|

市場調查報告書

商品編碼

2044288

歐洲電子製造服務:市場佔有率分析、行業趨勢和統計數據、成長預測(2026-2031 年)Europe Electronic Manufacturing Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

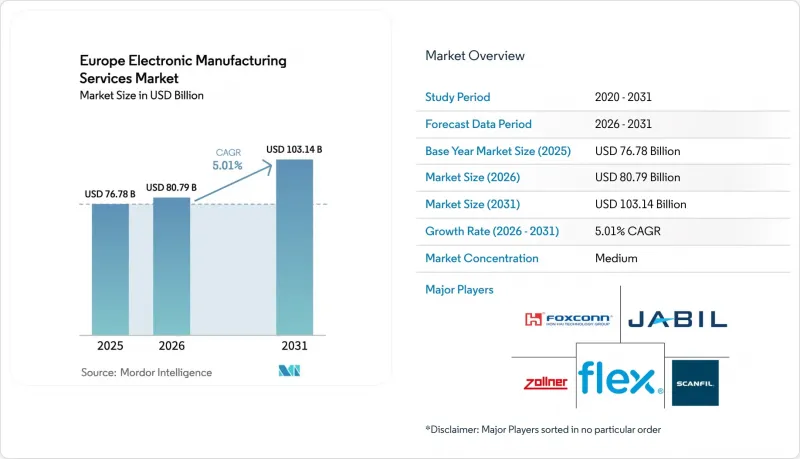

歐洲電子製造服務 (EMS) 市場預計到 2025 年將達到 767.8 億美元,到 2026 年將達到 807.9 億美元,到 2031 年將達到 1,031.4 億美元,2026 年至 2031 年的複合年成長率為 5.01%。

歐洲電子製造服務市場的強勁成長勢頭得益於以下因素:優先考慮供應鏈透明度的法規、汽車、工業和醫療領域對本地生產能力日益成長的需求,以及高混合、小批量生產項目持續從亞洲轉移到受監管的歐洲工廠。能夠證明符合 ISO 14001 和企業永續性報告指令 (CSRD) 的契約製造正在獲得多年框架契約,而那些沒有碳核算系統的供應商則正將訂單讓給那些提供可追溯、低排放組裝的競爭對手。近岸外包也將原型開發週期從八週縮短至三週,透過加快設計迭代和降低運輸成本來抵消更高的人事費用。自動化、協作機器人和人工智慧驅動的光學檢測技術持續降低直接人事費用,使複雜組裝與亞洲的成本差距從五年前的 40% 縮小至約 20%。

歐洲電子製造服務市場的趨勢與洞察

歐洲原始設備製造商正在擴大電子設備生產的外包規模。

原始設備製造商 (OEM) 正將資金從自有生產線轉移到軟體和電氣化領域,並將複雜的基板組裝和機殼組裝外包給已符合 ISO 13485 和 IPC 標準的合約合作夥伴。西門子於 2025 年出售其安貝格 PCB 業務,以及博世和 Zollner 之間加強合作,都像徵著這種轉變,使製造商擺脫了與表面黏著技術線和回流焊接爐相關的資金束縛。儘管預計到 2025 年歐洲的外包滲透率將達到 38%,但仍落後於亞洲,這表明歐洲電子製造服務市場仍有空間將更多自有工廠轉為外包。能夠在同一地點完成工程和製造的供應商可以在不到一周的時間內完成從原型到試生產的過渡,而這幾乎是企業內部無法實現的。這種趨勢在醫療和工業專案中最為明顯,因為合規性和變更管理的負擔更有利於專業的電子製造服務 (EMS) 合作夥伴。

汽車電子產品需求激增

每輛電池式電動車的PCB面積是傳統內燃機汽車的三到五倍,而歐洲L3級自動駕駛功能的合法認證又增加了雷射雷達、雷達和高性能域控制器。大眾動力公司和康創公司共同開發的電池管理系統(BMS),以及48伏架構的廣泛應用,都推高了對碳化矽(SiC)和氮化鎵(GaN)模組的需求。掌握了汽車級熱循環條件下覆晶和焊線組裝技術的電子製造服務(EMS)廠商,正獲得高利潤產品和長期合約。隨著一級供應商大力推進軟體定義汽車,他們依賴EMS合作夥伴每18個月進行一次硬體升級。預計到2031年,汽車領域將成為歐洲電子製造服務市場成長最快的領域。

與亞洲相比,歐洲的勞動力和能源成本較高。

德國的滿載人事費用平均為每小時 35 歐元(39.6 美元),而越南僅為每小時 4 歐元(4.5 美元),機器人技術僅部分彌補了這一差距。預計到 2025 年,德國的工業用電價格將達到每千瓦時 0.18 歐元(0.20 美元),是中國的兩倍多,這將擠壓波峰焊接和選擇性焊接生產線的利潤空間。雖然自動化已使直接人工工時減少了 25%,但由於機器人和偵測攝影機的折舊,間接成本仍然居高不下。必須在歐洲生產的產品,例如受電池法規約束的電池管理系統 (BMS) 模組,可以承受更高的成本,但對價格敏感的消費性電子產品則無法負擔。這種不平衡限制了歐洲電子製造服務市場的複合年成長率,直到能源價格趨於一致且自動化程度進一步提高。

細分市場分析

截至2025年,PCB組裝在歐洲電子製造服務市場銷售額中佔比41.22%,但隨著OEM廠商將機殼整合、線束和功能測試台等業務外包,預計到2031年,電子機械箱體製造業務將以6.11%的複合年成長率成長。這種轉變將使OEM廠商擺脫無塵室和溫濕度控制室的資金投入,同時也減少了用於合規性審核的人員。 EMS供應商透過將韌體編寫和線上檢驗捆綁銷售,並與客戶簽訂包含延遲交付違約金條款的多年期契約,從而獲得額外利潤。

由於產品生命週期超過10年,且設計變更通知往往會深入到組裝流程的各個環節,工業和醫療項目正在推動這一成長。位置德國和瑞士設計中心附近的整機工廠透過在幾天內完成設計回饋循環,並避免空運需要返工的子組件,從而減輕了人事費用上漲的影響。歐洲電子製造服務市場正透過引入供應鏈協調軟體而獲得進一步發展動力。該軟體可在排產中反映即時元件庫存狀態,並支援小批量生產中的分批套件組裝和平行工程。因此,ODM式工程服務也在不斷擴展,使EMS公司能夠在不產生可能危及監管核准的重新設計週期的情況下,對注重可製造性的基板佈局進行微調。

2025年,契約製造佔歐洲電子製造服務市場的63.71%。這反映了既有的外包模式,即原始設備製造商(OEM)擁有元件,而電子製造服務(EMS)公司則收取人事費用。然而,混合型和承包合約預計將以5.67%的複合年成長率成長,它們正在重塑責任框架,將元件採購、報廢和可追溯性的責任賦予EMS供應商。中小型OEM廠商正在採用這種模式,因為它使他們能夠利用Arrow和Avnet等分銷商的批量採購能力,從而避免2024-2025年可能出現的嚴重供不應求。

此外,承包工程合約使電子製造服務 (EMS) 公司能夠立即更換引腳相容的替代部件,無需等待原始設備製造商 (OEM) 的設計變更指令,從而避免生產中斷。財務實力雄厚的供應商會維持六個月的安全庫存,而這種策略對於小眾市場的參與企業來說遙不可及。因此,規模經濟正在不斷積累,產業重組也在推進,例如 Kontron 收購 Catec,後者將設計、採購和組裝整合到一個 ERP 平台中。因此,歐洲 EMS 市場正呈現日益集中化的趨勢,這些企業能夠在關鍵的醫療和汽車專案中承擔庫存持有成本,同時保持準時交貨的標準。

其他好處

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 歐洲原始設備製造商正在擴大電子設備生產的外包規模。

- 汽車電子產品(電動車、ADAS)需求激增

- 工業和醫療設備領域高混合、小批量生產的成長

- 歐盟電池相關獎勵:針對本地電池管理系統和電力電子產品

- 透過供應鏈安全相關立法促進近岸外包。

- 由於CSRD,對低碳EMS設施的需求增加。

- 市場限制因素

- 歐洲勞動力和能源成本高(與亞洲相比)

- 持續的零件短缺和庫存風險

- 先進SMT和自動化領域熟練勞動力短缺

- 歐盟合規負擔在中小EMS公司之間的分配

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

- 供應商的議價能力

- 買方的議價能力

- 新進入者的威脅

- 替代品的威脅

- 競爭公司之間的競爭

第5章 市場規模與成長預測

- 按服務類型

- 電子製造服務

- PCB組裝

- 電子機械組裝/箱體製造

- 原型

- 其他

- 工程服務

- 測試和開發實施服務

- 物流服務

- 其他

- 電子製造服務

- 按經營模式

- 契約製造(CM)

- ODM

- 混合/承包/其他經營模式

- 透過製造程序

- 表面黏著技術(SMT)

- 通孔技術(THT)

- 先進封裝/混合工藝

- 最終用戶

- 行動裝置(智慧型手機和平板電腦)

- 家用電器

- 電腦(桌上型電腦/筆記型電腦)

- 工業的

- 車

- 溝通

- 照明

- 醫療保健

- 其他

- 按地區

- 歐洲

- 德國

- 英國

- 其他歐洲國家

- 歐洲

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Foxconn Technology Group

- Flex Ltd.

- Jabil Inc.

- Zollner Elektronik AG

- GPV Group

- Scanfil Plc

- Videoton Holding

- Kontron AG

- Kitron ASA

- Cicor Group

- HANZA AB

- LACROIX Electronics

- NOTE AB

- Neways Electronics

- BMK Group

- Melecs EWS

- Variosystems AG

- TT Electronics Plc

- INCAP Oy

- Norautron AS

第7章 市場機會與未來展望

The Europe electronic manufacturing services market size is projected to be USD 76.78 billion in 2025, USD 80.79 billion in 2026, and reach USD 103.14 billion by 2031, growing at a CAGR of 5.01% from 2026 to 2031.

The momentum of the Europe electronics manufacturing services market stems from legislation that prioritizes supply-chain transparency, mounting demand for local capacity in automotive, industrial, and medical verticals, and the ongoing relocation of high-mix, low-volume programs from Asia to compliant European plants. Contract manufacturers that can prove ISO 14001 alignment and Corporate Sustainability Reporting Directive readiness are securing multi-year frameworks, while providers lacking carbon-accounting systems are losing bids to rivals offering traceable, low-emission assembly. Near-shoring also shortens prototype cycles from eight to three weeks, an advantage that offsets labor premiums through faster design iterations and lower freight expense. Automation, collaborative robotics, and AI-driven optical inspection continue to trim direct labor content, narrowing the cost delta with Asia to roughly 20% for complex assemblies, down from 40% five years earlier.

Europe Electronic Manufacturing Services Market Trends and Insights

Rising Outsourcing of Electronics Production by European OEMs

OEMs are channeling capital away from in-house lines toward software and electrification, pushing complex board population and box build into the hands of contract partners that already meet ISO 13485 and IPC standards. Siemens' 2025 divestiture of its Amberg PCB operation and Bosch's deeper collaboration with Zollner typify the transition, allowing manufacturers to release cash tied up in surface-mount lines and reflow ovens. Outsourcing penetration in Europe climbed to 38% in 2025 yet still trails Asia, implying runway for the Europe electronics manufacturing services market to convert additional captive plants. Providers able to co-locate engineering with manufacturing speed revisions from prototype to pilot in under a week, a cycle that captive plants rarely match. The trend is most pronounced in medical and industrial programs, where compliance and revision-control overhead favor specialist EMS partners.

Surge in Automotive Electronics Demand

Each battery electric vehicle embeds three to five times more PCB area than its combustion predecessor, and Europe's legal green-light for Level-3 autonomous functions is adding lidar, radar, and high-compute domain controllers. Volkswagen PowerCo's BMS co-development with Kontron and widespread adoption of 48-volt architectures increase silicon-carbide and gallium-nitride module demand. EMS sites that master flip-chip and wire-bond assembly under automotive-grade thermal cycling secure higher-margin content and long contracts. As Tier-1 suppliers push software-defined vehicles, they rely on EMS partners to iterate hardware every 18 months. This momentum positions automotive as the fastest advancing slice of the Europe electronic manufacturing services market through 2031.

Higher European Labor and Energy Costs vs. Asia

Fully loaded German labor averages EUR 35 per hour (USD 39.6) against EUR 4 in Vietnam (USD 4.5), a gulf only partly bridged by robotics. Industrial power in Germany cost EUR 0.18 per kWh (USD 0.20) during 2025, more than double Chinese rates, eroding margins on wave solder and selective-solder lines. Although automation trimmed direct labor minutes by 25%, amortization of robotics and inspection cameras keeps overhead high. Products that mandate European proximity, such as BMS modules subject to the Battery Regulation, survive the premium, but price-sensitive consumer gear does not. The imbalance caps the upper range of the Europe electronics manufacturing services market CAGR until energy-price convergence or more aggressive automation emerges.

Other drivers and restraints analyzed in the detailed report include:

- Near-Shoring Triggered by Supply-Chain Security Legislation

- CSRD-Driven Demand for Low-Carbon EMS Facilities

- Skilled-Labor Gap in Advanced SMT and Automation

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Europe electronic manufacturing services market size for PCB assembly commanded 41.22% of revenue in 2025, yet electromechanical box build is posting a 6.11% CAGR through 2031 as OEMs outsource enclosure integration, cable harnessing, and functional test benches. The migration frees OEM cash otherwise tied up in clean rooms and climate-controlled chambers, simultaneously reducing headcount dedicated to compliance audits. EMS providers capture additional margin by bundling firmware flashing and in-circuit verification, locking clients into multi-year agreements with penalty clauses for schedule slippage.

Industrial and medical programs fuel the surge because product lifecycles run a decade or more, and engineering change notifications often cascade deep into assembly. Box-build plants located near design centers in Germany and Switzerland complete engineering feedback loops in days, diminishing the impact of labor premiums by avoiding air freight on reworked sub-assemblies. The Europe electronic manufacturing services market gains further momentum as providers embed supply-chain orchestration software that pulls real-time component availability into scheduling, allowing split-lot kitting and concurrent engineering on low-volume runs. In turn, ODM-style engineering services grow alongside, enabling EMS firms to tweak board layouts for manufacturability without incurring redesign cycles that jeopardize regulatory approvals.

Contract manufacturing held a 63.71% share of the Europe electronic manufacturing services market in 2025, reflecting entrenched consignment models where OEMs own parts and EMS firms charge labor fees. However, hybrid and turnkey contracts, projected at a 5.67% CAGR, are resetting liability frameworks by making EMS vendors responsible for component sourcing, obsolescence, and traceability. Smaller OEMs embrace the model because it taps the bulk-buying leverage of distributors like Arrow and Avnet, thereby insulating them from allocation shortages that defined 2024-2025.

Turnkey deals also empower EMS houses to swap pin-compatible alternates instantly, bypassing OEM engineering change orders and preventing production stops. Providers with deep balance sheets underwrite six months of safety stock, a strategy out of reach for niche players. Consequently, scale advantages accumulate, prompting consolidation as evidenced by Kontron's integration of KATEK that merged design, procurement, and assembly inside a single ERP backbone. The Europe EMS market therefore witnesses a progressive concentration among operators capable of absorbing inventory carrying costs while maintaining just-in-time delivery metrics for critical medical and automotive projects.

The Europe Electronic Manufacturing Services Market Report is Segmented by Service Type (Engineering Services, and More), Business Model (Contract Manufacturing (CM), Original Design Manufacturing (ODM), and More), Manufacturing Process (Surface Mount Technology (SMT), Through-Hole Technology (THT), and More), End-User (Industrial, Automotive, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Foxconn Technology Group

- Flex Ltd.

- Jabil Inc.

- Zollner Elektronik AG

- GPV Group

- Scanfil Plc

- Videoton Holding

- Kontron AG

- Kitron ASA

- Cicor Group

- HANZA AB

- LACROIX Electronics

- NOTE AB

- Neways Electronics

- BMK Group

- Melecs EWS

- Variosystems AG

- TT Electronics Plc

- INCAP Oy

- Norautron AS

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Outsourcing of Electronics Production by European OEMs

- 4.2.2 Surge in Automotive Electronics Demand (EVs, ADAS)

- 4.2.3 Growth of High-Mix, Low-Volume Industrial and Medical Devices

- 4.2.4 EU Battery-Booster Incentives for Local BMS and Power-Electronics

- 4.2.5 Near-shoring Triggered by Supply-Chain Security Legislation

- 4.2.6 CSRD-Driven Demand for Low-Carbon EMS Facilities

- 4.3 Market Restraints

- 4.3.1 Higher European Labour and Energy Costs vs. Asia

- 4.3.2 Ongoing Component Shortages and Inventory Risk

- 4.3.3 Skilled-Labour Gap in Advanced SMT and Automation

- 4.3.4 Fragmented EU Compliance Burden for Smaller EMS Firms

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Type

- 5.1.1 Electronic Manufacturing Services

- 5.1.1.1 PCB Assembly

- 5.1.1.2 Electromechanical Assembly/Box Build

- 5.1.1.3 Prototyping

- 5.1.1.4 Other Electronic Manufacturing Services

- 5.1.2 Engineering Services

- 5.1.3 Test and Development Implementation Services

- 5.1.4 Logistics Services

- 5.1.5 Other Service Types

- 5.1.1 Electronic Manufacturing Services

- 5.2 By Business Model

- 5.2.1 Contract Manufacturing (CM)

- 5.2.2 Original Design Manufacturing (ODM)

- 5.2.3 Hybrid / Turnkey / Other Business Models

- 5.3 By Manufacturing Process

- 5.3.1 Surface Mount Technology (SMT)

- 5.3.2 Through-Hole Technology (THT)

- 5.3.3 Advanced Packaging / Hybrid Processes

- 5.4 By End-user

- 5.4.1 Mobile Devices (Smartphones and Tablets)

- 5.4.2 Consumer Electronics

- 5.4.3 Computer (PCs/Desktop/Laptops)

- 5.4.4 Industrial

- 5.4.5 Automotive

- 5.4.6 Communication

- 5.4.7 Lighting

- 5.4.8 Medical

- 5.4.9 Other End-users

- 5.5 By Geography

- 5.5.1 Europe

- 5.5.1.1 Germany

- 5.5.1.2 United Kingdom

- 5.5.1.3 Rest of Europe

- 5.5.1 Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Foxconn Technology Group

- 6.4.2 Flex Ltd.

- 6.4.3 Jabil Inc.

- 6.4.4 Zollner Elektronik AG

- 6.4.5 GPV Group

- 6.4.6 Scanfil Plc

- 6.4.7 Videoton Holding

- 6.4.8 Kontron AG

- 6.4.9 Kitron ASA

- 6.4.10 Cicor Group

- 6.4.11 HANZA AB

- 6.4.12 LACROIX Electronics

- 6.4.13 NOTE AB

- 6.4.14 Neways Electronics

- 6.4.15 BMK Group

- 6.4.16 Melecs EWS

- 6.4.17 Variosystems AG

- 6.4.18 TT Electronics Plc

- 6.4.19 INCAP Oy

- 6.4.20 Norautron AS

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

電子製造服務市場:2026-2032年全球市場預測(依服務類型、技術、組件類型、最終用戶產業及企業規模分類)

電子製造服務市場:2026-2032年全球市場預測(依服務類型、技術、組件類型、最終用戶產業及企業規模分類) 電子設備電子製造服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

電子設備電子製造服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 專業電子代工服務 (EMS) 市場:按服務、產品類型、經營模式、最終用途、國家和地區分類 - 全球產業分析、市場規模與佔有率及未來預測 (2026-2033)電子製造服務市場:依服務、經營模式、製造流程、最終用戶、國家及地區分類-全球產業分析、市場規模、市場佔有率及2026年至2033年預測

專業電子代工服務 (EMS) 市場:按服務、產品類型、經營模式、最終用途、國家和地區分類 - 全球產業分析、市場規模與佔有率及未來預測 (2026-2033)電子製造服務市場:依服務、經營模式、製造流程、最終用戶、國家及地區分類-全球產業分析、市場規模、市場佔有率及2026年至2033年預測 電子受託製造服務市場預測至2034年-按服務類型、經營模式、製造形式、最終用戶產業和地區分類的全球分析

電子受託製造服務市場預測至2034年-按服務類型、經營模式、製造形式、最終用戶產業和地區分類的全球分析 全球電訊設備受託製造服務(EMS)市場。

全球電訊設備受託製造服務(EMS)市場。 通訊電子製造服務市場:全球產業規模、佔有率、趨勢、機會和預測(按服務、應用和地區分類)、競爭格局(2021-2031 年)

通訊電子製造服務市場:全球產業規模、佔有率、趨勢、機會和預測(按服務、應用和地區分類)、競爭格局(2021-2031 年) 綠色電子製造市場規模、佔有率和成長分析:按製造流程、產品類型、最終用途產業和地區分類-2026-2033年產業預測馬來西亞電子製造服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

綠色電子製造市場規模、佔有率和成長分析:按製造流程、產品類型、最終用途產業和地區分類-2026-2033年產業預測馬來西亞電子製造服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 2026-2030年全球電子製造服務市場

2026-2030年全球電子製造服務市場