|

市場調查報告書

商品編碼

2061770

NOR閃存在家用電子電器)。NOR Flash For Consumer Electronics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

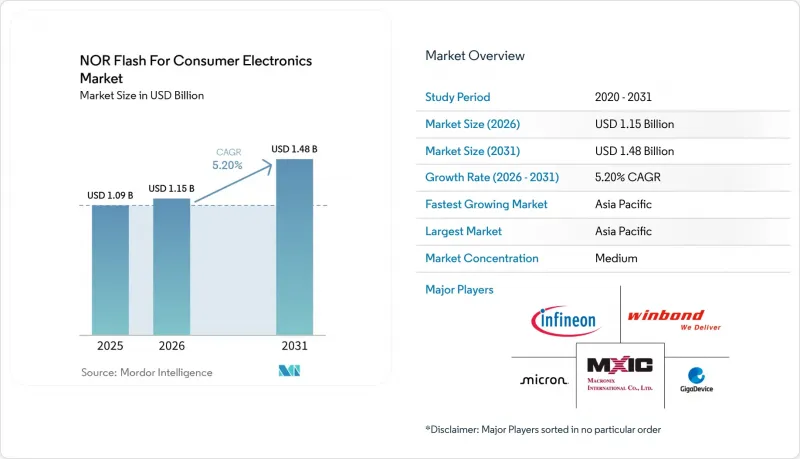

根據 Mordor Intelligence 預測,家用電子電器的 NOR 快閃記憶體市場規模將從 2025 年的 10.9 億美元成長到 2026 年的 11.5 億美元,到 2031 年將達到 14.8 億美元,2026 年至 2031 年的複合年成長率為 5.20%。

本報告依NOR快閃記憶體類型(串列和平行)、容量(2兆位元及以下及以上)、電壓(3V級、1.8V級及以上)、製程節點(55/58nm、65nm及以上)、封裝型態(WLCSP/CSP、QFN/SOIC等)及地區(北美、歐洲、亞太等)進行細分。市場預測以價值(美元)和銷售量(單位)為單位。

家用電子電器。

採用 XiP 架構的邊緣 AI 物聯網設備更傾向於使用高密度串列 NOR 記憶體。

家用電子電器領域的 NOR 快閃記憶體市場正受益於智慧顯示器、環境運算中心和連網家庭攝影機等邊緣 AI 設備的日益普及,這些設備需要具備高速啟動能力的程式碼儲存。由於這些產品需要持續存取韌體和推理相關功能,且不希望佔用過多 RAM,因此它們正轉向原地內存執行,這推動了設計週期中對高密度串行 NOR 閃存的需求。這一產品趨勢也有利於那些能夠將高密度、低電壓運行和緊湊尺寸相結合,以滿足小型化消費硬體需求的供應商。 2026 年 3 月,技嘉科技 (GigaDevice) 將其 GD25UF 1.2V 超低功耗 SPI NOR 快閃記憶體系列的容量範圍擴展至 8Mb 至 256Mb,使其產品定位於 AI 運算、穿戴式裝置、可聽裝置以及基於 ASIC 的平台。此次產品線的擴展印證了家用電子電器領域 NOR 快閃記憶體市場正從性能有限的基本代碼儲存組件轉向更高密度、更節能的串列設備這一觀點。

需要即時啟動(啟動後立即啟動)韌體的「語音優先」智慧家庭中心的普及。

此外,消費性電子市場對NOR快閃記憶體的需求也受到「語音優先」智慧家庭設備的推動,這些設備需要本地韌體持續可用,以便在喚醒事件發生後幾乎立即做出回應。智慧音箱、顯示中心、AI門鈴和智慧插座依賴於程式碼存儲,這種儲存方式無需像其他類型的記憶體那樣經歷漫長的載入過程,即可支援快速啟動。這種需求模式意義重大,因為許多品牌現在在其相關硬體平台上管理多個助理生態系統,這增加了每個設計必須處理的韌體支援量。華邦電子在其投資者資料中將智慧家庭定位為關鍵成長領域,並透露其F45nm製程相比上一代F58nm工藝,提高了TWS和物聯網應用的晶片尺寸效率。華邦電子也報告稱,到2025年,家用電子電器將佔其應用組合的29%,這表明這些設備類別對於家用電子電器NOR快閃記憶體市場和主要供應商而言仍然具有重要的商業性價值。

超過 256Mb 的 NAND 快閃記憶體的成本差異限制了高解析度相機的廣泛應用。

家用電子電器的NOR快閃記憶體市場在程式碼儲存容量需求遠超256Mb的應用中仍面臨實際容量限制。智慧型手機、運動攝影機和家庭監控產品中使用的高解析度相機模組正在迅速提高記憶體需求,這可能會將NAND快閃記憶體推向更具成本效益的大容量資料儲存領域。這種成本差距正在減少NOR閃光存在影像處理密集型裝置設計的應用,儘管快速啟動特性在系統層面仍然至關重要。宏碁在2024年年度報告中表示,其3D NOR快閃記憶體的研發旨在提高成本和密度競爭力,目標是在2026年下半年提供樣品,並在2027年開始量產。在這些產品廣泛商業化之前,家用電子電器的NOR快閃記憶體市場可能仍將在中低密度程式碼儲存領域保持強勁勢頭,而非滿足最高容量的影像相關儲存需求。

細分市場分析

到2025年,串列NOR快閃記憶體將佔據家用電子電器NOR快閃記憶體市場80.4%的佔有率,同時也是成長最快的類型,預計到2031年複合年成長率將達到6.7%。這一主導地位反映了消費平台設計在當前SoC藍圖中已徹底從平行記憶體控制器轉向串行配置。串行配置的線路更少,因此更適合緊湊的基板佈局,也更適合智慧音箱、穿戴式裝置、串流媒體設備和連網家庭產品中常見的低電壓工作環境。隨著品牌商對用於大批量產品的更小巧、更低功耗且更易於認證的記憶體解決方案的需求日益成長,這些特性確保了串行NOR快閃消費性電子產品NOR快閃記憶體市場中繼續佔據核心地位。

根據華邦電子2025會計年度財報,快閃記憶體業務將占公司營收的35%,這與串行NOR快閃存在其產品系列中的重要作用以及代碼儲存產品在家用電子電器市場中佔據的舉足輕重地位相符。人工智慧智慧家庭設備的普及,以及韌體不斷擴展語音、視覺和本地處理功能,也推動了這種品類的成長。並行NOR快閃記憶體仍然應用於老式機上盒、固定功能家電和簡單的遙控器設計中,因為在這些應用中重新設計成本較高。然而,隨著新一代半導體不再優先支援平行記憶體,並行NOR快閃記憶體的應用範圍逐漸縮小,這限制了傳統格式在消費性電子NOR快閃記憶體市場的長期生存空間。發展趨勢依然明確:串列產品將繼續佔據大多數現代消費性電子產品設計中的銷售基礎,並引領未來的產品藍圖。

預計到2025年,四路SPI將在消費性電子NOR快閃記憶體市場佔據42.3%的佔有率,並繼續成為眾多中階設備的標準介面。它滿足了智慧型手機、智慧電視、遊戲配件和串流硬體等設備的高吞吐量需求,而單路或雙路SPI則無法做到這一點,同時又避免了全八進制支援帶來的額外高成本和嚴格的設計要求。四路SPI廣泛的控制器相容性降低了OEM廠商的整合風險,並縮短了大批量產品的認證週期。這鞏固了四路SPI作為消費性電子市場NOR快閃記憶體領先介面的地位。

在高效能領域,隨著設備對更快的啟動速度和高階韌體執行速度的需求日益成長,預計到2031年,八進位和xSPI介面的年複合成長率將達到6.9%。 2025年11月,技嘉科技(GigaDevice)發表了GD25NX系列產品,該系列產品採用雙電壓設計,支援200MHz八進位SPI,吞吐量高達400MB/s,程式速度比傳統的1.8V八進位裝置快30%。此外,該產品將1.8V內核與1.2V I/O結合,無需在輕薄穿戴平台中使用外部升壓電路,這對於空間受限的裝置至關重要。雖然單路和雙路SPI介面對於簡單的物聯網節點和基礎消費性電子產品仍然十分重要,但NOR閃光存在家用電子電器市場的成長趨勢正轉向支援更高韌體載入要求和更豐富設備響應速度的介面。隨著產品配置向人工智慧和顯示器密集型平台轉變,Octal 和 xSPI 可能會在新高階設計專案中佔據更大的佔有率。

區域分析

到2025年,亞太地區將佔據消費性電子市場NOR快閃記憶體市場佔有率的52.8%,並將成為成長最快的地區,到2031年複合年成長率將達到7.2%。中國仍然是主要驅動力,擁有全球最大的消費性電子產品組裝基地,並不斷鞏固其作為智慧型手機、真無線耳機、智慧音箱和智慧家居硬體等本土記憶體供應商的地位。台灣正大幅提升晶圓產能和設計深度,華邦電子表示,為滿足閃存需求,其台中工廠的月晶圓開片量計劃在2026年底前提升至5.7萬至5.8萬片。日本憑藉其在高階電子設計和低功耗記憶體方面的專業知識為該地區提供支持,瑞薩電子在其記憶體產品系列組合中重點展示了睡眠電流僅為0.2微安培的串行NOR快閃記憶體解決方案。韓國在旗艦智慧型手機和連網顯示器產品領域繼續發揮至關重要的作用,這些產品中高吞吐量介面和高密度韌體儲存正變得越來越普遍。

北美和歐洲是家用電子電器市場中NOR快閃記憶體需求量第二大的地區,這主要得益於高階設備、遊戲生態系統、智慧家庭硬體和智慧連網家庭安防產品的需求。美國仍然是該地區最大的單一市場,這主要歸功於智慧音箱的高普及率、遊戲主機的更換週期以及連網家庭平台的升級。在歐洲,由於韌體完整性和安全更新能力在連網型設備的設計和規格中越來越受到重視,因此法規對記憶體容量的影響更為顯著。歐盟《網路彈性法案》在這一轉變中發揮了核心作用,它為依賴受管韌體運作的產品引入了更正式的安全框架。

在南美洲、中東和非洲,儘管絕對需求仍然較小,但對價格適中的智慧型手機、具成本效益的串流媒體產品和連接型家電的需求持續成長。巴西在南美洲表現突出,為中端串行NOR快閃記憶體產品提供了穩定的需求基礎,這得益於國內電子產品激勵政策對本地製造和組裝的支持。中階和阿拉伯聯合大公國正透過智慧城市和數位基礎設施計畫推動連網型設備的普及,這些計畫支持安全的消費者閘道和家庭系統。在整個非洲,需求與智慧型手機的普及率和進口/組裝趨勢密切相關,這使得擁有可靠的中等密度組件和長期生命週期支援的成熟供應商佔據優勢。雖然這些地區在家用電子電器市場的NOR快閃記憶體技術領域尚未佔據主導,但它們正在擴大主流密度和電壓標準串列產品的潛在基本客群。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 語音優先的智慧家庭中心數量激增,需要即時啟動韌體。

- 超低功耗穿戴式裝置正在推動對 45nm 以下製程的需求。

- 對聯網電視和遊戲機強制執行安全啟動和OTA更新。

- 中國55/40nm製程的國產化正在推動智慧型手機對中等密度NOR記憶體的需求。

- 四路/八路SPI介面,支援4K相機和無人機的高速發射架構

- 採用 XiP 架構的邊緣 AI 物聯網設備更傾向於使用高密度串列 NOR 記憶體。

- 市場限制因素

- 超過 256Mb 的 NAND 記憶體成本過高,阻礙了高解析度相機的廣泛應用。

- 45 奈米以下的微型化極限正促使 OEM 製造商轉向 MRAM/ReRAM 的替代技術。

- 由於中國產能增加,平均售價(ASP)下降,對供應商的利潤率帶來了壓力。

- 台灣代工廠的集中,為消費性電子產品的供應帶來了風險。

- 產業價值鏈分析

- 宏觀經濟因素對市場的影響

- 監理展望

- 技術展望

- 波特五力分析

- 價格分析

第5章 市場規模與成長預測

- NOR快閃記憶體類型

- 串行 NOR 快閃記憶體

- 並行 NOR 快閃記憶體

- 透過介面

- SPI 單/雙路

- 四路 SPI

- 八進位和xSPI

- 按密度

- 2兆位元或更少

- 2-4兆位元及以上

- 4 到 8 兆位元以上

- 8 至 16 兆位元及以上

- 16-32兆位元及以上

- 32-64兆位元及以上

- 64兆位元及以上至128兆比特

- 超過 128 兆比特到 256 兆比特

- 超過 256 兆比特

- 透過電壓

- 3 V級

- 1.8 V級

- 寬電壓範圍(1.65 至 3.6 V)

- 1.2 V級及以下車型

- 依製程技術節點

- 90奈米或以上

- 65 nm

- 55奈米(包括58奈米)

- 45 nm

- 28奈米或更小

- 按包裝類型

- WLCSP/CSP

- QFN/SOIC

- BGA/FBGA

- 其他包裝類型

- 按地區

- 北美洲

- 美國

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美國家

- 歐洲

- 德國

- 法國

- 英國

- 義大利

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 韓國

- 台灣

- 印度

- 東南亞

- 其他亞太國家

- 中東

- 土耳其

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 其他中東國家

- 非洲

- 南非

- 埃及

- 其他非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Winbond Electronics Corporation

- Macronix International Co. Ltd.

- GigaDevice Semiconductor Inc.

- Micron Technology Inc.

- Infineon Technologies AG

- Microchip Technology Inc.

- Integrated Silicon Solution Inc.

- Renesas Electronics Corporation

- Elite Semiconductor Microelectronics Technology Inc.

- Wuhan XMC

- Puya Semiconductor(Shanghai)Co. Ltd.

- Samsung Electronics Co. Ltd.

- Alliance Memory Inc.

- Zbit Semiconductor Inc.

- Xi'an Longsys Co. Ltd.

- Cypress Semiconductor Corp.

- AMIC Technology Corp.

- Fudan Microelectronics Group Co. Ltd.

- EON Silicon Solution Inc.

- Unigroup Guoxin Microelectronics Co. Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the nOR flash for consumer electronics market size is expected to increase from USD 1.09 billion in 2025 to USD 1.15 billion in 2026 and reach USD 1.48 billion by 2031, growing at a CAGR of 5.20% over 2026-2031.

This report is Segmented by NOR Flash Type (Serial, and Parallel), Density (2 Megabit and Less, and More), Voltage (3V Class, 1. 8V Class, and More), Process Technology Node (55/58 Nm, 65 Nm, and More), Packaging Type (WLCSP/CSP, QFN/SOIC, and More), and Geography (North America, Europe, Asia Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

Global NOR Flash For Consumer Electronics Market Trends and Insights

Edge-AI IoT Appliances Adopting XiP Architecture Favor High-Density Serial NOR

The NOR flash market for consumer electronics is benefiting from a broader base of edge-AI appliances, such as smart displays, ambient computing hubs, and connected home cameras, that require code storage with fast boot performance. These products are moving toward in-place execution of memory because firmware and inference-related functions need to remain accessible without excessive RAM overhead, which makes high-density serial NOR more attractive in the design cycle. The product direction also favors suppliers that can combine higher densities with low-voltage operation and compact footprints for miniaturized consumer hardware. GigaDevice expanded its GD25UF 1.2 V ultra-low-power SPI NOR flash family in March 2026 to cover 8 Mb to 256 Mb densities and positioned the series for AI computing, wearables, hearables, and ASIC-based platforms. That kind of product expansion supports the view that the NOR flash for the consumer electronics market is shifting toward denser serial devices with better power efficiency rather than basic code-storage parts with limited performance headroom.

Proliferation of Voice-First Smart-Home Hubs Requiring Instant-On Firmware

The NOR flash for the consumer electronics market is also supported by voice-first smart-home devices that need local firmware to stay available for near-instant response after wake events. Smart speakers, display hubs, AI doorbells, and smart plugs depend on code storage that can support fast start-up without the longer load sequence associated with other memory types. This demand pattern matters because many brands now manage several assistant ecosystems on related hardware platforms, which raises the amount of firmware support each design must carry. Winbond identified smart home as a key growth area in its investor materials and stated that its F45 nm process improved die-size efficiency for TWS and IoT applications compared with the older F58 nm generation. Winbond also reported that consumer electronics represented 29% of its 2025 application mix, showing that these device categories remain commercially important to the NOR flash for consumer electronics market and to the leading supplier base.

Cost Premium Versus NAND Above 256 Mb Limiting High-Resolution Camera Adoption

The NOR flash for the consumer electronics market still faces a practical density limit in applications where code storage needs move well beyond 256 Mb. High-resolution camera modules in smartphones, action cameras, and home surveillance products can quickly push memory requirements into a range where NAND remains more cost-effective for larger payloads. That cost gap reduces NOR usage in imaging-heavy device designs even when fast boot characteristics still matter at system level. Macronix stated in its 2024 annual report that its 3D NOR development is intended to improve cost and density positioning, and the company discussed sampling in the second half of 2026 with mass production targeted for 2027. Until such products reach broader commercial use, the NOR flash for the consumer electronics market is likely to remain strongest in low to mid-density code storage rather than in the highest-capacity imaging-related memory needs.

Other drivers and restraints analyzed in the detailed report include:

- Secure-Boot and OTA-Update Mandates in Connected TVs and Gaming Consoles

- China's 55 nm and 40 nm Localization Push Supporting Mid-Density NOR for Smartphones

- ASP Compression From Rising Chinese Capacity Pressuring Vendor Margins

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Serial NOR commanded 80.4% of the 2025 NOR flash for the consumer electronics market share and is also the fastest-growing type segment, with a projected 6.7% CAGR through 2031. This lead reflects how completely consumer platform design has moved away from parallel memory controllers in current SoC roadmaps. Serial configurations use fewer traces, fit better into tighter board layouts, and align more closely with the low-voltage operating conditions now common in smart speakers, wearables, streaming devices, and connected home products. These traits keep serial NOR at the center of the NOR flash market for consumer electronics, as brands seek smaller, lower-power, and easier-to-qualify memory solutions for high-volume products.

Winbond's 2025 annual results showed that flash memory accounted for 35% of the company's revenue, consistent with the large role of serial NOR in its portfolio and the weight of code-storage products in consumer electronics demand. The category is also helped by stronger adoption in AI-capable household devices, where firmware is expanding as voice, vision, and local processing features are added. Parallel NOR still serves older set-top boxes, fixed-function appliances, and simple remote-control designs where redesign costs are hard to justify. Even so, that installed base is gradually shrinking because newer silicon generations do not prioritize parallel memory support, which limits the long-term room for legacy formats in the NOR flash for consumer electronics market. The direction of travel remains clear, with serial products carrying both the volume base and the forward product roadmap for most modern consumer device designs.

Quad SPI accounted for 42.3% of the 2025 NOR flash market share in consumer electronics and remained the standard interface for a broad range of mid-range devices. It serves smartphones, smart TVs, gaming accessories, and streaming hardware that require higher throughput than single- or dual-SPI can provide without moving to the higher cost and tighter design requirements of full Octal support. The wide controller compatibility of Quad SPI reduces integration risk for OEMs and helps shorten qualification cycles in products with large annual volumes. This keeps Quad SPI firmly positioned as the workhorse interface across the NOR flash for the consumer electronics market.

At the performance end, Octal and xSPI are forecast to grow at a 6.9% CAGR through 2031 as devices demand faster boot times and higher execution speeds for advanced firmware. GigaDevice launched the GD25NX series in November 2025 with a dual-voltage design, 200 MHz Octal SPI support, throughput up to 400 MB/s, and a stated 30% faster program speed than conventional 1.8 V Octal devices. The product also eliminated the need for an external boost circuit in thin wearable platforms by pairing a 1.8 V core with 1.2 V I/O, which is important in space-limited devices. Single and dual SPI still matter in simpler IoT nodes and basic appliances, but the growth path in the NOR flash for consumer electronics market is moving toward interfaces that support more demanding firmware loads and richer device responsiveness. As the product mix shifts toward AI-enabled and display-heavy platforms, Octal and xSPI should take a larger share of new premium design wins.

Geography Analysis

Asia-Pacific accounted for 52.8% of NOR flash market share in the consumer electronics market in 2025 and is also the fastest-growing regional block, with a 7.2% CAGR through 2031. China remains the main anchor because it combines the largest consumer electronics assembly base with a growing domestic memory supply position in smartphones, TWS devices, smart speakers, and smart-home hardware. Taiwan adds major wafer capacity and design depth, and Winbond said its Taichung site is moving toward 57,000 to 58,000 monthly wafer starts by late 2026 to support flash demand. Japan supports the region through premium electronics design and low-power memory know-how, while Renesas has highlighted serial NOR solutions with sleep current as low as 0.2 µA in its memory portfolio materials. South Korea remains important in flagship smartphones and connected display products, where higher-throughput interfaces and denser firmware storage are more common.

North America and Europe formed the second-largest demand cluster in the NOR flash for consumer electronics market, driven by premium device demand, gaming ecosystems, smart-home hardware, and connected home security products. The United States remains the largest single-country market in this group because of strong smart-speaker penetration, console refresh cycles, and connected-home platform upgrades. Europe has a stronger regulatory impact on memory content because firmware integrity and secure update capabilities carry greater weight in connected device design and documentation. The EU Cyber Resilience Act is central to that shift because it brings a more formal security framework to products that rely on managed firmware behavior.

South America, the Middle East, and Africa remained smaller in absolute demand, but they continue to add volume in affordable smartphones, value-tier streaming products, and connected appliances. Brazil stands out in South America because domestic electronics incentives support local manufacturing and assembly, providing a stable demand base for mid-range serial NOR products. Saudi Arabia and the United Arab Emirates are strengthening connected-device use through smart-city and digital infrastructure programs that support secure consumer gateways and home systems. Across Africa, demand tracks smartphone adoption and import assembly patterns, which favor established suppliers offering reliable mid-density parts with long lifecycle support. These regions do not yet set the technology pace for NOR flash in the consumer electronics market, but they do expand the addressable customer base for standard-serial products at mainstream density and voltage points.

- Winbond Electronics Corporation

- Macronix International Co. Ltd.

- GigaDevice Semiconductor Inc.

- Micron Technology Inc.

- Infineon Technologies AG

- Microchip Technology Inc.

- Integrated Silicon Solution Inc.

- Renesas Electronics Corporation

- Elite Semiconductor Microelectronics Technology Inc.

- Wuhan XMC

- Puya Semiconductor (Shanghai) Co. Ltd.

- Samsung Electronics Co. Ltd.

- Alliance Memory Inc.

- Zbit Semiconductor Inc.

- Xi'an Longsys Co. Ltd.

- Cypress Semiconductor Corp.

- AMIC Technology Corp.

- Fudan Microelectronics Group Co. Ltd.

- EON Silicon Solution Inc.

- Unigroup Guoxin Microelectronics Co. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions And Market Definition

- 1.2 Scope Of The Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Proliferation Of Voice-First Smart-Home Hubs Requiring Instant-On Firmware

- 4.2.2 Ultra-Low-Power Wearables Driving Sub-45 nm Demand

- 4.2.3 Secure-Boot And OTA-Update Mandates In Connected TVs And Gaming Consoles

- 4.2.4 China's 55/40 nm Localization Push Boosting Mid-Density NOR For Smartphones

- 4.2.5 Quad/Octal SPI Interfaces Enabling 4K Camera And Drone Fast-Boot Architectures

- 4.2.6 Edge-AI IoT Appliances Adopting XiP Architecture Favouring Hi-Density Serial NOR

- 4.3 Market Restraints

- 4.3.1 Cost Premium Vs NAND Above 256 Mb Limiting Hi-Resolution Camera Adoption

- 4.3.2 Scaling Ceilings Beyond 45 nm Steering OEMs Toward MRAM/ReRAM Alternatives

- 4.3.3 ASP Compression From Rising Chinese Capacity Pressuring Vendor Margins

- 4.3.4 Foundry Concentration In Taiwan Exposing Consumer-Device Supply Risk

- 4.4 Industry Value Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Outlook

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitute Products

- 4.8.5 Intensity of Competitive Rivalry

- 4.9 Pricing Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 By NOR Flash Type (Value And Volume)

- 5.1.1 Serial NOR Flash

- 5.1.2 Parallel NOR Flash

- 5.2 By Interface (Value)

- 5.2.1 SPI Single / Dual

- 5.2.2 Quad SPI

- 5.2.3 Octal And xSPI

- 5.3 By Density (Value)

- 5.3.1 2 Megabit and Less

- 5.3.2 More than 2 to 4 Megabit

- 5.3.3 More than 4 to 8 Megabit

- 5.3.4 More than 8 to 16 Megabit

- 5.3.5 More than 16 to 32 Megabit

- 5.3.6 More than 32 to 64 Megabit

- 5.3.7 More than 64 to 128 Megabit

- 5.3.8 More than 128 to 256 Megabit

- 5.3.9 More than 256 Megabit

- 5.4 By Voltage (Value)

- 5.4.1 3 V Class

- 5.4.2 1.8 V Class

- 5.4.3 Wide-Voltage (1.65-3.6 V)

- 5.4.4 <=1.2 V Class

- 5.5 By Process Technology Node (Value)

- 5.5.1 90 nm and More

- 5.5.2 65 nm

- 5.5.3 55 nm (Incl. 58 nm)

- 5.5.4 45 nm

- 5.5.5 28 nm and Below

- 5.6 By Packaging Type (Value)

- 5.6.1 WLCSP / CSP

- 5.6.2 QFN / SOIC

- 5.6.3 BGA / FBGA

- 5.6.4 Other Packaging Types

- 5.7 By Geography (Value And Volume)

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 South America

- 5.7.2.1 Brazil

- 5.7.2.2 Argentina

- 5.7.2.3 Rest Of South America

- 5.7.3 Europe

- 5.7.3.1 Germany

- 5.7.3.2 France

- 5.7.3.3 United Kingdom

- 5.7.3.4 Italy

- 5.7.3.5 Russia

- 5.7.3.6 Rest of Europe

- 5.7.4 Asia-Pacific

- 5.7.4.1 China

- 5.7.4.2 Japan

- 5.7.4.3 South Korea

- 5.7.4.4 Taiwan

- 5.7.4.5 India

- 5.7.4.6 Southeast Asia

- 5.7.4.7 Rest of Asia-Pacific

- 5.7.5 Middle East

- 5.7.5.1 Turkey

- 5.7.5.2 Saudi Arabia

- 5.7.5.3 United Arab Emirates

- 5.7.5.4 Rest of Middle East

- 5.7.6 Africa

- 5.7.6.1 South Africa

- 5.7.6.2 Egypt

- 5.7.6.3 Rest of Africa

- 5.7.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials As Available, Strategic Information, Market Rank/Share, Products And Services, Recent Developments)

- 6.4.1 Winbond Electronics Corporation

- 6.4.2 Macronix International Co. Ltd.

- 6.4.3 GigaDevice Semiconductor Inc.

- 6.4.4 Micron Technology Inc.

- 6.4.5 Infineon Technologies AG

- 6.4.6 Microchip Technology Inc.

- 6.4.7 Integrated Silicon Solution Inc.

- 6.4.8 Renesas Electronics Corporation

- 6.4.9 Elite Semiconductor Microelectronics Technology Inc.

- 6.4.10 Wuhan XMC

- 6.4.11 Puya Semiconductor (Shanghai) Co. Ltd.

- 6.4.12 Samsung Electronics Co. Ltd.

- 6.4.13 Alliance Memory Inc.

- 6.4.14 Zbit Semiconductor Inc.

- 6.4.15 Xi'an Longsys Co. Ltd.

- 6.4.16 Cypress Semiconductor Corp.

- 6.4.17 AMIC Technology Corp.

- 6.4.18 Fudan Microelectronics Group Co. Ltd.

- 6.4.19 EON Silicon Solution Inc.

- 6.4.20 Unigroup Guoxin Microelectronics Co. Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet Need Analysis

2026年全球金屬氧化物半導體(MOS)微處理器市場報告2026年全球金屬氧化物半導體(MOS)標準單元和現場可程式邏輯市場報告

2026年全球金屬氧化物半導體(MOS)微處理器市場報告2026年全球金屬氧化物半導體(MOS)標準單元和現場可程式邏輯市場報告 工業級NOR快閃記憶體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)日本NOR快閃記憶體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)義大利 NOR Flash:市場佔有率分析、產業趨勢與統計資料、成長預測(2026-2031 年)

工業級NOR快閃記憶體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)日本NOR快閃記憶體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)義大利 NOR Flash:市場佔有率分析、產業趨勢與統計資料、成長預測(2026-2031 年) 人工智慧記憶體市場預測至2034年—按記憶體類型、組件、部署模式、技術、應用和地區分類的全球分析2026年全球快閃記憶體市場報告2026年全球金屬氧化物半導體(MOS)記憶體市場報告

人工智慧記憶體市場預測至2034年—按記憶體類型、組件、部署模式、技術、應用和地區分類的全球分析2026年全球快閃記憶體市場報告2026年全球金屬氧化物半導體(MOS)記憶體市場報告 快閃記憶體市場:按類型、單元結構和地區分類2026年全球存取記憶體和顯示器市場報告

快閃記憶體市場:按類型、單元結構和地區分類2026年全球存取記憶體和顯示器市場報告