|

市場調查報告書

商品編碼

2062070

聚丙烯不織布:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Polypropylene Non-woven Fabric - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

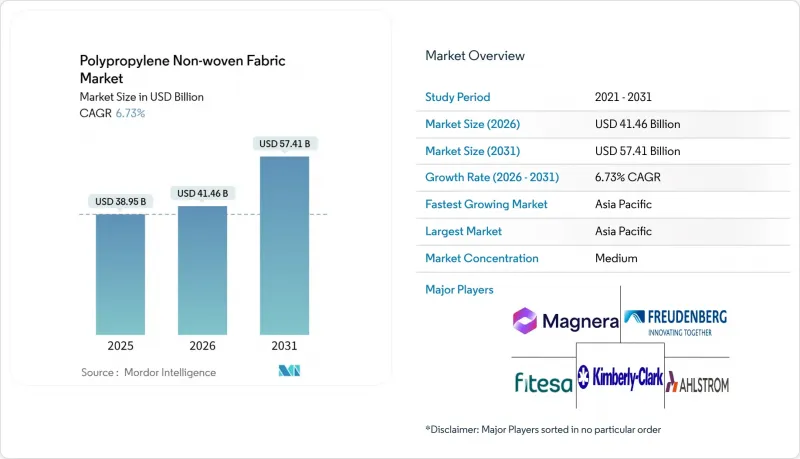

根據 Mordor Intelligence 預測,聚丙烯不織布市場規模將從 2025 年的 389.5 億美元成長到 2026 年的 414.6 億美元,到 2031 年將達到 574.1 億美元,2026 年至 2031 年的複合年成長率為 6.73%。

本報告按製造技術(紡粘、熔噴、SMS(熔噴-熔噴-紡絲)等)、應用領域(衛生、醫療、包裝、汽車、過濾及其他應用)、原料類型(均聚物和共聚物)以及地區(亞太、北美、歐洲、南美、中東和非洲)進行細分。市場預測以美元計價。

全球聚丙烯不織布市場趨勢與洞察

對一次性衛生和醫療產品的需求不斷成長

在新興經濟體,尿布、女性用衛生用品和失禁用品的廣泛使用,以及醫院系統建立的一次性感染控制規程,持續推動衛生和醫用一次性產品的銷售量成長。聚丙烯紡粘面層具有疏水錶面,滲透速度約1868毫米/秒,與纖維素基替代品相比,可縮短液體滲透時間。金佰利公司宣布的2025年在美國的多基地生產計劃,凸顯了品牌所有者的信心,並增加了國內卷材的採購量。由於SMS和SMMS複合材料的防護等級高於AAMI標準,且Tyvek無菌包裝產能的提升能夠滿足一次性醫療設備的激增需求,醫療產業的需求已超過衛生產業。產業評估指出,罩衣的阻隔性能標準與實際環境中病原體的存活率之間存在差距,這加速了人們對檢驗的抗菌聚丙烯基材的興趣。這些趨勢共同推動了聚丙烯不織布市場的潛在消費成長。

在包裝產業中不斷擴展的應用

為了符合歐洲2030年的回收目標,品牌所有者正轉向單一材料結構,這推動了軟包裝規格向高純度、單一製造地的聚丙烯不織布。北歐化工計畫於2026年擴大其「Borstar Nextension」等級產品的產能,旨在滿足這一合規性主導的需求,為食品接觸和醫療保健包裝袋提供密封性更佳、機械可回收性更高的產品。在物流領域,透氣性紡粘袋正被用作聚乙烯薄膜的替代品,因為它們可以減少運輸過程中冷凝造成的損壞,同時保持品牌印刷的可印刷性。包裝法規中納入的重複使用和空間限制可能會抑制某些一次性產品的需求,但同時,它們也催生了對符合重複使用標準的耐用不織布袋系統的需求。食品級再生聚丙烯的短期供應仍然緊張,其高價持續,進一步擴大了聚丙烯不織布市場中原生熔噴和紡粘捲材產品之間的價格差距。

針對一次性塑膠的環境和監管壓力

歐盟的《包裝和包裝廢棄物法規》將於2026年8月生效,該法規規定所有包裝到2030年必須達到至少C級可回收標準,到2038年必須達到A級或B級可回收標準,並且再生材料含量的配額將逐年增加。根據“生產者延伸責任制”,難以回收的複合材料將被徵收費用,這將直接影響低紙張重量通用紡粘購物袋和一次性餐具。歐盟於2025年9月發布的另一份草案規定,年處理超過1500噸顆粒的設施必須提交風險緩解計畫認證,違規者可能面臨高達其歐盟銷售額3%的罰款。北美各州也通過了類似的法律,禁止使用塑膠袋並強制要求使用再生材料,加強了相關法規的監管。雖然工業、汽車和地工織物不織布在很大程度上不會受到影響,但消費品包裝行業的加工商需要加快其可回收設計工作,以維持在聚丙烯不織布市場的市場進入。

細分市場分析

到2025年,紡粘聚丙烯不織布布市場將保持55%的市場佔有率,這得益於其高生產速度和低單位成本,使其適用於尿布、包袋和地工織物。儘管紡粘級聚丙烯不織布市場在基準年規模超過210億美元,但隨著市場日益飽和,其預期複合年成長率落後於其他細分技術。熔噴非織造布預計將以6.87%的年成長率成長,這主要得益於對N95口罩、暖通空調(HVAC)設備和電池電極隔膜等產品的更嚴格監管,這些產品需要直徑小於3微米的纖維。複合SMS和SMMS結構結合了紡粘的強度和熔噴的過濾性能,滿足了醫院罩衣和工業過濾領域的需求。在北美、土耳其和中國對Reicofil 5及同等生產線的投資顯示資本配置正在轉變。熱風耦合和壓延耦合交替的混合生產線將紙張重量範圍擴大到 10-200 g/m2,從而能夠進入汽車和屋頂材料市場。

政策勢頭進一步增強了技術發展的動力。美國能源局的暖通空調(HVAC)藍圖旨在2035年將商業建築的能耗降低50%,這將提振對高效熔噴材料的需求。同時,中國2026年室內空氣品質標準將PM2.5濃度限制在35µg/m3以內,刺激了對汽車和住宅過濾器的需求。 2020年至2021年的供應緊張凸顯了國內熔噴材料產能的必要性,也證明了印度、印尼和巴西等國政府獎勵措施的合理性。訂單供應商報告稱,訂單儲備已排至2028年,這支撐了聚丙烯不織布市場強勁的累積訂單。

區域分析

預計到2025年,亞太地區將佔全球需求的42.67%,並在2031年之前以6.91%的複合年成長率成長,這主要得益於中國和印度即將運作的超過3500萬噸的聚丙烯一體化生產能力。信實工業位於賈姆訥格爾的工廠計劃於2030年運作,年產能為520萬噸,僅該工廠每年就能供應超過100億平方公尺的紡粘不織布,這表明該地區正在推行進口替代戰略,以提高其自給自足能力。同樣,福建艾佛森在中國的計畫以及印尼圖班綜合體的建設也將加強亞洲內部的樹脂供應鏈,降低運輸成本和碳排放。加工商正利用這一優勢,透過在終端市場附近增設萊科菲爾和歐瑞康的生產線,縮短前置作業時間,並建立符合當地規格的紙張重量產品組合。

北美聚丙烯不織布市場正受惠於原始設備製造商(OEM)將生產基地遷回北美。金佰利公司斥資20億美元的跨州項目以及Avgol公司在北卡羅來納州部署Reicofil 5生產線,均增強了供應韌性,並降低了對亞洲進口的過度依賴。阿爾斯特龍公司計劃於2026年第四季對其位於伊利諾州的濾材進行升級改造,以滿足暖通空調(HVAC)和電動車(EV)過濾器日益成長的需求,並凸顯了市場結構向確保國內原料供應的轉變。樹脂價格上漲仍然是一個不利因素,但國內物流成本的降低和關稅規避在一定程度上抵消了原料成本的上漲。

在歐洲,需求不斷成長,這主要歸功於相關法規的推進,這些法規要求使用可回收解決方案。北歐化工(Borealis)2026年在布格豪森的投資恰逢塑膠包裝法規(PPWR)的最後期限,並將提供一種新型聚丙烯,為單一材料包裝袋和可消毒醫用包裝材料開拓市場。德國2024年聚丙烯進口量達90.3萬噸,顯示其對歐盟和中東地區原料的依賴程度較高。碳邊境調節機制(CBAM)的調整可能會進一步促使供應來源轉向低碳供應商。南美、中東和非洲仍然是新興市場,巴西的保護性種植補貼以及土耳其兩個年產能達100萬噸的聚丙烯生產項目,正在擴大該地區聚丙烯織物在作物保護和建築領域的應用。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 對一次性衛生和醫療產品的需求不斷成長

- 在包裝產業中不斷擴大應用

- 輕質且經濟實惠的材料的經濟性

- 在農業領域擴大應用

- 用於可重複使用個人防護裝備的抗菌聚丙烯不織布

- 市場限制因素

- 針對一次性塑膠的環境和監管壓力

- 聚丙烯價格波動與原油價格相關

- 歐盟碳排放邊境調節機制推高了進口成本。

- 價值鏈分析

- 監理情勢

- 波特五力模型

第5章 市場規模與成長預測

- 透過生產技術

- 紡粘

- 熔噴

- SMS(跨度融化跨度)

- SMMS(Spun-Melt-Melt-Spun)

- 其他生產技術

- 透過使用

- 衛生

- 醫學領域

- 包裝

- 車

- 過濾

- 農業

- 其他用途

- 依原料類型

- 均聚物

- 共聚物

- 按地區

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 東南亞國協

- 其他亞太國家

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 俄羅斯

- 北歐國家

- 其他歐洲國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 其他中東和非洲國家

- 亞太地區

第6章 競爭情勢

- 策略趨勢

- 市佔率和排名分析

- 公司簡介

- Ahlstrom

- Amcor plc

- Asahi Kasei Advance Corp.

- Avgol Nonwovens

- Dalian Ruiguang Nonwoven Group

- Don & Low Ltd.

- DuPont

- Fibertex Nonwovens A/S

- Fitesa SA

- Freudenberg Group

- Glatfelter Corp.

- Johns Manville

- Kimberly-Clark Worldwide, Inc.

- Kingsafe Group

- Lydall Performance Materials

- Magnera

- Mitsui Chemicals Inc.

- PFNonwovens Holding

- Sandler AG

- Schouw & Co.(Fibertex Personal Care)

- Shandong Kangjie Nonwovens

- Sunshine Nonwoven Fabric Co.

- Suominen Corp.

- Toray Advanced Materials Korea Inc.

第7章 市場機會與未來展望

According to Mordor Intelligence, the polypropylene non-woven fabric market size is expected to grow from USD 38.95 billion in 2025 to USD 41.46 billion in 2026 and is forecast to reach USD 57.41 billion by 2031 at 6.73% CAGR over 2026-2031.

This report is Segmented by Production Technology (Spunbond, Meltblown, SMS (Spun-Melt-Spun), and More), Application (Hygiene, Medical, Packaging, Automotive, Filtration, and Other Applications), Raw Material Type (Homopolymer and Copolymer), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Polypropylene Non-woven Fabric Market Trends and Insights

Growing Demand in Hygiene and Medical Disposables

Hygiene and medical disposables continue to underpin volume growth as diaper, feminine care, and incontinence products proliferate in emerging economies while hospital systems institutionalize single-use infection-control protocols. Polypropylene spunbond topsheets provide hydrophobic surfaces with air permeability around 1,868 mm/s, reducing fluid strike-through time versus cellulosic alternatives. Kimberly-Clark's multi-site US manufacturing program, announced in 2025, underlines brand-owner confidence and increases domestic roll-goods procurement. Medical demand is outpacing hygiene on a percentage basis as SMS and SMMS composites achieve higher AAMI protection levels and as Tyvek sterilization wrap capacity additions support the surge in single-use medical devices. Industry reviews highlight a gap between gown barrier standards and real-world pathogen persistence, accelerating interest in validated antimicrobial polypropylene substrates. Collectively, these developments raise baseline consumption in the polypropylene non-woven fabric market.

Expanding Usage in Packaging Industry

Brand owners are shifting toward monomaterial structures to comply with Europe's 2030 recyclability targets, steering flexible packaging specifications toward high-purity, single-site polypropylene nonwovens. Borealis' 2026 scale-up of Borstar Nextension grades aims to supply this compliance-driven demand, offering improved sealing and mechanical recyclability for food contact and healthcare pouches. In logistics, breathable spunbond bags replace polyethylene films because they cut condensation damage during transport while maintaining printability for branding. Reuse and void-space caps embedded in the packaging regulation could depress some single-use volumes, yet they simultaneously create openings for durable nonwoven bag systems that satisfy reuse metrics. Near-term supply of food-grade recycled polypropylene remains tight, sustaining a premium that further differentiates virgin meltblown and spunbond rolls within the polypropylene non-woven fabric market.

Environmental and Regulatory Pressure on Single-Use Plastics

The EU Packaging and Packaging Waste Regulation, effective August 2026, obliges every pack format to meet at least grade C recyclability by 2030 and grade A or B by 2038, with recycled-content quotas escalating yearly. Extended producer responsibility fees penalize hard-to-recycle composites, directly affecting low-grammage commodity spunbond shopping bags and single-use tableware. A separate EU draft issued in September 2025 requires pellet-handling sites above 1,500 tons/year to certify risk-mitigation plans and exposes violators to fines up to 3% of Union turnover. North-American states are adopting analogous bag bans and recycled-content laws, tightening the policy vice. While industrial, automotive, and geotextile nonwovens remain largely untouched, converters serving consumer packaging segments must accelerate design-for-recycling initiatives to retain market access within the polypropylene non-woven fabric market.

Other drivers and restraints analyzed in the detailed report include:

- Lightweight, Cost-Effective Material Economics

- Increasing Utilization in Agriculture

- Polypropylene Price Volatility Linked to Crude Oil

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Spunbond retained 55% of the polypropylene non-woven fabric market share in 2025 owing to high-speed output and low unit costs that suit diapers, bags, and geotextiles. The polypropylene non-woven fabric market size for spunbond grades exceeded USD 21 billion in the base year, yet its forecast CAGR lags niche technologies as saturation sets in. Melt-blown, projected to grow 6.87% annually, benefits from regulatory upgrades to N95 respirators, HVAC, and battery-electrode separators that demand fibers below 3 µm diameter. Composite SMS and SMMS structures marry spunbond strength with melt-blown filtration, capturing hospital gown and industrial filtration spend. Investments in Reicofil 5 and equivalent lines across North America, Turkey, and China illustrate the capital pivot. Hybrid lines that alternate hot-air and calender bonding extend the basis-weight range to 10-200 g/m2, enabling automotive and roofing penetration.

Policy momentum compounds technical drivers. The US Department of Energy HVAC roadmap targets 50% energy reductions in commercial buildings by 2035, incentivizing high-efficiency melt-blown media; meanwhile, China's 2026 indoor-air-quality standard caps PM2.5 at 35 µg/m3, spurring cabin-air and residential filter demand. Supply tightness during 2020-2021 underscored the necessity of domestic melt-blown capacity, justifying government incentives in India, Indonesia, and Brazil. Equipment suppliers report order pipelines stretching into 2028, supporting a healthy backlog for the polypropylene non-woven fabric market.

Geography Analysis

Asia-Pacific controlled 42.67% of global demand in 2025 and is on track for a 6.91% CAGR through 2031 as China and India commission over 35 mt of integrated polypropylene capacity. Reliance's 5.20 million tonnes per annum Jamnagar plant, slated for 2030, alone can feed more than 10 billion m2 of spunbond fabric yearly, signaling an import-replacement strategy that elevates regional self-sufficiency. China's Fujian Eversun pipeline and Indonesia's Tuban complex likewise tighten the intra-Asia resin loop, reducing freight costs and carbon footprints. Converters take advantage, adding Reicofil and Oerlikon lines near end-markets to cut lead times and tailor basis-weight portfolios for local specifications.

North America's polypropylene non-woven fabric market benefits from OEM reshoring moves. Kimberly-Clark's USD 2 billion multi-state program and Avgol's Reicofil 5 installation in North Carolina enhance supply resilience and reduce overreliance on Asian imports. Ahlstrom's filter-media upgrade in Illinois, set for Q4 2026, will meet surging HVAC and EV filtration demand, underlining a structural pivot to domestic raw-material security. Resin price premiums remain a headwind, but domestic logistics savings and tariff avoidance partially offset higher feedstock costs.

Europe adds demand mainly through regulatory push for recyclable solutions. Borealis' 2026 Burghausen investment lines up with PPWR deadlines, offering grades that unlock monomaterial pouches and sterilizable medical wrap markets. Germany's polypropylene imports of 903 kt in 2024 illustrate dependence on intra-EU and Middle Eastern feedstock; CBAM adjustments could further redirect flows toward lower-carbon suppliers. South America and the Middle East & Africa remain emerging pockets, with Brazil's protected-cultivation subsidies and Turkey's twin 1 million tonnes per annum polypropylene projects expanding regional applicability of crop-protection and construction fabrics.

- Ahlstrom

- Amcor plc

- Asahi Kasei Advance Corp.

- Avgol Nonwovens

- Dalian Ruiguang Nonwoven Group

- Don & Low Ltd.

- DuPont

- Fibertex Nonwovens A/S

- Fitesa S.A.

- Freudenberg Group

- Glatfelter Corp.

- Johns Manville

- Kimberly-Clark Worldwide, Inc.

- Kingsafe Group

- Lydall Performance Materials

- Magnera

- Mitsui Chemicals Inc.

- PFNonwovens Holding

- Sandler AG

- Schouw & Co. (Fibertex Personal Care)

- Shandong Kangjie Nonwovens

- Sunshine Nonwoven Fabric Co.

- Suominen Corp.

- Toray Advanced Materials Korea Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing demand in hygiene and medical disposables

- 4.2.2 Expanding usage in packaging industry

- 4.2.3 Lightweight, cost-effective material economics

- 4.2.4 Increasing utilization in agriculture

- 4.2.5 Antimicrobial PP nonwovens enabling reusable PPE

- 4.3 Market Restraints

- 4.3.1 Environmental and regulatory pressure on single-use plastics

- 4.3.2 Polypropylene price volatility linked to crude oil

- 4.3.3 EU carbon border adjustment raising import cost

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Production Technology

- 5.1.1 Spunbond

- 5.1.2 Meltblown

- 5.1.3 SMS (Spun-Melt-Spun)

- 5.1.4 SMMS (Spun-Melt-Melt-Spun)

- 5.1.5 Other Production Technologies

- 5.2 By Application

- 5.2.1 Hygiene

- 5.2.2 Medical

- 5.2.3 Packaging

- 5.2.4 Automotive

- 5.2.5 Filtration

- 5.2.6 Agriculture

- 5.2.7 Other Applications

- 5.3 By Raw Material Type

- 5.3.1 Homopolymer

- 5.3.2 Copolymer

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 Japan

- 5.4.1.3 India

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 Nordic Countries

- 5.4.3.8 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Strategic Moves

- 6.2 Market Share (%)/Ranking Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.3.1 Ahlstrom

- 6.3.2 Amcor plc

- 6.3.3 Asahi Kasei Advance Corp.

- 6.3.4 Avgol Nonwovens

- 6.3.5 Dalian Ruiguang Nonwoven Group

- 6.3.6 Don & Low Ltd.

- 6.3.7 DuPont

- 6.3.8 Fibertex Nonwovens A/S

- 6.3.9 Fitesa S.A.

- 6.3.10 Freudenberg Group

- 6.3.11 Glatfelter Corp.

- 6.3.12 Johns Manville

- 6.3.13 Kimberly-Clark Worldwide, Inc.

- 6.3.14 Kingsafe Group

- 6.3.15 Lydall Performance Materials

- 6.3.16 Magnera

- 6.3.17 Mitsui Chemicals Inc.

- 6.3.18 PFNonwovens Holding

- 6.3.19 Sandler AG

- 6.3.20 Schouw & Co. (Fibertex Personal Care)

- 6.3.21 Shandong Kangjie Nonwovens

- 6.3.22 Sunshine Nonwoven Fabric Co.

- 6.3.23 Suominen Corp.

- 6.3.24 Toray Advanced Materials Korea Inc.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

不織布磨料市場:按形狀、磨料、基材、粘合劑、柔軟性、工件、最終用途產業、應用和分銷管道分類-2026-2032年全球市場預測

不織布磨料市場:按形狀、磨料、基材、粘合劑、柔軟性、工件、最終用途產業、應用和分銷管道分類-2026-2032年全球市場預測 不織布包裝:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)不織布:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

不織布包裝:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)不織布:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 2026-2034年全球粗梳不織布市場規模、佔有率、趨勢及成長分析報告

2026-2034年全球粗梳不織布市場規模、佔有率、趨勢及成長分析報告 紡織短纖維市場規模、佔有率和成長分析:按纖維類型、應用、最終用途、通路和地區分類-2026-2033年產業預測

紡織短纖維市場規模、佔有率和成長分析:按纖維類型、應用、最終用途、通路和地區分類-2026-2033年產業預測 高密度聚乙烯(HDPE)不織布市場規模、佔有率和成長分析:按技術、應用、終端用戶產業和地區分類-2026-2033年產業預測

高密度聚乙烯(HDPE)不織布市場規模、佔有率和成長分析:按技術、應用、終端用戶產業和地區分類-2026-2033年產業預測 全球布袋市場分析:市場規模、佔有率、應用及預測(2018-2034)

全球布袋市場分析:市場規模、佔有率、應用及預測(2018-2034) 不織布市場:按材料、技術、應用和地區分類可沖式不織布市場:至2031年的未來展望棉水針不織布市場:依布料成分、紙張重量、後整理、應用及通路分類-2026-2032年全球市場預測

不織布市場:按材料、技術、應用和地區分類可沖式不織布市場:至2031年的未來展望棉水針不織布市場:依布料成分、紙張重量、後整理、應用及通路分類-2026-2032年全球市場預測