|

市場調查報告書

商品編碼

2061785

日本NOR快閃記憶體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)Japan NOR Flash - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

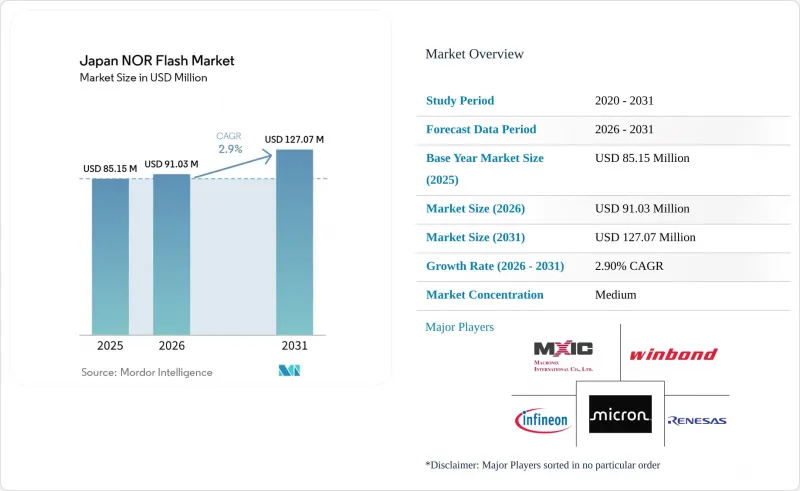

根據 Mordor Intelligence 預測,到 2031 年,日本 NOR 快閃記憶體市場規模預計將達到 1.2707 億美元,高於 2026 年的 9,103 萬美元,預計 2026 年至 2031 年的複合年成長率將達到 2.90%。

本報告按類型(例如,串行NOR快閃記憶體)、介面(例如,SPI單/雙介面)、容量(例如,小於2兆位元)、電壓(例如,3V級、1.8V級)、最終用戶應用(例如,家用電子電器)、製程節點(例如,90nm之前、55nm)、封裝類型(例如,WLCSP/CSP)和地區進行細分。市場預測以美元(USD)計價。

日本NOR快閃記憶體市場的趨勢與洞察

汽車ECU中嵌入式NOR快閃記憶體的廣泛應用

日本汽車製造商正將多個控制域整合到基於區域的架構中,並依靠高密度NOR快閃記憶體來實現亞秒啟動時間和空中韌體更新。英飛凌的ASIL-D認證SEMPER系列、技嘉的GD25/55系列以及宏碁的400MB/s八核心產品均通過了汽車安全標準認證,為一級供應商提供認證的建造模組。隨著電動車產量的不斷成長和ADAS法規的日益嚴格,韌體鏡像體積越來越大,儘管ECU數量有所減少,但每輛車所需的NOR快閃記憶體容量卻在增加。斯巴魯的2026平台採用了英飛凌的AURIX微控制器,正是這項變化的象徵,並加強了日本NOR快閃記憶體市場與國內汽車生產之間的連結。

工業自動化領域對高可靠性記憶體的需求

「工業5.0」正在推動工廠的物理資訊整合,日本經濟產業省已撥款295億日圓(約1.9億美元)用於研發邊緣人工智慧半導體,這些半導體旨在實現即時啟動並能承受嚴苛的工廠環境。這些技術進步至關重要,因為運行在專用5G網路上的控制器需要確定性的啟動能力。 NOR快閃記憶體因其「原地運行」功能而成為最佳選擇,該功能消除了NAND快閃記憶體陰影造成的延遲。為了滿足這項需求,供應商正在認證具有更寬溫度範圍和增強型糾錯碼的產品。這種使產品藍圖與日本自動化產業叢集保持一致的舉措,正在促進創新並支持日本先進製造業的發展。

向 28 奈米及更小過程的轉型需要大量資金投入。

將嵌入式NOR快閃記憶體遷移到更先進的製程節點可以降低每位元成本,但這需要昂貴的製造設備。雖然SST和UMC的28nm SuperFlash已經證明了其技術可行性,但由於日本的晶圓廠成本高於台灣和中國大陸,許多國內生產線仍然運作40-55nm製程。由於政府資金主要集中在邏輯半導體而非成熟的NOR快閃記憶體上,供應商被迫要麼接受較低的利潤率,要麼將生產外包,導致日本NOR快閃記憶體市場獲得經濟高效產能的速度放緩。

細分市場分析

預計到2025年,串列裝置將佔據日本NOR快閃記憶體市場77.81%的主導地位。這項優勢源自於其引腳數量更少、尺寸更小,使其成為ECU和物聯網闆卡等空間受限應用的理想選擇。這些裝置受益於技術進步,包括密度持續提升和八進位/xSPI模式的採用,在不增加成本的情況下實現了與平行NOR快閃記憶體相當的吞吐量。這種性能與成本效益的完美結合鞏固了其作為市場領導者的地位。此外,它們能夠滿足現代應用不斷變化的需求,確保了其持續的重要性。因此,預計串列裝置將在日本NOR快閃記憶體市場保持主導地位直至2031年。

同時,並行NOR記憶體仍然被眾多忠實基本客群用於傳統的工業控制器和航太系統。這些系統依賴專為16位元或32位元匯流排設計的微控制器,因此如果不進行重大改造,它們就無法與新技術相容。遷移這些平台需要大規模的PCB重新設計和重新認證流程,這既耗時又昂貴。因此,使用者通常選擇保留這些系統,從而確保了該細分市場在市場上的持續存在。儘管並行NOR記憶體目前處於小眾市場,但由於其在支援舊有應用程式發揮著至關重要的作用,預計其成長率將達到3.26%。這種穩定的需求凸顯了它在特定工業和航太應用場景中的重要性。

四路SPI介面佔總銷售額的49.12%,在主流設計中實現了成本與速度的平衡。其廣泛應用源自於它能夠在不顯著增加成本的情況下滿足各種應用的性能需求。同時,八路/xSPI介面的複合年成長率高達4.62%,成為日本NOR快閃記憶體市場成長最快的細分市場。這一成長主要歸功於其超過400 MB/s的卓越頻寬。如此高的頻寬使得多核心ADAS處理器能夠在不到一秒的時間內完成點火器準備,這對於2026年汽車專案而言至關重要。對先進汽車系統日益成長的需求進一步推動了八路/xSPI介面的普及。

單雙SPI介面適用於對價格敏感的穿戴式裝置和智慧家庭感測器,這些裝置運作頻率低,資料傳輸量適中。這些介面尤其適合那些成本效益優先於高效能的應用。它們的簡潔性和低功耗使其成為功能有限且間歇性使用設備的理想選擇。儘管其他介面取得了進步,但在控制組件成本至關重要的場景中,單雙SPI介面仍將繼續蓬勃發展。它們在市場上的持久存在凸顯了特定應用情境下對具成本效益解決方案的持續需求。因此,它們仍然是NOR快閃記憶體市場生態系統的重要組成部分。

至2025年,記憶體容量為64Mb或以下的設備將佔總銷售量的26.14%,主要用於穿戴式電子產品和傳統工廠節點。這些設備在注重成本效益和基本功能的應用中仍將發揮至關重要的作用。然而,技術進步正在提高某些應用的記憶體需求。 ADAS網域控制器、OLED時序控制器和開放式RAN無線裝置現在需要雙鏡像來實現故障安全更新,這實際上使其記憶體需求加倍。這種轉變正在推動高容量記憶體(尤其是256Mb以上的記憶體)的普及。高容量記憶體正以5.93%的速度成長,顯著促進了日本NOR快閃記憶體市場的成長,尤其是在高級產品領域。

雖然像 2MB 這樣的小容量記憶體仍然適用於超低成本標籤和基礎感測器,但其應用正在逐步擴展。邊緣人工智慧技術的普及推動了對更高級功能的需求,即使在注重成本的設計中也是如此。因此,這些設計預計將遷移到 4MB 記憶體,以整合推理庫並支援人工智慧驅動的功能。這種轉變凸顯了各種應用對更高儲存容量日益成長的需求。雖然這一過渡可能需要時間,但這種趨勢表明,記憶體在實現更智慧、更有效率的裝置方面的重要性日益凸顯。小容量記憶體的這種演變反映了塑造 NOR 快閃記憶體市場的更廣泛的技術進步。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 日本ADAS和電動車的發展推動了嵌入式NOR閃光存在汽車ECU中的廣泛應用。

- 社會5.0計劃中對工業自動化高可靠性記憶體的需求日益成長

- 從 LCD 到 OLED 和 MicroLED 面板的過渡需要高密度 NOR 記憶體用於時序控制器。

- 5G 基地台和 O-RAN 硬體的擴充需要高速啟動程式碼儲存。

- 基於經濟產業省韌性計畫的半導體供應鏈國產化

- 人工智慧邊緣設備的興起需要能夠即時在惡劣環境下啟動的程式碼儲存。

- 市場限制因素

- 在日本高成本的晶圓廠環境中,向28奈米及更低製程節點的轉型需要大量資金投入。

- SLC NAND 作為低成本替代方案在家用電子電器。

- 國內光刻能力的不足限制了 NOR(自然取向紅)光刻技術的大規模生產。

- 日圓匯率波動推高了進口光阻劑和設備的成本。

- 產業價值/價值鏈分析

- 技術展望

- 監理情勢

- 波特五力分析

- 價格分析

- 宏觀經濟因素對市場的影響

- 投資分析

第5章 市場規模與成長預測

- NOR快閃記憶體類型

- 串行 NOR 快閃記憶體

- 並行 NOR 快閃記憶體

- 透過介面

- SPI 單/雙路

- 四路 SPI

- 八進位和xSPI

- 按密度

- 2兆位元或更少

- 4兆位元或更少(大於2兆位元)

- 8兆位元或更少(大於4兆位元)

- 16兆位元或更少(大於8兆位元)

- 32兆位元或更少(超過16兆位元)

- 64兆位元或更少(超過32兆位元)

- 128兆位元或更少(超過64兆位元)

- 256兆位元或更少(超過128兆位元)

- 超過 256 兆比特

- 透過電壓

- 3 V級

- 1.8 V級

- 寬電壓範圍(1.65V 至 3.6V)

- 低於 1.8 V 等級(1.2 V 及同等等級)

- 透過最終用戶應用程式

- 家用電子產品

- 通訊基礎設施

- 車

- 產業

- 其他用途

- 依製程技術節點

- 90奈米及更早

- 65 nm

- 55 nm

- 45 nm

- 28奈米或更小

- 按包裝類型

- WLCSP/CSP

- QFN/SOIC

- BGA/FBGA

- 其他包裝類型

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- Vendor Positioning Analysis

- 公司簡介

- Infineon Technologies AG

- Winbond Electronics Corporation

- Renesas Electronics Corporation

- Macronix International Co., Ltd.

- Micron Technology Inc.

- GigaDevice Semiconductor Inc.

- Integrated Silicon Solution Inc.

- Microchip Technology Inc.

- Elite Semiconductor Microelectronics Technology Inc.

- Wuhan Xinxin Semiconductor Manufacturing Co. Ltd

- Puya Semiconductor(Shanghai)Co., Ltd.

- Fudan Microelectronics Group

- Cypress Semiconductor Corporation

- Rohm Co., Ltd.

- Dialog Semiconductor Plc

- Etron Technology Inc.

- Tower Semiconductor Ltd.

- SkyHigh Memory Limited

- Longsys Electronics Co., Ltd.

- Spansion LLC

第7章 市場機會與未來展望

According to Mordor Intelligence, the japan nOR flash market size is expected to increase from USD 91.03 million in 2026 to reach USD 127.07 million by 2031, growing at a CAGR of 2.90% over 2026-2031.

This report is Segmented by Type (Serial NOR Flash, and More), Interface (SPI Single/Dual, and More), Density (2 Megabit and Less, and More), Voltage (3 V Class, 1. 8 V Class and More), End-User Application (Consumer Electronics, and More), Process Technology Node (90 Nm and Older, 55 Nm, and More), Packaging Type (WLCSP/CSP, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Japan NOR Flash Market Trends and Insights

Proliferation of Embedded NOR Flash in Automotive ECUs

Japanese vehicle makers are consolidating multiple control domains into zonal architectures that rely on high-density NOR Flash for sub-second boot times and firmware-over-the-air updates. Infineon's ASIL-D-certified SEMPER family, GigaDevice's GD25/55 line, and Macronix's 400 MB/s Octal part all received automotive safety nods, giving tier-1 suppliers certified building blocks. Growing electric-vehicle output and stricter ADAS mandates enlarge firmware images, so each car now embeds more NOR bits even as ECU counts decline. Subaru's 2026 platform using Infineon AURIX microcontrollers exemplifies this shift, reinforcing the Japan NOR Flash market's link to domestic auto production.

Demand for High-Reliability Memory in Industrial Automation

Society 5.0 is driving factories toward cyber-physical convergence, with METI allocating JPY 29.5 billion (USD 0.19 billion) for edge-AI semiconductors designed to boot instantly and withstand extreme factory conditions. These advancements are critical as controllers operating on private 5G networks require deterministic start-up capabilities. NOR flash memory, with its execute-in-place feature, eliminates the latency associated with NAND shadowing, making it a preferred choice. To meet these demands, suppliers are qualifying products with wider temperature ranges and enhanced error-correction codes. This alignment of product roadmaps with Japanese automation clusters is fostering innovation and supporting the country's push toward advanced manufacturing.

Capital-Intensive Migration to 28 nm and Below Nodes

Moving embedded NOR to advanced nodes reduces cost per bit but demands expensive tooling. SST and UMC's 28 nm SuperFlash proves technical feasibility, yet most domestic lines still run 40-55 nm because Japan's fab costs outpace Taiwan and China. Government funds target logic rather than mature NOR, so suppliers must either absorb lower margins or outsource, dampening the pace at which the Japan NOR Flash market accesses cost-efficient capacity.

Other drivers and restraints analyzed in the detailed report include:

- Transition From LCD to OLED and MicroLED Panels

- Expansion of 5G Base Stations and O-RAN Hardware

- Growing Adoption of SLC NAND as a Substitute

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, serial devices captured a commanding 77.81% share of Japan's NOR Flash market. Their dominance is attributed to their lower pin count and compact footprints, which make them highly suitable for space-constrained applications such as ECUs and IoT boards. These devices benefit from advancements like continued density scaling and the adoption of Octal/xSPI modes, enabling them to achieve throughput levels comparable to parallel NOR without increasing costs. This combination of performance and cost-efficiency has solidified their position as the preferred choice in the market. Furthermore, their ability to meet the evolving demands of modern applications ensures their sustained relevance. Consequently, serial devices are expected to maintain their leadership in Japan's NOR Flash market through 2031.

Meanwhile, parallel NOR continues to serve a loyal customer base in legacy industrial controllers and aerospace systems. These systems rely on microcontrollers specifically designed for 16- or 32-bit buses, making them incompatible with newer technologies without significant modifications. Transitioning these platforms would require extensive PCB redesigns and recertification processes, which are both time-consuming and costly. As a result, users often opt to retain these systems, ensuring the segment's continued presence in the market. Despite its niche status, parallel NOR is projected to achieve a respectable 3.26% growth rate, driven by its critical role in supporting legacy applications. This steady demand underscores its importance in specific industrial and aerospace use cases.

Quad SPI, accounting for 49.12% of revenue, strikes a balance between cost and speed for mainstream designs. Its widespread adoption is driven by its ability to meet the performance requirements of various applications without significantly increasing costs. On the other hand, the Octal/xSPI segment is emerging as the fastest-growing player in Japan's NOR Flash market, boasting a 4.62% CAGR. This growth is attributed to its superior bandwidth capabilities, which exceed 400 MB/s. Such high bandwidth enables multi-core ADAS processors to achieve sub-second ignition readiness, a critical requirement for 2026 vehicle programs. The increasing demand for advanced automotive systems further fuels the adoption of Octal/xSPI interfaces.

Single and Dual SPI cater to price-sensitive wearables and smart-home sensors, which boot infrequently and handle modest data transmissions. These interfaces are particularly suited for applications where cost efficiency is a priority over high performance. Their simplicity and low power consumption make them ideal for devices with limited functionality and intermittent usage. Despite advancements in other interfaces, Single and Dual SPI will continue to thrive in scenarios where controlling the bill of materials takes precedence. Their persistence in the market highlights the ongoing demand for cost-effective solutions in specific use cases. As a result, they remain a vital part of the NOR Flash market ecosystem.

In 2025, devices with 64 Mb memory and below accounted for 26.14% of sales, primarily in body electronics and traditional factory nodes. These devices continue to play a significant role in applications where cost efficiency and basic functionality are prioritized. However, advancements in technology have led to increased memory requirements in certain applications. ADAS domain controllers, OLED timing-controllers, and Open RAN radios now demand dual images for failsafe updates, effectively doubling their memory needs. This shift has driven the adoption of higher memory densities, particularly those exceeding 256 Mb. These higher densities are expanding at a rate of 5.93%, significantly contributing to the growth of Japan's NOR Flash market, especially in premium product segments.

While lower memory ranges, like 2 Mb, still cater to ultra-low-cost tags and basic sensors, their applications are gradually evolving. The proliferation of edge-AI technologies is driving a need for more advanced capabilities even in cost-sensitive designs. As a result, these designs are expected to transition to 4 Mb memory to accommodate inference libraries and support AI-driven functionalities. This shift highlights the growing demand for higher memory capacities across various applications. Although the transition may take time, the trend underscores the increasing importance of memory in enabling smarter and more efficient devices. The evolution of these lower ranges reflects the broader technological advancements shaping the NOR Flash market.

List of Companies Covered in this Report:

- Infineon Technologies AG

- Winbond Electronics Corporation

- Renesas Electronics Corporation

- Macronix International Co., Ltd.

- Micron Technology Inc.

- GigaDevice Semiconductor Inc.

- Integrated Silicon Solution Inc.

- Microchip Technology Inc.

- Elite Semiconductor Microelectronics Technology Inc.

- Wuhan Xinxin Semiconductor Manufacturing Co. Ltd

- Puya Semiconductor (Shanghai) Co., Ltd.

- Fudan Microelectronics Group

- Cypress Semiconductor Corporation

- Rohm Co., Ltd.

- Dialog Semiconductor Plc

- Etron Technology Inc.

- Tower Semiconductor Ltd.

- SkyHigh Memory Limited

- Longsys Electronics Co., Ltd.

- Spansion LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Proliferation of Embedded NOR Flash in Automotive ECUs Driven by Japan's ADAS and EV Growth

- 4.2.2 Demand for High-Reliability Memory in Industrial Automation Amid Society 5.0 Initiatives

- 4.2.3 Transition from LCD to OLED and MicroLED Panels Requiring Higher-Density NOR for Timing Controllers

- 4.2.4 Expansion of 5G Base Stations and O-RAN Hardware Requiring Fast Boot-Code Storage

- 4.2.5 Localization of Semiconductor Supply Chain Under METI Resilience Programs

- 4.2.6 Emergence of AI Edge Devices Demanding Instant-On Code Storage in Harsh Environments

- 4.3 Market Restraints

- 4.3.1 Capital-Intensive Migration to 28 nm and Below Nodes in Japan's High-Cost Fab Environment

- 4.3.2 Growing Adoption of SLC NAND as a Lower-Cost Substitute in Consumer Electronics

- 4.3.3 Limited Domestic Lithography Capacity Constraining High-Volume NOR Production

- 4.3.4 Yen Volatility Inflating Imported Photoresist and Equipment Costs

- 4.4 Industry Value / Supply-Chain Analysis

- 4.5 Technological Outlook

- 4.6 Regulatory Landscape

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Pricing Analysis

- 4.9 Impact of Macroeconomic Factors on the Market

- 4.10 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE, VOLUME)

- 5.1 By NOR Flash Type (Value)

- 5.1.1 Serial NOR Flash

- 5.1.2 Parallel NOR Flash

- 5.2 By Interface (Value)

- 5.2.1 SPI Single / Dual

- 5.2.2 Quad SPI

- 5.2.3 Octal and xSPI

- 5.3 By Density (Value)

- 5.3.1 2 Megabit and Less

- 5.3.2 4 Megabit and Less (Greater than 2 Mb)

- 5.3.3 8 Megabit and Less (Greater than 4 Mb)

- 5.3.4 16 Megabit and Less (Greater than 8 Mb)

- 5.3.5 32 Megabit and Less (Greater than 16 Mb)

- 5.3.6 64 Megabit and Less (Greater than 32 Mb)

- 5.3.7 128 Megabit and Less (Greater than 64 Mb)

- 5.3.8 256 Megabit and Less (Greater than 128 Mb)

- 5.3.9 Greater than 256 Megabit

- 5.4 By Voltage (Value)

- 5.4.1 3 V Class

- 5.4.2 1.8 V Class

- 5.4.3 Wide-Voltage (1.65 V - 3.6 V)

- 5.4.4 Sub-1.8 V Class (1.2 V and Similar)

- 5.5 By End-User Application (Value, Volume)

- 5.5.1 Consumer Electronics

- 5.5.2 Communication Infrastructure

- 5.5.3 Automotive

- 5.5.4 Industrial

- 5.5.5 Other Applications

- 5.6 By Process Technology Node (Value)

- 5.6.1 90 nm and Older

- 5.6.2 65 nm

- 5.6.3 55 nm

- 5.6.4 45 nm

- 5.6.5 28 nm and Below

- 5.7 By Packaging Type (Value)

- 5.7.1 WLCSP / CSP

- 5.7.2 QFN / SOIC

- 5.7.3 BGA / FBGA

- 5.7.4 Other Packaging Types

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Vendor Positioning Analysis

- 6.5 Company Profiles

- 6.5.1 Infineon Technologies AG

- 6.5.2 Winbond Electronics Corporation

- 6.5.3 Renesas Electronics Corporation

- 6.5.4 Macronix International Co., Ltd.

- 6.5.5 Micron Technology Inc.

- 6.5.6 GigaDevice Semiconductor Inc.

- 6.5.7 Integrated Silicon Solution Inc.

- 6.5.8 Microchip Technology Inc.

- 6.5.9 Elite Semiconductor Microelectronics Technology Inc.

- 6.5.10 Wuhan Xinxin Semiconductor Manufacturing Co. Ltd

- 6.5.11 Puya Semiconductor (Shanghai) Co., Ltd.

- 6.5.12 Fudan Microelectronics Group

- 6.5.13 Cypress Semiconductor Corporation

- 6.5.14 Rohm Co., Ltd.

- 6.5.15 Dialog Semiconductor Plc

- 6.5.16 Etron Technology Inc.

- 6.5.17 Tower Semiconductor Ltd.

- 6.5.18 SkyHigh Memory Limited

- 6.5.19 Longsys Electronics Co., Ltd.

- 6.5.20 Spansion LLC

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

2026年全球金屬氧化物半導體(MOS)微處理器市場報告2026年全球金屬氧化物半導體(MOS)標準單元和現場可程式邏輯市場報告

2026年全球金屬氧化物半導體(MOS)微處理器市場報告2026年全球金屬氧化物半導體(MOS)標準單元和現場可程式邏輯市場報告 工業級NOR快閃記憶體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年)

工業級NOR快閃記憶體:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031年) 人工智慧記憶體市場預測至2034年—按記憶體類型、組件、部署模式、技術、應用和地區分類的全球分析2026年全球快閃記憶體市場報告2026年全球金屬氧化物半導體(MOS)記憶體市場報告

人工智慧記憶體市場預測至2034年—按記憶體類型、組件、部署模式、技術、應用和地區分類的全球分析2026年全球快閃記憶體市場報告2026年全球金屬氧化物半導體(MOS)記憶體市場報告 快閃記憶體市場:按類型、單元結構和地區分類2026年全球存取記憶體和顯示器市場報告

快閃記憶體市場:按類型、單元結構和地區分類2026年全球存取記憶體和顯示器市場報告 快閃記憶體控制器市場按NAND類型、介面類型、外形規格、應用和最終用戶分類,全球預測(2026-2032年)

快閃記憶體控制器市場按NAND類型、介面類型、外形規格、應用和最終用戶分類,全球預測(2026-2032年) NOR快閃記憶體市場分析及預測(至2035年):依類型、產品類型、技術、應用、設備、最終用戶、組件、製程、部署類型及功能分類

NOR快閃記憶體市場分析及預測(至2035年):依類型、產品類型、技術、應用、設備、最終用戶、組件、製程、部署類型及功能分類