|

市場調查報告書

商品編碼

2061846

烘焙加工設備:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Bakery Processing Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

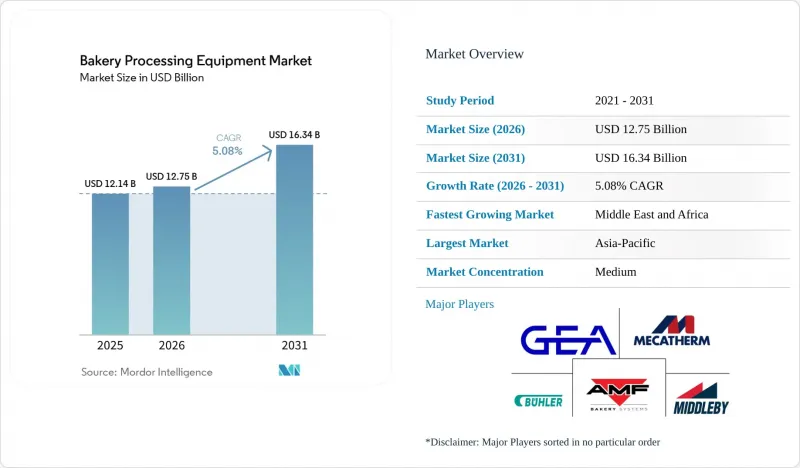

根據 Mordor Intelligence 預測,麵包加工設備的市場規模預計將從 2025 年的 121.4 億美元成長到 2026 年的 127.5 億美元,到 2031 年達到 163.4 億美元,2026 年至 2031 年的複合年成長率為 5.08%。

本報告按設備類型(攪拌機和混合機、分割機和滾圓機、成型機和壓片機、烤箱和醒發箱、其他)、應用領域(麵包、蛋糕和糕點、餅乾、披薩餅皮、其他)以及地區(北美、歐洲、亞太、南美、中東和非洲)進行細分。市場預測以美元計價。

全球烘焙加工設備市場趨勢及洞察

世界各地對手工和特色烘焙產品的需求日益成長。

配備獨立區域控制和麵團處理設備的層式烤箱目前處於設計需求的前沿。即使在高水分、長時間發酵的麵團中,這些設備也能保持氣孔結構,這對於手工麵包製作中實現理想的質地和風味至關重要。此外,隨著6%的消費者現在更傾向於在家中或商店購買烘焙產品,對靈活高效的加工設備的需求日益成長。烤箱和醒發箱市場的供應商正見證著對高度柔軟性的生產線的激增需求,這些生產線無需更換模具即可在恰巴塔和佛卡夏之間切換。這提高了營運效率並減少了停機時間。根據IBIE 2025年的調查,64%的北美烘焙師累計在未來24個月內為專用生產線預留預算,尤其關注斯卑爾脫小麥和玉米的加工能力,這主要是由於消費者對古老穀物及其健康益處的興趣所驅動的。雖然這種趨勢在對成本較為敏感的亞太地區不太明顯,但上海和孟買的精品連鎖店已經開始順應西方的需求模式,儘管滯後了五年,但它們正逐步迎合日益壯大的注重健康和高階消費者的利基市場。

自動化和衛生設計標準的進步

諸如FSMA、NSF/ANSI 169和EHEDG等法規強制要求使用衛生機殼、免工具拆卸和CIP清洗系統,以確保食品加工和製造符合嚴格的衛生和安全標準。 Middlebee和VMI等供應商正在銷售攪拌機和烤箱,這些設備可將清潔時間縮短40%,並能以數位方式記錄衛生管理週期,從而減輕資金籌措負擔並提高營運效率。嵌入式感測器和智慧人機介面(HMI)可協助操作人員降低60%的人事費用,投資可在12至18個月內收回。鑑於薪資成長速度超過融資成本,自動化成為一種經濟高效的解決方案,這一點尤其具有吸引力。同時,小規模企業正在採用季節性租賃協議來克服資金短缺,使他們能夠在無需大量前期投資的情況下採用先進設備。

對先進設備生產線進行大量資本投資

目前,承包麵包房的建設需要200萬至500萬美元的投資。 9至12個月的前置作業時間以及比2024年之前的平均值高出200至300個基點的資金籌措,加劇了這項挑戰。不斷上漲的成本和更長的交貨週期是進入市場的主要障礙。由於預算緊張,新參與企業轉向二手歐洲二手設備,折扣高達70%。雖然這種方法降低了初始資本投資,但往往會導致營運效率下降。此外,依賴翻新設備限制了業務擴充性,使這些公司難以與成熟的市場領導競爭。這種選擇延緩了自動化技術的全面普及,這一趨勢在拉丁美洲和東南亞尤為明顯。自動化普及的延遲進一步影響了這些地區的生產力和滿足不斷成長的消費者需求的能力。

細分市場分析

預計到2025年,烤箱和醒發箱將佔據熱處理設備市場總銷售額的32.56%,佔據主導地位。這一主導地位得益於其豐富的產品線,包括層式、架式、隧道式、螺旋式和混合燃料系統,每種系統都旨在滿足不同的加工能力和配方需求。這些系統對於麵包生產至關重要,並支撐著該細分市場的強勁需求。此外,混合燃料隧道、熱回收模組和快速換帶系統等創新技術不僅提高了營運效率,還有助於降低成本,從而延長了設備的升級週期。儘管來自中國OEM廠商的價格壓力不容忽視,但眼光獨到的優質買家依然堅定不移,他們優先考慮的是生命週期成本、可靠性和售後服務。

模塑機和片狀成型機正迅速崛起,預計到2031年將佔據14%的市場。這一快速成長主要得益於可頌麵包和酥皮點心等分層糖果甜點工業化生產的擴張。預計到2031年,該細分市場的複合年成長率將達到5.08%,這表明高產量烘焙企業正在擴大採用此類設備。尤其是在大規模型工廠中,麵團處理的自動化和統一化的努力正在推動這一成長。此外,精密成型技術的進步以及與連續生產線的無縫整合也在加速其應用。隨著烘焙製造商不斷擴大其分層產品線,對最先進的模塑機和片狀成型設備的投資預計將進一步加速。

區域分析

預計到2025年,亞太地區將繼續維持領先地位,佔39.53%的銷售佔有率,主要得益於中國、印度和東南亞國協新增產能的擴張。本土OEM廠商提供的價格優勢有助於本地烘焙業者更快收回投資,但在配方精準度和運作至關重要的領域,高階進口產品仍然更受歡迎。都市化和包裝烘焙食品需求的成長正在推動二、三線城市的資本投資。此外,政府對食品加工基礎設施的獎勵也加速了先進烘焙技術的應用。區域企業也擴大採用自動化技術,以提高產品一致性並減少對技術純熟勞工的依賴。

預計中東和非洲地區將以7.02%的複合年成長率實現強勁成長。在沙烏地阿拉伯,政府支持的投資重點放在麵包這一主食的本地生產;而埃及生產商已將產量提高了五倍,以滿足北非超級市場的需求。零售連鎖店的擴張和現代銷售模式的普及推動了對標準化、大規模生產麵包解決方案的需求。海灣國家對糧食安全計畫的投資進一步增強了當地的生產能力。與歐洲設備供應商的合作使區域製造商能夠提升其技術能力。人口成長和不斷變化的都市區消費模式將繼續支撐市場的長期成長。

在歐洲和北美這兩個市場佔有率較大的地區,企業的焦點正從擴大產能轉向投資設備升級。這項轉變的主要驅動力是日益嚴格的衛生和能源法規。製造商優先考慮設備升級,以滿足嚴格的排放氣體法規和食品安全標準。數位化技術的引進,包括物聯網監控系統,正成為設備採購決策的關鍵因素。烘焙企業可以透過在現有生產線中引入節能組件來控制營運成本。此外,人手不足也加速了自動化和遠距離診斷的應用。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 世界各地對手工和特色烘焙產品的需求日益成長。

- 自動化和衛生設計標準的進步

- 在永續性法規的背景下引入節能設備

- 亞太地區新興市場工業規模麵包房的擴張

- 利用物聯網進行預測性維護,減少意外停機時間。

- 用於無麩質和替代穀物配方的專用設備

- 市場限制因素

- 先進設備生產線的大量資本投資

- 技術純熟勞工短缺和學習曲線陡峭

- 電子元件供應鏈中的脆弱性

- 預計即將實施的碳關稅正在推高生命週期成本。

- 供應鏈分析

- 監理展望

- 技術展望

- 波特五力分析

第5章 市場規模與成長預測

- 依設備類型

- 攪拌機和攪拌器

- 分切機和圓角機

- 注塑機和板材切割機

- 烤箱和醒發箱

- 其他

- 透過使用

- 麵包

- 蛋糕和糕點

- 餅乾和曲奇

- 披薩餅皮

- 其他

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 其他北美國家

- 歐洲

- 德國

- 英國

- 義大利

- 法國

- 西班牙

- 荷蘭

- 其他歐洲國家

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 其他亞太國家

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 中東和非洲

- 南非

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他中東和非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- GEA Group Aktiengesellschaft

- Buhler Holding AG

- John Bean Technologies Corporation

- The Middleby Corporation(Baker Perkins)

- Ali Group Srl(Rondo)

- AMF Bakery Systems(a Markel Food Group Company)

- Mecatherm SA

- Rademaker BV

- WP Bakery Group GmbH

- Koenig Maschinen GmbH

- European Pastry & Bakery Machinery(EBAK)

- Reading Bakery Systems(a Markel Food Group Company)

- Revent International AB

- Shaffer Mixing

- Zeppelin Systems GmbH

- Oshikiri Machinery Ltd.

- VMI SA(VMI Group)

- Sigma Srl

- Rheon Automatic Machinery Co., Ltd.

- Gemini Bakery Equipment Company

第7章 市場機會與未來展望

According to Mordor Intelligence, the bakery processing equipment market size is expected to increase from USD 12.14 billion in 2025 to USD 12.75 billion in 2026 and reach USD 16.34 billion by 2031, growing at a 5.08% CAGR over 2026-2031.

This report is Segmented by Equipment Type (Mixers and Blenders, Dividers and Rounders, Molders and Sheeters, Ovens and Proofers, Others), Application (Bread, Cakes and Pastries, Cookies and Biscuits, Pizza Crusts, Others), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). Market Forecasts are Provided in Terms of Value (USD).

Global Bakery Processing Equipment Market Trends and Insights

Rising global demand for artisanal and specialty bakery products

Independent zone-control deck ovens and gentle-handling molders are now at the forefront of design briefs, allowing for high-hydration, long-fermentation doughs that maintain their gas-cell structure, which is critical for achieving desired texture and flavor profiles in artisanal baking. Moreover, as 6% of consumers shift their preferences towards bakery purchases, whether at home or in-store, the demand for adaptable and efficient processing equipment becomes increasingly evident. Suppliers in the ovens and proofers market are witnessing a surge in demand for flexible lines, capable of transitioning from ciabatta to focaccia without the need for tooling swaps, thereby enhancing operational efficiency and reducing downtime. An IBIE survey from 2025 highlighted that 64% of North American bakers are allocating budgets for specialty lines within the next 24 months, with a particular focus on spelt and einkorn capabilities, driven by consumer interest in ancient grains and their perceived health benefits. While this trend is muted in the cost-sensitive Asia-Pacific region, boutique chains in Shanghai and Mumbai are already aligning with Western demand patterns, albeit with a five-year delay, as they gradually cater to a growing niche of health-conscious and premium-seeking consumers.

Increased automation and hygienic-design standards

Protocols like FSMA, NSF/ANSI 169, and EHEDG mandate sanitary enclosures, tool-free disassembly, and CIP circuits to ensure compliance with stringent hygiene and safety standards in food processing and manufacturing. Vendors, including Middleby and VMI, tout mixers and ovens that slash cleaning time by 40% and digitally log sanitation cycles, lightening the audit load and improving operational efficiency. With embedded sensors and smart HMIs, operators enjoy a 60% reduction in labor costs and a return on investment within 12 to 18 months. This is especially appealing as wage inflation surpasses financing expenses, making automation a cost-effective solution. Meanwhile, smaller operators are turning to leasing structures with seasonal repayments to navigate the capital gap, enabling them to adopt advanced equipment without significant upfront investment.

High capital expenditure for advanced equipment lines

Turnkey bakeries now demand an investment of USD 2-5 million. This challenge is intensified by lead times stretching 9-12 months and financing costs that are 200-300 basis points higher than averages seen before 2024. These higher costs and extended timelines have created significant barriers for new players in the market. With tighter budgets, new entrants are leaning towards refurbished European machinery, snagging them at discounts of up to 70%. This approach allows them to reduce initial capital expenditure but often comes at the expense of operational efficiency. Additionally, the reliance on refurbished equipment limits the scalability of operations, making it harder for these players to compete with established market leaders. This choice has led to a postponement in fully adopting automation, a trend particularly evident in Latin America and Southeast Asia. The delayed automation adoption further impacts productivity and the ability to meet growing consumer demand in these regions.

Other drivers and restraints analyzed in the detailed report include:

- Energy-efficient equipment adoption amid sustainability mandates

- Expansion of industrial-scale bakeries in emerging asia-pacific markets

- Skilled-labor shortage and steep learning curve

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, ovens and proofers are set to command a dominant 32.56% share of the thermal-processing equipment market's total revenue. Their supremacy is bolstered by a diverse product lineup, featuring deck, rack, tunnel, spiral, and hybrid fuel systems, each tailored for distinct throughput and formulation needs. These systems are indispensable in bakery production, underscoring the segment's robust demand. Furthermore, innovations like hybrid-fuel tunnels, heat-recovery modules, and rapid belt-change systems not only boost operational efficiency but also curtail costs, perpetuating a cycle of equipment upgrades. While Chinese OEMs exert pricing pressures, discerning premium buyers remain steadfast, emphasizing lifecycle costs, reliability, and after-sales service.

Molders and sheeters are on a rapid ascent, eyeing a 14% market share by 2031. This surge is fueled by the rising industrial-scale production of laminated delicacies like croissants and pastries. Anticipating a CAGR of 5.08% until 2031, the segment's growth is a testament to its adoption in high-volume bakery operations. The push for automation and uniformity in dough handling, especially in large-scale and export-focused facilities, drives this expansion. Moreover, advancements in precision forming and seamless integration with continuous production lines are hastening the adoption. As bakery producers broaden their laminated offerings, the momentum for investing in cutting-edge molding and sheeting equipment is poised to escalate.

Geography Analysis

In 2025, the Asia-Pacific region is projected to hold a leading 39.53% revenue share, driven by the development of greenfield capacities in China, India, and various ASEAN nations. Domestic OEMs offer price advantages that enable local bakers to achieve faster returns on investment, although premium imports remain preferred in scenarios where recipe precision and uptime are critical. The rise in urbanization and increasing demand for packaged bakery products are driving equipment investments in tier-2 and tier-3 cities. Additionally, government incentives supporting food processing infrastructure are accelerating the adoption of advanced baking technologies. Regional players are also increasingly adopting automation to enhance consistency and reduce reliance on skilled labor.

The Middle East and Africa are expected to record a strong 7.02% CAGR. In Saudi Arabia, sovereign wealth investments are focused on localizing staple bread production, while Egyptian producers are increasing output fivefold to meet the needs of North African supermarkets. Expanding retail chains and modern trade formats are boosting demand for standardized, high-volume baking solutions. Investments in food security programs across Gulf nations are further strengthening local production capabilities. Partnerships with European equipment suppliers are also enabling regional manufacturers to upgrade their technological capabilities. Population growth and evolving urban consumption patterns continue to support long-term market growth.

Europe and North America, which together account for a significant market share, are shifting their focus from capacity expansion to replacement spending. This shift is primarily driven by stringent hygiene and energy regulations. Manufacturers are prioritizing equipment upgrades to meet strict emissions and food safety standards. The adoption of digitalization, including IoT-enabled monitoring systems, is becoming a key factor in equipment procurement decisions. Retrofitting existing production lines with energy-efficient components is helping bakeries manage operational costs. Furthermore, labor shortages are accelerating the adoption of automation and remote diagnostics.

- GEA Group Aktiengesellschaft

- Buhler Holding AG

- John Bean Technologies Corporation

- The Middleby Corporation (Baker Perkins)

- Ali Group S.r.l. (Rondo)

- AMF Bakery Systems (a Markel Food Group Company)

- Mecatherm S.A.

- Rademaker B.V.

- WP Bakery Group GmbH

- Koenig Maschinen GmbH

- European Pastry & Bakery Machinery (EBAK)

- Reading Bakery Systems (a Markel Food Group Company)

- Revent International AB

- Shaffer Mixing

- Zeppelin Systems GmbH

- Oshikiri Machinery Ltd.

- VMI SA (VMI Group)

- Sigma S.r.l.

- Rheon Automatic Machinery Co., Ltd.

- Gemini Bakery Equipment Company

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising global demand for artisanal and specialty bakery products

- 4.2.2 Increased automation and hygienic-design standards

- 4.2.3 Energy-efficient equipment adoption amid sustainability mandates

- 4.2.4 Expansion of industrial-scale bakeries in emerging Asia-Pacific markets

- 4.2.5 IoT-enabled predictive maintenance reducing unplanned downtime

- 4.2.6 Specialized equipment for gluten-free and alt-grain formulations

- 4.3 Market Restraints

- 4.3.1 High capital expenditure for advanced equipment lines

- 4.3.2 Skilled-labor shortage and steep learning curve

- 4.3.3 Electronic-component supply-chain fragility

- 4.3.4 Prospective carbon-border taxes inflating lifecycle costs

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Equipment Type

- 5.1.1 Mixers and Blenders

- 5.1.2 Dividers and Rounder

- 5.1.3 Molders and Sheeters

- 5.1.4 Ovens and Proofers

- 5.1.5 Others

- 5.2 By Application

- 5.2.1 Bread

- 5.2.2 Cakes and Pastries

- 5.2.3 Cookies and Biscuits

- 5.2.4 Pizza Crusts

- 5.2.5 Others

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.1.4 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 Italy

- 5.3.2.4 France

- 5.3.2.5 Spain

- 5.3.2.6 Netherlands

- 5.3.2.7 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 South Africa

- 5.3.5.2 Saudi Arabia

- 5.3.5.3 United Arab Emirates

- 5.3.5.4 Rest of Middle East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 GEA Group Aktiengesellschaft

- 6.4.2 Buhler Holding AG

- 6.4.3 John Bean Technologies Corporation

- 6.4.4 The Middleby Corporation (Baker Perkins)

- 6.4.5 Ali Group S.r.l. (Rondo)

- 6.4.6 AMF Bakery Systems (a Markel Food Group Company)

- 6.4.7 Mecatherm S.A.

- 6.4.8 Rademaker B.V.

- 6.4.9 WP Bakery Group GmbH

- 6.4.10 Koenig Maschinen GmbH

- 6.4.11 European Pastry & Bakery Machinery (EBAK)

- 6.4.12 Reading Bakery Systems (a Markel Food Group Company)

- 6.4.13 Revent International AB

- 6.4.14 Shaffer Mixing

- 6.4.15 Zeppelin Systems GmbH

- 6.4.16 Oshikiri Machinery Ltd.

- 6.4.17 VMI SA (VMI Group)

- 6.4.18 Sigma S.r.l.

- 6.4.19 Rheon Automatic Machinery Co., Ltd.

- 6.4.20 Gemini Bakery Equipment Company

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

烘焙和麵包加工設備市場:2026-2032年全球市場預測(按產品類型、設備類型、產能、技術、分銷管道和最終用途分類)

烘焙和麵包加工設備市場:2026-2032年全球市場預測(按產品類型、設備類型、產能、技術、分銷管道和最終用途分類) 麵包加工設備市場規模、佔有率、成長率及全球產業分析:按類型、應用和地區的洞察,2026-2034年的預測全球烘焙加工設備市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

麵包加工設備市場規模、佔有率、成長率及全球產業分析:按類型、應用和地區的洞察,2026-2034年的預測全球烘焙加工設備市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 2026年全球烘焙加工設備市場報告

2026年全球烘焙加工設備市場報告 烘焙設備市場:市場機會、成長促進因素、產業趨勢分析及預測(2026-2035)

烘焙設備市場:市場機會、成長促進因素、產業趨勢分析及預測(2026-2035) 烘焙加工設備市場規模、佔有率及成長分析(按設備類型、運作模式、應用、最終用戶和地區分類)-2026-2033年產業預測

烘焙加工設備市場規模、佔有率及成長分析(按設備類型、運作模式、應用、最終用戶和地區分類)-2026-2033年產業預測 烘焙加工設備市場規模、佔有率和趨勢分析報告:按設備、應用、地區和細分市場預測,2026-2033年

烘焙加工設備市場規模、佔有率和趨勢分析報告:按設備、應用、地區和細分市場預測,2026-2033年 商用烤爐翻轉輥:全球市場佔有率及排名、總收入及需求預測(2025-2031年)全球烘焙加工設備市場規模(按設備類型、應用、區域範圍、預測)

商用烤爐翻轉輥:全球市場佔有率及排名、總收入及需求預測(2025-2031年)全球烘焙加工設備市場規模(按設備類型、應用、區域範圍、預測) 2025-2029年全球工業烘焙加工設備市場

2025-2029年全球工業烘焙加工設備市場