|

市場調查報告書

商品編碼

2062143

美國零售物流:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)United States Retail Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

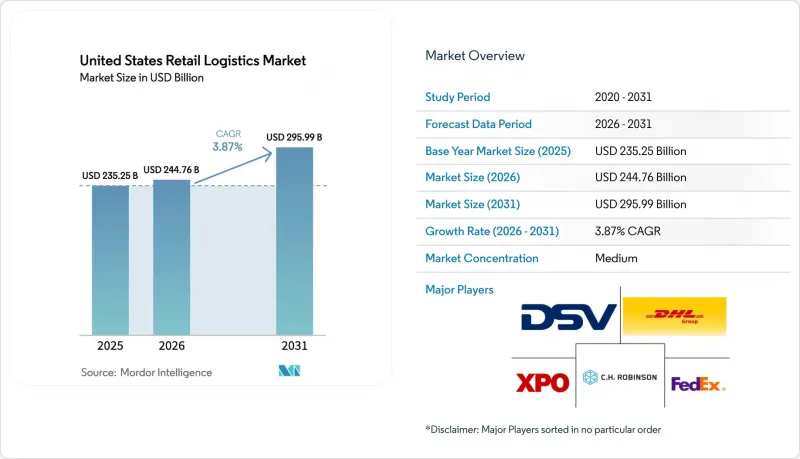

據 Mordor Intelligence 稱,2025 年美國零售物流市場價值為 2352.5 億美元,預計到 2031 年將達到 2959.9 億美元,而 2026 年為 2447.6 億美元,預測期(2026-2031 年)的複合成長率為 3.87%。

零售商正開始將門市轉型為履約中心,溫控網路正在擴展以滿足複雜的生物製藥產品線需求,而聯邦政府的「綠色走廊」計畫正在加速向電動長途運輸車輛的轉型。本報告按服務類型(運輸、倉儲物流及其他)、溫控方式(常溫、冷藏、冷凍、非低溫運輸)、產品類型(食品飲料、服裝鞋帽、消費電子產品、醫療保健及藥品及其他)和地區(東北部、東南部、西南部)進行細分。市場預測以美元計價。

美國零售物流市場趨勢與洞察

拓展全通路線上購買線下取貨(BOPIS)模式

線上購買,商店提 (BOPIS) 模式將數微型倉配,從而實現快速訂單處理。這種模式降低了最後一公里配送成本,同時由於顧客提貨時往往會進行額外購買,因此也增加了門店客流量。隨著大型連鎖店增加對即時庫存可見性和無縫應用程式訂購系統的投入,競爭壓力日益加劇,顧客對速度和可靠性的期望也越來越高。然而,中小零售商往往難以滿足這些期望。隨著郊區人口的成長和電子商務滲透率的提高,BOPIS 正逐漸附加價值服務轉變為標準的履約方式。

生物製藥主導對超低溫的需求

生物製藥、細胞和基因療法以及mRNA治療方法的快速發展,推動了對專業低溫儲存和配送基礎設施的需求成長。這些治療方法通常需要嚴格的溫度控制(有時低至-70 度C),因此需要先進的低溫運輸物流、冗餘的電力系統和嚴密監控的運輸網路。波士頓、舊金山和三角研究園區(RTP)等創新叢集正在增加對溫控倉儲和末端配送解決方案的投資,以滿足醫療機構和研究機構的需求。此外,處理敏感生物製藥的複雜性促使物流供應商採用即時追蹤、預測性風險管理和合規運營,從而導致整個藥品供應鏈的複雜性增加和成本結構變化。

工業地產空置率低

內陸帝國、達拉斯/沃斯堡、芝加哥和新澤西州北部等主要物流樞紐的低空置率限制了供應鏈的擴張。由於可用倉庫空間處於歷史低位,租戶面臨租金上漲、位置選擇有限以及獲取倉儲前置作業時間所需時間延長等問題。這種供需失衡在適合電子商務和自動化應用的現代化高層倉庫中尤其嚴重,這類倉庫仍供不應求。因此,租戶被迫選擇位置欠佳或老舊物業,導致運輸效率低下和營運成本增加。短期來看,這些限制因素會降低網路的擴充性,導致擴張計畫延誤,尤其對於快速成長的零售商和第三方物流(3PL) 供應商而言更是如此。

細分市場分析

到2025年,運輸服務將占美國零售物流市場佔有率的60.26% 。附加價值服務、套件組裝、逆向物流和貼標服務正以6.66%的複合年成長率成長,反映出零售商正向差異化履約轉型。整合的夥伴關係關係將運輸、倉儲和客製化服務整合在一起,減少了人工操作次數,提高了物流透明度。

倉儲業者正在其物流中心整合簡化的生產工作站、退貨中心和包裹級個人化客製化功能。品牌願意為這些功能支付溢價,因為諸如配送準確率和退貨處理速度等客戶體驗指標直接影響客戶忠誠度。這種轉變正在將倉庫從成本中心轉變為價值鏈中的價值創造樞紐。因此,能夠整合速度、客製化和數據視覺性的營運商正在B2B和D2C(直接面對消費者)市場中獲得競爭優勢。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 擴展全通路「線上購買,商店取貨」(BOPIS)網路

- 生物製藥主導了溫控藥物運輸的激增。

- 近岸外包和聯邦政府對「美國製造」產品的激勵措施正在促進國內庫存地點的增加。

- 即時貨物可視化平台的廣泛部署

- 零售訂閱/忠誠度計畫推動了定期配送量的成長

- 聯邦政府為零排放軌道走廊提供的資金(IIJA津貼)

- 市場限制因素

- 主要都會區工業地產的空置率處於歷史低點。

- 貨物竊盜案增多,保費飆升

- 雲端物流堆疊中的網路安全漏洞

- 鐵路和港口聯運樞紐長期面臨底盤短缺問題

- 價值供應鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

第5章 市場規模與成長預測

- 按服務類型

- 運輸

- 路

- 航空

- 鐵路

- 海

- 倉儲/物流

- 附加價值服務及其他服務(套件組裝、包裝、貼標)

- 運輸

- 溫度管理要求

- 低溫運輸

- 室溫(15-25 度C)

- 冷藏(2-8 度C)

- 冷凍(低於0°C)

- 非低溫運輸

- 低溫運輸

- 依產品類型

- 食品/飲料

- 服裝和鞋類

- 家用電器

- 醫療和藥品

- 家具和室內用品

- 其他

- 按地區(美國)

- 東北

- 中西部

- 東南

- 西南

- 西方

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- UPS

- FedEx

- DHL Group

- CH Robinson

- XPO Inc.

- GXO Logistics

- Ryder System

- JB Hunt

- Schneider National

- Lineage Logistics

- Americold

- Penske Logistics

- Kuehne+Nagel

- DSV

- GEODIS

- NFI Industries

- Xpress Global Systems(XGS)

- Kenco Logistics

- Marten Transport

- CMA CGM Group(CEVA Logistics)

第7章 市場機會與未來展望

According to Mordor Intelligence, the united states retail logistics market size was valued at USD 235.25 billion in 2025 and is estimated to grow from USD 244.76 billion in 2026 to reach USD 295.99 billion by 2031, at a CAGR of 3.87% during the forecast period (2026-2031).

Retailers have begun converting stores into fulfillment nodes, temperature-controlled networks are expanding to serve complex biologics pipelines, and federal green-corridor programs are accelerating the shift toward electric line-haul fleets. This report is Segmented by Service Type (Transportation, Warehousing & Distribution, and More), by Temperature-Control (Ambient, Chilled, Frozen, Non Cold Chain), by Product Type (Food and Beverages, Apparel and Footwear, Electronic Appliances, Healthcare & Pharmaceuticals, and More), and by Region (Northeast, Southeast, Southwest). The Market Forecasts are Provided in Terms of Value (USD).

United States Retail Logistics Market Trends and Insights

Omnichannel BOPIS (Buy-Online-Pick-Up-In-Store) Expansion

Buy-online-pick-up-in-store (BOPIS) continues to reshape suburban retail logistics by blending digital convenience with physical store networks. Retailers are increasingly redesigning store footprints to accommodate dedicated pickup zones, curbside lanes, and micro-fulfillment backrooms that enable rapid order staging. This model reduces last-mile delivery costs while increasing store traffic, as customers frequently make incremental purchases during pickup visits. The competitive pressure is intensifying as large chains invest in real-time inventory visibility and seamless app-based ordering, raising customer expectations for speed and reliability capabilities that smaller retailers often struggle to match. As suburban populations grow and e-commerce penetration deepens, BOPIS is becoming a default fulfillment option rather than a value-added service.

Biologics-Led Ultra-Cold Demand

The rapid growth of biologic drugs, cell and gene therapies, and mRNA-based treatments is driving demand for specialized ultra-cold storage and distribution infrastructure. These therapies often require strict temperature ranges, sometimes as low as -70°C, creating a need for advanced cold chain logistics, redundant power systems, and highly monitored transportation networks. Innovation clusters such as Boston, San Francisco, and Research Triangle Park (RTP) are seeing increased investment in temperature-controlled warehousing and last-mile delivery solutions tailored to healthcare providers and research institutions. The complexity of handling sensitive biologics is also pushing logistics providers to adopt real-time tracking, predictive risk management, and compliance-focused operations, elevating the overall sophistication and cost structure of pharmaceutical supply chains.

Industrial Real Estate Vacancy Lows

Persistently low vacancy rates across major logistics hubs such as the Inland Empire, Dallas-Fort Worth, Chicago, and Northern New Jersey are constraining supply chain expansion. With available warehouse space at historic lows, tenants face rising lease rates, limited location choice, and longer lead times for securing capacity. This imbalance is particularly acute for modern, high-clearance facilities suited for e-commerce and automation, which remain in short supply. As a result, occupiers are forced into suboptimal locations or older assets, increasing transportation inefficiencies and operating costs. In the short term, these constraints limit network scalability and delay expansion plans, especially for fast-growing retailers and third-party logistics providers.

Other drivers and restraints analyzed in the detailed report include:

- Near-shoring & "Made in USA" Incentives

- Real-Time Freight Visibility Platforms

- Rising Cargo Theft & Insurance Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Transportation services generated 60.26% of the 2025 United States retail logistics market share. Value-added offerings, kitting, reverse logistics, and labeling are increasing at 6.66% CAGR, reflecting retailers' shift toward differentiated fulfillment. Integrated partnerships now bundle transportation, warehousing, and customization, reducing hand-offs and improving visibility.

Warehouse operators embed light-manufacturing stations, returns centers, and package-level personalization inside distribution hubs. Brands pay premiums for these capabilities because customer experience metrics such as delivery accuracy and returns turnaround directly drive loyalty. This shift is transforming warehouses from cost centers into value-generating nodes within the supply chain. As a result, operators who can integrate speed, customization, and data visibility are gaining a competitive edge in both B2B and direct-to-consumer markets.

List of Companies Covered in this Report:

- UPS

- FedEx

- DHL Group

- C.H. Robinson

- XPO Inc.

- GXO Logistics

- Ryder System

- J.B. Hunt

- Schneider National

- Lineage Logistics

- Americold

- Penske Logistics

- Kuehne+Nagel

- DSV

- GEODIS

- NFI Industries

- Xpress Global Systems (XGS)

- Kenco Logistics

- Marten Transport

- CMA CGM Group (CEVA Logistics)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Omnichannel "Buy-Online-Pick-Up" (BOPIS) Network Expansion

- 4.2.2 Biologics-Led Surge in Temperature-Controlled Pharma Shipments

- 4.2.3 Near-Shoring and Federal "Made In USA" Incentives Boosting Domestic Inventory Nodes

- 4.2.4 Widespread Roll-Out of Real-Time Freight-Visibility Platforms

- 4.2.5 Retail Subscription/Loyalty Programs Driving Scheduled Delivery Volumes

- 4.2.6 Federal Funding for Zero-Emission Truck Corridors (IIJA Grants)

- 4.3 Market Restraints

- 4.3.1 Record-Low Industrial Real-Estate Vacancy in Core Metros

- 4.3.2 Escalating Cargo-Theft and Insurance Premiums

- 4.3.3 Cyber-Security Vulnerabilities in Cloud Logistics Stacks

- 4.3.4 Persistent Chassis Shortages at Rail and Port Intermodal Hubs

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Service Type

- 5.1.1 Transportation

- 5.1.1.1 Road

- 5.1.1.2 Air

- 5.1.1.3 Rail

- 5.1.1.4 Sea

- 5.1.2 Warehousing and Distribution

- 5.1.3 Value-Added Services and Others (Kitting, Packaging, Labeling)

- 5.1.1 Transportation

- 5.2 By Temperature-Control Requirement

- 5.2.1 Cold Chian

- 5.2.1.1 Ambient (15-25 °C)

- 5.2.1.2 Chilled (2-8 °C)

- 5.2.1.3 Frozen (Less than 0 °C)

- 5.2.2 Non Cold Chain

- 5.2.1 Cold Chian

- 5.3 By Product Type

- 5.3.1 Food and Beverages

- 5.3.2 Apparel and Footwear

- 5.3.3 Electronic Appliances

- 5.3.4 Healthcare and Pharmaceuticals

- 5.3.5 Furniture and Home Furnishings

- 5.3.6 Others

- 5.4 By Region (United States)

- 5.4.1 Northeast

- 5.4.2 Midwest

- 5.4.3 Southeast

- 5.4.4 Southwest

- 5.4.5 West

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 UPS

- 6.4.2 FedEx

- 6.4.3 DHL Group

- 6.4.4 C.H. Robinson

- 6.4.5 XPO Inc.

- 6.4.6 GXO Logistics

- 6.4.7 Ryder System

- 6.4.8 J.B. Hunt

- 6.4.9 Schneider National

- 6.4.10 Lineage Logistics

- 6.4.11 Americold

- 6.4.12 Penske Logistics

- 6.4.13 Kuehne+Nagel

- 6.4.14 DSV

- 6.4.15 GEODIS

- 6.4.16 NFI Industries

- 6.4.17 Xpress Global Systems (XGS)

- 6.4.18 Kenco Logistics

- 6.4.19 Marten Transport

- 6.4.20 CMA CGM Group (CEVA Logistics)