|

市場調查報告書

商品編碼

2062241

氮化鈦塗層:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Titanium Nitride Coating - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

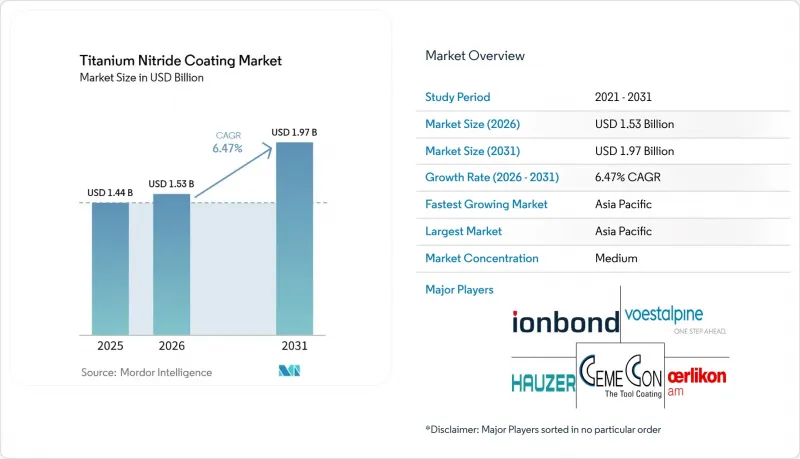

據 Mordor Intelligence 稱,2025 年氮化鈦塗層市值為 14.4 億美元,預計到 2031 年將從 2026 年的 15.3 億美元成長至 19.7 億美元,預測期(2026-2031 年)複合年成長率為 6.47%。

本報告按薄膜沉積技術(物理氣相沉積、化學氣相沉積、等離子噴塗PVD)、基板(金屬、陶瓷等)、應用(切削刀具、機械加工零件等)和地區(亞太地區、北美地區、歐洲地區、南美地區、中東和非洲地區)進行細分。市場預測以美元計價。

全球氮化鈦塗層市場趨勢及洞察

對耐磨和耐腐蝕塗層的需求日益成長

如今,工具機所有者不僅將氮化鈦 (TiN) 視為一種高階選擇,更將其視為一種節省成本的措施,它能將切削刀具的使用壽命延長三倍,並將射出成型單元的停機時間減少一半。 TiN 的維氏硬度超過 2000 Hv,摩擦係數接近 0.4,因此活塞環、渦輪增壓器軸和氣門挺桿等產品能夠滿足 ISO 6507 硬度測試和 ASTM G99 耐磨標準,同時也能避免使用致癌性的六價鉻層。預計到 2025 年,中國的刀具出口額將超過 200 億美元,印度的精密零件產業預計將以每年 12% 的速度成長。由於 TiN 具有更高的耐久性,因此結合了更低的人事費用,這兩個國家的產品價格都優於歐洲老牌企業。奈米複合材料 TiSiCN 的各種變體還能進一步降低 20% 的摩擦係數,並提高高達 2% 的燃油效率,符合更嚴格的 CAFE 標準。

精密加工和切削刀具產業的擴張

亞太地區五軸數控工具機的普及以及航太業重返北美,推動了對能夠承受200米/分鐘進給速度的氮化鈦(TiN)塗層硬質合金刀片的需求。高功率脈衝磁控濺鍍(HiPIMS)技術能夠在複雜形狀的工件上沉積高密度TiN塗層,使用者普遍反映,在Ti-6Al-4V銑削加工中,刀具壽命提高了300%。歐瑞康位於密西根州的工廠計劃於2026年1月運作,該工廠與其渦輪引擎加工叢集位於同一廠區,從而縮短了基於AS9100和Nadcap標準的認證流程。在生產關聯激勵措施(PLI)的支持下,印度的工具機產值在2025會計年度達到28億美元,這些生產連結獎勵計畫抵銷了塗層生產線的資本投資。

PVD/CVD設備的初始成本高

一台豪瑟Flexicoat 1000(配備用於1x1公尺模具的CARC+塗層室)售價超過200萬美元,加上預處理、遮蔽和後處理設備,價格很容易超過500萬美元。印度中小企業(SME)的資本財貸款利率高達9-11%,投資回收期超過七年,而它們的德國競爭對手的資金籌措卻低於5%。因此,市場形成了寡占格局,以歐瑞康(Oerlikon)、Ionbond和Bodycoat等財力雄厚的老牌公司為中心,這些公司在全球各地部署設備並收取高額塗層費用。

細分市場分析

到2025年,PVD製程將佔據氮化鈦塗層市場71.89%的佔有率。這主要歸功於其能夠實現1-5µm的薄膜厚度,並兼具超過2000 HV的硬度以及美觀的金色光澤,而這正是切削刀具和消費電子產品買家所追求的特性。 CVD製程在10-20µm厚度和深孔附著力方面仍佔有一席之地,但其800 度C的循環溫度限制了其在鋁和聚合物基板的應用。採用等離子噴塗PVD製程製備的厚TiN塗層能夠保護渦輪壓縮機葉片免受沙粒和鹽分的侵蝕。 BryCoat公司的PS-PVD產品系列檢驗,其疲勞強度僅比未經處理的Ti-6Al-4V合金降低0.24%,並且預計到2031年將以7.03%的複合年成長率成長。

HiPIMS技術源自於PVD技術,透過輸送高能量離子實現高密度、低應力塗層。 Ionbond公司的Flexicoat系統將於2025年在瑞典推出,屆時將使當地航太級鈦合金的產能提升40%,工具壽命延長300%。同時,在3D積體電路擴散阻擋層中形成的ALD TiN塗層雖然仍屬於CVD製程的一個子領域,但在晶圓層面已確立了其溢價地位。 ISO 14577硬度基準讓買家根據性能而非製程選擇供應商,從而加速了技術轉型,削弱了PVD的優勢。

區域分析

亞太地區將主導氮化鈦塗層市場,預計到2025年將佔全球銷售額的41.87%,並預計在2031年之前以7.22%的複合年成長率持續成長。中國憑藉著22萬噸的海綿鈦產量和超過200億美元的設備出口額,為該地區提供了堅實的基礎。日本投資390億日圓的「大阪鈦業」計畫預計到2027年將新增1萬噸產能。台灣和韓國正在推動3奈米節點原子層沉積(ALD)氮化鈦擴散阻擋層的需求,這得益於台積電(TSMC)的取得專利的CMP相容阻擋層技術。東南亞國協正在建造入門級物理氣相沉積(PVD)生產線,但高昂的資本投資成本和資金籌措限制了短期產量。

預計到2025年,北美將成為全球第二大生產地,主要得益於航太業重返北美以及《通貨膨脹控制法案》下的氫能補貼政策。歐瑞康公司位於密西根州的工廠將於2026年1月投產,該工廠將與其渦輪機零件加工中心位於同一廠址。同時,博迪科特公司斥資800萬美元收購了頻譜 Thermal Processing公司,這將擴大其在美國東北部獲得Nadcap認證的真空熱處理和氮化鈦(TiN)加工能力。加拿大和墨西哥的塗層公司正利用美墨加協定(USMCA)的相關規定,將其塗層流程轉移到更靠近原始設備製造商(OEM)最終組裝的位置,以降低關稅風險。

歐洲憑藉德國的精密工程、義大利的奢侈品產業以及法國圖盧茲的航太產業叢集,保持強大的市場地位。 Ionbond公司在瑞典產能提升40%,並在圖盧茲擴建其類鑽石碳(DLC)生產線,顯示現有企業集中在空中巴士和一級供應商附近。歐盟的REACH奈米材料註冊計畫和綠色交易的氫能目標都在影響市場需求。大規模塗料公司承擔著合規成本,這限制了市場的分散化。南美洲和中東市場雖然規模較小,但仍在持續成長,其中巴西整形外科植入市場兩位數的成長以及沙烏地阿拉伯的「2030願景」產業計畫是推動需求成長的最初催化劑。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 市場分析與定義的前提條件

- 分析範圍

第2章 分析方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 對耐磨和耐腐蝕塗層的需求日益成長

- 精密加工和切削刀具產業的擴張

- 在生物醫學植入和醫療設備的應用日益廣泛

- 應用於電子設備和奢侈品的裝飾性飾面

- 氫電解槽雙極板的電導率要求

- 3D IC封裝中擴散阻擋層的整合

- 市場限制因素

- PVD/CVD設備的初始成本高

- 在惡劣化學環境下的性能限制

- 對奈米氮化鈦的職業安全和環境影響進行審查

- 高純度鈦原料供應風險

- 價值鏈分析

- 波特五力分析

第5章:預測市場規模與成長率

- 透過成膜技術

- 物理氣相沉積(PVD)

- 化學氣相沉積(CVD)

- 等離子噴塗PVD(PS-PVD)

- 按基板

- 金屬(鐵、鋁、鈦合金)

- 陶瓷

- 塑膠聚合物

- 其他基板(玻璃、複合材料)

- 透過使用

- 切削刀具和機械加工零件

- 模具

- 醫療器械和牙科器械

- 汽車零件

- 家用電子電器和裝飾金屬製品

- 航太零件

- 其他應用(能源、時鐘、光學儀器)

- 按地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 東南亞國協

- 其他亞太國家

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲國家

- 亞太地區

第6章 競爭情勢

- 市場集中度

- 策略舉措和趨勢

- 市佔率和排名分析

- 公司簡介

- Acree Technologies Inc.

- Advanced Coating Technologies

- Bodycote plc

- BryCoat Inc.

- CemeCon AG

- IHI HAUZER TECHNO COATING BV

- Ion Vacuum(IVAC)Technologies Corp.

- Ionbond

- NISSIN ELECTRIC Co.

- Northeast Coating Technologies

- OC Oerlikon Management AG

- Platit AG

- Richter Precision Inc.

- Surface Engineering Technologies LLC

- Techmetals Inc.

- Teer Coatings Ltd.

- TS VTI

- voestalpine eifeler Group

- Wallwork Advanced Coatings

第7章 市場機會與未來展望

According to Mordor Intelligence, the titanium nitride coating market size was valued at USD 1.44 billion in 2025 and is estimated to grow from USD 1.53 billion in 2026 to reach USD 1.97 billion by 2031, at a CAGR of 6.47% during the forecast period (2026-2031).

This report is Segmented by Deposition Technology (Physical Vapor Deposition, Chemical Vapor Deposition, and Plasma-Spray PVD), Substrate Material (Metals, Ceramics, and More), Application (Cutting Tools and Machining Components, and More), and Geography (Asia-Pacific, North America, Europe, South America, and the Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Titanium Nitride Coating Market Trends and Insights

Growing Demand for Wear- and Corrosion-Resistant Coatings

Machinery owners now view TiN not as a premium option but as a cost-of-doing-business safeguard that triples cutting-tool life and halves downtime in injection-molding cells. Vickers hardness above 2,000 Hv and a friction coefficient near 0.4 allow piston rings, turbocharger shafts, and valve lifters to move away from carcinogenic hexavalent chromium layers while still meeting ISO 6507 hardness tests and ASTM G99 wear criteria. China's tooling exports exceeded USD 20 billion in 2025, and India's precision-parts sector grew 12% year-on-year, both undercutting European incumbents by pairing low-labor cost with TiN-enhanced durability. Nanocomposite TiSiCN variants further shave friction by 20%, yielding up to 2% fuel-economy gains as CAFE standards tighten.

Expansion of Precision Machining and Cutting-Tool Sectors

Five-axis CNC proliferation in Asia-Pacific and aerospace reshoring across North America heighten demand for TiN-coated carbide inserts that survive 200 m/min feed rates. High-power impulse magnetron sputtering (HiPIMS) packs denser TiN onto complex geometries; users routinely report 300% tool-life improvements when milling Ti-6Al-4V. Oerlikon's January 2026 Michigan plant is co-located with turbine-engine machining clusters, shortening qualification loops under AS9100 and Nadcap. India's machine-tool output reached USD 2.8 billion in fiscal 2025, bolstered by Production-Linked Incentives that offset coating-line capital outlays.

High Upfront Cost of PVD/CVD Equipment

A single Hauzer Flexicoat 1000, with CARC+ chambers rated for 1 X 1 m molds, costs more than USD 2 million and balloons past USD 5 million when pre-cleaning, masking, and post-processing are added. Indian SMEs (small and medium enterprises) pay 9-11% interest on capital-goods loans, stretching payback beyond seven years, whereas German rivals finance below 5%. The result is oligopolistic clustering around deep-pocketed incumbents, Oerlikon, Ionbond, Bodycote, who amortize gear across global centers and command premium coating tariffs.

Other drivers and restraints analyzed in the detailed report include:

- Rising Use in Biomedical Implants and Medical Devices

- Adoption in Decorative Finishes for Electronics and Luxury Goods

- Nano-TiN Workplace Safety and Environmental Scrutiny

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

PVD represented 71.89% of the Titanium Nitride Coating market share in 2025, owing to its 1-5 µm films that marry greater than or equal to 2,000 HV hardness with decorative gold luster demanded by cutting-tool and consumer-electronics buyers. CVD retains footholds where 10-20 µm thickness or deep-hole conformality trump temperature limits, yet its 800°C cycles constrain aluminum and polymer substrates. Plasma-spray PVD's thick TiN skirts protect turbine compressor blades from sand and salt erosion; BryCoat's PS-PVD product portfolio, validated by 0.24% fatigue-strength drop versus bare Ti-6Al-4V, is scaling at 7.03% CAGR into 2031.

HiPIMS, an outgrowth of PVD, packs extra ion energy that yields dense, low-stress coatings; Ionbond's 2025 installation of Flexicoat machines in Sweden raised local capacity 40%, enabling 300% tool-life gains on aerospace-grade titanium alloys. Meanwhile, ALD TiN inside 3D-IC diffusion barriers remains a CVD sub-segment but commands wafer-level premiums. ISO 14577 hardness benchmarking now allows buyers to select suppliers by performance rather than process, fostering cross-technology substitution that chips PVD dominance.

Geography Analysis

Asia-Pacific dominated the Titanium Nitride Coating market with 41.87% revenue in 2025 and is projected to expand at 7.22% CAGR to 2031. China anchors the regional base with 220,000 tons of sponge output and more than USD 20 billion in tool exports, while Japan's JPY 39 billion Osaka Titanium project adds 10,000 tons of capacity by fiscal 2027. Taiwan and South Korea steer demand for ALD TiN diffusion barriers at 3 nm nodes, aided by TSMC's patented CMP-compatible barrier technology. ASEAN nations are erecting entry-level PVD lines, but high capital costs and financing gaps temper near-term throughput.

North America ranked second in 2025, propelled by aerospace reshoring and the Inflation Reduction Act hydrogen credits. Oerlikon's January 2026 Michigan hub is co-located with turbine-component machining centers, while Bodycote's USD 8 million Spectrum Thermal Processing buy enlarges Nadcap-accredited vacuum heat-treat and TiN capacity in the U.S. Northeast. Canadian and Mexican coaters gain under USMCA (United States-Mexico-Canada Agreement) rules, relocating deposition closer to OEM final assembly lines and trimming tariff exposure.

Europe retains a strong foothold via Germany's precision engineering, Italy's luxury-goods segment, and France's Toulouse aerospace corridor. Ionbond's 40% Sweden capacity boost and Toulouse DLC line expansion show incumbents clustering near Airbus and Tier-1 suppliers. EU REACH nano-material registration and Green Deal hydrogen targets both shape demand; larger coaters shoulder compliance costs, nudging fragmentation downward. South America and the Middle East remain smaller but rising; Brazil's double-digit orthopedic-implant growth and Saudi Vision 2030 industrial plans are early demand sparks.

- Acree Technologies Inc.

- Advanced Coating Technologies

- Bodycote plc

- BryCoat Inc.

- CemeCon AG

- IHI HAUZER TECHNO COATING B.V.

- Ion Vacuum (IVAC) Technologies Corp.

- Ionbond

- NISSIN ELECTRIC Co.

- Northeast Coating Technologies

- OC Oerlikon Management AG

- Platit AG

- Richter Precision Inc.

- Surface Engineering Technologies LLC

- Techmetals Inc.

- Teer Coatings Ltd.

- TS VTI

- voestalpine eifeler Group

- Wallwork Advanced Coatings

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing demand for wear- and corrosion-resistant coatings

- 4.2.2 Expansion of precision machining and cutting-tool sectors

- 4.2.3 Rising use in biomedical implants and medical devices

- 4.2.4 Adoption in decorative finishes for electronics and luxury goods

- 4.2.5 Hydrogen-electrolyser bipolar-plate conductivity needs

- 4.2.6 3D-IC packaging diffusion-barrier integration

- 4.3 Market Restraints

- 4.3.1 High upfront cost of PVD/CVD equipment

- 4.3.2 Performance limits under aggressive chemistries

- 4.3.3 Nano-TiN workplace safety and environmental scrutiny

- 4.3.4 High-purity titanium feedstock supply risk

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Deposition Technology

- 5.1.1 Physical Vapor Deposition (PVD)

- 5.1.2 Chemical Vapor Deposition (CVD)

- 5.1.3 Plasma-Spray PVD (PS-PVD)

- 5.2 By Substrate Material

- 5.2.1 Metals (Steel, Aluminium, and Ti-Alloys)

- 5.2.2 Ceramics

- 5.2.3 Plastics and Polymers

- 5.2.4 Other Substrates (Glass and Composites)

- 5.3 By Application

- 5.3.1 Cutting Tools and Machining Components

- 5.3.2 Molds and Dies

- 5.3.3 Medical and Dental Instruments

- 5.3.4 Automotive Components

- 5.3.5 Consumer Electronics and Decorative Hardware

- 5.3.6 Aerospace Parts

- 5.3.7 Other Applications (Energy, Watches, and Optical Devices)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 Japan

- 5.4.1.3 India

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves and Developments

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, Recent Developments)}

- 6.4.1 Acree Technologies Inc.

- 6.4.2 Advanced Coating Technologies

- 6.4.3 Bodycote plc

- 6.4.4 BryCoat Inc.

- 6.4.5 CemeCon AG

- 6.4.6 IHI HAUZER TECHNO COATING B.V.

- 6.4.7 Ion Vacuum (IVAC) Technologies Corp.

- 6.4.8 Ionbond

- 6.4.9 NISSIN ELECTRIC Co.

- 6.4.10 Northeast Coating Technologies

- 6.4.11 OC Oerlikon Management AG

- 6.4.12 Platit AG

- 6.4.13 Richter Precision Inc.

- 6.4.14 Surface Engineering Technologies LLC

- 6.4.15 Techmetals Inc.

- 6.4.16 Teer Coatings Ltd.

- 6.4.17 TS VTI

- 6.4.18 voestalpine eifeler Group

- 6.4.19 Wallwork Advanced Coatings

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

全球溫度響應塗料市場

全球溫度響應塗料市場 TaC塗層全球市場研究報告,2026年

TaC塗層全球市場研究報告,2026年 2026年全球塗料市場報告

2026年全球塗料市場報告 低溫氣體噴塗市場:商業機會、成長要素、產業趨勢分析及2026-2035年預測氮化鈦塗層市場機會、成長要素、產業趨勢分析及2026-2035年預測。

低溫氣體噴塗市場:商業機會、成長要素、產業趨勢分析及2026-2035年預測氮化鈦塗層市場機會、成長要素、產業趨勢分析及2026-2035年預測。 遊艇塗料市場:2026-2032年全球市場預測(依塗料類型、樹脂類型、技術、船舶類型、應用領域、應用方法、通路和最終用戶分類)耐化學腐蝕塗料市場:商機、成長要素、產業趨勢分析及2026-2035年預測

遊艇塗料市場:2026-2032年全球市場預測(依塗料類型、樹脂類型、技術、船舶類型、應用領域、應用方法、通路和最終用戶分類)耐化學腐蝕塗料市場:商機、成長要素、產業趨勢分析及2026-2035年預測 無氫類類金剛石碳(DLC)塗層市場報告:按類型、應用和地區分類(2026-2034 年)電子束固化塗料市場:依樹脂類型、配方、設備類型及應用分類-2026-2032年全球市場預測前表面塗料市場:2026-2032年全球市場預測(依產品種類、裝飾性塗料類型、價格範圍、包裝規格、應用、最終用戶產業及通路分類)

無氫類類金剛石碳(DLC)塗層市場報告:按類型、應用和地區分類(2026-2034 年)電子束固化塗料市場:依樹脂類型、配方、設備類型及應用分類-2026-2032年全球市場預測前表面塗料市場:2026-2032年全球市場預測(依產品種類、裝飾性塗料類型、價格範圍、包裝規格、應用、最終用戶產業及通路分類)