefits.

North America Chemical Resistant Coating Market accounted for 35% share in 2025 and continues to demonstrate strong growth potential. The region has established itself as a key hub for advanced coating technologies, supported by a well-developed industrial base, modern manufacturing infrastructure, and stringent environmental regulations. These factors encourage the adoption of high-performance and eco-friendly coating systems, enabling companies to align with safety standards while improving operational efficiency.

Leading companies operating in the Global Chemical Resistant Coating Market include PPG Industries, Inc., AkzoNobel N.V., The Sherwin-Williams Company, Hempel A/S, Jotun A/S, Axalta Coating Systems, RPM International Inc., Nippon Paint Holdings Co., Ltd., Kansai Paint Co., Ltd., Asian Paints Limited, Carboline Company, and Tnemec Company, Inc. Companies in the chemical resistant coating market are adopting strategies such as expanding production capacity and strengthening global distribution networks to meet increasing demand across industries. Significant investments in research and development are enabling the creation of advanced formulations that offer enhanced durability, improved chemical resistance, and reduced environmental impact. Strategic collaborations and partnerships are helping firms access new markets and broaden their customer base. Many companies are also focusing on sustainable innovation by developing low-emission and eco-friendly coating solutions to comply with evolving regulatory standards. In addition, mergers and acquisitions are being utilized to consolidate market position, enhance technological capabilities, and diversify product portfolios, while branding and marketing efforts emphasize performance reliability and long-term cost efficiency.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Resin Type

- 2.2.3 Technology

- 2.2.4 Film Thickness

- 2.2.5 End-Use

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand in industrial applications

- 3.2.1.2 Stringent environmental regulations

- 3.2.1.3 Growing infrastructure development

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High production costs

- 3.2.2.2 Fluctuating raw material prices

- 3.2.3 Market opportunities

- 3.2.3.1 Transition to powder coating technologies in heavy industry

- 3.2.3.2 Sustainable & bio-based resin development

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By resin type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Resin Type, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Epoxy

- 5.3 Polyester

- 5.4 Fluoropolymers

- 5.5 Polyurethane

- 5.6 Other resins

Chapter 6 Market Estimates and Forecast, By Technology, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Solvent-based

- 6.3 Water-based

- 6.4 Powder Coating

- 6.5 Others

Chapter 7 Market Estimates and Forecast, By Film Thickness, 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Thin Film Coatings

- 7.3 Medium Build Coatings

- 7.4 Heavy Duty Coatings

- 7.5 Ultra-Heavy Duty Systems

Chapter 8 Market Estimates and Forecast, By End-User, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Chemical

- 8.2.1 Chemical Processing Plants

- 8.2.2 Petrochemical Facilities

- 8.2.3 Fertilizer Manufacturing

- 8.2.4 Others

- 8.3 Oil & gas

- 8.4 Marine

- 8.5 Construction & infrastructural

- 8.6 Others

Chapter 9 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 The Sherwin-Williams Company

- 10.2 Jotun A/S

- 10.3 AkzoNobel N.V.

- 10.4 PPG Industries, Inc.

- 10.5 Hempel A/S

- 10.6 Axalta Coating Systems

- 10.7 RPM International Inc.

- 10.8 Kansai Paint Co., Ltd.

- 10.9 Nippon Paint Holdings Co., Ltd.

- 10.10 Asian Paints Limited

- 10.11 Carboline Company

- 10.12 Tnemec Company, Inc.

冷噴塗塗料市場規模、佔有率和成長分析:按技術、材料、應用、終端用戶產業和地區分類-2026-2033年產業預測

冷噴塗塗料市場規模、佔有率和成長分析:按技術、材料、應用、終端用戶產業和地區分類-2026-2033年產業預測 全球溫度響應塗料市場

全球溫度響應塗料市場 TaC塗層全球市場研究報告,2026年

TaC塗層全球市場研究報告,2026年 2026年全球塗料市場報告

2026年全球塗料市場報告 低溫氣體噴塗市場:商業機會、成長要素、產業趨勢分析及2026-2035年預測氮化鈦塗層市場機會、成長要素、產業趨勢分析及2026-2035年預測。

低溫氣體噴塗市場:商業機會、成長要素、產業趨勢分析及2026-2035年預測氮化鈦塗層市場機會、成長要素、產業趨勢分析及2026-2035年預測。 冷噴塗:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)氮化鈦塗層:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

冷噴塗:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)氮化鈦塗層:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 遊艇塗料市場:2026-2032年全球市場預測(依塗料類型、樹脂類型、技術、船舶類型、應用領域、應用方法、通路和最終用戶分類)

遊艇塗料市場:2026-2032年全球市場預測(依塗料類型、樹脂類型、技術、船舶類型、應用領域、應用方法、通路和最終用戶分類) 無氫類類金剛石碳(DLC)塗層市場報告:按類型、應用和地區分類(2026-2034 年)

無氫類類金剛石碳(DLC)塗層市場報告:按類型、應用和地區分類(2026-2034 年)