|

市場調查報告書

商品編碼

2061629

電動汽車增程器:市場佔有率分析、產業趨勢與統計及成長預測(2026-2031 年)Electric Vehicle Range Extender - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

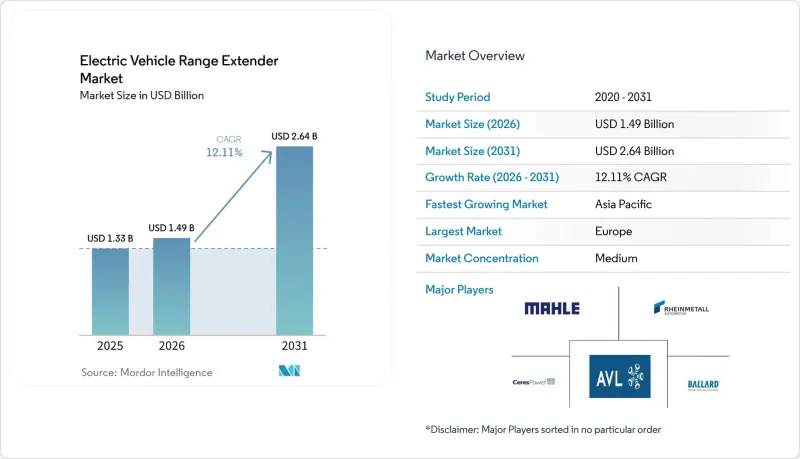

根據 Mordor Intelligence 預測,電動車增程器的市場規模預計將從 2025 年的 13.3 億美元成長到 2026 年的 14.9 億美元,到 2031 年將達到 26.4 億美元,2026 年至 2031 年的複合年成長率為 12.1%。

本報告按類型(內燃機和燃料電池增程器、固體氧化物燃料電池增程器等)、組件(電池組、馬達、發電機等)、車輛類型(乘用車和輕型商用車等)、功率輸出(30kW以下和30-60kW等)以及地區進行細分。市場預測以價值(美元)和銷售(台)兩種形式呈現。

全球電動汽車增程器市場趨勢與洞察

政府的零排放法規正在加速整車製造商的需求。

監管壓力正迫使動力傳動系統藍圖重新評估,加速電動車增程器市場的成長。 2024年生效的歐盟7排放標準要求重型卡車的氮氧化物排放減少50%,迫使製造商迅速轉型為混合動力。加州的「先進清潔汽車II」計畫要求到2035年,所有銷售的車輛都必須是零排放車輛;華盛頓州也採用了類似的標準,允許汽車製造商透過增程器車型獲得合規積分。美國環保署(EPA)提出的2027-2032年法規要求將車隊的平均二氧化碳排放減少到每英里82克,隨著公共充電基礎設施的不斷完善,增程器正成為一種切實可行的選擇。汽車製造商目前正優先考慮可擴展的架構,以同時滿足純電動車和增程器車型的需求,從而確保在全球市場的柔軟性。

電池價格下降使得經濟高效的混合動力架構成為可能。

鋰離子電池成本降至每千瓦時139美元,降低了整體系統成本,使汽車製造商能夠在不超出成本目標的前提下,將緊湊型電池組與輔助發電機結合。向磷酸鐵鋰電池的轉變進一步降低了成本,尤其是在商用車領域,因為在這些領域,電池循環壽命比續航里程更為重要。電動車增程器市場也受惠於美國的《通貨膨脹控制法案》和歐盟的投資計劃,這些計劃正在加速電池生產的在地化,降低物流成本,並鼓勵採用整合式增程器生產線。 EUROBAT預測,到2035年,歐洲對鋰電池的需求將成長八倍,這將進一步增強有利於混合動力佈局的規模經濟效益。

快速充電網路的擴展減少了對增程器的需求。

美國電氣化組織(Electrify America)計畫在2024年將充電網路擴大25%,並安裝5,000個高功率充電站,以縮短平均充電時間。美國國家電動車基礎設施計畫(NEVI)計畫在2028年投資50億美元,安裝50萬個公共充電樁,其中僅加州就計畫在2030年安裝3.9萬個直流快速充電樁。隨著充電網路的發展,純電動車的實用性日益增強,對輔助發電機的需求也在一定程度上下降,但農村貨運仍面臨充電基礎設施短缺的問題。

細分市場分析

到2025年,內燃機增程器在電動車增程器市場仍將佔66.72%的佔有率。這是因為汽車製造商可以沿用小型汽油和燃氣引擎成熟的供應鏈。該平台與現有的廢氣後處理系統、診斷工具和生產線相容,從而縮短了開發週期。然而,燃料電池增程器正以22.05%的複合年成長率快速發展,並成為高效能商用車產品藍圖的核心,這些商用車必須在其所在地區實現零排放。 Ceres Power和瀟柴動力的固體氧化物燃料電池堆在穩定負載下可實現高電效率,使其適用於城市公車和貨車。

固體氧化物燃料電池系統支援多種燃料,例如氫氣、甲烷和氨氣,隨著氫氣供應鏈的擴展,企業可以藉此規避未來價格波動帶來的風險。微型燃氣渦輪增程器在需要高功率密度的專案中佔據一席之地,例如高性能汽車和航太原型機。例如, Delta Motorsports 的演示裝置表明,35kW 的微型燃氣渦輪機比同等功率的活塞式引擎更輕,產生的排放物也更少。自由活塞線性發電機和鋅空氣電池技術目前仍處於展示室階段,尚未進入市場,但它們的長期變革潛力持續吸引創業投資資金。

在2025年的電動車增程器市場中,電池組將佔總價值的43.02%,凸顯了儲能在所有架構中的核心角色。合適的容量選擇仍然需要設計上的平衡。電池組必須提供約80-100公里的純電續航里程,以滿足都市區通行法規的要求,同時又不能增加車輛重量,以免影響有效負載容量。儘管功率轉換器的單價較高,但由於商用車隊需要長時間無怠速運轉和低溫性能,因此它是成長最快的組件,複合年成長率高達18.45%。先進的功率轉換器負責在電池組、發電機和驅動馬達之間分配能量,而新一代碳化矽元件可將損耗降低高達30%。

溫度控管系統正逐漸成為關鍵組件類別,尤其是在燃料電池和固體氧化物燃料電池應用中,因為控制動作溫度直接影響系統的效率和耐久性。固體氧化物燃料電池系統的研究表明,熱循環可靠性和燃料重整技術是需要先進溫度控管解決方案的主要技術挑戰。先進的電池管理系統和增程器控制策略的整合,推動了對能夠最佳化系統整體效率並管理多種能源來源的精密電力電子設備的需求。組件供應商正致力於模組化設計,以實現不同增程器架構之間的靈活整合。例如,採埃孚(ZF)等公司正在開發將發電機、逆變器和齒輪組整合到單一封裝中的系統,從而降低複雜性並提高可靠性。

區域分析

歐洲在電動車增程器市場處於領先地位,預計到2025年將佔據33.95%的市場佔有率,這主要得益於日益嚴格的車輛平均二氧化碳排放標準以及即將實施的歐7排放標準。該地區的汽車製造商正在利用現有的汽油引擎生產線,對其進行改造以適應E10燃料,並將其與在本土超級工廠組裝的磷酸鋰鐵鋰電池組相結合。法國、德國和荷蘭的市政當局已經強制要求在城區使用電動車,並且正在將本地配送車輛逐步過渡到串聯式混合動力汽車。

亞太地區正以18.90%的複合年成長率快速成長。這主要得益於中國增程器電動車(EREV)市場的持續成長。儘管純電動車(BEV)的補貼正在逐步減少,但預計到2024年,EREV仍將佔電動SUV銷量的25%。受消費者對高速公路充電問題的擔憂推動,EREV車型已佔大型SUV註冊量的60%。在日本,政府的藍圖目標是到2035年實現100%的電動車(xEV)銷量,而增程器平台將在未來10年內為現有製造商的政策應變提供支持,直至電池供應鏈擴展。在印度,城際巴士業者對增程式電動車的興趣日益濃厚,因為夜間需要在車庫充電,而白天在電力供應不足的農村線路仍需要使用發電機。

隨著美國環保署 (EPA) 收緊中型卡車的溫室氣體排放標準,以及多個州正在遵守加州的「先進清潔汽車 II」標準,北美有望成為第三大成長支柱。像 Harbinger 這樣的新創公司正在開發滑板式底盤,並可選配模組化汽油或氫燃料電池增程器作為續航里程模組,然後將其銷售給公共產業公司和市政服務車輛。加拿大已推出無污染燃料採購獎勵,而墨西哥則利用《美墨加協定》(USMCA) 吸引能夠免稅出口長距離續航貨車的契約製造。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 政府的零排放法規正在加速整車製造商的需求。

- 電池價格的下降使得經濟高效的混合動力架構成為可能。

- 都市區的超低排放區正在促進增程器的採用。

- 電子商務最後一公里配送車輛的快速成長。

- 防禦性採購靜音監視動力傳動系統(難以被雷達偵測)

- 採礦業向電池柴油混合動力運輸卡車的轉變(一個被忽視的趨勢)

- 市場限制因素

- 快速充電網路的發展減少了對擴展器的需求。

- 動力傳動系統的複雜性以及純電動車的替代方案

- 由於即將實施的歐8和加州空氣資源委員會(CARB)法規,對車內燃燒進行了限制(儘管沒有公開討論)。

- 缺乏殘值數據阻礙了車隊融資(這是一個不易察覺的因素)。

- 價值鏈分析

- 監理情勢

- 技術展望

- 波特五力模型

第5章 市場規模與成長預測

- 按類型

- ICE增程器

- 燃料電池增程器

- 固體氧化物燃料電池增程器

- 微型增程器

- 其他新興技術

- 按組件

- 電池組

- 電動機

- 發電機

- 電源轉換器

- 控制單元

- 溫度控管系統

- 按車輛類型

- 搭乘用車

- 輕型商用車

- 大型商用車輛

- 非公路用車輛

- 依輸出類型

- 小於30千瓦

- 30~60 kW

- 60~100 kW

- 超過100千瓦

- 按地區

- 北美洲

- 美國

- 加拿大

- 其他北美國家

- 歐洲

- 德國

- 英國

- 法國

- 義大利

- 西班牙

- 荷蘭

- 挪威

- 俄羅斯

- 其他歐洲國家

- 亞太地區

- 中國

- 日本

- 印度

- 韓國

- 澳洲

- 其他亞太國家

- 中東和非洲

- 沙烏地阿拉伯

- 阿拉伯聯合大公國

- 土耳其

- 埃及

- 南非

- 其他中東和非洲國家

- 北美洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- MAHLE International GmbH

- Rheinmetall Automotive AG

- Ceres Power Holdings plc

- Ballard Power Systems Inc.

- AVL List GmbH

- Magna International Inc.

- Horizon Fuel Cell Technologies

- Plug Power Inc.

- Nissan Motor Co., Ltd.

- BMW AG

- General Motors Co.

- Lotus Engineering

- Nikola Corporation

- REE Automotive

- Wrightspeed

- Tata Motors Ltd.

- Toyota Motor Corporation

- Ashok Leyland Ltd.

- Hyundai Motor Company

- Weichai Power Co., Ltd.

- Cummins Inc.

- Jiangling Motors Co., Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the electric vehicle range extender market size is expected to grow from USD 1.33 billion in 2025 to USD 1.49 billion in 2026 and is forecast to reach USD 2.64 billion by 2031 at 12.11% CAGR over 2026-2031.

This report is Segmented by Type (ICE and Fuel Cell Range Extender, Solid-Oxide Fuel Cell Range Extender and More), Component (Battery Pack and Electric Motor, Generator and More), Vehicle Class (Passenger Cars and Light Commercial Vehicles, and More), Power Output (Less Than 30 KW and 30-60 KW, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

Global Electric Vehicle Range Extender Market Trends and Insights

Government Zero-Emission Mandates Accelerating OEM Demand

Regulatory pressure is reshaping powertrain roadmaps and accelerating growth in the Electric Vehicle Range Extender Market. Euro 7 limits that took effect in 2024 slash NOx for heavy-duty trucks by 50%, pushing manufacturers to hybridize quickly. California's Advanced Clean Cars II requires 100% zero-emission sales by 2035, and Washington State mirrors those standards, letting OEMs earn compliance credits from range-extended models. Proposed U.S. EPA rules for 2027-2032 would force average fleet emissions down to 82 g CO2/mile, making range extenders an attainable option while public charging rolls out. Automakers now prioritize scalable architectures that accept both battery-only and range-extended variants for flexibility across world markets.

Falling Battery Prices Enabling Cost-Efficient Hybrid Architectures

Lithium-ion cost declines to USD 139 per kWh lowered total system outlays, letting OEMs pair compact packs with auxiliary gensets without breaching cost targets. Shifts toward lithium-iron-phosphate chemistry add further margin, especially for commercial fleets where cycle life outweighs range. The Electric Vehicle Range Extender Market is also benefiting from the U.S. Inflation Reduction Act and EU investment programs that are localizing cell production, trimming logistics expenses, and favoring integrated range extender lines. EUROBAT forecasts an eightfold jump in European lithium battery demand by 2035, reinforcing economies of scale that benefit hybrid layouts.

Fast-Charging Network Build-Out Reducing Need for Extenders

Electrify America expanded its network 25% in 2024, targeting 5,000 high-power stalls that shrink average charge times. The U.S. NEVI program funnels USD 5 billion through 2028 to create 500,000 public ports, while California alone plans for 39,000 DC fast chargers by 2030. As coverage improves, pure BEVs become more practical, eroding some demand for auxiliary gensets, though rural freight still faces gaps.

Other drivers and restraints analyzed in the detailed report include:

- Urban Ultra-Low-Emission Zones Spurring Adoption

- Rapid Growth of Last-Mile E-Commerce Fleets

- High Drivetrain Complexity vs BEV Alternatives

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

ICE range extenders maintained 66.72% of the Electric Vehicle Range Extender Market share in 2025 because OEMs can reuse mature supply chains for small gasoline or gaseous-fuel engines. The platform accommodates existing emission after-treatment, diagnostic tools, and manufacturing lines, shortening development cycles. However, Fuel-cell range extenders are advancing at a 22.05% CAGR and anchor product roadmaps for high-efficiency commercial vehicles that must achieve zero local emissions. Solid-oxide stacks from Ceres Power and Weichai Power achieve high electrical efficiency at steady-state loads, making them viable for urban buses and distribution trucks.

Solid-oxide fuel-cell systems also tolerate multiple fuels - hydrogen, methane, and ammonia, allowing operators to hedge against future price swings as the hydrogen supply chain expands. Micro-turbine range extenders hold a niche for high-power-density projects such as performance cars and aerospace prototypes. Delta Motorsport's demonstrator, for example, shows how a 35-kW micro gas turbine can weigh less than a comparable piston engine while emitting fewer particulates. Although free-piston linear generators and zinc-air chemistries sit in laboratories rather than showrooms, their long-term disruption potential keeps venture funding active.

Battery packs accounted for 43.02% of total value in the Electric Vehicle Range Extender Market in 2025, underscoring the central role of energy storage in every architecture. Right-sizing remains a design balancing act: packs must deliver roughly 80-100 km of electric range to satisfy urban-access rules without inflating curb weight to the point of eroding payload. Despite higher unit cost, power converter exhibit the fastest component growth at a 18.45% CAGR because commercial fleets need long idle-free periods and low-temperature performance. Sophisticated power converters channel energy between the pack, generator, and traction motor, and next-generation silicon-carbide devices cut losses by up to 30%.

Thermal management systems are emerging as a critical component category, particularly for fuel cell and solid oxide fuel cell applications where operating temperature control directly impacts system efficiency and durability. Research on solid oxide fuel cell systems indicates that thermal cycling reliability and fuel reforming technologies represent key technical challenges requiring advanced thermal management solutions.The integration of advanced battery management systems with range extender control strategies is driving demand for sophisticated power electronics that can manage multiple energy sources while optimizing overall system efficiency. Component suppliers are focusing on modular designs that enable flexible integration across different range extender architectures, with companies like ZF developing integrated systems that combine generators, inverters, and gearsets in unified packages to reduce complexity and improve reliability.

Geography Analysis

Europe led the electric vehicle range extender market with 33.95% 2025 revenue share due to stringent fleet-average CO2 norms and the impending Euro 7 regime. OEMs there leverage existing gasoline engine lines converted for E10 fuel and pair them with lithium-iron-phosphate packs assembled in domestic gigafactories. City councils in France, Germany, and the Netherlands already require electric operation inside urban cores, pushing local delivery fleets toward series hybrids.

Asia-Pacific advances at a 18.90% CAGR because China's extended-range electric vehicle segment - accounting for 25% of 2024 electric SUV sales - continues scaling even as pure BEV subsidies taper. EREV designs dominate large-SUV registrations at 60% share thanks to consumer anxiety over highway charging. In Japan, the government roadmap targets 100% xEV sales by 2035, leaving a decade-long window where range-extender platforms help legacy manufacturers satisfy policy while battery supply chains ramp. India sees emerging interest from intercity bus operators that need overnight depot charging but still require daytime generator use for rural routes with weak grid access.

North America makes up the third growth pillar as the Environmental Protection Agency tightens greenhouse-gas standards for medium-duty trucks and several states align with California's Advanced Clean Cars II. Start-ups such as Harbinger develop skateboard chassis with modular gasoline or hydrogen fuel-cell extenders as optional range modules, marketing them to utilities and municipal service fleets. Canada follows with clean-fuel purchase incentives, while Mexico attracts contract manufacturers leveraging the United States-Mexico-Canada Agreement to export range-extended delivery vans tariff-free.

- MAHLE International GmbH

- Rheinmetall Automotive AG

- Ceres Power Holdings plc

- Ballard Power Systems Inc.

- AVL List GmbH

- Magna International Inc.

- Horizon Fuel Cell Technologies

- Plug Power Inc.

- Nissan Motor Co., Ltd.

- BMW AG

- General Motors Co.

- Lotus Engineering

- Nikola Corporation

- REE Automotive

- Wrightspeed

- Tata Motors Ltd.

- Toyota Motor Corporation

- Ashok Leyland Ltd.

- Hyundai Motor Company

- Weichai Power Co., Ltd.

- Cummins Inc.

- Jiangling Motors Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Government zero-emission mandates accelerating OEM demand

- 4.2.2 Falling battery prices enabling cost-efficient hybrid architectures

- 4.2.3 Urban ultra-low-emission zones spurring range-extender adoption

- 4.2.4 Rapid growth of last-mile e-commerce fleets

- 4.2.5 Defense procurement of silent-watch hybrid powertrains (under-the-radar)

- 4.2.6 Mining industry shift to battery-diesel hybrid haul trucks (under-the-radar)

- 4.3 Market Restraints

- 4.3.1 Fast-charging network build-out reducing need for extenders

- 4.3.2 High drivetrain complexity vs. BEV alternatives

- 4.3.3 Upcoming Euro 8 and CARB rules limiting onboard combustion (under-the-radar)

- 4.3.4 Limited residual-value data hindering fleet financing (under-the-radar)

- 4.4 Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD) and Volume (Units))

- 5.1 By Type

- 5.1.1 ICE Range Extender

- 5.1.2 Fuel Cell Range Extender

- 5.1.3 Solid-Oxide Fuel Cell Range Extender

- 5.1.4 Micro-Turbine Range Extender

- 5.1.5 Other Emerging Technologies

- 5.2 By Component

- 5.2.1 Battery Pack

- 5.2.2 Electric Motor

- 5.2.3 Generator

- 5.2.4 Power Converter

- 5.2.5 Control Unit

- 5.2.6 Thermal Management System

- 5.3 By Vehicle Class

- 5.3.1 Passenger Cars

- 5.3.2 Light Commercial Vehicles

- 5.3.3 Heavy Commercial Vehicles

- 5.3.4 Off-Highway Vehicles

- 5.4 By Power Output

- 5.4.1 Less than 30 kW

- 5.4.2 30 - 60 kW

- 5.4.3 60 - 100 kW

- 5.4.4 More than 100 kW

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Netherlands

- 5.5.2.7 Norway

- 5.5.2.8 Russia

- 5.5.2.9 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 Saudi Arabia

- 5.5.4.2 United Arab Emirates

- 5.5.4.3 Turkey

- 5.5.4.4 Egypt

- 5.5.4.5 South Africa

- 5.5.4.6 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products & Services, and Recent Developments)

- 6.4.1 MAHLE International GmbH

- 6.4.2 Rheinmetall Automotive AG

- 6.4.3 Ceres Power Holdings plc

- 6.4.4 Ballard Power Systems Inc.

- 6.4.5 AVL List GmbH

- 6.4.6 Magna International Inc.

- 6.4.7 Horizon Fuel Cell Technologies

- 6.4.8 Plug Power Inc.

- 6.4.9 Nissan Motor Co., Ltd.

- 6.4.10 BMW AG

- 6.4.11 General Motors Co.

- 6.4.12 Lotus Engineering

- 6.4.13 Nikola Corporation

- 6.4.14 REE Automotive

- 6.4.15 Wrightspeed

- 6.4.16 Tata Motors Ltd.

- 6.4.17 Toyota Motor Corporation

- 6.4.18 Ashok Leyland Ltd.

- 6.4.19 Hyundai Motor Company

- 6.4.20 Weichai Power Co., Ltd.

- 6.4.21 Cummins Inc.

- 6.4.22 Jiangling Motors Co., Ltd.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

電動汽車增程器市場報告:按類型、組件、車輛類型和地區分類(2026-2034 年)

電動汽車增程器市場報告:按類型、組件、車輛類型和地區分類(2026-2034 年) 全球電動車增程器市場

全球電動車增程器市場 電動車增程器市場:按增程器類型、燃料類型、功率範圍、車輛類型、應用和銷售管道分類-2026-2032年全球預測

電動車增程器市場:按增程器類型、燃料類型、功率範圍、車輛類型、應用和銷售管道分類-2026-2032年全球預測 全球及中國增程器車(REEV)及插電式混合動力汽車(PHEV)市場(2026 年)

全球及中國增程器車(REEV)及插電式混合動力汽車(PHEV)市場(2026 年) 增程型電動車(EREV)市場規模、佔有率和成長分析:按產品類型、推進系統、電池類型、最終用戶和地區分類-2026-2033年產業預測

增程型電動車(EREV)市場規模、佔有率和成長分析:按產品類型、推進系統、電池類型、最終用戶和地區分類-2026-2033年產業預測 增程器電動車市場展望:歐洲、美國、中國,2024-2040年全球電動汽車增程器市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

增程器電動車市場展望:歐洲、美國、中國,2024-2040年全球電動汽車增程器市場規模、佔有率、趨勢和成長分析報告(2026-2034年) 電動車增程器市場-全球產業規模、佔有率、趨勢、機會與預測:按類型、組件類型、車輛類型、地區和競爭格局分類,2021-2031年

電動車增程器市場-全球產業規模、佔有率、趨勢、機會與預測:按類型、組件類型、車輛類型、地區和競爭格局分類,2021-2031年 增程型電動車市場:依車輛類型、增程器類型、電池容量、應用和地區劃分 - 全球市場分析(2025-2035)

增程型電動車市場:依車輛類型、增程器類型、電池容量、應用和地區劃分 - 全球市場分析(2025-2035) 電動汽車增程器市場:市場機會、成長促進因素、產業趨勢分析及預測(2026-2035)

電動汽車增程器市場:市場機會、成長促進因素、產業趨勢分析及預測(2026-2035)