|

市場調查報告書

商品編碼

1913380

烘焙設備市場:市場機會、成長促進因素、產業趨勢分析及預測(2026-2035)Bakery Processing Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

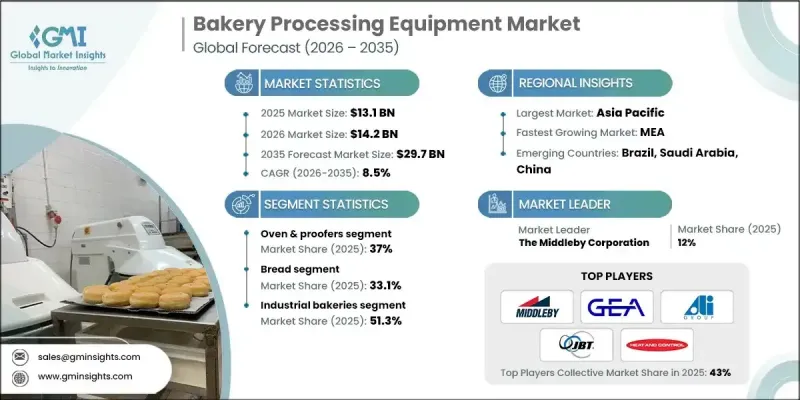

全球烘焙設備市場預計到 2025 年將達到 131 億美元,到 2035 年將達到 297 億美元,年複合成長率為 8.5%。

市場成長的驅動力在於整個麵包製作流程中自動化程度的加速提升,越來越多的公司致力於提高效率、減少勞動力依賴並維持統一的產品標準。自動化系統的廣泛應用最佳化了端到端的生產流程,幫助烘焙師在滿足不斷成長的生產需求的同時,有效控制了營運成本。消費者對差異化、客製化烘焙產品的需求日益成長,也影響著設備的採購決策,促使企業投資於能夠適應頻繁產品變更而不影響生產效率的靈活型機器。同時,人們對食品安全和衛生標準的日益重視也影響著設備的設計重點。烘焙師更加重視能夠支援衛生管理、降低污染風險並符合不斷變化的監管要求的機器。設備供應商也積極回應,推出兼顧清潔性、耐用性和合規性的設計,進一步強調了品質保證在現代烘焙環境中的重要性。這些趨勢共同作用,使麵包製作設備成為實現擴充性、合規性和滿足消費者需求的關鍵基礎。

| 市場覆蓋範圍 | |

|---|---|

| 開始年份 | 2025 |

| 預測期 | 2026-2035 |

| 初始市場規模 | 131億美元 |

| 市場規模預測 | 297億美元 |

| 複合年成長率 | 8.5% |

預計到2025年,商用烘焙領域將佔據51.3%的市場。該領域高度依賴大型高性能設備,以支援連續生產,同時確保大批量產品的品質穩定。該領域的需求將繼續集中在能夠提高精度、減少人工勞動並有助於實現成本效益型大規模生產的解決方案上。

2023年,醒發箱市佔率比37%。此細分市場在控制烘焙和醒發條件方面發揮核心作用,這些條件直接影響產品的均勻性、結構和整體品質。此類設備因其能夠維持穩定的加工環境,從而確保可靠的生產效果而備受青睞。

預計到2025年,歐洲烘焙設備市場規模將達到39億美元,這主要得益於強大的創新能力、嚴格的品質標準以及對永續發展的永續性重視。該地區的製造商在繼續優先考慮先進工程技術、能源效率和環保生產實踐的同時,也始終遵守法規結構並滿足不斷變化的消費者期望。

目錄

第1章:分析方法和範圍

第2章執行摘要

第3章業界考察

- 產業生態系分析

- 供應商情況

- 利潤率

- 每個階段的附加價值

- 影響價值鏈的因素

- 中斷

- 產業影響因素

- 促進要素

- 提高自動化程度以彌補烘焙行業的人手不足

- 冷凍和包裝烘焙產品成長

- 注重食品安全和產品一致性

- 產業潛在風險與挑戰

- 小規模麵包店初始資本投資成本高

- 現有設施的空間和公用設施限制

- 市場機遇

- 零售連鎖店和店內烘焙坊的擴張

- 潔淨標示、無麩質和特色產品趨勢

- 促進要素

- 成長潛力分析

- 監管環境

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 波特五力分析

- PESTEL 分析

- 價格趨勢

- 按地區

- 依產品類型

- 未來市場趨勢

- 科技與創新趨勢

- 當前技術趨勢

- 新興技術

- 專利狀態

- 貿易統計(HS編碼)

(註:貿易統計數據僅涵蓋主要國家。)

- 主要進口國

- 主要出口國

- 永續性和環境方面

- 永續努力

- 減少廢棄物策略

- 生產中的能源效率

- 環保舉措

- 考慮到碳足跡

第4章 競爭情勢

- 介紹

- 公司市佔率分析

- 按地區

- 北美洲

- 歐洲

- 亞太地區

- 拉丁美洲

- 中東和非洲

- 按地區

- 企業矩陣分析

- 主要企業的競爭分析

- 競爭定位矩陣

- 主要趨勢

- 企業合併(M&A)

- 商業夥伴關係與合作

- 新產品發布

- 業務拓展計劃

第5章 依產品類型分類的市場估算與預測(2022-2035 年)

- 烤箱醒發箱

- 混合器

- 體重低於250公斤

- 250~500 kg

- 500~1,000 kg

- 1,000~1,500 kg

- 1500公斤或以上

- 切片機

- 體重低於100公斤

- 100-150 kg

- 150~250 kg

- 250~350 kg

- 350公斤或以上

- 片狀成型機/模具成型機

- 500~1,000 kg

- 1,000~1,500 kg

- 1500公斤或以上

- 其他

第6章 按應用領域分類的市場估算與預測(2022-2035 年)

- 麵包

- 糕點

- 披薩

- 可頌麵包

- 扁麵包

- 派餅/乳酪餡餅

- 餅乾

- 玉米餅

7. 依最終用途分類的市場估計與預測(2022-2035 年)

- 商用麵包店

- 手工麵包店

- 零售麵包店

- 其他

第8章 各地區市場估算與預測(2022-2035 年)

- 北美洲

- 美國

- 加拿大

- 歐洲

- 德國

- 英國

- 法國

- 西班牙

- 義大利

- 其他歐洲

- 亞太地區

- 中國

- 印度

- 日本

- 澳洲

- 韓國

- 亞太其他地區

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 其他拉丁美洲

- 中東和非洲

- 沙烏地阿拉伯

- 南非

- 阿拉伯聯合大公國

- 其他中東和非洲地區

第9章:公司簡介

- The Middleby Corporation

- GEA Group

- ALI Group SRL A Socio Unico

- John Bean Technologies Corporation

- Markel Ventures Inc.

- Heat and Control, Inc.

- Rheon Automatic Machinery Co., Ltd.

- Fritsch Group

- Baker Perkins Ltd.

- Gemini Bakery Equipment Company

The Global Bakery Processing Equipment Market was valued at USD 13.1 billion in 2025 and is estimated to grow at a CAGR of 8.5% to reach USD 29.7 billion by 2035.

Market momentum is driven by the accelerating shift toward automation across bakery operations, as businesses focus on improving efficiency, lowering workforce dependency, and maintaining uniform product standards. Automated systems are increasingly being adopted to optimize end-to-end production workflows, helping bakeries meet rising output requirements while controlling operational expenses. Growing consumer demand for differentiated and made-to-order bakery offerings is also influencing equipment purchasing decisions, encouraging investment in adaptable machinery capable of handling frequent product changes without affecting throughput. In parallel, heightened attention to food safety and hygiene standards is shaping equipment design priorities. Bakeries place greater emphasis on machinery that supports sanitation, reduces contamination risk, and aligns with evolving regulatory expectations. Equipment suppliers are responding by introducing designs that support cleanliness, durability, and compliance, reinforcing the importance of quality assurance in modern bakery environments. These combined trends continue to position bakery processing equipment as a critical enabler of scalable, compliant, and consumer-responsive production.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $13.1 Billion |

| Forecast Value | $29.7 Billion |

| CAGR | 8.5% |

The industrial bakeries segment accounted for 51.3% share in 2025. This segment relies heavily on large-scale, high-performance equipment to support continuous production while ensuring consistent quality across large volumes. Demand from this segment remains focused on solutions that improve precision, reduce manual intervention, and support cost-efficient mass production.

The ovens and proofers category represented 37% share in 2023. This segment plays a central role in controlling baking and fermentation conditions, which directly influences product consistency, structure, and overall quality. Equipment in this category is valued for its ability to maintain stable processing environments that support reliable production outcomes.

Europe Bakery Processing Equipment Market reached USD 3.9 billion in 2025, supported by strong innovation capabilities, rigorous quality benchmarks, and a growing focus on sustainability. Regional manufacturers continue to prioritize advanced engineering, energy efficiency, and environmentally responsible production practices, aligning with regulatory frameworks and evolving consumer expectations.

Key companies active in the Global Bakery Processing Equipment Market include GEA Group, Baker Perkins Ltd., The Middleby Corporation, Rheon Automatic Machinery Co., Ltd., Gemini Bakery Equipment Company, ALI Group S.R.L. A Socio Unico, Heat and Control, Inc., John Bean Technologies Corporation, Fritsch Group, and Markel Ventures Inc. Companies operating in the Global Bakery Processing Equipment Market are strengthening their competitive position through technology-driven innovation and customer-focused solutions. Many manufacturers are investing in automation and digital integration to enhance equipment performance and operational reliability. Customization capabilities are being expanded to help bakeries respond to changing consumer preferences without sacrificing efficiency. Strategic partnerships with bakery operators are supporting long-term equipment adoption and service-based revenue models.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product Type

- 2.2.3 Application

- 2.2.4 End Use

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising automation to offset bakery labor shortages

- 3.2.1.2 Growth in frozen and packaged bakery products

- 3.2.1.3 Focus on food safety and product consistency

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High upfront capital cost for small bakeries

- 3.2.2.2 Space and utility constraints in existing facilities

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of retail chains and in-store bakeries

- 3.2.3.2 Clean-label, gluten-free and specialty product trends

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

( Note: The trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2022-2035 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Oven & proofers

- 5.3 Mixers

- 5.3.1 Below 250 kg

- 5.3.2 250-500 kg

- 5.3.3 500-1,000 kg

- 5.3.4 1,000-1,500 kg

- 5.3.5 Above 1,500 kg

- 5.4 Slicer

- 5.4.1 Below 100 kg

- 5.4.2 100-150 kg

- 5.4.3 150-250 kg

- 5.4.4 250-350 kg

- 5.4.5 Above 350 kg

- 5.5 Sheeters & molders

- 5.5.1 500-1,000 kg

- 5.5.2 1,000-1,500 kg

- 5.5.3 Above 1,500 kg

- 5.6 Others

Chapter 6 Market Estimates and Forecast, By Application, 2022-2035 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Bread

- 6.3 Pastry

- 6.4 Pizza

- 6.5 Croissant

- 6.6 Flatbread

- 6.7 Pie/Quiche

- 6.8 Biscuits

- 6.9 Tortilla

Chapter 7 Market Estimates and Forecast, By End Use 2022-2035 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Industrial bakeries

- 7.3 Artisanal bakeries

- 7.4 Retail bakeries

- 7.5 Others

Chapter 8 Market Estimates and Forecast, By Region, 2022-2035 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 The Middleby Corporation

- 9.2 GEA Group

- 9.3 ALI Group S.R.L. A Socio Unico

- 9.4 John Bean Technologies Corporation

- 9.5 Markel Ventures Inc.

- 9.6 Heat and Control, Inc.

- 9.7 Rheon Automatic Machinery Co., Ltd.

- 9.8 Fritsch Group

- 9.9 Baker Perkins Ltd.

- 9.10 Gemini Bakery Equipment Company

烘焙加工設備:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

烘焙加工設備:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 麵包加工設備市場:2026-2032年全球市場預測(依產品類型、設備類型、加工能力、技術、通路和最終用途分類)

麵包加工設備市場:2026-2032年全球市場預測(依產品類型、設備類型、加工能力、技術、通路和最終用途分類) 麵包加工設備市場規模、佔有率、成長率及全球產業分析:按類型、應用和地區的洞察,2026-2034年的預測全球烘焙加工設備市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

麵包加工設備市場規模、佔有率、成長率及全球產業分析:按類型、應用和地區的洞察,2026-2034年的預測全球烘焙加工設備市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 2026年全球烘焙加工設備市場報告

2026年全球烘焙加工設備市場報告 烘焙加工設備市場規模、佔有率及成長分析(按設備類型、運作模式、應用、最終用戶和地區分類)-2026-2033年產業預測

烘焙加工設備市場規模、佔有率及成長分析(按設備類型、運作模式、應用、最終用戶和地區分類)-2026-2033年產業預測 烘焙加工設備市場規模、佔有率和趨勢分析報告:按設備、應用、地區和細分市場預測,2026-2033年

烘焙加工設備市場規模、佔有率和趨勢分析報告:按設備、應用、地區和細分市場預測,2026-2033年 商用烤爐翻轉輥:全球市場佔有率及排名、總收入及需求預測(2025-2031年)全球烘焙加工設備市場規模(按設備類型、應用、區域範圍、預測)

商用烤爐翻轉輥:全球市場佔有率及排名、總收入及需求預測(2025-2031年)全球烘焙加工設備市場規模(按設備類型、應用、區域範圍、預測) 2025-2029年全球工業烘焙加工設備市場

2025-2029年全球工業烘焙加工設備市場