|

市場調查報告書

商品編碼

2038370

無線園藝設備市場機會、成長要素、產業趨勢分析及2026-2035年預測Cordless Garden Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

預計到 2025 年,全球無線園藝設備市場價值將達到 119 億美元,並預計以 8.7% 的複合年成長率成長,到 2035 年達到 276 億美元。

日益增強的環保意識和更嚴格的排放標準正促使消費者以更清潔的替代品取代傳統的燃油工具。電池效能的提升,包括更高的效率、更快的充電速度和更長的使用壽命,進一步加速了清潔工具的普及。與傳統產品相比,無線園藝設備因其便攜性、易用性和低維護成本而日益受到歡迎。住宅維修活動的增加以及人們對戶外空間美觀性的日益關注也推動了市場成長。消費者擴大投資於園藝和景觀美化,將其視為提升生活品質和關注健康的一部分。製造商也積極回應,拓展產品線,推出符合不斷變化的永續發展期望和監管要求的節能高效解決方案。

| 市場範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 上市時的市場規模 | 119億美元 |

| 預測金額 | 276億美元 |

| 複合年成長率 | 8.7% |

無線園藝設備市場也受惠於消費者對便利、低噪音戶外維護工具日益成長的偏好。電池供電解決方案因其運作效率高、環境影響小而正在取代傳統系統。能源儲存系統的技術進步延長了使用時間,提高了產品性能,進一步增強了市場滲透率。此外,旨在減少碳排放的監管措施也促進了無線產品在住宅和商業領域的應用。

預計到2025年,割草機市場規模將達到47億美元,並在2035年之前以9.4%的複合年成長率成長。由於割草機在私人住宅和商業場所的日常草坪養護中發揮著至關重要的作用,該市場一直保持著主導地位。與傳統的燃油動力設備相比,無線割草機因其運作安靜、操控靈活和易於使用等優點而越來越受歡迎。

預計到2025年,住宅市場將佔據76.4%的市場佔有率,並在2026年至2035年間以7%的複合年成長率成長。家庭園藝和草坪護理活動的日益普及推動了這一市場主導地位。由於便利、低噪音和運作優點,無線家電仍然是住宅的首選,使其成為家庭使用的理想之選。

美國無線園藝設備市場預計到2025年將達到41億美元,並在2035年之前以8%的複合年成長率成長。推動美國市場擴張的主要因素是郊區居住的日益普及,個人草坪護理在郊區十分普遍。電池驅動的割草機、修剪機、吹風機和樹籬修剪機因其易用性和低噪音而備受青睞。消費者越來越重視電池續航力長、充電速度快以及同一電池系統下多種工具的兼容性。

目錄

第1章:調查方法和範圍

第2章執行摘要

第3章業界考察

- 生態系分析

- 供應商情況

- 利潤率

- 每個階段增加的價值

- 影響價值鏈的因素

- 影響產業的因素

- 促進因素

- 擴大電池驅動和環保園藝工具的使用

- 家庭園藝和景觀美化活動越來越受歡迎。

- 拓展住宅景觀美化及物業管理服務

- 挑戰與挑戰

- 與有線或燃氣動力電器相比,其初始成本較高。

- 電池壽命有限,需要充電。

- 機會

- 智慧和物聯網園藝設備的整合

- 都市區對永續、靜音的戶外工具的需求不斷成長。

- 促進因素

- 成長潛力分析

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 監理情勢

- 標準和合規要求

- 區域法規結構

- 認證標準

- 波特五力分析

- PESTEL 分析

- 價格分析(基於初步調查)

- 對過去價格趨勢的分析(基於初步研究)

- 根據業務類型分類的定價策略(高階/價值/成本加成)(基於初步調查)

- 價格比較:電池供電式電器與瓦斯供電電器

- 電池成本對設備總價的影響

- 區域價格波動及其影響因素

- 貿易資料分析(HS編碼:8467.21)(基於初步調查)

- 進出口量和進口額趨勢(基於付費資料庫)

- 主要貿易路線及關稅的影響(基於付費資料庫)

- 主要出口國及進口國

- 貿易政策對市場動態的影響

- 生產能力和生產趨勢(基於初步調查)

- 按地區和主要生產商分類的設備產能(基於初步調查)

- 運轉率和擴張計劃(基於初步調查)

第4章 競爭情勢

- 介紹

- 企業市佔率分析

- 按地區

- 企業矩陣分析

- 主要市場公司的競爭分析

- 競爭定位矩陣

- 主要進展

- 併購

- 夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 市場估算與預測:依產品類型分類,2022-2035年

- 割草機

- 鏈鋸

- 綠籬修剪機

- 吹葉機

- 割草機

- 其他工具

第6章 市場估價與預測:依電池類型分類,2022-2035年

- 鋰離子電池(Li-ion)

- 鎳鎘(NiCd)

- 其他

第7章 市場估計與預測:依價格分類,2022-2035年

- 低的

- 中等的

- 高的

第8章 市場估計與預測:依應用領域分類,2022-2035年

- 住宅

- 商業的

第9章 市場估價與預測:依通路分類,2022-2035年

- 線上

- 離線

第10章 市場估價與預測:依地區分類,2022-2035年

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 亞太地區

- 中國

- 印度

- 日本

- 韓國

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中東和非洲(MEA)

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 南非

第11章:公司簡介

- AL-KO

- Bosch

- EGO Power+

- Einhell

- Greenworks

- Honda

- Husqvarna

- John Deere

- Karcher

- Makita

- Positec Tool Corporation

- Stanley Black & Decker

- STIHL

- Techtronic Industries(TTI)

- Toro

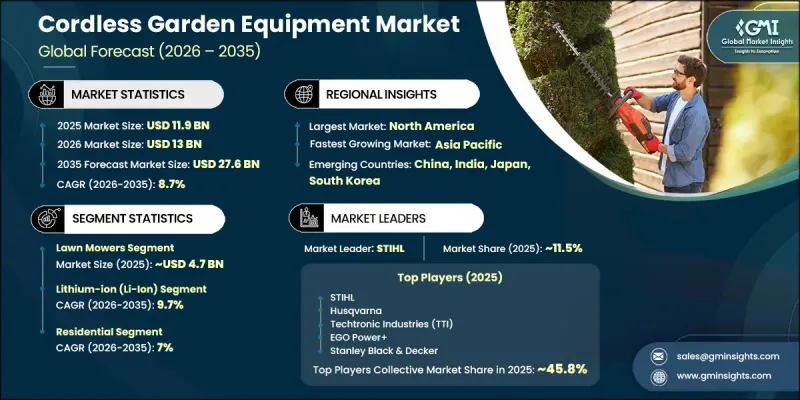

The Global Cordless Garden Equipment Market was valued at USD 11.9 billion in 2025 and is estimated to grow at a CAGR of 8.7% to reach USD 27.6 billion by 2035.

Rising environmental awareness and tightening emission standards are encouraging consumers to replace traditional fuel-powered tools with cleaner alternatives. Improvements in battery performance, including higher efficiency, faster charging capabilities, and longer operational life, are further accelerating adoption. Cordless garden equipment is gaining popularity due to its portability, ease of operation, and lower maintenance requirements compared to conventional alternatives. Expanding home improvement activities and increased interest in outdoor aesthetics are also contributing to market growth. Consumers are increasingly investing in gardening and landscaping as part of lifestyle enhancement and wellness-focused living. Manufacturers are responding by expanding product portfolios with energy-efficient, high-performance solutions aligned with evolving sustainability expectations and regulatory requirements.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $11.9 Billion |

| Forecast Value | $27.6 Billion |

| CAGR | 8.7% |

The cordless garden equipment market is also benefiting from growing consumer preference for convenient and low-noise outdoor maintenance tools. Battery-powered solutions are increasingly replacing conventional systems due to their operational efficiency and reduced environmental impact. Technological advancements in energy storage systems are enabling longer usage durations and improved product performance, further strengthening market penetration. In addition, regulatory initiatives aimed at reducing carbon emissions are encouraging wider adoption of cordless alternatives across residential and commercial applications.

The lawn mowers segment accounted for USD 4.7 billion in 2025 and is expected to grow at a CAGR of 9.4% through 2035. This segment maintains a dominant position due to its essential role in regular lawn maintenance across both private and commercial spaces. Cordless variants are increasingly preferred for their quiet operation, mobility, and ease of use compared to traditional fuel-based equipment.

The residential segment held a 76.4% share in 2025 and is projected to grow at a CAGR of 7% from 2026 to 2035. This dominance is supported by rising participation in home gardening and lawn care activities. Homeowners continue to favor cordless equipment due to its convenience, low noise levels, and environmentally friendly operation, making it highly suitable for household use.

United States Cordless Garden Equipment Market reached USD 4.1 billion in 2025 and is expected to grow at a CAGR of 8% through 2035. Market expansion in the country is supported by widespread suburban living, where private lawn maintenance is common. Strong demand is observed for battery-operated lawn mowers, trimmers, blowers, and hedge cutters due to their ease of use and reduced noise output. Consumers increasingly prioritize long battery life, fast charging performance, and compatibility across multiple tools powered by unified battery systems.

Key companies operating in the Global Cordless Garden Equipment Market include Husqvarna, Stanley Black & Decker, Bosch, STIHL, John Deere, Makita, Techtronic Industries (TTI), Greenworks, Honda, Toro, EGO Power+, Einhell, AL-KO, Karcher, and Positec Tool Corporation. Companies in the Cordless Garden Equipment Market are focusing on technological innovation, product diversification, and sustainability-driven strategies to strengthen their market position. They are investing in advanced battery systems to improve runtime, charging speed, and overall efficiency. Many manufacturers are expanding their cordless product portfolios to cover a wider range of gardening applications, enhancing consumer convenience. Strategic partnerships and distribution expansion, particularly through online and retail channels, are helping companies reach broader customer bases. Firms emphasize compatibility across tool platforms to create ecosystem-based product offerings. Additionally, continuous research and development efforts aimed at improving performance, durability, and environmental compliance are enabling companies to maintain strong competitive positioning in the evolving market landscape.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product Type

- 2.2.3 Battery Type

- 2.2.4 Price

- 2.2.5 End Use

- 2.2.6 Distribution channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising adoption of battery-powered and eco-friendly garden tools

- 3.2.1.2 Growing popularity of home gardening and landscaping activities

- 3.2.1.3 Expansion of residential landscaping and property maintenance services

- 3.2.2 Pitfalls & Challenges

- 3.2.2.1 Higher upfront cost compared to corded or gas-powered equipment

- 3.2.2.2 Limited battery life and charging requirements

- 3.2.3 Opportunities

- 3.2.3.1 Integration of smart and IoT-enabled garden equipment

- 3.2.3.2 Rising trend of sustainable and noise-free outdoor tools in urban areas

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Regulatory landscape

- 3.6.1 Standards and compliance requirements

- 3.6.2 Regional regulatory frameworks

- 3.6.3 Certification standards

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Pricing analysis (driven by primary research)

- 3.9.1 Historical price trend analysis (driven by primary research)

- 3.9.2 Pricing strategy by player type (premium / value / cost-plus) (driven by primary research)

- 3.9.3 Price comparison: battery vs gas-powered equipment

- 3.9.4 Impact of battery cost on overall equipment pricing

- 3.9.5 Regional price variations & drivers

- 3.10 Trade data analysis (HS Code- 8467.21) (driven by primary research)

- 3.10.1 Import/export volume & value trends (driven by paid data base)

- 3.10.2 Key trade corridors & tariff impact (driven by paid data base)

- 3.10.3 Major exporting & importing countries

- 3.10.4 Trade policy impact on market dynamics

- 3.11 Capacity & production landscape (driven by primary research)

- 3.11.1 Installed capacity by region & key producer (driven by primary research)

- 3.11.2 Capacity utilization rates & expansion pipelines (driven by primary research)

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Product Type, 2022 - 2035, (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Lawn mowers

- 5.3 Chainsaws

- 5.4 Hedge trimmers

- 5.5 Leaf blowers

- 5.6 Grass trimmers

- 5.7 Other tools

Chapter 6 Market Estimates & Forecast, By Battery Type, 2022 - 2035, (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Lithium-Ion (Li-Ion)

- 6.3 Nickel-Cadmium (NiCd)

- 6.4 Others

Chapter 7 Market Estimates & Forecast, By Price, 2022 - 2035, (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Low

- 7.3 Medium

- 7.4 High

Chapter 8 Market Estimates & Forecast, By End Use, 2022 - 2035, (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Residential

- 8.3 Commercial

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Online

- 9.3 Offline

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035, (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 Saudi Arabia

- 10.6.2 UAE

- 10.6.3 South Africa

Chapter 11 Company Profiles

- 11.1 AL-KO

- 11.2 Bosch

- 11.3 EGO Power+

- 11.4 Einhell

- 11.5 Greenworks

- 11.6 Honda

- 11.7 Husqvarna

- 11.8 John Deere

- 11.9 Karcher

- 11.10 Makita

- 11.11 Positec Tool Corporation

- 11.12 Stanley Black & Decker

- 11.13 STIHL

- 11.14 Techtronic Industries (TTI)

- 11.15 Toro

自動割草機市場 - 全球產業規模、佔有率、趨勢、機會、預測:按產品類型、技術、燃料類型、應用、地區和競爭格局分類,2021-2031年

自動割草機市場 - 全球產業規模、佔有率、趨勢、機會、預測:按產品類型、技術、燃料類型、應用、地區和競爭格局分類,2021-2031年 電動切割機:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)

電動切割機:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年) 割草機市場:依最終用戶產業、產品類型、驅動系統、預期用途、動力來源和地區分類

割草機市場:依最終用戶產業、產品類型、驅動系統、預期用途、動力來源和地區分類 無線割草機市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測

無線割草機市場規模、佔有率、成長及全球產業分析:按類型、應用和地區分類的洞察,2026-2034 年預測 割草機市場:產品類型、動力系統、銷售管道、應用、最終用途 - 2026-2032年全球市場預測商用割草機市場:2026-2032年全球市場預測(按產品類型、動力來源、引擎類型、刀片類型、最終用戶和通路分類)割草機市場:依產品類型、動力來源、銷售管道和最終用戶分類,全球預測,2026-2032年有線電動割草機市場:依產品類型、功率等級、馬達類型、應用、通路分類,全球預測(2026-2032)

割草機市場:產品類型、動力系統、銷售管道、應用、最終用途 - 2026-2032年全球市場預測商用割草機市場:2026-2032年全球市場預測(按產品類型、動力來源、引擎類型、刀片類型、最終用戶和通路分類)割草機市場:依產品類型、動力來源、銷售管道和最終用戶分類,全球預測,2026-2032年有線電動割草機市場:依產品類型、功率等級、馬達類型、應用、通路分類,全球預測(2026-2032) 手推式割草機市場規模、佔有率和成長分析:按產品類型、動力來源、切割寬度、應用、最終用戶、分銷管道、地區和行業預測,2026-2033 年。

手推式割草機市場規模、佔有率和成長分析:按產品類型、動力來源、切割寬度、應用、最終用戶、分銷管道、地區和行業預測,2026-2033 年。 氣墊式割草機市場規模、佔有率和成長分析:按產品類型、刀片/切割系統、應用、最終用戶、分銷管道和地區分類-2026-2033年產業預測

氣墊式割草機市場規模、佔有率和成長分析:按產品類型、刀片/切割系統、應用、最終用戶、分銷管道和地區分類-2026-2033年產業預測