|

市場調查報告書

商品編碼

2062074

電動切割機:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)Power Cutter - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

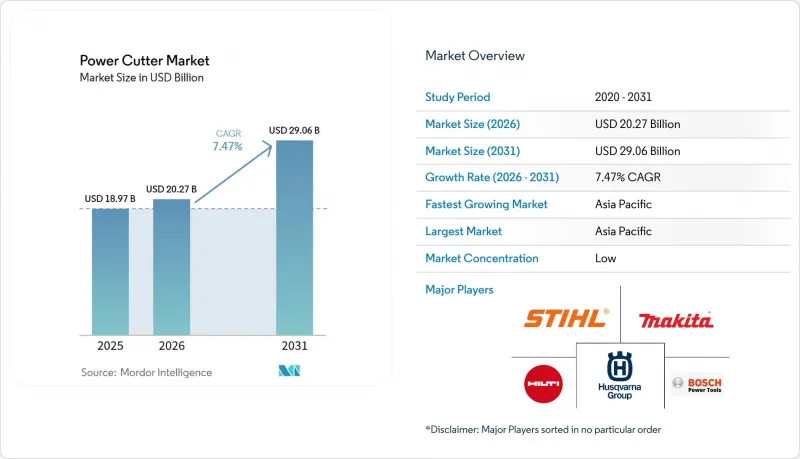

根據 Mordor Intelligence 預測,電動切割機市場規模預計將在 2025 年達到 189.7 億美元,2026 年達到 202.7 億美元,到 2031 年達到 290.6 億美元,2026 年至 2031 年的複合年成長率為 7.47%。

本報告按動力來源(汽油動力、有線電動等)、產品類型(手持式切割鋸、步行式切割機等)、刀片類型(鋒利刀片、鑽石刀片等)、終端用戶行業(建築拆除、汽車等)和地區(北美、亞太等)進行細分。市場預測以十億美元為單位。

全球電動切割機市場趨勢及洞察

擴大其在緊急救援和災害應變行動的應用

隨著複合材料和高抗張強度鋼在現代車輛中的應用日益廣泛,緊急服務機構正將具備連網功能的電動切割機納入其標準配備包。諸如Weber Rescue Systems的SMART-FORCE等平台提供的即時電池診斷、使用日誌和位置追蹤功能,能夠提升跨多個地點車隊的緊急應變能力和資產管理水平。其緊湊的外形和專用附件使其能夠在狹小空間內作業,例如在公共交通和多車事故現場進行快速切割。這些功能降低了現場工具運作的風險,並透過部署後的跨轄區互助簡化了救援行動。隨著零排放車輛的普及,救援人員需要具備可靠煞車和抑塵功能的無火花鑽石鋸片解決方案,這推動了電動切割機市場對高品質無線平台的需求。網路和電池管理功能也有助於各部門制定基於生命週期的更換計畫和培訓方案,從而加強採購計畫與實際營運需求的契合度。

房屋翻新和維修工程數量不斷增加。

由於住宅翻新和小規模商業改造的持續熱潮,能夠加工瓷磚、石材和輕金屬的可攜式切割機需求依然旺盛。住宅和小規模承包商使用連續刃鑽石鋸片進行瓷磚切割,使用分段式鋸片快速進行混凝土作業,從而縮短多材料專案中的鋸片更換時間。對於室內作業,由於必須遵守相關法規並顧及鄰居的感受,水刀和防塵罩等配件已成為標配。租賃服務使得即使是週末專案也能使用高階切割機,避免了購買成本過高的問題。同時,承包商正在為其切割機配備易於與集塵機和水清洗套件整合的功能,以便處理居住場所的灰塵和碎屑。這些趨勢,加上業主在資金籌措環境緊張的情況下優先考慮維修而非新建,共同支撐了電動切割機市場的廣泛用戶群。

安全隱憂和工人受傷風險

旋轉切割工具本身有反彈、刀片卡死和飛濺碎屑等風險,而且現場作業環境多變,這些風險會進一步加劇。製造商正透過引入強化刀片防護罩、電子煞車和智慧馬達控制系統等功能來應對這些問題,這些功能可在刀片卡死時自動切斷電源。隨著室內和封閉空間切割作業的增加,噴水系統和防塵罩也逐漸成為標準配置,用於控制二氧化矽的暴露。無線可攜式設備降低了在擁擠工作區域發生絆倒事故的風險,並簡化了安裝過程。由於監管和法律責任的壓力,電動切割機市場的買家越來越注重工具的整體整合安全功能,例如煞車時間和粉塵控制。配備多個感測器和煞車功能的型號日益普及,將有助於降低事故的嚴重性,並減少專業工作團隊的停機時間。

細分市場分析

到2025年,有線電動切割機將佔據47.1%的市場佔有率,這反映了在需要持續數小時切割作業的情況下,電池更換週期可能會中斷工作流程,而持續扭矩供應的重要性。這一市場佔有率與混凝土板切割、高層建築鋼筋切割以及固定加工站等對不間斷運作週期要求極高的場合相符。電池供電的手持式切割機預計將成長最快,到2031年複合年成長率將達到8.8%,這得益於平台規模的擴大、冷卻能力的提升以及充電技術的進步,其與有線切割機的性能差距正在縮小。各品牌都強調透過單一生態系統實現覆蓋範圍,使多個類別的設備能夠透過單一充電器和少量電池組進行維護,從而提高設備利用率並降低設備管理的複雜性。憑藉電子煞車和過載保護功能,無線切割機現在也滿足了以往固定安裝設備所需的安全標準。隨著承包商將電池投資擴展到數百種相容的工具類型,平台鎖定正成為電動切割機市場的策略因素。此外,採購還反映了對粉塵控制和振動減少的要求,這些要求在都市區和封閉迴路境中,當設計中沒有引擎排氣系統時,往往更容易實施。

與內建儲能裝置相比,有線切割機無需初始電池成本,重量也更輕,這在狹小空間和重複切割作業中尤其有利。汽油動力切割機在偏遠地區和災害救援中仍然發揮作用,尤其是在高功率連續作業的情況下,因為加油比充電更快,但在人口密集的城市,其使用受到排放氣體法規的限制。液壓系統在拆除和地下作業等扭矩密度至關重要的領域仍然佔據著一個特殊的細分市場,但軟管和輔助裝置限制了其移動性。隨著無線產品無需壓縮機設備和氣路維護,氣動解決方案正逐漸式微。隨著無線生態系統的成熟,電動切割機產業的業主希望產品能與防塵罩、供水系統和集塵機整合,以實現全面的合規性。買家正在比較整個系統的成本,而不僅僅是單一工具的價格,當生產力和安全性的提升超過初始投資時,高品質的無線解決方案將在電動切割機市場中廣泛應用。

區域分析

預計到2025年,亞太地區將佔全球銷售額的38.4%,並在資料中心建設、國家基礎設施項目和大規模交通走廊建設的推動下,以8.5%的複合年成長率成長至2031年。中國2021年的施工機械銷售和挖土機出貨量表明,混凝土、鋼筋和瀝青切割設備的需求將持續存在。印度的國家基礎建設項目總額達100兆盧比(約1.2兆美元),將推動高速公路和交通樞紐對切割設備的多年需求(約1.2兆美元)。從剪切機汗到沙賈漢布爾貝霍爾的區域快速交通系統(RRT)預計將於2026年8月開工建設,並於2031年11月竣工。預計這將使整個建設期間對接縫切割、溝槽切割和車站切割設備的需求保持穩定。東京、首爾、新加坡和香港的都市區排放氣體和噪音法規正在推動室內和夜間作業對電動切割設備的需求成長。韓國本土汽車製造商的投資,包括影響韓國產能的決策,將提高供應韌性並前置作業時間。

北美和歐洲合計約佔全球整體銷售額的一半,其特點是定價較高、培訓體系完善且合規性強。美國基礎設施資金籌措的透明度有助於承包商維持工具預算的穩定性,從而保障設備的運作和技術支援。歐洲關於排放氣體、二氧化矽粉塵和手部振動的法規不斷提高基本規格,促使整合切割機、集塵機和水清洗套件的整合系統更受青睞。 CE 標誌和 EN 標準推動了採購方對性能有據可查且材料可追溯性可靠的產品的偏好。德國等市場對手推車電鋸操作員的訓練資格進一步規範了工具的選擇和使用。隨著無線平台性能的不斷提升,室內和封閉式作業正在逐漸擺脫對汽油動力設備的依賴,因為無線平台無需專用通風系統即可滿足當地法規要求。

南美洲和中東及非洲地區對需求平衡做出了貢獻。巴西、智利和秘魯的採礦和採石業支撐了用於岩芯修整和岩石加工的重型切割機的訂單。波灣合作理事會(GCC)市場的大型建設項目正推動需求暫時性激增,具體情況取決於大型企劃的階段。在非洲,隨著某些經濟區的工業化進程推進,公路網建設和港口擴建正在推動市場逐步成長。外匯波動和標準應用的變化正在影響銷售管道策略,國際建築商通常會指定高階品牌以確保安全性和品質一致性。在全部區域,租賃發揮著至關重要的作用,因為建築商會根據專案進度和現金流量計劃調整工具的使用。動力切割機市場正受益於這種柔軟性,即使購買計劃被推遲,也能更容易獲得高階型號。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 擴大其在緊急救援和災害應變行動的應用

- 維修的數量不斷增加

- 道路建設和維護業務的擴張

- DIY和專業園林綠化服務的成長

- 人們越來越偏好無線和電池供電的型號。

- 採礦和採石業的擴張

- 市場限制因素

- 安全隱憂和工人受傷風險

- 頻繁更換刀片和耗材成本

- 建設活動的季節性需求波動

- 身體壓力與人體工學挑戰

- 價值供應鏈分析

- 監理情勢

- 技術展望

- 產業吸引力—五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間的競爭

- 刀片技術和兼容性生態系統

- 專業市場與消費者市場之間的市場兩極化

第5章 市場規模與成長預測

- 透過動力來源

- 氣體類型

- 有線電動

- 氣動型

- 油壓

- 電池供電(手持式)

- 依產品類型

- 手持式切割鋸

- 推式切割器

- 固定式切割機

- 按刀片類型

- 拋光刀片

- 鑽石刀片

- 硬質合金和複合材料刀片

- 按最終用戶行業分類

- 建設與拆除

- 一般製造業、金屬加工及製造

- 車

- 航太

- 其他(一般消費者、DIY愛好者、園藝師、地方政府等)

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 秘魯

- 其他南美國家

- 歐洲

- 英國

- 德國

- 法國

- 義大利

- 西班牙

- 比荷盧經濟聯盟(比利時、荷蘭、盧森堡)

- 北歐國家(丹麥、芬蘭、冰島、挪威、瑞典)

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 東協(印尼、泰國、菲律賓、馬來西亞、越南)

- 其他亞太國家

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 卡達

- 科威特

- 土耳其

- 埃及

- 南非

- 奈及利亞

- 其他中東和非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Husqvarna Group

- Stihl Holding AG & Co. KG

- Makita Corporation

- Hilti Corporation

- Bosch Power Tools(Robert Bosch GmbH)

- Milwaukee Tool(Techtronic Industries)

- DeWalt(Stanley Black & Decker)

- HiKoki(Koki Holdings)

- Norton Clipper(Saint-Gobain Abrasives)

- ICS Diamond Tools(Blount International)

- Evolution Power Tools

- Wacker Neuson SE

- Metabo HPT

- Festool(TTS Tooltechnic Systems)

- Chicago Pneumatic

- Einhell Germany AG

- Ryobi Tools(TTI)

- Positec Group(Worx)

- Tyrolit Group

- ECHO Incorporated

第7章 市場機會與未來展望

According to Mordor Intelligence, the power cutter market size is projected to be USD 18.97 billion in 2025, USD 20.27 billion in 2026, and reach USD 29.06 billion by 2031, growing at a CAGR of 7.47% from 2026 to 2031.

This report is Segmented by Power Source (Gas-Powered, Electric - Corded, and More), by Product Type (Handheld Cut-Off Saws, Walk-Behind Cutters, and More), by Blade Type (Abrasive Blades, Diamond Blades, and More), by End-User Industry (Construction & Demolition, Automotive, and More), and by Geography (North America, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value in USD Billion.

Global Power Cutter Market Trends and Insights

Rising Adoption in Emergency Rescue and Disaster Response Operations

Emergency services are integrating connected power cutters into their standard operating kits due to the rise of composite materials and high-strength steels in modern vehicles. Real-time battery diagnostics, usage logs, and location tracking in platforms like Weber Rescue Systems' SMART-FORCE improve readiness verification and asset control across multi-station fleets. Compact form factors and specialty attachments support confined-space operations, including rapid access cuts in mass transit and multi-vehicle incidents. These capabilities reduce the risk of on-scene tool downtime and streamline mutual-aid recoveries after cross-jurisdictional deployments. As zero-emissions vehicles proliferate, responders need non-sparking diamond-blade solutions with reliable braking and dust control, which strengthens the case for premium cordless platforms in the power cutter market. Connectivity and battery management also help departments plan life-cycle replacement and training, which tightens procurement alignment with operational demands.

Growing Renovation and Remodeling Activities

Sustained home renovation and light commercial remodeling keep demand high for portable cutters that can handle porcelain, tile, masonry, and light metal tasks. Homeowners and small contractors combine continuous-rim diamond blades for clean tile cuts with segmented blades for faster concrete work, which reduces changeover time on multi-material projects. Water-suppression and dust-shroud accessories have become standard choices for indoor tasks where compliance and neighbor comfort matter. Rental programs extend access to higher-end cutters for weekend projects where purchase does not pencil out. In parallel, contractors standardize on cutters that integrate easily with vacuums and water kits to manage dust and debris on occupied sites. This activity sustains a broad base of users in the power cutter market as property owners prioritize upgrades over new builds when financing conditions are tight.

Safety Hazards and Operator Injury Risks

Rotating-blade tools present inherent risks that include kickback, binding, and debris ejection, and job sites often operate under variable conditions that can amplify these hazards. Manufacturers have responded with enhanced blade guards, electronic brakes, and intelligent motor controls that cut power during binding events. As more cutting shifts are being performed indoors or into enclosed spaces, water-suppression systems and dust shrouds are also being standardized to manage silica exposure. Portable units without cords reduce trip hazards around crowded work areas and improve setup discipline. Buyers in the power cutter market increasingly assess tools by their integrated safety stack, from braking times to dust mitigation, due to regulatory and liability pressures. Wider adoption of sensor-rich and brake-equipped models can reduce incident severity and downtime on professional crews.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Road Construction and Maintenance Programs

- Growth in DIY and Professional Landscaping Services

- Frequent Blade Replacement and Consumable Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Electric corded models held 47.1% share in 2025, reflecting value in continuous torque delivery on multi-hour cutting tasks where battery-swap cycles could disrupt workflow. This position aligns with use on slab cuts, rebar sections on high-rise decks, and stationary fabrication stations where uninterrupted duty cycles are critical. Battery-powered handhelds show the fastest expansion at 8.8% CAGR through 2031 as platform-scale, cooling, and charging improvements narrow performance gaps with corded baselines. Brands emphasize single-ecosystem coverage so one charger and a few packs sustain multiple categories, which increases utilization and lowers fleet complexity. Electronic braking and overload protection features help cordless units meet safety expectations that once favored fixed installations. Platform lock-in has become a strategic factor in the power cutter market as contractors extend battery investments across hundreds of compatible tools. Procurement also reflects dust-control and vibration demands that are often easier to implement on designs without engine emissions systems in urban or enclosed environments.

Corded units eliminate upfront battery costs and reduce weight relative to onboard energy storage, which helps in tight spaces and repetitive cutting sequences. Gas-powered cutters still serve remote and disaster-response roles where refueling remains faster than charging, especially on sustained high-output cycles, although emissions policies in dense cities limit their use. Hydraulic systems continue to occupy a specialized niche for demolition and subsurface utility work where torque density is paramount, though hoses and auxiliary packs limit mobility. Pneumatic solutions are retreating as cordless options remove compressor infrastructure and airline maintenance. As cordless ecosystems mature, owners in the power cutter industry expect better integration with dust shrouds, water systems, and vacuums to deliver holistic compliance. Buyers weigh all-in system costs, not just tool-only price, which supports broader adoption of premium cordless solutions in the power cutter market when productivity gains and safety features offset initial investment.

Geography Analysis

Asia-Pacific accounted for 38.4% of 2025 revenue and is projected to grow at 8.5% CAGR through 2031, anchored by data-center construction, national infrastructure programs, and large transit corridors. China's 2021 construction-equipment sales and excavator volumes signal sustained complementary demand for cutters across concrete, rebar, and asphalt use cases. India's National Infrastructure Pipeline totals INR 100 trillion (USD 1.2 trillion), reinforcing multi-year demand for cutting equipment across highways and transit centers (USD 1.2 trillion). The Regional Rapid Transport System segment from Sarai Kale Khan to Shahjahanpur-Behror kicks off in August 2026 and is expected to be completed by November 2031, which implies sustained needs for joint, trench, and station cuts over the timeline. Urban emissions and noise policies in Tokyo, Seoul, Singapore, and Hong Kong steer buyers toward electric options for indoor and nighttime work. Localized OEM investments, including capacity decisions affecting South Korea, improve supply resilience and lead times.

North America and Europe together hold roughly the remaining half of global revenue, with premium pricing, codified training, and advanced compliance ecosystems. Funding visibility for United States infrastructure contributes to stable tool budgets among contractors that prioritize uptime and support. European regulations on emissions, silica dust, and hand-arm vibration continue to lift baseline specifications, which support integrated systems that combine cutters, vacuums, and water kits. CE marking and EN standards reinforce procurement preferences for documented performance and traceable materials. Training credentials for walk-behind saw operators in markets like Germany further formalize tool selection and usage. As cordless platforms improve, indoor and enclosed-space tasks shift away from gas equipment to meet local rules without specialized ventilation.

South America and the Middle East & Africa contribute to the balance of demand. Mining and quarrying across Brazil, Chile, and Peru sustain orders for heavy-duty cutters used in core trimming and rock processing. Large-scale construction in Gulf Cooperation Council markets produces episodic surges tied to mega-project phases. In Africa, road connectivity and port expansions add incremental growth as industrialization advances in select economies. Currency volatility and uneven enforcement of standards influence channel strategies, with international contractors often specifying premium brands for safety and quality consistency. Across these regions, rental plays an important role as contractors align tool access with project schedules and cash-flow planning. The power cutter market benefits from this flexibility, which expands access to premium platforms where outright purchase is deferred.

- Husqvarna Group

- Stihl Holding AG & Co. KG

- Makita Corporation

- Hilti Corporation

- Bosch Power Tools (Robert Bosch GmbH)

- Milwaukee Tool (Techtronic Industries)

- DeWalt (Stanley Black & Decker)

- HiKoki (Koki Holdings)

- Norton Clipper (Saint-Gobain Abrasives)

- ICS Diamond Tools (Blount International)

- Evolution Power Tools

- Wacker Neuson SE

- Metabo HPT

- Festool (TTS Tooltechnic Systems)

- Chicago Pneumatic

- Einhell Germany AG

- Ryobi Tools (TTI)

- Positec Group (Worx)

- Tyrolit Group

- ECHO Incorporated

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Adoption in Emergency Rescue and Disaster Response Operations

- 4.2.2 Growing Renovation and Remodeling Activities

- 4.2.3 Expansion of Road Construction and Maintenance Programs

- 4.2.4 Growth in DIY and Professional Landscaping Services

- 4.2.5 Increasing Preference for Cordless and Battery-Powered Models

- 4.2.6 Mining and Quarrying Industry Expansion

- 4.3 Market Restraints

- 4.3.1 Safety Hazards and Operator Injury Risks

- 4.3.2 Frequent Blade Replacement and Consumable Costs

- 4.3.3 Seasonal Demand Fluctuations in Construction Activity

- 4.3.4 Physical Strain and Ergonomic Challenges

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Industry Attractiveness - Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Blade Technology and Compatibility Ecosystem

- 4.9 Professional vs. Consumer Grade Market Bifurcation

5 Market Size & Growth Forecasts (Value, In USD Billion)

- 5.1 By Power Source

- 5.1.1 Gas-powered

- 5.1.2 Electric - Corded

- 5.1.3 Pneumatic

- 5.1.4 Hydraulic

- 5.1.5 Battery-powered (hand-held)

- 5.2 By Product Type

- 5.2.1 Handheld Cut-off Saws

- 5.2.2 Walk-behind Cutters

- 5.2.3 Stationary Cut-off Machines

- 5.3 By Blade Type

- 5.3.1 Abrasive Blades

- 5.3.2 Diamond Blades

- 5.3.3 Carbide & Multi-material Blades

- 5.4 By End-user Industry

- 5.4.1 Construction & Demolition

- 5.4.2 General Manufacturing, Metalworking & Fabrication

- 5.4.3 Automotive

- 5.4.4 Aerospace

- 5.4.5 Others (Consumer, DIY, Landscaping, Municipal, etc.)

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Peru

- 5.5.2.4 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 BENELUX (Belgium, Netherlands, and Luxembourg)

- 5.5.3.7 NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- 5.5.3.8 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 Australia

- 5.5.4.5 South Korea

- 5.5.4.6 ASEAN (Indonesia, Thailand, Philippines, Malaysia, Vietnam)

- 5.5.4.7 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Qatar

- 5.5.5.4 Kuwait

- 5.5.5.5 Turkey

- 5.5.5.6 Egypt

- 5.5.5.7 South Africa

- 5.5.5.8 Nigeria

- 5.5.5.9 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Husqvarna Group

- 6.4.2 Stihl Holding AG & Co. KG

- 6.4.3 Makita Corporation

- 6.4.4 Hilti Corporation

- 6.4.5 Bosch Power Tools (Robert Bosch GmbH)

- 6.4.6 Milwaukee Tool (Techtronic Industries)

- 6.4.7 DeWalt (Stanley Black & Decker)

- 6.4.8 HiKoki (Koki Holdings)

- 6.4.9 Norton Clipper (Saint-Gobain Abrasives)

- 6.4.10 ICS Diamond Tools (Blount International)

- 6.4.11 Evolution Power Tools

- 6.4.12 Wacker Neuson SE

- 6.4.13 Metabo HPT

- 6.4.14 Festool (TTS Tooltechnic Systems)

- 6.4.15 Chicago Pneumatic

- 6.4.16 Einhell Germany AG

- 6.4.17 Ryobi Tools (TTI)

- 6.4.18 Positec Group (Worx)

- 6.4.19 Tyrolit Group

- 6.4.20 ECHO Incorporated

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment

電動割草機市場-2026-2032年全球市場預測割草機市場-2026-2032年全球市場預測

電動割草機市場-2026-2032年全球市場預測割草機市場-2026-2032年全球市場預測 手推式割草機:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年)

手推式割草機:市場佔有率分析、行業趨勢和統計數據以及成長預測(2026-2031 年) 自動割草機市場 - 全球產業規模、佔有率、趨勢、機會、預測:按產品類型、技術、燃料類型、應用、地區和競爭格局分類,2021-2031年

自動割草機市場 - 全球產業規模、佔有率、趨勢、機會、預測:按產品類型、技術、燃料類型、應用、地區和競爭格局分類,2021-2031年 無線園藝設備市場機會、成長要素、產業趨勢分析及2026-2035年預測

無線園藝設備市場機會、成長要素、產業趨勢分析及2026-2035年預測 割草機市場:依最終用戶產業、產品類型、驅動系統、預期用途、動力來源和地區分類

割草機市場:依最終用戶產業、產品類型、驅動系統、預期用途、動力來源和地區分類 無線割草機市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測割草機市場:產品類型、動力系統、銷售管道、應用、最終用途 - 2026-2032年全球市場預測商用割草機市場:2026-2032年全球市場預測(按產品類型、動力來源、引擎類型、刀片類型、最終用戶和通路分類)割草機市場:依產品類型、動力來源、銷售管道和最終用戶分類,全球預測,2026-2032年

無線割草機市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測割草機市場:產品類型、動力系統、銷售管道、應用、最終用途 - 2026-2032年全球市場預測商用割草機市場:2026-2032年全球市場預測(按產品類型、動力來源、引擎類型、刀片類型、最終用戶和通路分類)割草機市場:依產品類型、動力來源、銷售管道和最終用戶分類,全球預測,2026-2032年