|

市場調查報告書

商品編碼

2061988

農業著色劑:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Agricultural Colorants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

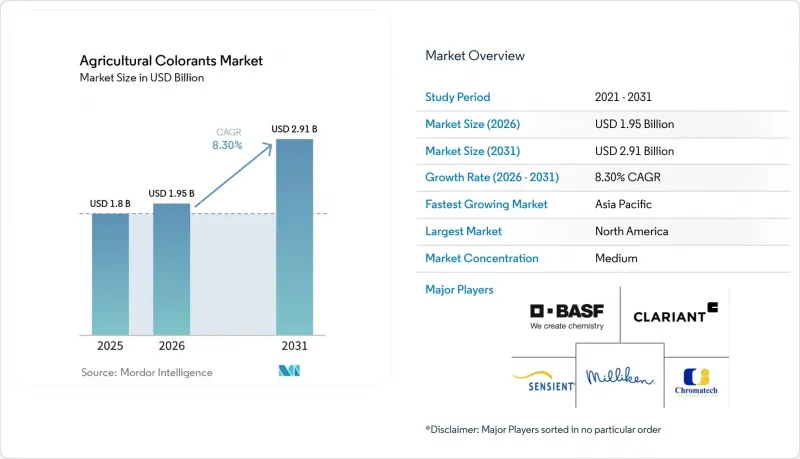

根據 Mordor Intelligence 預測,農業著色劑市場規模將從 2025 年的 18 億美元成長到 2026 年的 19.5 億美元,到 2031 年將進一步達到 29.1 億美元,2026 年至 2031 年的複合年成長率預計為 8.3%。

本報告按產品類型(染料和顏料)、應用領域(例如,種子處理著色劑)、劑型(例如,液體、粉末)、作物類型(例如,穀物、油籽、豆類)和地區(北美、歐洲、亞太、南美、非洲和中東)進行細分。報告以美元計價,呈現市場規模和預測數據。

全球農業著色劑市場趨勢及洞察

根據農藥法規強制執行種子顏色編碼

據農藥監管機構稱,監管機構正在將顏色編碼要求納入種子供應鏈。在美國,聯邦法規強制要求區分處理過的種子,加州在2025年進一步加強了新菸鹼類殺蟲劑的使用標準,規定使用不同的顏色以最大限度地減少授粉昆蟲接觸這些殺蟲劑的機會。同樣,印度的《2026年種子法》規定,違規者將被處以300萬印度盧比(約合3.6萬美元)的罰款,強制要求使用QR碼可追溯包裝,並實際上要求種子在進入市場時必須使用可見的著色劑。雖然成熟地區的種子滲透率正在上升,但在東南亞和非洲部分地區仍然很低,合規要求的實施為種子市場帶來了更多機會。

精密農業中對可見標記的需求

配備電腦視覺的噴霧器利用對比染料來驗證噴灑模式。約翰迪爾公司於2023年推出的「See and Spray Ultimate」系統,適用於北美大部分機型,該系統使用指示染料來驗證深色土壤中的噴灑覆蓋率。根據Ecorobotix公司2024年發布的數據顯示,瑞士一項使用其ARA精準噴霧器的試驗表明,化學品用量減少了95%。市場正日益兩極化,大規模農民傾向於經濟實惠的藍色染料,而特種作物種植者則選擇紫外線可視化混合物,以便利用無人機進行噴灑範圍測繪。

石油化學染料原料價格波動

根據美國能源資訊署(EIA)數據顯示,與石化產品密切相關的原油價格在2023年下跌了約10%,反映出上游能源市場的顯著波動。這些波動直接影響染料中間體的成本,導致農業著色劑價格不穩定,並增加農藥生產商的配方成本。此外,對石化衍生原料的依賴使供應鏈面臨地緣政治緊張局勢、煉油廠停產和監管挑戰等風險,加劇了成本的不確定性。儘管該行業正在逐步探索生物基替代品以減少對石化產品的依賴,但高昂的生產成本和有限的規模化能力仍然阻礙其廣泛應用。

細分市場分析

截至2025年,染料將佔據農業著色劑市場最大佔有率,達到46%。其主導地位源自於染料的溶解性,使其適用於快速水性種子披衣工藝,從而實現高效均勻的應用。顏料市場預計將呈現最高的成長率,從2026年到2031年將以11.2%的複合年成長率成長。顏料在對耐久性和性能要求極高的應用中更受歡迎,例如儲存在炎熱熱帶地區的聚合物包膜性肥料,這些應用需要具有紫外線穩定性和耐熱性。

根據二次性研究,成熟企業正透過使用可生物分解的分散劑來維持市場穩定。巴斯夫公司(BASF SE)於2025年推出的「Sokalan CP 301」可增強顏料在聚己內酯黏合劑中的懸浮性,從而加速微塑膠的消除。顏料生產商被要求用氧化鐵和符合耐褪色標準的先進有機顏料來取代重金屬基紅色和黃色顏料。科萊恩公司(Clariant AG)的“Agrocer”系列產品表明,有機紅色顏料在穀物中的性能與重金屬顏料相當。然而,與鉻酸鹽基顏料相比,有機紅色顏料成本較高,限制了其在肥料中的應用。

預計到2025年,種子處理劑將在農業著色劑市場佔據41%的最大市場。美國農業部(USDA)的報告指出,這一主導地位主要歸功於主要產區玉米和大豆作物的近乎全面推廣。同時,作物保護化學著色劑領域預計將在2026年至2030年間以12.7%的複合年成長率(CAGR)實現最高成長。據Precision Planting公司稱,2024年進行的田間試驗表明,SymphonyVision技術透過最大限度地減少噴霧重疊並實現即時噴嘴控制,從而減少除草劑浪費,提高行栽系統的噴灑效率。

應用領域的多元化與設備的進步密切相關。種子處理應用採用能與聚合物塗層有效融合的液體染料,而肥料混合器則傾向於使用無塵顆粒,以最大限度地減少空氣中的顆粒物。噴霧器需要快速褪色的液體標記物,以防止在新鮮農產品上留下殘留物。 Chromatech 提供多種受監管的庫存單位 (SKU),以滿足這些多樣化的需求。市場動態反映了精密設備的日益普及,而這又受到無人機應用日益廣泛的推動。指示染料有望縮小與傳統上佔據主導地位的種子處理應用之間的銷售量差距。

區域分析

預計北美將繼續保持其在農業著色劑市場的最大佔有率,到2025年將佔32%。這一主導地位得益於玉米種子處理技術的廣泛應用以及監管部門對視覺區分的強制性要求。加州正在進行一項利用紫外線進行合規性審計的試點項目,這可能會提升對可追溯色素的需求。在加拿大,根據加拿大衛生署關於微塑膠的指導方針,建議使用可生物分解的塗層。相較之下,墨西哥的種子著色劑應用有限,該國以小規模為主。然而,錫那羅亞州的蔬菜出口商正在實施噴灑指示器,以最大限度地減少滴灌系統中除草劑的浪費。

預計亞太地區將錄得最高成長率,2026年至2031年的複合年成長率將達到10.8%。在中國,大規模農業無人機編隊的作業需要使用低黏度指示染料。同時,在越南和泰國,政府對機械化插秧機的補貼正在加速顏色編碼技術的普及,儘管該技術目前尚未廣泛應用。在澳大利亞,儘管面臨高成本的挑戰,但向生物基顏料的過渡已取得進展。在日本溫室種植業,人們正在考慮使用隱形標籤來驗證供應鏈的真實性。然而,降低成本對於更廣泛地應用這項技術至關重要。

由於REACH法規導致顏料退出市場,歐洲市場受到影響,配方迅速轉向以氧化鐵和有機顏料為主。在西歐,種子處理劑的使用趨於飽和,隨著糧食種植機械化程度的提高,成長動能正轉向波蘭和羅馬尼亞等東歐國家。在南美洲,巴西主導農業著色劑市場,主要得益於大豆和甘蔗等作物採用顏色編碼。同時,阿根廷預計到2025年化肥進口量將成長17.5%,這將推動對顆粒狀顏料的需求。中東和非洲市場仍然分散,南非的釀酒葡萄種植者正在測試噴灑指示劑,以盡量減少農藥漂移到鄰近的有機農場。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 根據農藥法規,種子必須進行顏色編碼。

- 精密農業中對可見標記的需求

- 在無人機和自動噴灑器上採用噴灑指示染料。

- 推廣低粉塵、高負載種子披衣的相關法規

- 用於審核農藥施用狀態的紫外線顯色染料

- 用於人工智慧驅動的供應鏈認證的隱形標記

- 市場限制因素

- 石油化學染料原料價格波動

- 農藥製劑中重金屬和揮發性有機化合物(VOCs)的基準值

- 色素與活性成分相互作用所帶來的風險

- 種子性狀辨識技術可減少對顏色編碼的需求

- 監理情勢

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 依產品類型

- 染料

- 顏料

- 透過使用

- 種子處理著色劑

- 肥料和土壤改良劑用著色劑

- 用於作物保護的化學著色劑

- 用於灌溉和發泡記號筆的著色劑

- 按形式

- 液體

- 粉末

- 顆粒

- 按作物類型

- 穀類和穀類食品

- 油籽

- 豆子

- 水果和蔬菜

- 其他作物

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 其他北美國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 法國

- 英國

- 義大利

- 西班牙

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 印尼

- 越南

- 泰國

- 菲律賓

- 其他亞太國家

- 中東

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他中東國家

- 非洲

- 南非

- 埃及

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- BASF SE

- Clariant AG

- Sensient Technologies Corporation

- Milliken & Company

- Chromatech, Inc.

- Huntsman International LLC(Venator Materials PLC)

- Organic Dyes and Pigments, LLC

- LANXESS AG

- RPM International Inc.(DayGlo Color Corp.)

- Sudarshan Chemical Industries Limited

- SP Colour & Chemicals

- Kuraray Co., Ltd.

- DIC Corporation

- Sun Chemical Corporation

- Heubach GmbH

第7章 市場機會與未來展望

According to Mordor Intelligence, the agricultural colorants market size is projected to grow from USD 1.80 billion in 2025 to USD 1.95 billion in 2026 and is further projected to reach USD 2.91 billion by 2031, registering a CAGR of 8.3% during 2026-2031.

This report is Segmented by Product Type (Dyes and Pigments), by Application (Seed Treatment Colorants, and More), by Form (Liquid, Powder, and More), by Crop Type (Cereals and Grains, Oilseeds, Pulses, and More) and by Geography (North America, Europe, Asia-Pacific, South America, Africa, and Middle East). The Report Offers the Market Size and Forecasts in Terms of Value (USD).

Global Agricultural Colorants Market Trends and Insights

Mandatory Seed-Color Coding Under Pesticide Regulations

According to the Department of Pesticide Regulation, regulators are incorporating color-coding requirements into seed supply chains. In the United States, federal regulations mandate the differentiation of treated seeds, and California further strengthened these standards in 2025 for neonicotinoids, specifying distinct colors to minimize pollinator exposure. Similarly, India's Seed Act of 2026 introduces monetary penalties of INR 3 million (USD 36,000) and requires QR-traceable packaging, effectively mandating the use of visible colorants for market entry. Penetration rates have increased in mature regions but remain lower in Southeast Asia and parts of Africa, providing opportunities driven by compliance requirements.

Demand for Visible Markers in Precision Agriculture

Computer-vision sprayers utilize contrast dyes to verify application patterns. John Deere's See and Spray Ultimate, deployed on most units across North America in 2023, uses indicator dyes to confirm coverage on dark soils. According to Ecorobotix in 2024, Swiss trials with the company's ARA precision sprayer demonstrated a 95% reduction in chemical usage. The market is experiencing divergence, with large row-crop growers favoring economical blue dyes, while specialty-crop producers are opting for UV-traceable blends that enable drone-based coverage mapping.

Petrochemical Dye Feedstock Price Volatility

According to the United States Energy Information Administration, crude oil prices, which are closely tied to petrochemical derivatives, decreased by approximately 10% in 2023, reflecting notable fluctuations in upstream energy markets. These variations directly influence the cost of dye intermediates, resulting in inconsistent pricing for agricultural colorant manufacturers and higher formulation costs for agrochemical companies. Furthermore, reliance on petrochemical-based inputs exposes the supply chain to risks such as geopolitical tensions, refinery disruptions, and regulatory challenges, exacerbating cost uncertainties. Although the industry is gradually exploring bio-based alternatives to reduce dependency, higher production costs and limited scalability continue to hinder their broader adoption.

Other drivers and restraints analyzed in the detailed report include:

- Adoption of Spray Indicator Dyes for Drones and Autonomous Sprayers

- Regulatory Push for Low-Dust, High-Load Seed Coatings

- Heavy-Metal and Volatile Organic Compound (VOC) Limits in Agrochemical Formulations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Dyes accounted for the largest agricultural colorants market share in 2025, representing 46% of the market. This dominance is attributed to their solubility, which is well-suited for high-speed aqueous seed-coating processes, enabling efficient and uniform application. The pigments market size is projected to grow at the fastest rate, with a CAGR of 11.2% from 2026 to 2031. Pigments are preferred in applications requiring ultraviolet stability and heat resistance, such as polymer-coated fertilizers stored in elevated tropical temperatures, where durability and performance are critical.

Second-tier analysis highlights that incumbents are maintaining market continuity through the use of biodegradable dispersants. BASF SE's Sokalan CP 301, introduced in 2025, supports pigment suspension within polycaprolactone binders, facilitating the shift away from microplastics. Pigment manufacturers are required to replace heavy-metal reds and yellows with iron oxides or advanced organic pigments that meet fade-resistance standards. Clariant AG's Agrocer line demonstrates that organic reds can achieve comparable performance on cereals. However, the adoption of fertilisers remains limited due to higher costs compared to chromate pigments.

Seed treatment is projected to account for the largest market share of 41% for the agricultural colorants market in 2025. This dominance is attributed to near-universal coverage of corn and soybean crops in established regions, as reported by the United States Department of Agriculture (USDA). Meanwhile, the crop protection chemical colorants segment is projected to grow at the fastest CAGR of 12.7% from 2026 to 2030. According to Precision Planting, field trials conducted in 2024 showed that SymphonyVision technology reduces herbicide waste by minimizing spray overlap and enabling real-time nozzle control, thereby improving application efficiency in row crop systems.

Application fragmentation corresponds with advancements in equipment. Seed treatment applications utilize liquid dyes that integrate effectively into polymer coatings, while fertilizer blenders prefer dust-free granules to minimize airborne particulates. Spray operators require rapidly fading liquid markers to prevent residue on fresh produce. Chromatech offers multiple compliance-cleared stock-keeping units to cater to these varied demands. Market share dynamics reflect the adoption of precision equipment as drone usage increases. Indicator dyes may reduce the volume gap with traditionally dominant seed treatment applications.

Geography Analysis

North America is projected to hold the largest share of the agricultural colorants market, accounting for 32% in 2025. This dominance is driven by widespread seed treatment practices in corn and regulatory requirements mandating visible distinctions. California is conducting pilot ultraviolet compliance audits, potentially driving demand for traceable pigments. In Canada, biodegradable coatings are being encouraged under Health Canada's microplastic guidelines. In contrast, Mexico has limited seed-coloration coverage, primarily due to the dominance of smallholder farms. However, vegetable exporters in Sinaloa are implementing spray indicators to minimize herbicide waste in drip irrigation systems.

The Asia-Pacific region is projected to register the fastest CAGR of 10.8% from 2026 to 2031. China's large agricultural drone fleet necessitates low-viscosity indicator dyes. whereas government subsidies for mechanized rice planters in Vietnam and Thailand are facilitating the adoption of color-coding, which currently remains low. Meanwhile, Australia is shifting toward bio-based pigments, despite the challenges associated with higher costs. Japan's greenhouse sector is investigating the use of invisible taggants for supply chain authentication. However, broader implementation is contingent on achieving cost reductions.

The European market is influenced by REACH-driven pigment withdrawals, prompting swift reformulations favoring iron oxides and organic pigments. In Western Europe, seed-treatment adoption exceeds saturation, with incremental growth shifting eastward to countries like Poland and Romania as cereal mechanization advances. In South America, Brazil dominates the agricultural colorants market, driven by the adoption of color-coding for crops such as soy and sugarcane. Meanwhile, Argentina's projected 17.5% increase in fertilizer imports by 2025 is projected to boost demand for granular pigments. The Middle East and Africa markets remain fragmented, with South African wine-grape growers testing spray indicators to minimize drift onto neighboring organic farms.

- BASF SE

- Clariant AG

- Sensient Technologies Corporation

- Milliken & Company

- Chromatech, Inc.

- Huntsman International LLC (Venator Materials PLC)

- Organic Dyes and Pigments, LLC

- LANXESS AG

- RPM International Inc. (DayGlo Color Corp.)

- Sudarshan Chemical Industries Limited

- SP Colour & Chemicals

- Kuraray Co., Ltd.

- DIC Corporation

- Sun Chemical Corporation

- Heubach GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Mandatory seed-color coding under pesticide regulations

- 4.2.2 Demand for visible markers in precision agriculture

- 4.2.3 Adoption of spray indicator dyes for drones and autonomous sprayers

- 4.2.4 Regulatory push for low-dust, high-load seed coatings

- 4.2.5 UV-traceable colorants for pesticide coverage audit

- 4.2.6 Invisible taggants for AI-based supply chain authentication

- 4.3 Market Restraints

- 4.3.1 Petrochemical dye feedstock price volatility

- 4.3.2 Heavy-metal and volatile organic compound (VOC) limits in agrochemical formulations

- 4.3.3 Dye-active-ingredient interaction risks

- 4.3.4 Seed trait ID technologies reducing color-coding needs

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Dyes

- 5.1.2 Pigments

- 5.2 By Application

- 5.2.1 Seed Treatment Colorants

- 5.2.2 Fertilizer and Soil Amendment Colorants

- 5.2.3 Crop Protection Chemical Colorants

- 5.2.4 Irrigation and Foam Marker Colorants

- 5.3 By Form

- 5.3.1 Liquid

- 5.3.2 Powder

- 5.3.3 Granules

- 5.4 By Crop Type

- 5.4.1 Cereals and Grains

- 5.4.2 Oilseeds

- 5.4.3 Pulses

- 5.4.4 Fruits and Vegetables

- 5.4.5 Other Crops

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.1.4 Rest of North America

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 France

- 5.5.3.3 United Kingdom

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 Australia

- 5.5.4.5 Indonesia

- 5.5.4.6 Vietnam

- 5.5.4.7 Thailand

- 5.5.4.8 Philippines

- 5.5.4.9 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Egypt

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 BASF SE

- 6.4.2 Clariant AG

- 6.4.3 Sensient Technologies Corporation

- 6.4.4 Milliken & Company

- 6.4.5 Chromatech, Inc.

- 6.4.6 Huntsman International LLC (Venator Materials PLC)

- 6.4.7 Organic Dyes and Pigments, LLC

- 6.4.8 LANXESS AG

- 6.4.9 RPM International Inc. (DayGlo Color Corp.)

- 6.4.10 Sudarshan Chemical Industries Limited

- 6.4.11 SP Colour & Chemicals

- 6.4.12 Kuraray Co., Ltd.

- 6.4.13 DIC Corporation

- 6.4.14 Sun Chemical Corporation

- 6.4.15 Heubach GmbH

7 Market Opportunities and Future Outlook

著色劑市場:2026-2032年全球市場預測,依顏色類型、原料、形態、應用及通路分類

著色劑市場:2026-2032年全球市場預測,依顏色類型、原料、形態、應用及通路分類 著色劑市場:按地區和應用分類的需求及至2034年的預測

著色劑市場:按地區和應用分類的需求及至2034年的預測 2026-2030年全球顏料市場園林綠化色素市場:按來源、顏色、形態、最終用戶、銷售管道和應用方法分類,全球預測(2026-2032年)聚合物著色劑市場按應用、終端用戶產業、產品類型、聚合物類型、化學類型、分銷管道和技術分類-2026-2032年全球預測

2026-2030年全球顏料市場園林綠化色素市場:按來源、顏色、形態、最終用戶、銷售管道和應用方法分類,全球預測(2026-2032年)聚合物著色劑市場按應用、終端用戶產業、產品類型、聚合物類型、化學類型、分銷管道和技術分類-2026-2032年全球預測 著色劑市場規模、佔有率和趨勢分析報告:按應用、地區和細分市場預測(2026-2033 年)

著色劑市場規模、佔有率和趨勢分析報告:按應用、地區和細分市場預測(2026-2033 年) 著色劑市場規模、佔有率和成長分析(按類型、技術、配方和地區分類)—2026-2033年產業預測

著色劑市場規模、佔有率和成長分析(按類型、技術、配方和地區分類)—2026-2033年產業預測 著色劑市場-全球產業規模、佔有率、趨勢、機會和預測(按類型、最終用戶、地區和競爭細分,2020-2030 年)著色劑市場、規模、佔有率、趨勢、行業分析報告:按顏色、形式、成分、行業和地區 - 市場預測,2025-2034 年

著色劑市場-全球產業規模、佔有率、趨勢、機會和預測(按類型、最終用戶、地區和競爭細分,2020-2030 年)著色劑市場、規模、佔有率、趨勢、行業分析報告:按顏色、形式、成分、行業和地區 - 市場預測,2025-2034 年 農業著色劑市場報告:趨勢、預測和競爭分析(至 2030 年)

農業著色劑市場報告:趨勢、預測和競爭分析(至 2030 年)