|

市場調查報告書

商品編碼

2063393

馬來西亞電子製造服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)Malaysia Electronics Manufacturing Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本網頁內容可能與最新版本有所差異。詳細情況請與我們聯繫。

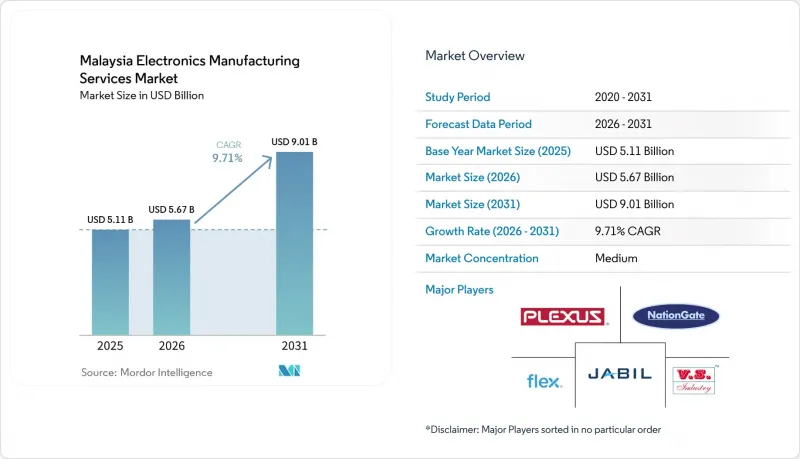

根據 Mordor Intelligence 預測,馬來西亞電子製造服務市場規模將從 2025 年的 51.1 億美元成長到 2026 年的 56.7 億美元,到 2031 年將達到 90.1 億美元,2026 年至 2031 年的複合年成長率為 9.71%。

本報告按服務類型(電子製造服務、工程服務等)、經營模式(契約製造等)、製造流程(表面黏著技術、通孔技術等)、最終用戶(行動裝置、家用電子電器等)和地區進行細分。市場預測以美元計價。

馬來西亞電子製造服務市場的趨勢與洞察

檳城EMS走廊外商直接投資擴大

檳城預計將在2025年上半年吸引125億馬幣(32億美元)的已通過核准投資,年增150%,鞏固其作為馬來西亞半導體中心的地位。英特爾、英飛凌和AT&S等公司正在推進數十億美元的擴張計劃,重點是晶片整合和系統級封裝(SiP)解決方案。檳城擁有許多機械加工供應商、貨運樞紐和大學,這降低了新參與企業的推出成本,並加快了其投產速度。預計到2025年,檳城將佔馬來西亞電子產品出口總額的45%,並印證了馬來西亞投資發展局(MIDA)所指出的集聚效應。

馬來西亞5G行動電話出口擴張

2025年第三季度,東南亞地區共出貨2,560萬部5G智慧型手機,其中馬來西亞的組裝線為中國的區域和最終組裝基地供貨。專用於射頻模組和基板的軟性SMT生產線縮短了交貨週期,使品牌能夠向新興市場推出售價低於300美元的機型。 2025年7月,電子設備出口年增22.5%,部分原因是行動電話組件的出口成長。為此,契約製造製造商引進了軟性SMT生產線,能夠在單班制內切換生產基板。這使得品牌能夠每週對韌體進行微調,而不會影響生產週期。根據「國家投資願景」框架,超過3億馬幣(約7,600萬美元)的項目可享有100%的資本支出抵扣,為符合5G可追溯性要求的回流焊接爐和自動光學檢測系統提供了大量補貼。

先進包裝業技術純熟勞工短缺

馬來西亞需要在2030年前儲備6萬名工程師,但每年只有5,000名相關專業的大學畢業生,儘管先進包裝生產線獲得了大量資金,產能仍然有限。預計到2025年,經驗豐富的包裝工程師的薪資漲幅將超過12%,這將削弱其成本優勢,迫使企業設計產學合作項目,但這些項目的課程設置仍然比行業需求滯後兩年之久。為了彌補這一差距,企業正在實施為期六個月的短期學徒計劃,但較短的培訓時間往往導致畢業生缺乏統計過程控制(SPC)方面的深入知識,從而在大規模推出初期造成更高的缺陷率。一些電子製造服務(EMS)供應商正在從台灣和韓國招募人才,但外籍員工的成本(包括住宅和教育津貼)可能比本地員工高出40%。產學研聯盟已經開發了微凸塊冶金和熱界面材料化學的新課程,但這些課程要到 2027 年底才會開始招收學生。

細分市場分析

該細分市場主要由智慧型手機和工業控制設備的PCB組裝驅動,預計到2025年將佔馬來西亞電子製造服務市場佔有率的42.73%。電子機械組裝預計將以9.86%的複合年成長率成長,主要受電動車電池管理系統和線束製造的推動。馬來西亞整機組裝電子製造服務市場預計將在2026年至2031年間實現顯著成長,這主要得益於OEM廠商對從設計到交貨全程服務的需求。

服務供應商透過獲得認證來脫穎而出,從而實現溢價,例如醫療行業的 ISO 13485 認證和汽車行業的 IATF 16949 認證。原型製作、物流以及測試和開發服務仍然是至關重要的策略立足點,有助於在設計初期階段留住客戶。儘管通用 PCB組裝面臨價格壓力,因為低成本市場吸引了大量大量生產訂單,但馬來西亞的品管系統保護了航太、工業和醫療等細分市場。

預計到2025年,契約製造將佔總收入的60.91%,凸顯了契約製造在電子製造服務市場的主導地位。隨著客戶越來越重視單一來源責任制以加快產品週期,混合型和承包合約模式預計將以10.13%的複合年成長率穩步成長。這些合約模式對於尋求縮短產品上市時間的公司來說極具吸引力,因為它們能夠提高流程效率並降低複雜性。馬來西亞電子製造服務市場,尤其是承包契約,預計將持續成長至2031年,這得益於供應商在元件採購和設計方面的優勢。

Jabiru斥資10億馬幣(約2.5億美元)在檳城園區興建新廠,凸顯了該公司不僅追求組裝收入,更致力於設計和物流收入的策略。這項大規模投資反映了公司拓展自身能力、提升價值鏈市場佔有率的決心。檳城園區可望成為創新和營運效率中心,進一步鞏固Jabiru的市場地位。同時,儘管原始設計製造(ODM)的市場佔有率目前較小,但其發展勢頭強勁,尤其是在那些缺乏內部工程能力的穿戴式設備和智慧家居品牌中。 ODM的成長表明,新興產品類型對專業設計和製造解決方案的需求日益成長。

其他好處:

- Excel格式的市場預測(ME)表

- 3個月的分析師支持

目錄

第1章:引言

- 研究假設和市場定義

- 調查範圍

第2章:調查方法

第3章執行摘要

第4章 市場狀況

- 市場概覽

- 市場促進因素

- 檳城EMS走廊外商直接投資增加

- 馬來西亞擴大5G行動電話出口

- 對高混合低產量(HMLV)生產的需求不斷成長

- 國家投資計畫(NIA)下的政府獎勵

- 從中國當地實現供應鏈多元化

- 二級EMS廠商智慧工廠4.0應用的興起

- 市場限制因素

- 先進包裝業技術純熟勞工短缺

- 能源成本波動對SMT生產線的影響

- 美元計價成分的外匯波動風險

- 來自越南和泰國的區域競爭日益加劇

- 產業價值鏈分析

- 監理情勢

- 技術展望

- 宏觀經濟因素對市場的影響

- 波特五力分析

第5章 市場規模與成長預測

- 服務類型

- 電子製造服務

- 印刷基板組裝

- 電子機械組裝/箱體製造

- 原型製作

- 其他電子製造服務

- 工程服務

- 測試和開發執行

- 物流服務

- 其他服務類型

- 電子製造服務

- 按經營模式

- 契約製造(CM)

- 原始設計製造(ODM)

- 混合/承包/其他經營模式

- 透過製造程序

- 表面黏著技術(SMT)

- 通孔技術(THT)

- 先進封裝/混合工藝

- 最終用戶

- 行動裝置(智慧型手機和平板電腦)

- 家用電子產品

- 電腦(桌上型電腦/筆記型電腦)

- 產業

- 車

- 溝通

- 照明

- 醫學領域

- 其他最終用戶

第6章 競爭情勢

- 市場集中度

- 策略趨勢

- 市佔率分析

- 公司簡介

- Flex Ltd.

- Jabil Inc.

- Celestica Inc.

- Sanmina Corporation

- Plexus Corp

- Venture Corporation Ltd.

- Benchmark Electronics Inc.

- VS Industry Berhad

- NationGate Holdings Berhad

- Integrated Manufacturing Solutions Sdn Bhd

- SKP Resources Berhad

- EG Industries Berhad

- ATA IMS Berhad

- PIE Industrial Berhad

- Mi Technovation Berhad

- Inari Amertron Berhad

- Cape EMS Bhd

- Scanfil Plc

- Wistron Corporation

- Universal Scientific Industrial Co. Ltd.

第7章 市場機會與未來展望

According to Mordor Intelligence, the malaysia electronics manufacturing services market is expected to grow from USD 5.11 billion in 2025 to USD 5.67 billion in 2026 and is forecasted to reach USD 9.01 billion by 2031 at 9.71% CAGR over 2026-2031.

This report is Segmented by Service Type (Electronic Manufacturing Services, Engineering Services, and More), Business Model (Contract Manufacturing, and More), Manufacturing Process (Surface Mount Technology, Through-Hole Technology, and More), End-User (Mobile Devices, Consumer Electronics, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Malaysia Electronics Manufacturing Services Market Trends and Insights

Growing Foreign Direct Investments in Penang EMS Corridor

Penang attracted MYR 12.5 billion (USD 3.2 billion) in approved investments during 1H 2025, 150% higher than the prior-year period, confirming its status as Malaysia's semiconductor hub. Intel, Infineon, and AT&S have multibillion-dollar expansion pipelines focused on chiplet integration and system-in-package solutions. Penang's dense network of machining vendors, cargo hubs, and universities lowers onboarding costs for new entrants and accelerates time-to-production. The state accounted for 45% of Malaysia's electronics exports in 2025, reinforcing the agglomeration benefits identified by MIDA.

Expansion of 5G Handset Exports from Malaysia

Southeast Asia shipped 25.6 million 5G smartphones in Q3 2025, with Malaysian assembly lines feeding both regional and Chinese final-integration sites. Flexible SMT lines dedicated to radio-frequency modules and multilayer boards drive quick-turn orders as brands push sub-USD 300 models to emerging markets. Electronics exports climbed 22.5% year-on-year in July 2025, powered partly by handset sub-assemblies. Contract manufacturers have responded by dedicating flexible SMT lines that switch between two-layer and eight-layer boards inside a single shift, allowing brands to release weekly firmware tweaks without disrupting takt time. The National Investment Aspirations framework grants 100% capital-allowance offsets for projects exceeding MYR 300 million (USD 76 million), effectively subsidizing reflow ovens and automatic optical-inspection systems that meet 5G traceability rules

Skilled Labour Shortages in Advanced Packaging

Malaysia must add 60,000 engineers by 2030, yet universities graduate only 5,000 relevant candidates annually, constraining throughput even as capital pours into advanced packaging lines. Wage inflation for experienced packaging engineers exceeded 12% in 2025, eroding cost advantages and forcing firms to design co-op programs whose curricula still lag industry needs by up to two years. To fill gaps, firms run accelerated six-month apprentice programs, but the compressed timeline means graduates often lack deep statistical-process-control skills, leading to higher scrap during ramp-up phases. Some EMS providers import talent from Taiwan and South Korea, yet expatriate packages can cost 40% more than local hires once housing and schooling allowances are included. Industry-academic consortia have drafted new curricula in micro-bump metallurgy and thermal-interface-material chemistry, but courses will not matriculate students until late-2027.

Other drivers and restraints analyzed in the detailed report include:

- Rising Demand for High-Mix, Low-Volume Production

- Supply-Chain Diversification Away from Mainland China

- Energy-Cost Volatility Affecting SMT Lines

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The segment held 42.73% of Malaysia electronics manufacturing services market share in 2025, anchored by PCB assembly for smartphones and industrial controls. Electromechanical assembly is forecast to expand at a 9.86% CAGR, powered by battery-management systems and wire-harness builds for electric vehicles. Malaysia's electronic manufacturing services market for box build is projected to grow exponentially between 2026 and 2031, driven by OEM demand for design-to-delivery accountability.

Providers differentiate through certifications- ISO 13485 for medical, IATF 16949 for automotive- that command premium pricing. Prototyping, logistics, and test-and-development services remain strategic footholds, enabling lock-in during early design decisions. Commoditized PCB assembly faces pricing pressure as low-cost markets attract high-volume work, but Malaysia's quality frameworks defend niches in aerospace, industrial, and medical builds.

In 2025, contract manufacturing accounted for a significant 60.91% of total revenue. This highlights the dominant role of contract manufacturing in the electronic manufacturing services market. As clients increasingly prioritize single-source accountability to expedite product cycles, hybrid and turnkey arrangements are projected to grow at a robust 10.13% CAGR. These arrangements offer streamlined processes and reduced complexities, making them attractive to businesses aiming for faster time-to-market. The Malaysia electronics manufacturing services market, particularly in turnkey engagements, is poised for steady growth through 2031, capitalizing on suppliers' advantages in component procurement and their embedded design expertise.

Jabil's investment of MYR 1 billion (USD 0.25 billion) in its Penang campus underscores its strategy to harness not just assembly revenue, but also design fees and logistics income. This significant investment reflects the company's commitment to expanding its capabilities and capturing a larger share of the value chain. The Penang campus is expected to serve as a hub for innovation and operational efficiency, further strengthening Jabil's market position. While Original Design Manufacturing (ODM) commands a smaller segment, it's gaining momentum, especially among brands venturing into wearables or smart-home categories that lack in-house engineering capabilities. This growth in ODM highlights the increasing demand for specialized design and manufacturing solutions in emerging product categories.

List of Companies Covered in this Report:

- Flex Ltd.

- Jabil Inc.

- Celestica Inc.

- Sanmina Corporation

- Plexus Corp

- Venture Corporation Ltd.

- Benchmark Electronics Inc.

- VS Industry Berhad

- NationGate Holdings Berhad

- Integrated Manufacturing Solutions Sdn Bhd

- SKP Resources Berhad

- EG Industries Berhad

- ATA IMS Berhad

- PIE Industrial Berhad

- Mi Technovation Berhad

- Inari Amertron Berhad

- Cape EMS Bhd

- Scanfil Plc

- Wistron Corporation

- Universal Scientific Industrial Co. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Foreign Direct Investments in Penang's EMS Corridor

- 4.2.2 Expansion of 5G Handset Exports from Malaysia

- 4.2.3 Rising Demand for High-Mix, Low-Volume (HMLV) Production

- 4.2.4 Government Incentives Under National Investment Aspirations (NIA)

- 4.2.5 Supply-Chain Diversification Away from Mainland China

- 4.2.6 Emergence of Smart Factory 4.0 Adoption Among Tier-2 EMS

- 4.3 Market Restraints

- 4.3.1 Skilled Labour Shortages in Advanced Packaging

- 4.3.2 Energy-Cost Volatility Affecting SMT Lines

- 4.3.3 Currency Fluctuation Risk Versus USD-Denominated Components

- 4.3.4 Intensifying Regional Competition from Vietnam & Thailand

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Types

- 5.1.1 Electronic Manufacturing Services

- 5.1.1.1 PCB Assembly

- 5.1.1.2 Electromechanical Assembly/Box Build

- 5.1.1.3 Prototyping

- 5.1.1.4 Other Electronic Manufacturing Services

- 5.1.2 Engineering Services

- 5.1.3 Test and Development Implementation

- 5.1.4 Logistics Services

- 5.1.5 Other Service Types

- 5.1.1 Electronic Manufacturing Services

- 5.2 By Business Model

- 5.2.1 Contract Manufacturing (CM)

- 5.2.2 Original Design Manufacturing (ODM)

- 5.2.3 Hybrid / Turnkey / Other Business Models

- 5.3 By Manufacturing Process

- 5.3.1 Surface Mount Technology (SMT)

- 5.3.2 Through-Hole Technology (THT)

- 5.3.3 Advanced Packaging / Hybrid Processes

- 5.4 By End-User

- 5.4.1 Mobile Devices (Smartphones and Tablets)

- 5.4.2 Consumer Electronics

- 5.4.3 Computer (PCs / Desktops / Laptops)

- 5.4.4 Industrial

- 5.4.5 Automotive

- 5.4.6 Communication

- 5.4.7 Lighting

- 5.4.8 Medical

- 5.4.9 Other End-Users

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Flex Ltd.

- 6.4.2 Jabil Inc.

- 6.4.3 Celestica Inc.

- 6.4.4 Sanmina Corporation

- 6.4.5 Plexus Corp

- 6.4.6 Venture Corporation Ltd.

- 6.4.7 Benchmark Electronics Inc.

- 6.4.8 VS Industry Berhad

- 6.4.9 NationGate Holdings Berhad

- 6.4.10 Integrated Manufacturing Solutions Sdn Bhd

- 6.4.11 SKP Resources Berhad

- 6.4.12 EG Industries Berhad

- 6.4.13 ATA IMS Berhad

- 6.4.14 PIE Industrial Berhad

- 6.4.15 Mi Technovation Berhad

- 6.4.16 Inari Amertron Berhad

- 6.4.17 Cape EMS Bhd

- 6.4.18 Scanfil Plc

- 6.4.19 Wistron Corporation

- 6.4.20 Universal Scientific Industrial Co. Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

電子製造服務市場:2026-2032年全球市場預測(依服務類型、技術、組件類型、最終用戶產業及企業規模分類)

電子製造服務市場:2026-2032年全球市場預測(依服務類型、技術、組件類型、最終用戶產業及企業規模分類) 電子設備電子製造服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031)

電子設備電子製造服務:市場佔有率分析、產業趨勢與統計、成長預測(2026-2031) 專業電子代工服務 (EMS) 市場:按服務、產品類型、經營模式、最終用途、國家和地區分類 - 全球產業分析、市場規模與佔有率及未來預測 (2026-2033)電子製造服務市場:依服務、經營模式、製造流程、最終用戶、國家及地區分類-全球產業分析、市場規模、市場佔有率及2026年至2033年預測

專業電子代工服務 (EMS) 市場:按服務、產品類型、經營模式、最終用途、國家和地區分類 - 全球產業分析、市場規模與佔有率及未來預測 (2026-2033)電子製造服務市場:依服務、經營模式、製造流程、最終用戶、國家及地區分類-全球產業分析、市場規模、市場佔有率及2026年至2033年預測 電子受託製造服務市場預測至2034年-按服務類型、經營模式、製造形式、最終用戶產業和地區分類的全球分析

電子受託製造服務市場預測至2034年-按服務類型、經營模式、製造形式、最終用戶產業和地區分類的全球分析 全球電訊設備受託製造服務(EMS)市場。

全球電訊設備受託製造服務(EMS)市場。 通訊電子製造服務市場:全球產業規模、佔有率、趨勢、機會和預測(按服務、應用和地區分類)、競爭格局(2021-2031 年)

通訊電子製造服務市場:全球產業規模、佔有率、趨勢、機會和預測(按服務、應用和地區分類)、競爭格局(2021-2031 年) 綠色電子製造市場規模、佔有率和成長分析:按製造流程、產品類型、最終用途產業和地區分類-2026-2033年產業預測

綠色電子製造市場規模、佔有率和成長分析:按製造流程、產品類型、最終用途產業和地區分類-2026-2033年產業預測 2026-2030年全球電子製造服務市場

2026-2030年全球電子製造服務市場 全球電子製造服務市場規模、佔有率、趨勢和成長分析報告(2026-2034年)

全球電子製造服務市場規模、佔有率、趨勢和成長分析報告(2026-2034年)